Problem 8-5B (40 minutes)

2014

Jan. 1

Machinery ……………………………………………………….

114,270

Cash ………………………………………………………….…..

114,270

To record costs of machinery ($107,800 +$6,470).

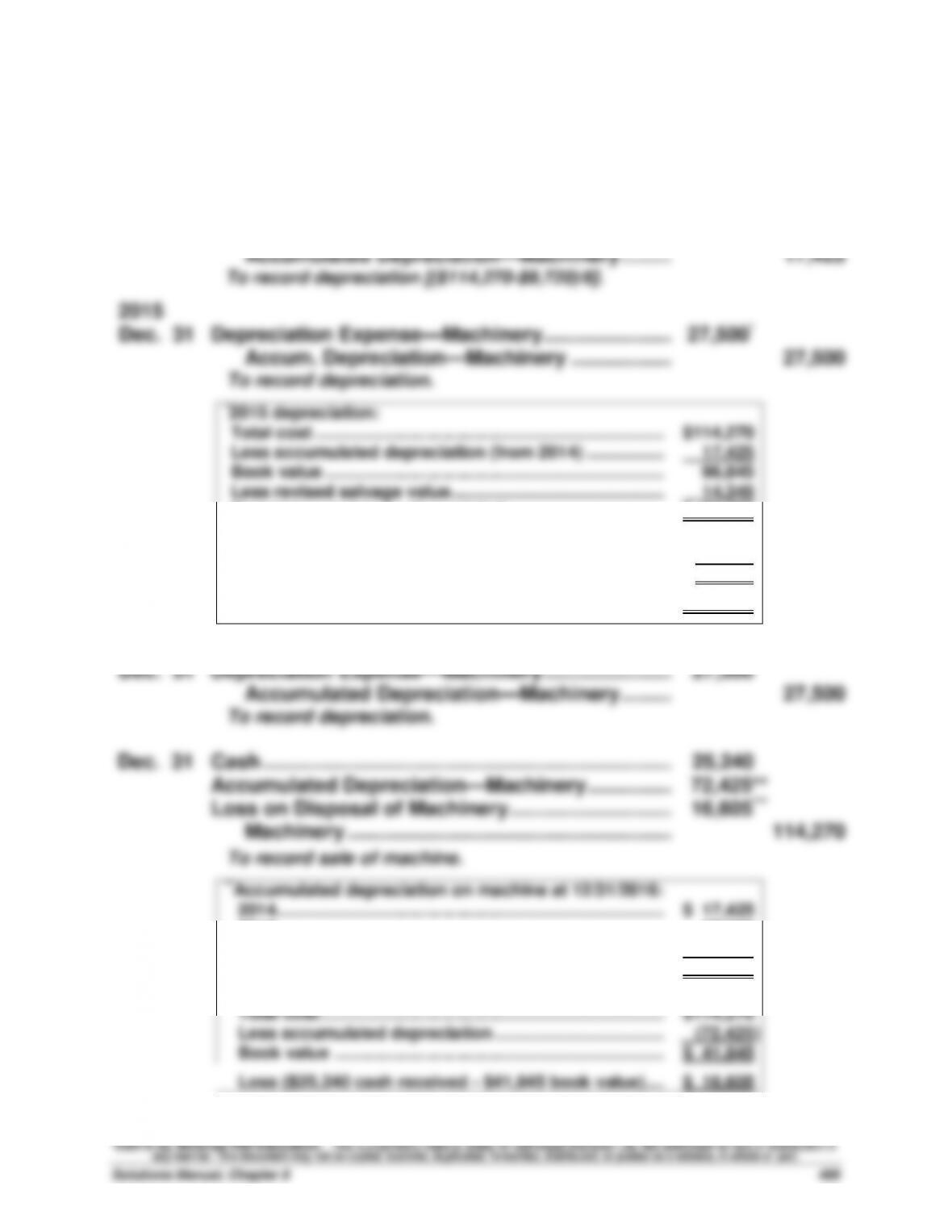

Dec. 31

Depreciation Expense—Machinery …………………..…..

17,425

Accumulated Depreciation—Machinery …………..

17,425

To record depreciation [($114,270-$9,720)/6].

2015

Dec. 31

Depreciation Expense—Machinery …………………..…..

27,500*

Accum. Depreciation—Machinery …………………..

27,500

To record depreciation.

*2015 depreciation:

Total cost ………………………………………………………………………..

$114,270

Less accumulated depreciation (from 2014) …………….………..

17,425

Book value …………………………………………………………….………..

96,845

Less revised salvage value ……………………………………..………..

14,345

Remaining cost to be depreciated……………………………………..

$ 82,500

Revised useful life ………………………………………………….……

4 yrs.

Less 1 year in 2014 ……………………………………………………….

1 yrs.

Revised remaining useful life ………………………………….………..

3 yrs.

Total depreciation for 2015 ($82,500/ 3 yrs) ……………….………..

$ 27,500

2016

Dec. 31

Depreciation Expense—Machinery …………………..…..

27,500

Accumulated Depreciation—Machinery …………..

27,500

To record depreciation.

Dec. 31

Cash ……………………………………………………………….…..

25,240

Accumulated Depreciation—Machinery ………………..

72,425**

Loss on Disposal of Machinery ………………………..…

16,605***

Machinery …………………………..……………………..…..

114,270

To record sale of machine.

**Accumulated depreciation on machine at 12/31/2016:

2014 ……………………………………………………………………...

$ 17,425

2015 ……………………………………………………………………...

27,500

2016 ……………………………………………………………………...

27,500

Total ……………………………………………………………………..

$ 72,425

***Book value of machine at 12/31/2016:

Total cost …………………………..………………………………….

$114,270

Less accumulated depreciation ……………………………...

(72,425)

Book value …………………………………………………………...

$ 41,845

Loss ($25,240 cash received – $41,845 book value)…..

$ 16,605

Problem 8-6B (20 minutes)

1.

Jan. 1

Machinery …………………………..…………………………….

150,000

Cash …………………………..……………………………….

150,000

To record machinery costs.

Jan. 2

Machinery …………………………..…………………………….

3,510

Cash …………………………..……………………………….

3,510

To record machinery costs.

Jan. 4

Machinery …………………………..…………………………….

4,600

Cash …………………………..……………………………….

4,600

To record machinery costs.

2. a. First year

Dec. 31

Depreciation Expense—Machinery ……………………….

20,000

Accumulated Depreciation—Machinery ……….….

20,000

To record depreciation [($158,110-$18,110)/7 = $20,000].

b. Sixth year

Dec. 31

Depreciation Expense—Machinery ……………………….

20,000

Accumulated Depreciation—Machinery ……….….

20,000

To record the sixth year’s depreciation.

3. Accumulated depreciation at the date of disposal

First six years’ depreciation (6 x $20,000) ………………...

$120,000

Book value at the date of disposal

Original total cost …………………………………………………...

$158,110

Accumulated depreciation ……………………………………....

(120,000)

Total ……………………………………………………………………....

$ 38,110

a. Sold for $28,000 cash

Dec. 31

Cash ……………………………………………………………….…..

28,000

Loss on Sale of Machinery …………………………………..

10,110

Accumulated Depreciation—Machinery ………………..

120,000

Machinery …………………………..……………………..…..

158,110

Dec. 31

Cash ……………………………………………………………….…..

52,000

120,000

Machinery …………………………..……………………..…..

158,110

Loss from Fire ……………………………………………………..

13,110

120,000

Problem 8-7B (20 minutes)

a.

Feb. 19

Mineral Deposit …………………………..……………..………..

5,400,000

Cash …………………………………………………….…

5,400,000

To record purchase of mineral deposit.

b.

Mar. 21

Machinery ………………………………………………….……

400,000

Cash …………………………………………………….…

400,000

To record costs of machinery.

c.

Dec. 31

Depletion Expense—Mineral Deposit ………….………..

342,900

Accum. Depletion—Mineral Deposit ………………..

342,900

To record depletion [$5,400,000/

4,000,000 tons = $1.35 per ton.

254,000 tons x $1.35 = $342,900].

d.

Dec. 31

Depreciation Expense—Machinery ……………..………..

25,400

Accum. Depreciation—Machinery …………………..

25,400

To record depreciation [$400,000/

4,000,000 tons = $0.10 per ton.

254,000 tons x $0.10 = $25,400].

Analysis Component

Similarities—Amortization, depletion, and depreciation are similar in that

they are all methods of allocating costs of long-term assets to the periods

that benefit from their use.

Differences—They are different in that they apply to different types of long–

term assets: amortization applies to intangible assets (with definite useful

lives); depletion applies to natural resources; and depreciation applies to

plant assets. Also, amortization is typically computed using the straight–

line method, whereas the units–of-production method is routinely used in

depletion.

Problem 8-8B (20 minutes)

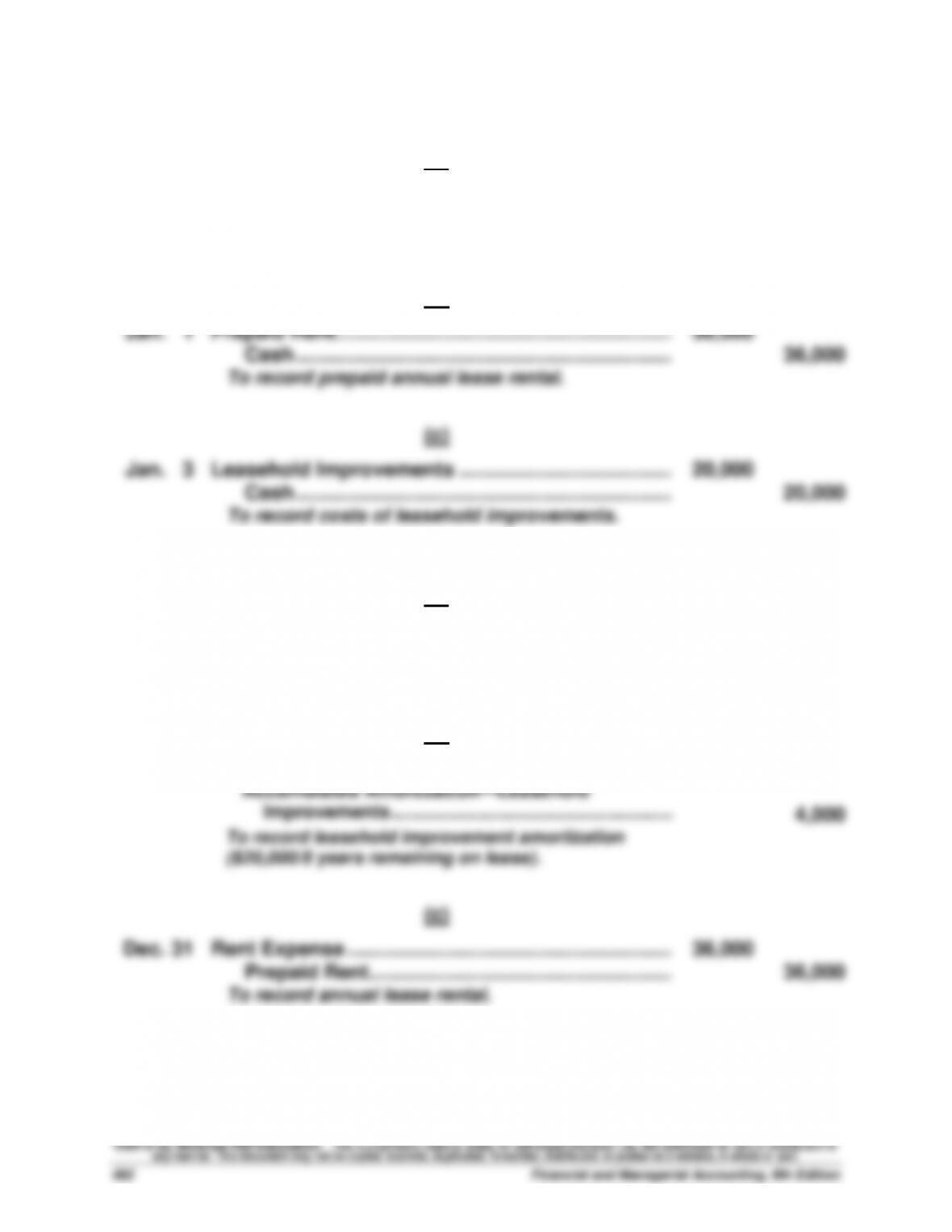

1.

2015

(a)

Jan. 1

Leasehold ……………………………………………………….

40,000

Cash ………………………………………………………….…..

40,000

To record payment for sublease.

(b)

Jan. 1

Prepaid Rent……………………………………………………….

36,000

Cash ………………………………………………………….…..

36,000

To record prepaid annual lease rental.

(c)

Jan. 3

Leasehold Improvements ………………………………..…..

20,000

Cash ………………………………………………………….…..

20,000

To record costs of leasehold improvements.

2.

2015

(a)

Dec. 31

Rent Expense ………………………………………………….…..

8,000

Accumulated Amortization—Leasehold …………..

8,000

To record leasehold amortization ($40,000/5).

(b)

Dec. 31

Amortization Expense—Leasehold Improvements ….…..

4,000

Accumulated Amortization—Leasehold

Improvements …………………………………………………..

4,000

To record leasehold improvement amortization

($20,000/5 years remaining on lease).

(c)

Dec. 31

Rent Expense ………………………………………………….…..

36,000

Prepaid Rent…………………………………………………..

36,000

To record annual lease rental.

©2016 by McGraw–Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in

any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

Solutions Manual, Chapter 8

493

Serial Problem — SP 8

Serial Problem — SP 8, Business Solutions (45 minutes)

1. For the three months ended March 31, 2016, depreciation expense was

$400 for office equipment and $1,250 for the computer equipment.

2.

December 31,

2015

December 31,

2016

Office Equipment …………………………….……

$ 8,000

$ 8,000

Accumulated Depreciation–Office

Equipment ………………………………….……

400

2,000

Office Equipment (book value) ………..……

$ 7,600

$ 6,000

December 31,

2015

December 31,

2016

Computer Equipment …………………………..

$20,000

$20,000

Accumulated Depreciation–

Computer Equipment ………………………

1,250

6,250

Computer Equipment (book value)…..……

$18,750

$13,750

3.

Total asset turnover = Net sales / Average total assets

The 3-month total asset turnover at March 31, 2016:

$44,000 / [($83,460 + $120,268)/2] = 0.43 times (rounded)

©2016 by McGraw–Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in

any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

Financial and Managerial Accounting, 6th Edition

494

Reporting in Action — BTN 8-1

1. The percent of original cost remaining to be depreciated is computed

by taking the ratio of the book value of property and equipment to the

2. In Apple’s “Summary of Significant Accounting Policies” (Note 1:

Property, Plant and Equipment) it discloses estimated useful lives by

3. The change in total property and equipment before accumulated

depreciation for the year ended September 28, 2013, is an increase of

$6,632 million ($28,519 – $21,887). In comparison, according to the

4. Total asset turnover for year ended ($ millions):

9/28/2013: = 0.89 times

$156,508

5. Solution depends on the financial statement data obtained.

$170,910

($207,000 + 176,064)/2

($176,064 + $116,371)/2

©2016 by McGraw–Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in

any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

Solutions Manual, Chapter 8

495

Comparative Analysis — BTN 8-2

Note: Total asset turnover = Net sales / Average total assets

1. Total asset turnover for Apple ($ millions)

Current Year: = 0.89 times

2. Each dollar of Apple’s assets produces $0.89 and $1.07 in net sales for

the current and prior year, respectively. Each dollar of Google’s assets

produces $0.58 and $0.60 in net sales for the current year and prior

$156,508

($93,798 + $72,574)/2

$170,910

($207,000 + 176,064)/2