Problem 8-3A (45 minutes)

Part 1

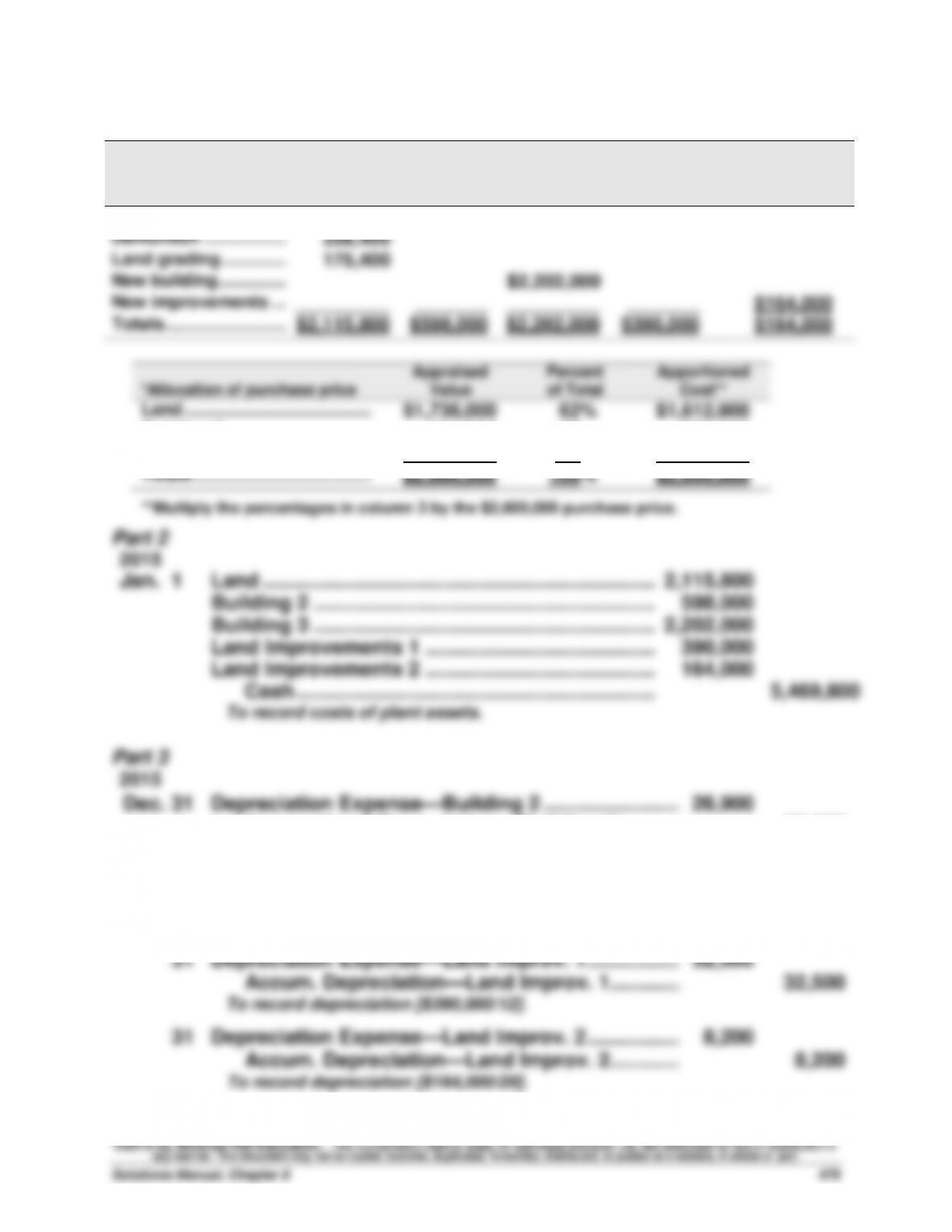

Land

Building

2

Building

3

Land

Improve-

ments 1

Land

Improvements

2

Purchase price* ……….………

$1,612,000

$598,000

$390,000

Demolition ………………………

328,400

Land grading …………..………

175,400

New building……………………

$2,202,000

New improvements ….………

_________

_______

_________

_______

$164,000

Totals ……………………..……

$2,115,800

$598,000

$2,202,000

$390,000

$164,000

*Allocation of purchase price

Appraised

Value

Percent

of Total

Apportioned

Cost**

Land …………………………………..

$1,736,000

62%

$1,612,000

Building 2 …………………………..

644,000

23

598,000

Land Improvements 1 ………....

420,000

15

390,000

Totals ………………………………...

$2,800,000

100%

$2,600,000

**Multiply the percentages in column 3 by the $2,600,000 purchase price.

Part 2

2015

Jan. 1

Land …………………………………………………………….

2,115,800

Building 2 …………………………………………………….

598,000

Building 3 …………………………………………………….

2,202,000

Land Improvements 1 …………………………………..

390,000

Land Improvements 2 …………………………………..

164,000

Cash ……………………………………………………….

5,469,800

To record costs of plant assets.

Part 3

2015

Dec. 31

Depreciation Expense—Building 2 …………………….…..

26,900

Accumulated Depreciation—Building 2 ………..…..

26,900

To record depreciation [($598,000 – $60,000)/20].

31

Depreciation Expense—Building 3 …………………….…..

72,400

Accumulated Depreciation—Building 3 ………..…..

72,400

To record depreciation [($2,202,000 – $392,000)/25].

31

Depreciation Expense—Land Improv. 1 ……………..…..

32,500

Accum. Depreciation—Land Improv. 1 ………….…..

32,500

To record depreciation [$390,000/12].

31

Depreciation Expense—Land Improv. 2 ……………..…..

Problem 8-4A (50 minutes)

2014

Jan. 1

Equipment ……………………………………………………....

300,600

Cash …………………………………………………………...

300,600

To record loader costs ($287,600 +$11,500 +$1,500).

Jan. 3

Equipment ……………………………………………………….

4,800

Cash ………………………………………………………….…..

4,800

To record betterment of loader.

Dec. 31

Depreciation Expense—Equipment ………………….…..

70,850*

Accumulated Depreciation—Equipment ……..…..

70,850

To record depreciation.

*2014 depreciation after January 3rd betterment

Total original cost ………………………………………………………….

$300,600

Plus cost of betterment ………………………………………………….

4,800

Revised cost of equipment ……………………………………………..

305,400

Less revised salvage ($20,600 + $1,400) …………………………

22,000

Cost to be depreciated ……………………………………………………

283,400

Annual depreciation ($283,400 / 4 years) ………………………….

$ 70,850

2015

Jan. 1

Equipment ……………………………………………………….

5,400

Cash ………………………………………………………….…..

5,400

To record extraordinary repair on loader.

Feb. 17

Repairs Expense—Equipment …………………………..

820

Cash ………………………………………………………….…..

820

To record ordinary repair on loader.

Dec. 31

Depreciation Expense—Equipment ………………….…..

43,590*

Accumulated Depreciation—Equipment ……..…..

43,590

To record depreciation.

*2015 depreciation after January 1st extraordinary repair

Total cost ($305,400 + $5,400) ……………………………………………………….

$310,800

Less accumulated depreciation …………………………..…………………………..

70,850

Book value …………………………………………………………………….……………..

239,950

Less salvage ………………………………………………………………….………………..

22,000

Remaining cost to be depreciated …………………………..…………………………..

$217,950

Revised remaining useful life (Original 4 years – 1yr. + 2yrs.) ..……………………….

5 yrs.

Revised annual depreciation ($217,950 / 5 yrs) …………………………..

$ 43,590

Problem 8-5A (40 minutes)

2014

Jan. 1

Trucks ………………………………………………………………...

22,000

Cash ……………………………………………………………...

22,000

To record cost of truck ($20,515 + $1,485).

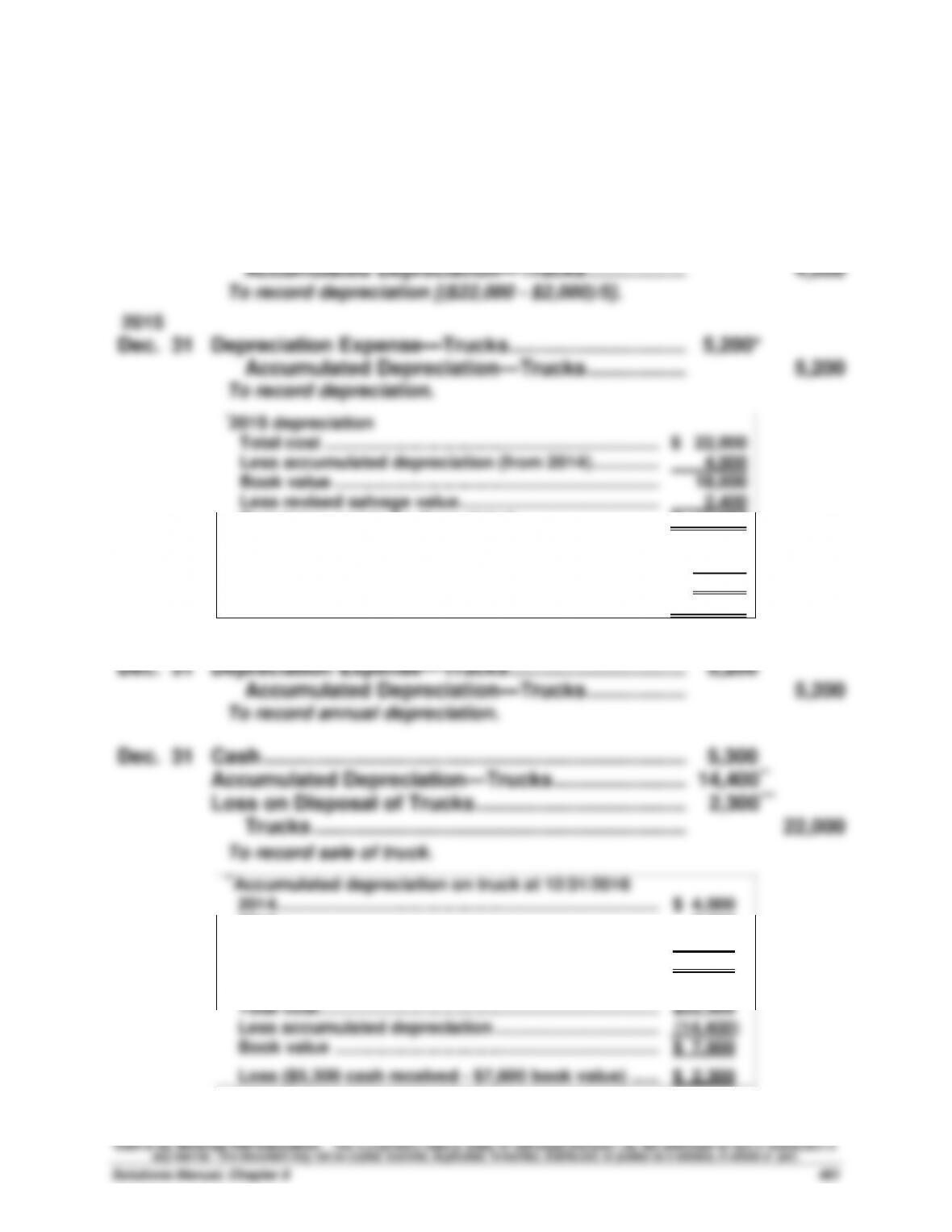

Dec. 31

Depreciation Expense—Trucks …………………………..

4,000

Accumulated Depreciation—Trucks ………………..

4,000

To record depreciation [($22,000 – $2,000)/5].

2015

Dec. 31

Depreciation Expense—Trucks …………………………..

5,200*

Accumulated Depreciation—Trucks ………………..

5,200

To record depreciation.

*2015 depreciation

Total cost ……………………………………………………………………………………

$ 22,000

Less accumulated depreciation (from 2014) …………..………………

4,000

Book value ………………………………………………………….………………………..

18,000

Less revised salvage value …………………………………..…………………..

2,400

Remaining cost to be depreciated …………………………..

$ 15,600

Revised useful life …………………………..…………………..………

4 yrs.

Less one year used in 2014 ………………………………….……………………

1 yrs.

Revised remaining useful life ……………………………….………………………

3 yrs.

Total depreciation for 2015 ($15,600/3) ………………….……….

$ 5,200

2016

Dec. 31

Depreciation Expense—Trucks …………………………..

5,200

Accumulated Depreciation—Trucks ………………..

5,200

To record annual depreciation.

Dec. 31

Cash …………………………………………………………………...

5,300

Accumulated Depreciation—Trucks ……………………..

14,400**

Loss on Disposal of Trucks ………………………………....

2,300***

Trucks …………………………………………………………...

22,000

To record sale of truck.

**Accumulated depreciation on truck at 12/31/2016

2014 ……………………………………………………………………...

$ 4,000

2015 ……………………………………………………………………...

5,200

2016 ……………………………………………………………………...

5,200

Total ……………………………………………………………………..

$14,400

***Book value of truck at 12/31/2016

Total cost ……………………………………………………………...

$22,000

Less accumulated depreciation ……………………………...

(14,400)

Book value …………………………………………………………...

$ 7,600

Loss ($5,300 cash received – $7,600 book value) ……..

$ 2,300

Problem 8-6A (20 minutes)

1.

Jan. 2

Machinery …………………………..…………………………..

178,000

Cash …………………………..……………………………...

178,000

To record machinery purchase.

Jan. 3

Machinery …………………………..…………………………..

2,840

Cash …………………………..……………………………...

2,840

To record machinery costs.

Jan. 3

Machinery …………………………..…………………………..

1,160

Cash …………………………..……………………………...

1,160

To record machinery costs.

2. a. First year

Dec. 31

Depreciation Expense—Machinery ………………….……

28,000

Accumulated Depreciation—Machinery ……..……

28,000

To record depreciation [($182,000 – $14,000)/6].

b. Fifth year

Dec. 31

Depreciation Expense—Machinery ………………….……

28,000

Accumulated Depreciation—Machinery ……..……

28,000

To record year’s depreciation.

3. Accumulated depreciation at the date of disposal

Five years’ depreciation (5 x $28,000) …………………....

$140,000

Book value at the date of disposal

Original total cost ………………………………………………...

$182,000

Accumulated depreciation …………………………………....

(140,000)

Book value …………………………………………………………..

$ 42,000

a. Sold for $15,000 cash

Dec. 31

Cash ……………………………………………………………..…….

15,000

Loss on Sale of Machinery …………………………….…….

27,000

Accumulated Depreciation—Machinery ………….…….

140,000

Machinery ……………………………………………………….

182,000

b. Sold for $50,000 cash

Dec. 31

Cash ……………………………………………………………..…….

50,000

Accumulated Depreciation—Machinery ………….…….

140,000

Machinery ……………………………………………………….

182,000

Gain on Sale of Machinery …………………………..

8,000

c. Destroyed in fire and collected $30,000 cash from insurance co.

Dec. 31

Cash ……………………………………………………………..…….

30,000

Accumulated Depreciation—Machinery ………….…….

140,000

Loss from Fire ……………………………………………….…….

12,000

Machinery ……………………………………………………….

182,000

Problem 8-7A (20 minutes)

a.

July 23

Mineral Deposit ……………………………………………………

4,715,000

Cash ……………………………………………………….

4,715,000

To record purchase of mineral deposit.

b.

July 25

Machinery ……………………………………………………….

410,000

Cash ……………………………………………………….

410,000

To record costs of machinery.

c.

Dec. 31

Depletion Expense—Mineral Deposit ……………………

441,600

Accum. Depletion—Mineral Deposit ……..…………

441,600

To record depletion [$4,715,000/

5,125,000 tons = $0.92 per ton.

480,000 tons x $0.92 = $441,600].

d.

Dec. 31

Depreciation Expense—Machinery …………….…………

38,400

Accum. Depreciation—Machinery ………..…………

38,400

To record depreciation [$410,000/

5,125,000 tons = $0.08 per ton.

480,000 tons x $0.08 = $38,400].

Analysis Component

Similarities—Amortization, depletion, and depreciation are similar in that

they are all methods of allocating costs of long-term assets to the periods

that benefit from their use.

Differences—They are different in that they apply to different types of long–

term assets: amortization applies to intangible assets with (definite) useful

lives; depletion applies to natural resources; and depreciation applies to

plant assets. Also, amortization is typically computed using the straight–

line method, whereas the units-of-production method is routinely used in

depletion.

Problem 8-8A (20 minutes)

1.

2015

(a)

June 25

Leasehold ……………………………………………………....

200,000

Cash ………………………………………………………..…….

200,000

To record payment for sublease.

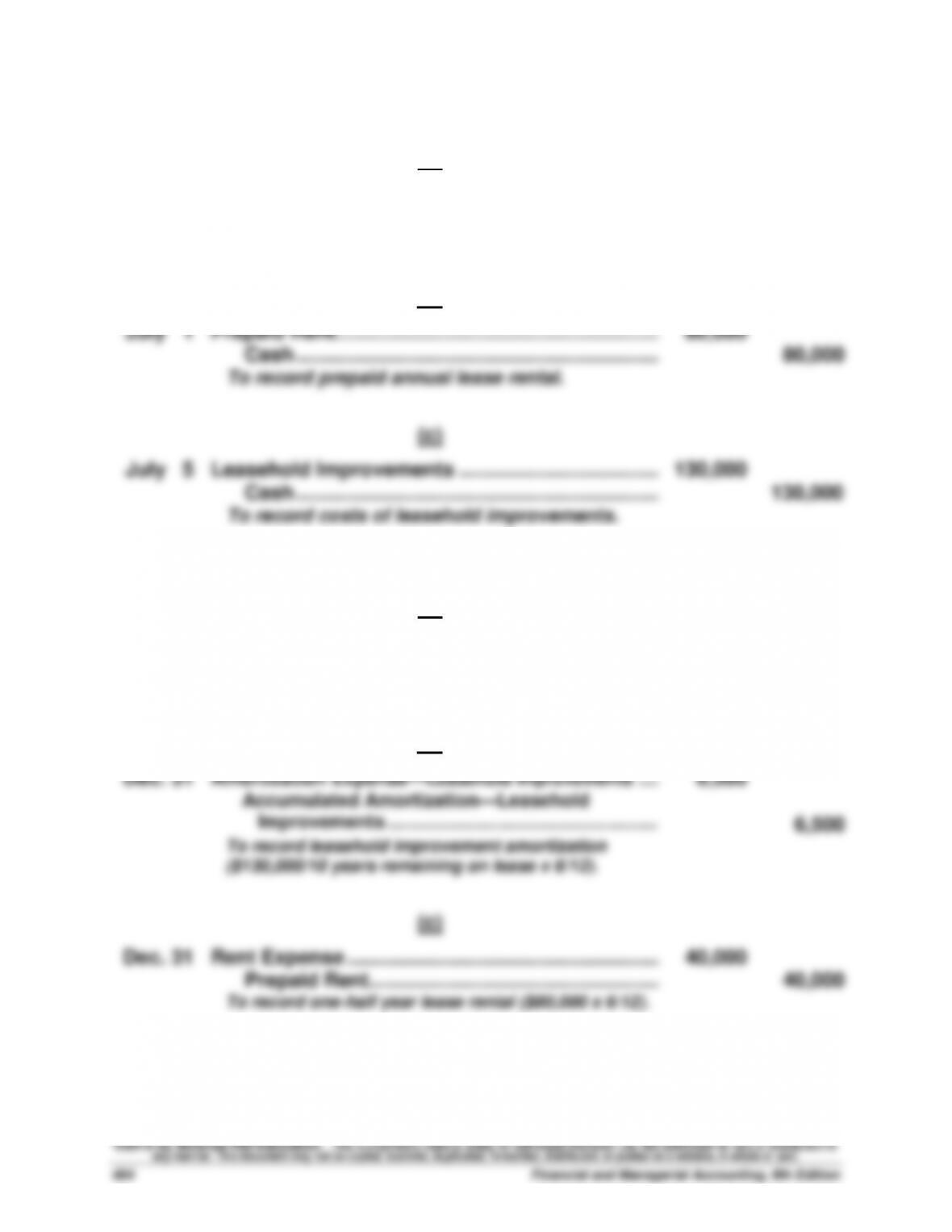

(b)

July 1

Prepaid Rent………………………………………………….……

80,000

Cash ………………………………………………………..…….

80,000

To record prepaid annual lease rental.

(c)

July 5

Leasehold Improvements …………………………………….

130,000

Cash ………………………………………………………..…….

130,000

To record costs of leasehold improvements.

2.

2015

(a)

Dec. 31

Rent Expense ………………………………………………..…….

10,000

Accumulated Amortization—Leasehold …….…….

10,000

To record leasehold amortization ($200,000/10 x 6/12).

(b)

Dec. 31

Amortization Expense—Leasehold Improvements ….…….

6,500

Accumulated Amortization—Leasehold

Improvements …………………………………………….……..

6,500

To record leasehold improvement amortization

($130,000/10 years remaining on lease x 6/12).

(c)

Dec. 31

Rent Expense ………………………………………………..…….

40,000

Prepaid Rent…………………………………………….…….

40,000

To record one-half year lease rental ($80,000 x 6/12).

Problem 8-1B (50 minutes)

Part 1

Estimated

Market Value

Percent

of Total

Apportioned

Cost

Building ……………………..

$ 890,000

50%

$ 900,000

Land …………………………..

427,200

24

432,000

Land improvements …...

249,200

14

252,000

Trucks ………………………..

213,600

12

216,000

Total …………………………..

$1,780,000

100%

$1,800,000

Problem 8-2B (25 minutes)

Cost of machine …………………………..

$324,000

Less estimated salvage value ……….………………….

30,000

Total depreciable cost ………………….……….

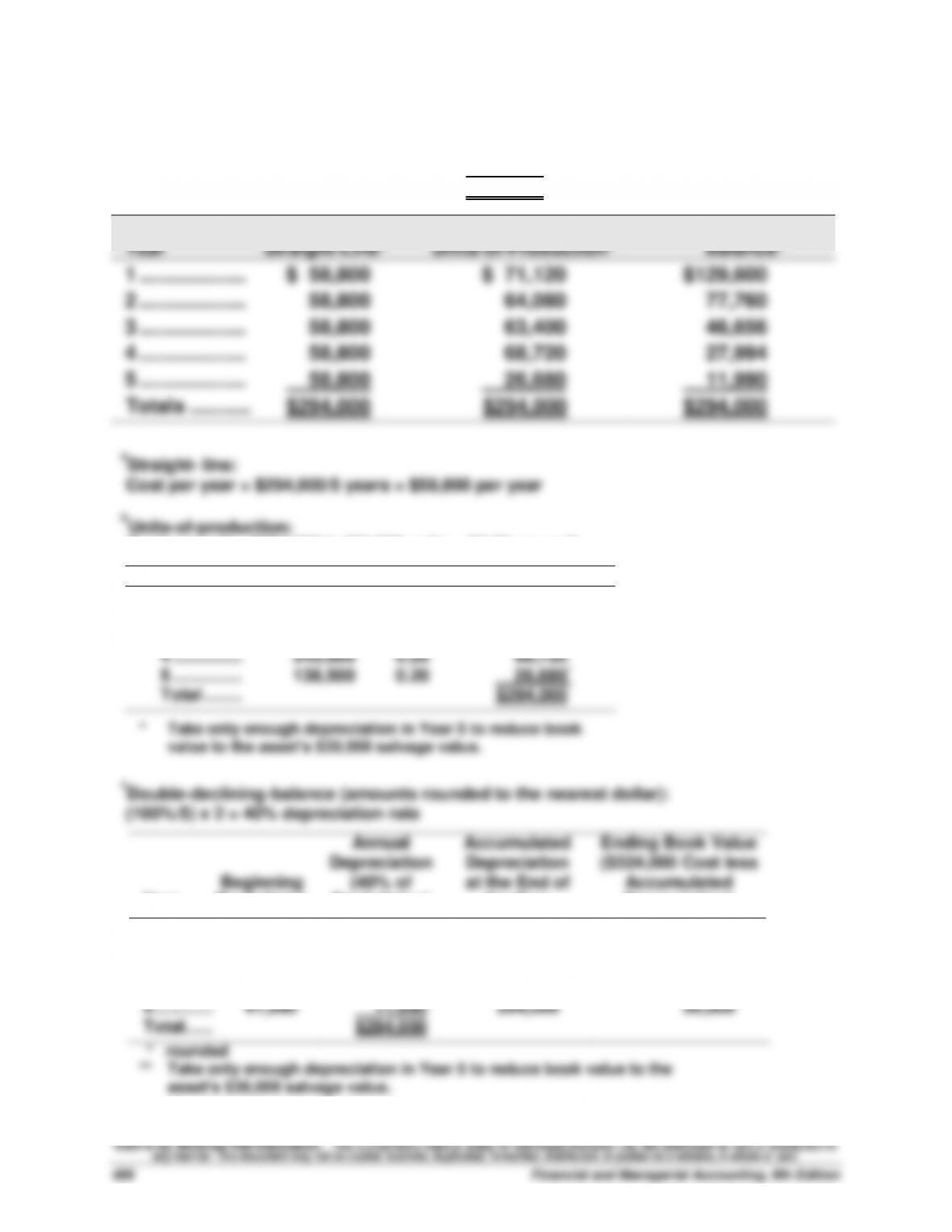

$294,000

Year

Straight-Linea

Units-of-Productionb

Double-Declining-

Balancec

1 ……………….

$ 58,800

$ 71,120

$129,600

2 ……………….

58,800

64,080

77,760

3 ……………….

58,800

63,400

46,656

4 ……………….

58,800

68,720

27,994

5 ……………….

58,800

26,680

11,990

Totals ………..

$294,000

$294,000

$294,000

aStraight- line:

Cost per year = $294,000/5 years = $58,800 per year

bUnits-of-production:

Cost per unit = $294,000/1,470,000 units = $0.20 per unit

Year

Units

Unit Cost

Depreciation

1 …………..

355,600

$0.20

$ 71,120

2 …………..

320,400

0.20

64,080

3 …………..

317,000

0.20

63,400

4 …………..

343,600

0.20

68,720

5 …………..

138,500

0.20

26,680*

Total ……..

$294,000

* Take only enough depreciation in Year 5 to reduce book

value to the asset’s $30,000 salvage value.

cDouble-declining-balance (amounts rounded to the nearest dollar):

(100%/5) x 2 = 40% depreciation rate

Year

Beginning

Book Value

Annual

Depreciation

(40% of

Book Value)

Accumulated

Depreciation

at the End of

the Year

Ending Book Value

($324,000 Cost less

Accumulated

Depreciation)

1 …………

$324,000

$129,600

$129,600

$194,400

2 …………

194,400

77,760

207,360

116,640

3 …………

116,640

46,656

254,016

69,984

4 …………

69,984

27,994*

282,010

41,990

5 …………

41,990

11,990**

294,000

30,000

Total……

$294,000

* rounded

** Take only enough depreciation in Year 5 to reduce book value to the

asset’s $30,000 salvage value.

Problem 8-3B (45 minutes)

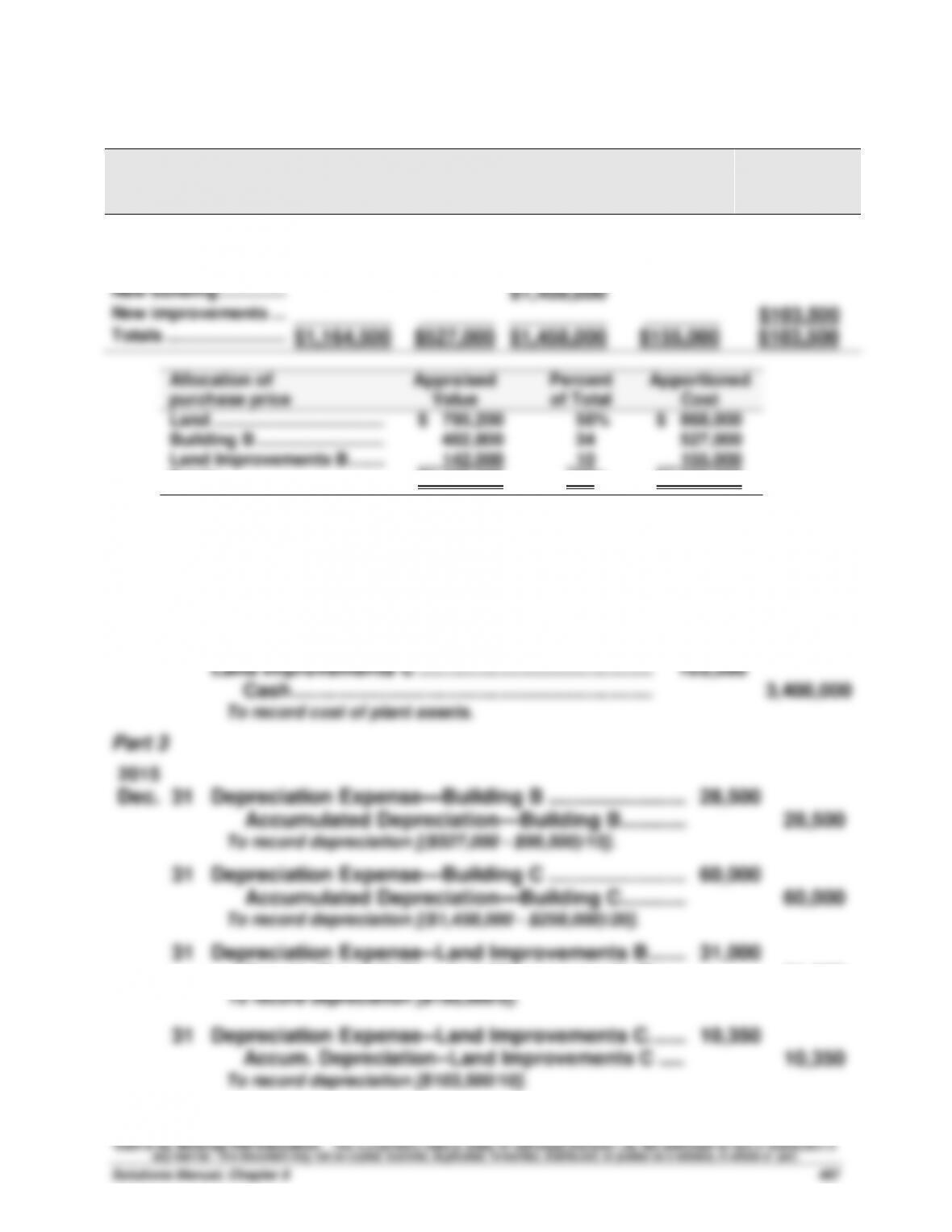

Part 1

Land

Building

B

Building

C

Land

Improve-

ments B

Land

Improve-

ments C

Purchase price* ……….

$ 868,000

$527,000

$155,000

Demolition ………………

122,000

Land grading …………..

174,500

New building……………

$1,458,000

New improvements ….

_________

_______

_________

_______

$103,500

Totals ……………………..

$1,164,500

$527,000

$1,458,000

$155,000

$103,500

Allocation of

purchase price

Appraised

Value

Percent

of Total

Apportioned

Cost

Land …………………………………..

$ 795,200

56%

$ 868,000

Building B …………………………..

482,800

34

527,000

Land Improvements B ……..…..

142,000

10

155,000

Totals …………………………….…..

$1,420,000

100%

$1,550,000

Part 2

2015

Jan. 1

Land …………………………………………………………………

1,164,500

Building B…………………………………………………………

527,000

Building C…………………………………………………………

1,458,000

Land Improvements B …………………………..………….

155,000

Land Improvements C …………………………..………….

103,500

Cash ……………………………………………………………

3,408,000

To record cost of plant assets.

Part 3

2015

Dec. 31

Depreciation Expense—Building B …………………….…….

28,500

Accumulated Depreciation—Building B ……………………..

28,500

To record depreciation [($527,000 – $99,500)/15].

31

Depreciation Expense—Building C ……………………...

60,000

Accumulated Depreciation—Building C …………..

60,000

To record depreciation [($1,458,000 – $258,000)/20].

31

Depreciation Expense—Land Improvements B ……...

31,000

Accum. Depreciation—Land Improvements B …….

31,000

To record depreciation [$155,000/5].

31

Depreciation Expense—Land Improvements C. ……..

10,350

Accum. Depreciation—Land Improvements C …….

10,350

To record depreciation [$103,500/10].

Problem 8-4B (50 minutes)

2014

Jan. 1

Equipment …………………………………………………………..

27,670

Cash ……………………………………………………………...

27,670

To record costs of van ($25,860 + $1,810).

Jan. 3

Equipment …………………………………………………………..

1,850

Cash ……………………………………………………………...

1,850

To record betterment of van.

Dec. 31

Depreciation Expense—Equipment ……………………...

5,124*

Accumulated Depreciation—Equipment ………....

5,124

To record depreciation.

*2014 depreciation after January 3rd betterment

Total original cost …………………………..…………………………..

$27,670

Plus cost of betterment ………………………………………..…………

1,850

Revised cost of equipment ………………………………………………

29,520

Less revised salvage ($3,670 + $230) …………………………..

3,900

Cost to be depreciated ……………………………………………………

$25,620

Annual depreciation ($25,620 / 5 years) …………………………..

$ 5,124

2015

Jan. 1

Equipment …………………………………………………………..

2,064

Cash ……………………………………………………………...

2,064

To record extraordinary repair on van.

May 10

Repairs Expense—Equipment ……………………………..

800

Cash ……………………………………………………………...

800

To record ordinary repair on van.

Dec. 31

Depreciation Expense—Equipment ……………………...

3,760

Accumulated Depreciation—Equipment ………....

3,760

To record depreciation.

*2015 depreciation after 1/1 extraordinary repair

Total cost ($29,520 + $2,064) ………………………………………….……………

$31,584

Less accumulated depreciation ……………………………………..………………..

5,124

Book value ……………………………………………………………………………………

26,460

Less salvage ……………………………………………………………………………………

3,900

Remaining cost to be depreciated…………………………………..…………………..

$22,560

Revised remaining useful life (Original 5 years – 1yr. + 2yrs.) …………………………..

6 yrs.

Revised annual depreciation ($22,560 / 6 yrs) ………………….……….

$ 3,760