Ethics Challenge — BTN 9-3

1. It is in Bly’s self-interest to maximize the amount of revenues less

warranty expenses so as to maximize his personal bonus. Since Bly

2. Although Bly might be able to affect the amount of revenues less

warranty expenses via the warranty expense accrual in the short run,

over several years the amounts should even out. The dealership

should probably adjust the warranty expense accrual to match the

usual (average) experience over time. Given the variable nature of

1. McDonald’s 2013 current liabilities include the following:

Accounts payable

2. The portion of long-term debt maturing in the next 12 months ($

millions) is:

3. Times interest earned for McDonald’s as of 12/31/2013

($ millions)

12/31/2013

Net Income ……………………………………………………...

$ 5,586.0

Plus income taxes …………………………………………...

2,618.6

Plus interest expense ……………………………………….

521.9

Income before interest and taxes ……………………..

$ 8,726.5

Times interest earned ……………………………………...

16.72 times

Comment: The 16.72 times interest earned ratio seems more than

sufficient for McDonald’s to cover its interest obligations, and it is

higher than the industry average of 15.0.

1. Option A: Interest Expense = $6,000 x 10% x 90/360 = $150

Option B: Interest Expense = $6,000 x 8% x 120/360 = $160

2. Entries:

2a. Issue date, Option A

June 1

Cash …………………………………………………………….….

6,000

Notes Payable …………………………………………….

6,000

Borrowed cash by issuing an

interest-bearing note.

6,000

Notes Payable …………………………………………….

6,000

Borrowed cash by issuing an

6,000

Interest Expense …………………………………………..….

6,150

6,000

©2016 by McGraw–Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in

any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

Solutions Manual, Chapter 9

555

Teamwork in Action (Concluded)

4. Entries:

4a. Adjusting entry, Option A (Dec. 31)

Dec. 31

Interest Expense …………………………………………..….

50

Interest Payable ………………………………………….

50

Accrue interest on note

payable [$6,000 x 10% x 30/360].

4b. Adjusting entry, Option B (Dec. 31)

Dec. 31

Interest Expense …………………………………………..….

40

Interest Payable ………………………………………….

40

Accrue interest on note payable

[$6,000 x 8% x 30/360].

4c. Maturity date entry, Option A

March 1

Interest Expense …………………………………………..….

100

Interest Payable ……………………………………………….

50

Notes Payable ………………………………………………….

6,000

Cash ……………………………………………………….

6,150

Repaid note plus interest.

4d. Maturity date entry, Option B

March 31

Interest Expense …………………………………………..….

120

Interest Payable ……………………………………………….

40

Notes Payable ………………………………………………….

6,000

Cash ……………………………………………………….

6,160

Repaid note plus interest.

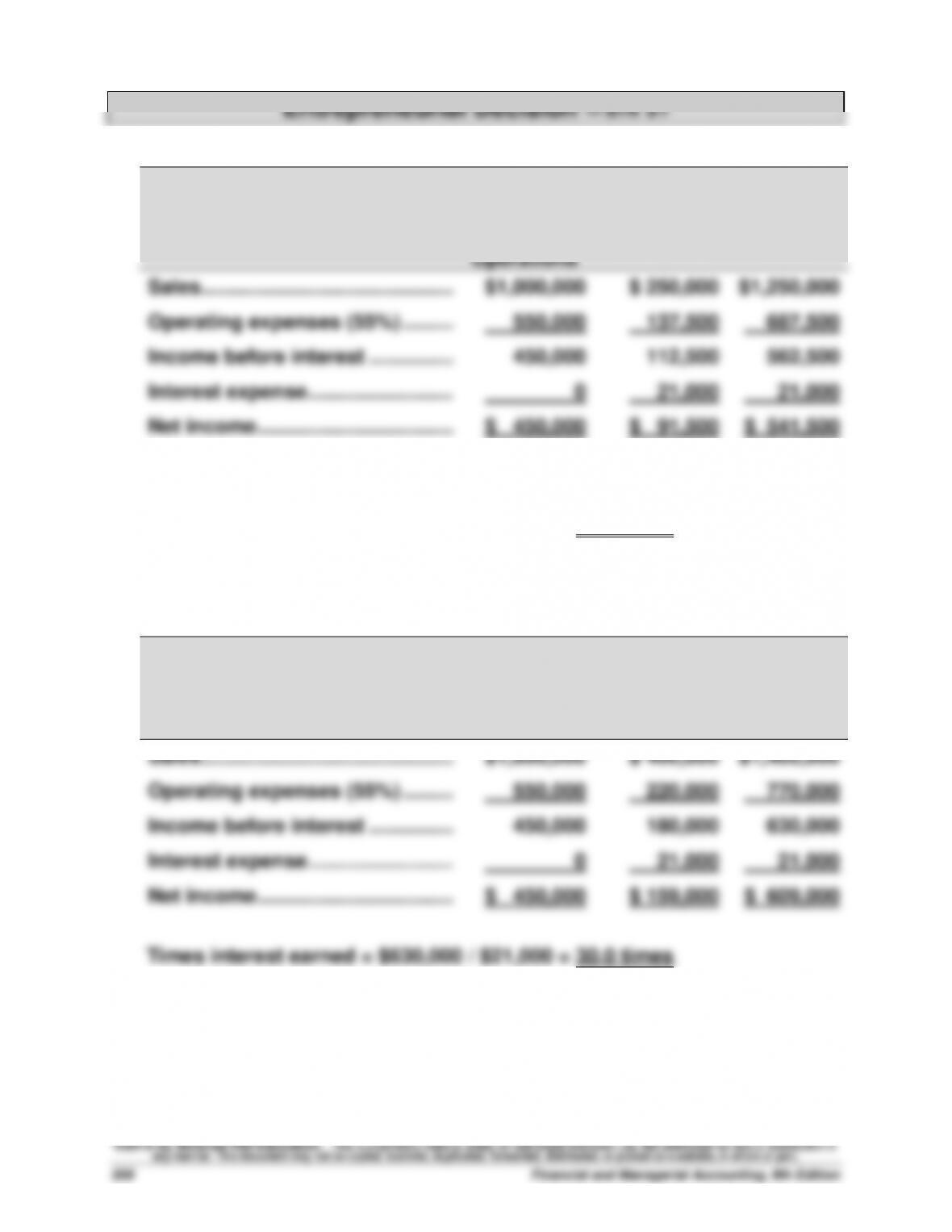

1.

Uncharted Play

Income Statement (Prospective)

Current

Operations

European

Total

Sales ………………………………………

$1,000,000

$ 250,000

$1,250,000

Operating expenses (55%) ………

550,000

137,500

687,500

Income before interest ……………

450,000

112,500

562,500

Interest expense ……………………..

0

21,000

21,000

Net income …………………………..…

$ 450,000

$ 91,500

$ 541,500

2. Times interest earned = $562,500 / $21,000 = 26.8 times

3.

Uncharted Play

Income Statement (Prospective)

Current

Operations

European

Total

Sales …………………………..………….

$1,000,000

$ 400,000

$1,400,000

Operating expenses (55%) ………

550,000

220,000

770,000

Income before interest ……………

450,000

180,000

630,000

Interest expense ……………………..

0

21,000

21,000

Net income …………………………..…

$ 450,000

$ 159,000

$ 609,000

Times interest earned = $630,000 / $21,000 = 30.0 times

©2016 by McGraw–Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in

any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

Solutions Manual, Chapter 9

557

Entrepreneurial Decision (concluded)

4.

Uncharted Play

Income Statement (Prospective)

Current

Operations

European

Total

Sales …………………………..………….

$1,000,000

$ 100,000

$1,100,000

Operating expenses (55%) ………

550,000

55,000

605,000

Income before interest ……………

450,000

45,000

495,000

Interest expense ……………………..

0

21,000

21,000

Net income …………………………..…

$ 450,000

$ 24,000

$ 474,000

Times interest earned = $495,000 / $21,000 = 23.6 times

5. In each of these cases, the company’s times interest earned is at least

23.6, so it appears that if it takes out the loan and can generate at least

$100,000 in sales in Europe, then the company will have little trouble

paying its interest expense.

1. Samsung— Times interest earned

(KRW in millions)

Current Year

Prior Year

Net income …………………………………..……..

₩ 30,474,764

₩ 23,845,285

Add income taxes …………………………..

7,889,515

6,069,732

Income before income taxes ………………..

38,364,279

29,915,017

Add interest expense* …………………..……..

7,754,972

7,934,450

Income before taxes and interest ….……..

₩ 46,119,251

₩ 37,849,467

Times interest earned ratio …………………..

5.95a

4.77b

* Interest expense is labeled “Finance expense” on Samsung’s consolidated statements of income.

a 46,119,251 / 7,754,972

b 37,849,467 / 7,934,450

2. Of these three companies, Apple and Google both have superior

coverage of interest expense for the two years analyzed. Specifically,