Chapter 17 – Job Order Cost Systems and Overhead Allocations

Financial and Managerial Accounting, 17/e 17-1

17 JOB ORDER COST SYSTEMS

AND OVERHEAD ALLOCATIONS

Chapter Summary

Cost accounting systems are typically designed to accommodate the specific needs

of individual companies. In this chapter, we demonstrate a widely used accounting

system for measuring and tracking resource consumption: job order costing. Job order

costing is a method for tracking resource consumption directly to individual services and

products.

Job order costing is typically used by companies that tailor their goods or services

to the specific needs of individual customers. In job order costing, the costs of direct

materials, direct labor, and overhead are accumulated separately for each job. This

chapter provides a detailed introduction to job order costing. Job-order costing is shown

to be a reasonable approach to assigning manufacturing costs to distinct units of

production such as buildings, batches of furniture, financial audits, etc. When the units

produced are all of a similar type, the complexity of job costing is unnecessary and

process cost systems are an efficient alternative. Process cost systems are introduced in

Chapter 18.

Modern manufacturing firms produce a wide variety of products. These diverse

products sometimes place very different demands on a company’s productive resources.

Under such circumstances, the broad cost averaging characteristic of job-order and

process cost systems can produce significant cost distortions. Activity based cost systems

are offered as an alternative. These systems differ from traditional approaches in the way

that they assign indirect costs to pools before applying them to products. In so doing,

ABC systems better capture the relationships between products and the resources they

consume.

Learning Objectives

1. Explain the purposes of cost accounting systems.

2. Identify the processes for creating goods and services that are suited to job order

costing.

3. Explain the purpose and computation of overhead application rates for job order

costing.

4. Describe the purpose and the content of a job cost sheet.

5. Account for the flow of costs when using job order costing.

6. Define overhead-related activity cost pools and provide several examples.

Chapter 17 – Job Order Cost Systems and Overhead Allocations

7. Demonstrate how activity bases are used to assign activity cost pools to units

produced.

Brief topical outline

A Cost accounting systems

1 Job order cost systems and the creation of goods and services

2 Overhead application rates

a Computation and use of overhead application rates ‒

see Your Turn (page 763)

3 What “drives” overhead costs?

a The use of multiple overhead application rates

b The increasing importance of proper overhead allocation

B Job order costing

1 The job cost sheet

2 Flow of costs in job costing: an illustration

3 Accounting for direct materials – see Case in Point (page 766)

4 Accounting for direct labor costs

5 Accounting for overhead costs

a Application of overhead costs to jobs

b Over- or underapplied overhead – see Your Turn (page 770)

6 Accounting for completed jobs

7 Job order costing in service industries

C Activity-based costing (ABC) ‒ see Case in Point (page 771)

1 How ABC works

2 The benefits of ABC

3 ABC versus a single application rate: a comparison

4 Stage 1: separate activity cost pools

a Maintenance department costs

b Assigning maintenance department costs to activity pools

c Utilities costs

d Assigning utilities costs to activity pools

5 Stage 2: Allocate activity cost pools to the products

a Allocation of repair cost pool to each product line

b Allocation of set-up cost pool to each product line

c Allocation of heating cost pool to each product line

d Allocation of machinery cost pool to each product line

6 Determining unit costs using ABC

D The trend toward more informative cost accounting systems – see Ethics,

Fraud & Corporate Governance (page 779)

E Concluding remarks

Chapter 17 – Job Order Cost Systems and Overhead Allocations

Financial and Managerial Accounting, 17/e 17-3

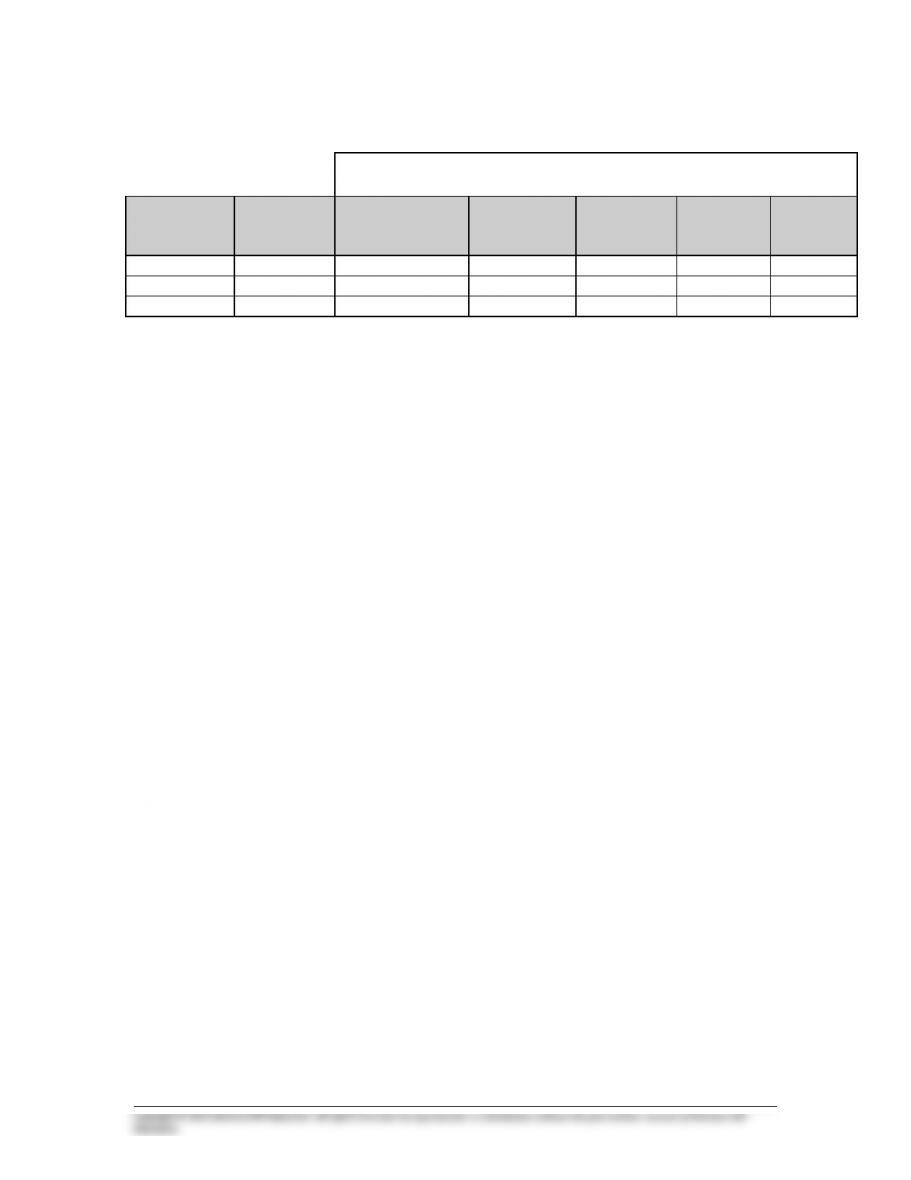

Topical coverage and suggested assignment

Homework Assignment

(To Be Completed Prior to Class)

Class

Meetings on

Chapter

Topical

Outline

Coverage

Discussion

Questions

Brief

Exercises

Exercises

Problems

Critical

Thinking

Cases

1

A – B

1, 3, 4

5

1, 3

2

1

2

B – C

6, 7

1, 2, 4

4, 6

5

3

C – E

13, 14, 15

8, 9, 10

9, 14, 15

8

2

Comments and observations

Teaching objectives for Chapter 17

In this chapter, the concepts of product costing are illustrated in a job order cost

accounting system. Our primary objectives in presenting cost accounting systems are to:

1 Explain the basic purposes of cost accounting systems, with emphasis upon the

usefulness of unit cost data.

2 Illustrate the determination of the cost of finished goods manufactured, and of unit

costs, in a job order cost system. Emphasize that costs are accumulated separately for

each “job”.

4 Explain why an overhead application rate is needed to assign a reasonable amount of

overhead costs as jobs are completed.

5 Discuss the potential for cost distortions arising from the use of volume-based activity

bases when applying overhead to diverse multiple products.

6 Demonstrate the use of multiple activity cost pools and activity bases in determining

unit costs.

Chapter 17 – Job Order Cost Systems and Overhead Allocations

General comments

We find that the introduction of the “flow” of manufacturing costs in Chapter 16 greatly

enhances students’ abilities to understand the determination and use of unit costs.

We caution against placing too much emphasis upon the format of cost accounting

schedules, such as job cost sheets. The format of these schedules will vary significantly

from one business entity to the next. Most students, of course, will never have to actually

prepare such schedules in their professional career. On the other hand, they should be able

to locate and interpret the important elements of the schedules

notably the cost of

finished goods manufactured and unit costs.

We stress that the flow of costs in a job order cost system parallels the flow of

manufacturing costs introduced in the preceding chapter. Also, we emphasize those

characteristics of a company‘s production activities that make job order costing more

appropriate. Exercises 4 and 5 are intended to serve this purpose. Students generally have

little difficulty in understanding job order cost accounting systems. Thus, we include the

quite comprehensive Problem 3 in our second assignment. (This problem also addresses

the issue of over- or underapplied overhead.)

Activity based costing has become central to the development of modern cost

systems. We emphasize to students that traditional job-order and process costing systems

were not designed for a diverse multiple product environment. It is relatively easy to

illustrate the potential for cost distortion resulting from the use of a single volume-based

cost driver such as labor hours. Problem 7 has been designed with this purpose in mind

and we highly recommend covering it in class.

An aside In some instances real-world cost accounting systems have become simpler

than our treatment suggests. Harley-Davidson no longer records direct labor as a separate

cost element. Direct labor costs are included with total plant overhead. Furthermore,

overhead is not added to inventory as in-process parts are produced. Instead, overhead is

applied only when a finished unit is completed.

Supplemental Exercises

Group Exercise

Job-order costing is used by many service businesses as well as by manufacturers.

The system when used in any organization requires a substantial amount of record

keeping and documentation and can thus be very costly to maintain. Interview a

representative of a local CPA or law firm to determine how professionals in the firm

maintain their time records. Does the information that the system produces seem to

justify its cost? Prepare a presentation to the class based on your findings.

Chapter 17 – Job Order Cost Systems and Overhead Allocations

Financial and Managerial Accounting, 17/e 17-5

CHAPTER 17 NAME #

10-MINUTE QUIZ A SECTION

Indicate the best answer for each question in the space provided.

1 In a job order cost system, the sum of debits to the Work in Process controlling

account during a particular period is equal to each of the following except:

a The total of debits to the Materials Inventory, Direct Labor, and

Manufacturing Overhead accounts during the period.

b The total of direct materials, direct labor, and manufacturing overhead

costs applied to jobs during the period.

c The total of amounts entered on job cost sheets during the period.

d The total of credits to the Materials Inventory, Direct Labor, and

Manufacturing Overhead accounts during the period.

2 The Work in Process controlling account of a manufacturing firm shows a debit

balance of $5,000 at the end of an accounting period. The job cost sheet of the

two uncompleted jobs shows charges of $700 and $1,300 for materials used and

charges of $400 and $600 for direct labor used. From this information, it appears

that the company is using a predetermined factory overhead rate (as a percentage

of direct labor cost) of:

a 100%. b 200%. c 33%. d 50%.

3 The use of activity–based costing is most appropriate for:

a Firms that manufacture multiple product lines.

b Firms that have very low manufacturing overhead costs relative to other

costs of production.

c Firms with high levels of production activity.

d Firms that account separately for product and period costs.

Chapter 17 – Job Order Cost Systems and Overhead Allocations

CHAPTER 17 NAME

#________

10-MINUTE QUIZ B SECTION

The information below is taken from the job cost sheets of O’Leary Company:

Job Number

Manufacturing Costs

as of Oct. 31

Manufacturing

Costs in November

350

$10,955

351

$8,810

352

$2,375

$5,593

353

$6,522

$10,279

354

$2,128

$5,573

355

$3,987

During November, job numbers 352 and 353 were completed and job numbers 350, 351 and

352 were delivered to customers. Jobs nos. 354 and 355 are still in process at November 30.

From this information, compute the following:

1 What is the work in process inventory at October 31? $__________

2 What is the finished goods inventory at October 31? $__________

3 What is the cost of goods sold during November? $__________

4 What is the work in process at November 30? $__________

5 What is the finished goods inventory at November 30? $__________

Chapter 17 – Job Order Cost Systems and Overhead Allocations

Financial and Managerial Accounting, 17/e 17-7

SOLUTIONS TO CHAPTER 17 10-MINUTE QUIZZES

QUIZ A

QUIZ B

1

Job 352 = $2,375 as of October 31

Job 353 = $6,522 as of October 31

Job 354 = $2,128 as of October 31

Total = $11,025

Chapter 17 – Job Order Cost Systems and Overhead Allocations

Assignment Guide to Chapter 17

Brief Exercises

Exercises

Problems

Cases

Net

1 – 10

1 – 15

1

2

3

4

5

6

7

8

1

2

3

4

Time estimate (in minutes)

< 15

< 15

40

40

25

30

25

40

30

40

35

10

25

30

Difficulty rating

E

E

M

M

M

S

E

M

M

S

M

E

M

M

Learning Objectives:

5

1, 2, 3

√

√

√

√

√

√

√

√

1. Explain the purposes of cost

accounting systems.

2. Identify the processes for creating

goods and services that are suited to

job order costing.

5

1, 2, 3, 5

√

√

√

√

√

√

√

3. Explain the purpose and

computation of overhead

application rates for job order

costing.

3, 4

1, 2, 3, 4, 6,

7, 8, 9, 10,

11, 12, 13

√

√

√

√

√

4. Describe the purpose and the

content of a job cost sheet.

1, 2, 3, 6, 7,

8, 9, 10, 11,

12, 13

√

√

√

√

√

5. Account for the flow of costs when

using job order costing.

1, 2, 4, 6, 7, 8

2, 3, 6, 7, 8,

9, 10, 11, 12,

13

√

√

√

√

√

6. Define overhead-related activity cost

pools and provide several examples.

9, 10

1, 4, 14, 15

√

√

7. Demonstrate how activity bases are

used to assign activity cost pools to

units produced.

1, 14, 15

√

√

√

√

√

√