Ex. 17.8

(continued

)

d.

Ex. 17.9 a. 1/5 Materials Inventory ………………………

…

800,000

1/14 Work in Process Inventory ………………

…

200,000

Materials Inventory ……………………. 200,000

Used direct materials on job no. 1002.

1/18 Work in Process Inventory ………………

…

100,000

Materials Inventory ……………………. 100,000

…

1/27 Work in Process Inventory ………………

…

258,750

Manufacturing Overhead ………….…… 258,750

1/28 Finished Goods Inventory ……………………

…

884,000

Work in Process Inventory ……………… 884,000

Applied direct labor to jobs: job no. 1001,

$3,600; job no. 1002, $5,400; job no. 1003,

$1,350.

Applied overhead to jobs: job no. 1001,

$90,000; job no. 1002, $135,000; job no.

1003, $33,750.

Manufacturing overhead applied to jobs totaled $75,000. Actual

manufacturing overhead costs totaled $78,000. Thus, overhead was

underapplied by $3,000. This amount was closed to Cost of Goods Sold on

December 31 (see part a).

…

Sales ………………………………………… 725,000

Sold job no. 1001 on account.

Cost of Goods Sold ……………………………

…

543,600

Finished Goods Inventory …………………. 543,600

Record cost of job no. 1001.

Cost of Goods Sold ..……………………… 8,750

b. Cost of Goods Sold (unadjusted) ……………………………………….. 543,600$

Overapplied overhead …………………………………………………… (8,750)

.

Beginning Work in Process Inventory …………………………………

…

$ 0

Direct materials for jobs 1001, 1002, & 1003 ………………………….. 750,000

Direct labor for jobs 1001, 1002, & 1003 ……………………………….

.

10,350

Overhead applied to jobs 1001, 1002, & 1003 …………………………. 258,750

Cost of jobs 1001 & 1002 transferred …………………………………

…

(884,000)

Work in Process Inventory, January 31 ………………………………

…

135,100$

Beginning Finished Goods Inventory …………………………………

…

$ 0

Cost of completed jobs 1001 & 1002 …………………………………… 884,000

Cost of job no. 1001 sold ………………………………………………… (543,600)

Finished Goods Inventory, January 31 …………………………………

.

340,400$

Closed overapplied manufacturing overhead

($258,750 applied – $250,000 actual).

d. Manufacturing overhead applied to jobs totaled $258,750. Actual

Ex. 17.10 a. Materials Inventory …….………………………………. 125,000

Accounts Payable ………………………………. 125,000

b. Work in Process Inventory ………..……………………. 100,000

Materials Inventory ………………………………. 100,000

Cash ………………………………………………. 150,000

To record actual overhead costs incurred.

e. Work in Process Inventory ………..…………………… 140,000

Manufacturing Overhead ………………………… 140,000

To apply overhead to jobs in December.

f. Accounts Receivable …………..………………………… 600,000

Sales ………………………………………………. 600,000

To record December sales on account.

Cost of Goods Sold ………..……………………………

…

325,000

Finished Goods Inventory ………………………. 325,000

To record the purchase of direct materials on account.

(continued) Manufacturing Overhead ……………………… 10,000

i. Sales ………………………………………………………………………. 600,000$

Cost of Goods Sold ($325,000 + $10,000) ……………………………. 335,000

Ex. 17.11 a. Actual manufacturing overhead ………………………………………… 200,000$

Debit balance in Manufacturing Overhead account ………………… (40,000)

Manufacturing overhead applied ………………………………………

…

160,000$

b. $160,000 overhead applied ÷ 5,000 DLH ………………………………. $32 per DLH

c. $176,000 budgeted overhead ÷ $32 application rate ………………… 5,500 DLH

Direct labor rate …………………………………………………………

…

$22 per hour

e. Beginning Work in Process Inventory …………………………………. 50,000$

Total manufacturing costs charged to production ……………………. 590,000

Ending Work in Process Inventory …………………………………….. (40,000)

Costs transferred to finished goods ……………………………………. 600,000$

Cost of Goods Sold ($580,000 + $40,000) ……………………………… 620,000

Gross Profit ………………………………………………………………. 900,000$

Selling and Administrative Expenses ………………………………….. 700,000

Net Income ……………………………………………………………….. 200,000$

To close underapplied manufacturing overhead

($150,000 actual – $140,000 applied).

Ex. 17.12 a. Beginning Materials Inventory ……………………………………

…

16,000$

Direct labor incurred ………………………………………………… 190,000

Manufacturing overhead applied …………………………………… 285,000 2

Costs transferred to finished goods …………………………………. (420,000) 3

Work in Process Inventory lost in the fire ………………………….

.

193,000$

c. Beginning Finished Goods Inventory ……………………………….

.

30,000$

Ex. 17.13 a. Work in Process Inventory:

Job no. 1000 …………………………………………………………

…

12,400$

Job no. 1001 …………………………………………………………

…

15,000

Work in Process Inventory, February 28 …………………………

…

27,400$

…

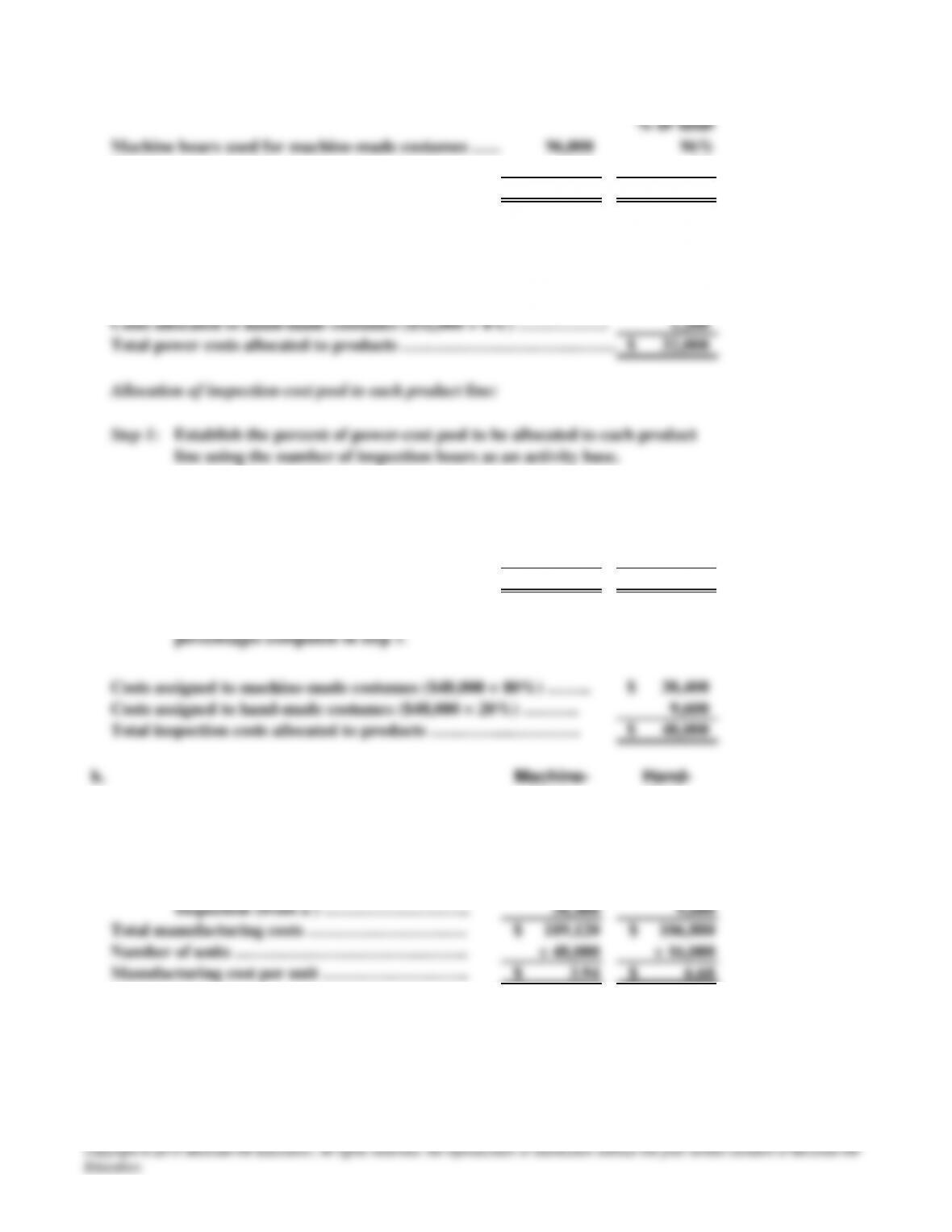

Ex. 17.14 a.

Power-cost pool: Machine hours

Inspection-cost pool: Number of inspection hours

The most likely cost drivers for each cost pool are:

Thus, the amount of total manufacturing overhead cost assigned to each pool is

computed as follows:

…

Machine hours used for hand-made costumes……….

.

4,000 4%

Total machine hours ………………………………….. 100,000 100%

Step 2:

Costs allocated to machine-made costumes ($32,000 × 96%) ………. 30,720$

% of total

Ins

p

ection hours for machine-made costumes ………

.

2,000 80%

Inspection hours for hand-made costumes …………. 500 20%

Total inspection hours ………………………………

…

2,500 100%

Step 2:

Allocate $32,000 in power-cost pool to each product line based on the

percentages computed in step 1.

Allocate $48,000 in inspection-cost pool to each product line based on the

Ex. 17.14

(continued) c. Machine-

Made

Costumes Hand-Made

Costumes

$ 240,000 $ 160,000

Less: 120,000 96,000

$ 1.06 $ 3.32

Ex. 17.15 a. Direct materials ……………………………………………………

…

$ 14,000

Direct labor …………………………………………………………

…

15,000

Maintenance ($40,000 × 60/600 machine hours) …………………

…

4,000

Materials handling ($20,000 × 20/400 moves) ……………………

…

1,000

…

…

b. Bid price: $34,700 × 175% = $60,725

Profitability per unit ………………………………

Direct labor and materials

Sales

SOLUTIONS TO PROBLEMS SET

A

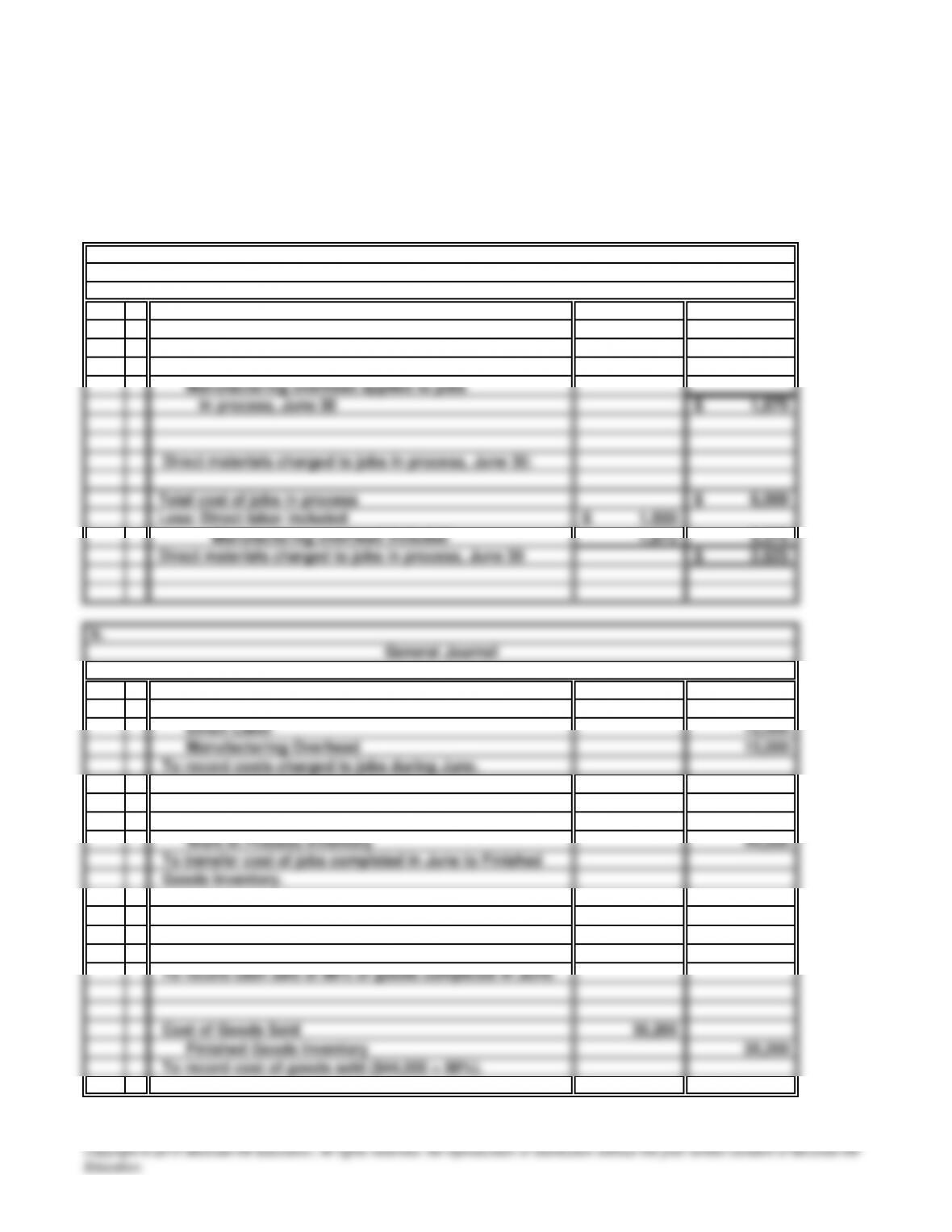

20 Minutes, Easy PROBLEM 17.1

A

JENSEN FENCES

a.

Manufacturing overhead charged to jobs in process,

June 30:

Direct labor charged to jobs in process, June 30 1,500$

Overhead application rate 125%

(1) Work in Process Inventor

y

45,000

Materials Inventor

y

18,000

(2) Finished Goods Inventor

y

44,000

y

(3) Cash 50,000

Sales 50,000

General Journal