Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

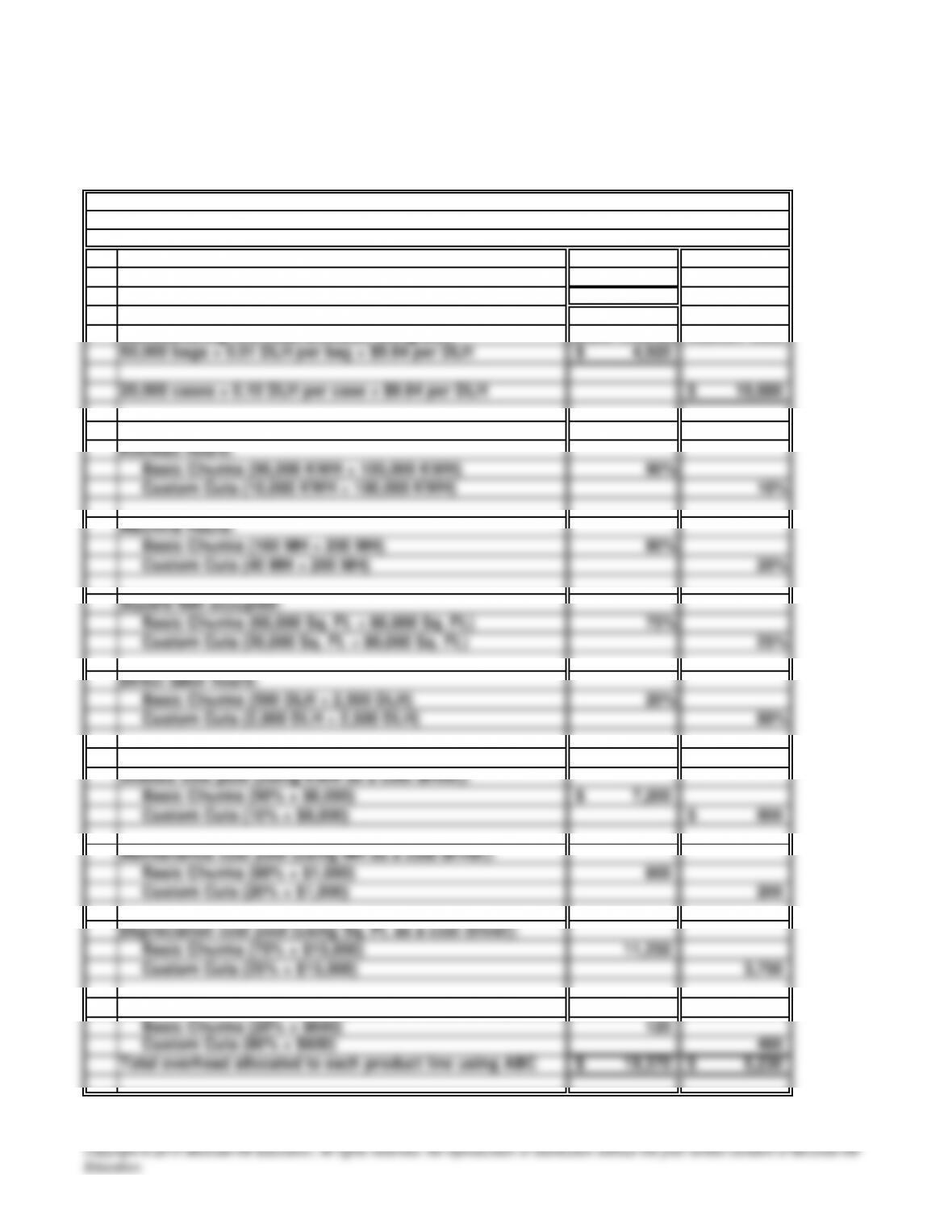

45 Minutes, Strong PROBLEM 17.8

A

HEALTHY HOUND, INC.

a. Budgeted manufacturing overhead 24,600$

Budgeted direct labor hours (DLH) ÷ 2,500

Manufacturing overhead application rate 9.84$ per DLH

Manufacturing overhead allocated using DLH Basic Chunks Custom Cuts

b. Percent of cost driver assigned to each product line Basic Chunks Custom Cuts

Manufacturing overhead allocated using ABC Basic Chunks Custom Cuts

Miscellaneous cost pool (using DLH as a cost driver):

PROBLEM 17.8

A

HEALTHY HOUND, INC. (concluded)

c. Total manufacturing costs allocated to each product line Basic Chunks Custom Cuts

d.

e.

The Custom Cuts product line is very labor intensive in comparison to the Basic Chunks

product line. Thus, the company’s current practice of using direct labor hours to allocate

The benefits the company would achieve by implementing an activity-based costing system

include: (1) a better identification of its operating inefficiencies, (2) a better understanding

SOLUTIONS TO PROBLEMS SET B

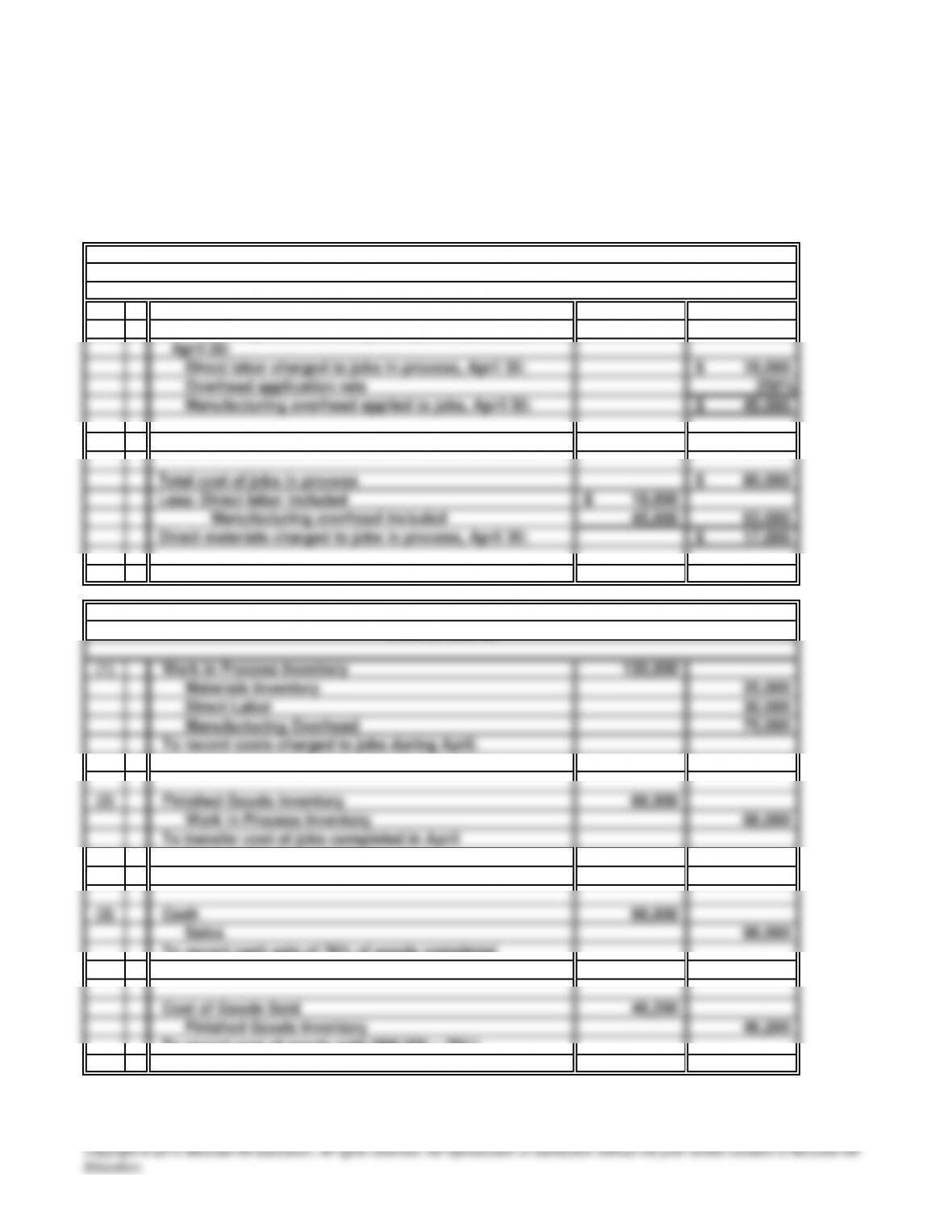

20 Minutes, Easy PROBLEM 17.1B

WINONA ENTERPRISES

a.

Manufacturing overhead charged to jobs in process,

Direct materials charged to jobs in process, April 30:

b.

to Finished Goods Inventory

.

To record cash sale of 70% of goods completed

in April.

To record cost of goods sold ($66,000 × 70%).

General Journal

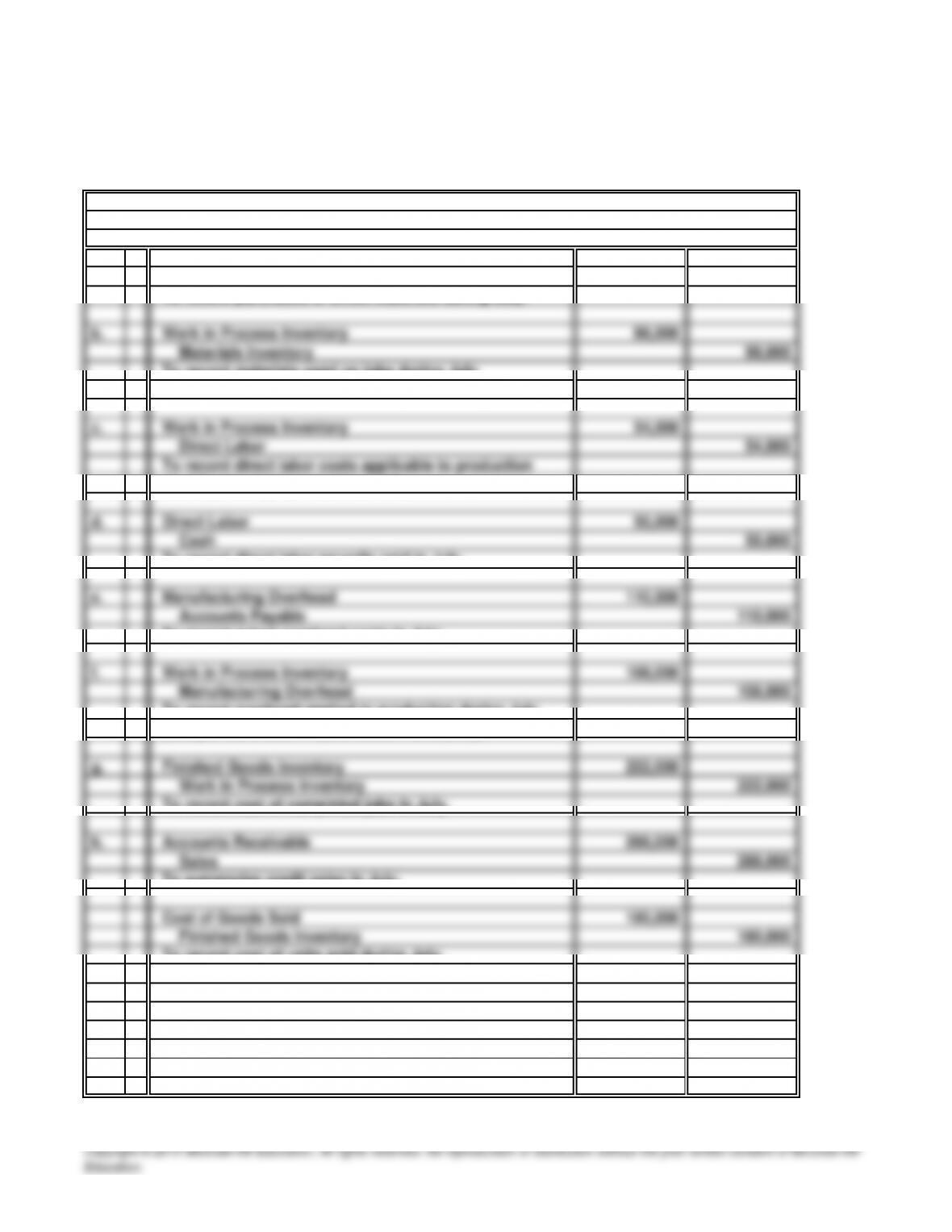

15 Minutes, Easy PROBLEM 17.2B

FARGO DEVELOPMENT CO.

General Journal

a. Materials Inventor

y

100,000

Accounts Payabl

e

100,000

To record purchases of direct materials during July.

To record materials used on jobs during Jul

y

per materials requisitions.

in July per employees’ time cards.

To record direct labor payrolls paid in July.

To record actual overhead costs in July.

To record overhead applied to production during Jul

y

($60 per labor hour × 1,800 hours = $108,000).

To record cost of completed jobs in July.

To summarize credit sales in July.

To record cost of units sold during July.

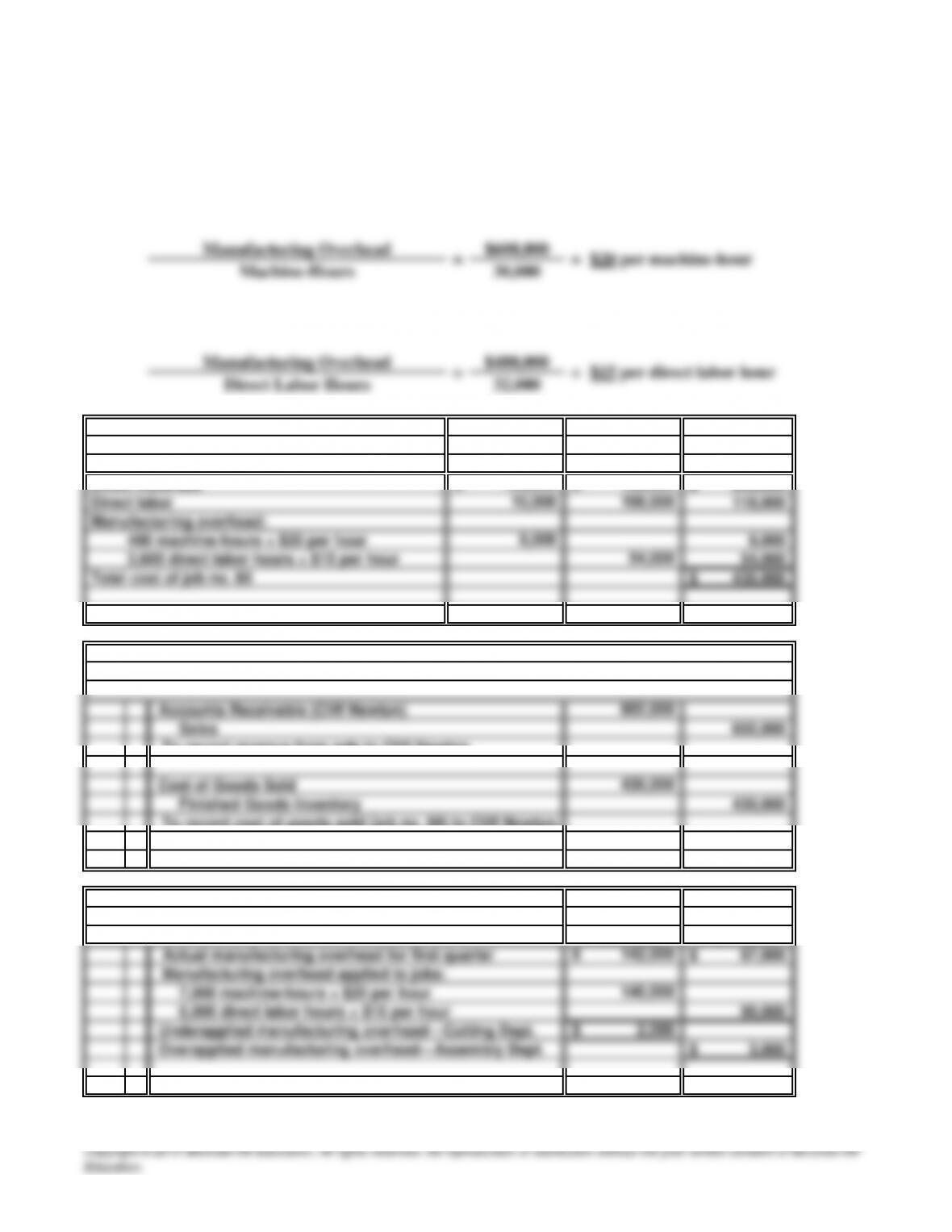

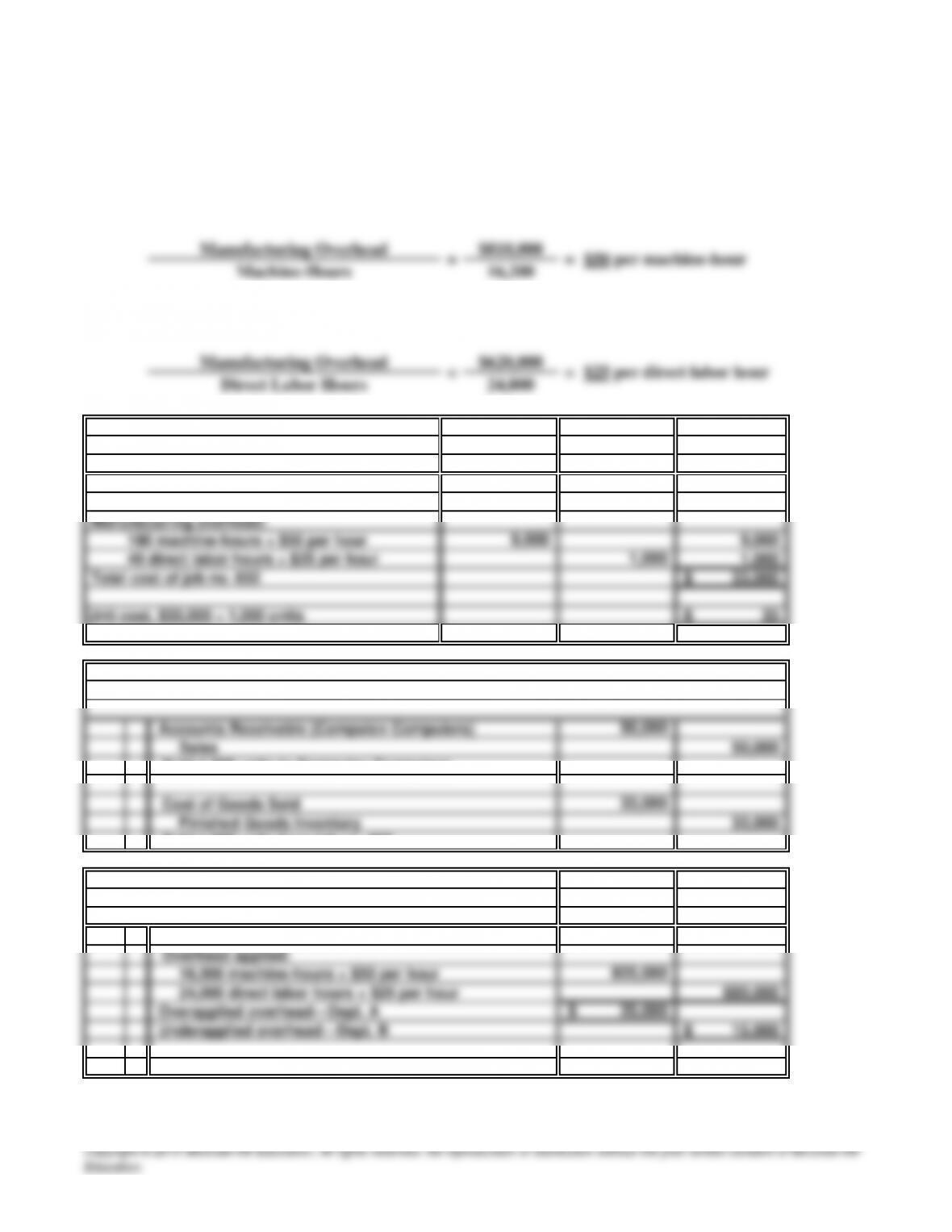

30 Minutes, Medium PROBLEM 17.3B

LINCOLN ESTATES

a. Cutting Department overhead application rate based on machine-hours:

Assembly Department overhead application rate based on direct labor hours:

b. Job no. 80

Total

Direct materials 250,000$

To record revenue from sale to Cliff Newton.

To record cost of goods sold (job no. 80) to Cliff Newton.

d. Assembl

y

Departmen

t

Assembly

150,000$

Department Department

100,000$ 10,000

Cutting

Cutting

Department

30 Minutes, Medium PROBLEM 17.4B

MONARK ELECTRONICS

a. Department A overhead application rate:

b. Job no. 652

Total

Direct materials 20,750$

Direct labor 2,250

c. General Journal

Sold 1,000 units to Computex Computers.

Sold 1,000 units from job no. 652.

d.

Dept. B

Actual overhead for the yea

r

615,000$

Overhead applied:

Dept. A

19,000$ 1,750$

1,500

750

Dept. B

800,000$

Dept. A

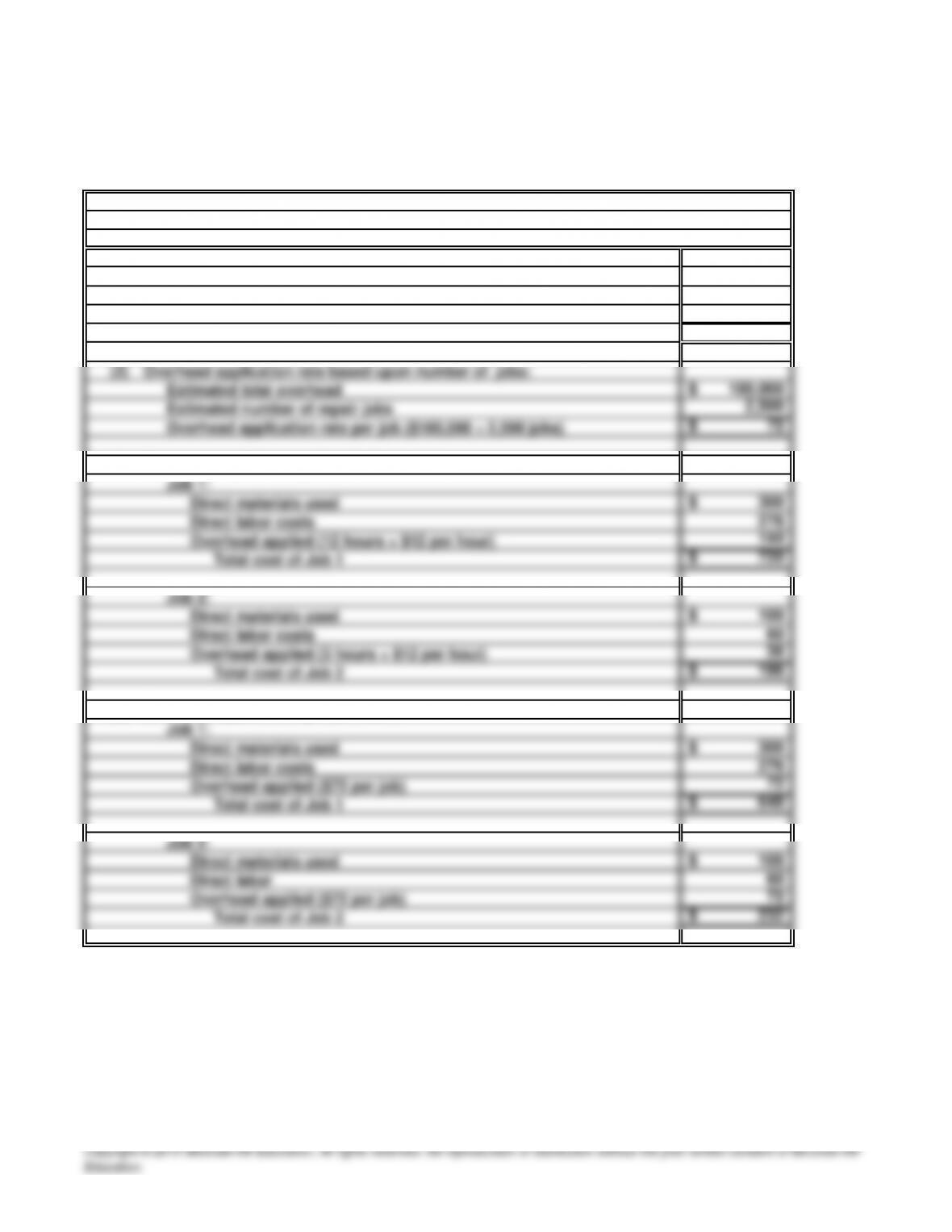

35 Minutes, Medium PROBLEM 17.5B

BIG BOOMERS

a.

(

1

)

180,000$ 15,000

12$

b.

(

1

)

(

2

)

300$

276 72

Total cost of Job 1 648$

100$ 60 72

Total cost of Job 2 232$

Overhead applied ($72 per job)

Overhead applied ($72 per job)

Job 2:

Direct materials used

Direct labor

Direct labor costs

Overhead application rate per job ($180,000 ÷ 2,500 jobs)

Overhead applied on a per-job basis:

Job 1:

Overhead applied using direct labor hours:

Job 1:

Direct materials used

Estimated number of repair jobs

Overhead application rate based on direct labor hours:

Estimated total overhead

Estimated direct labor hours

($180,000 ÷ 15,000 hours)

Overhead application rate per direct labor hour

PROBLEM 17.5B

BIG BOOMERS (concluded)

c.

Allocating overhead based upon the number of jobs assumes that each job should be

charged with an equal amount ($72) of overhead. This allocation method ignores the fact

Comments on the alternative overhead applications:

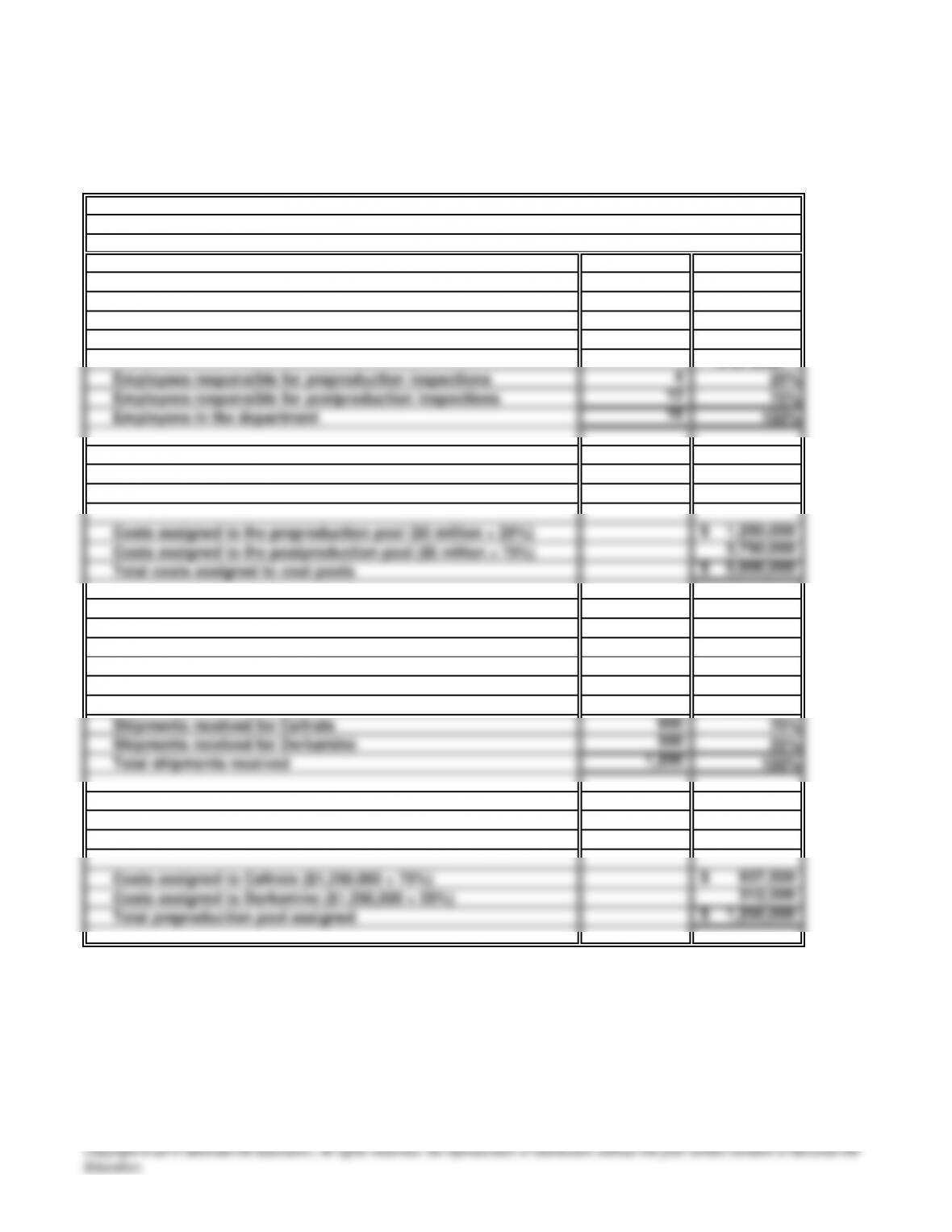

30 Minutes, Medium PROBLEM 17.6B

LOGAN PHARMACEUTICA

L

a.

% of total

312,500

1,250,000

$

Costs assigned to Dorkamine ($1,250,000 × 25%)

Total preproduction pool assigned

Assigning quality control department costs to activity pools:

Step 1:

Establish the percent of the department’s costs

to be assigned to each activity cost pool using the

number of employees as an activity base.

PROBLEM 17.6B

LOGAN PHARMACEUTICAL (concluded

)

c.

% of total

d. The company should consider reassigning its inspectors so that more time and effort is spent

inspecting shipments of Dorkamine materials. If relatively few problems are associated with

the material used to make Caltrate, time currently spent inspecting Caltrate materials

would be better spent inspecting the Dorkamine materials. Moreover, if inferior raw

materials are identified before being placed into production, fewer postproduction

inspectors may be needed. In short, the company should (1) conduct more frequent and

careful inspections of Dorkamine materials, and (2) reassign inspectors from

postproduction responsibilities to preproduction responsibilities.

Allocation of postproduction cost pool:

Step 1: Establish the percent of the pool to be allocated

to each product line using the number of batches

produced as an activity base.