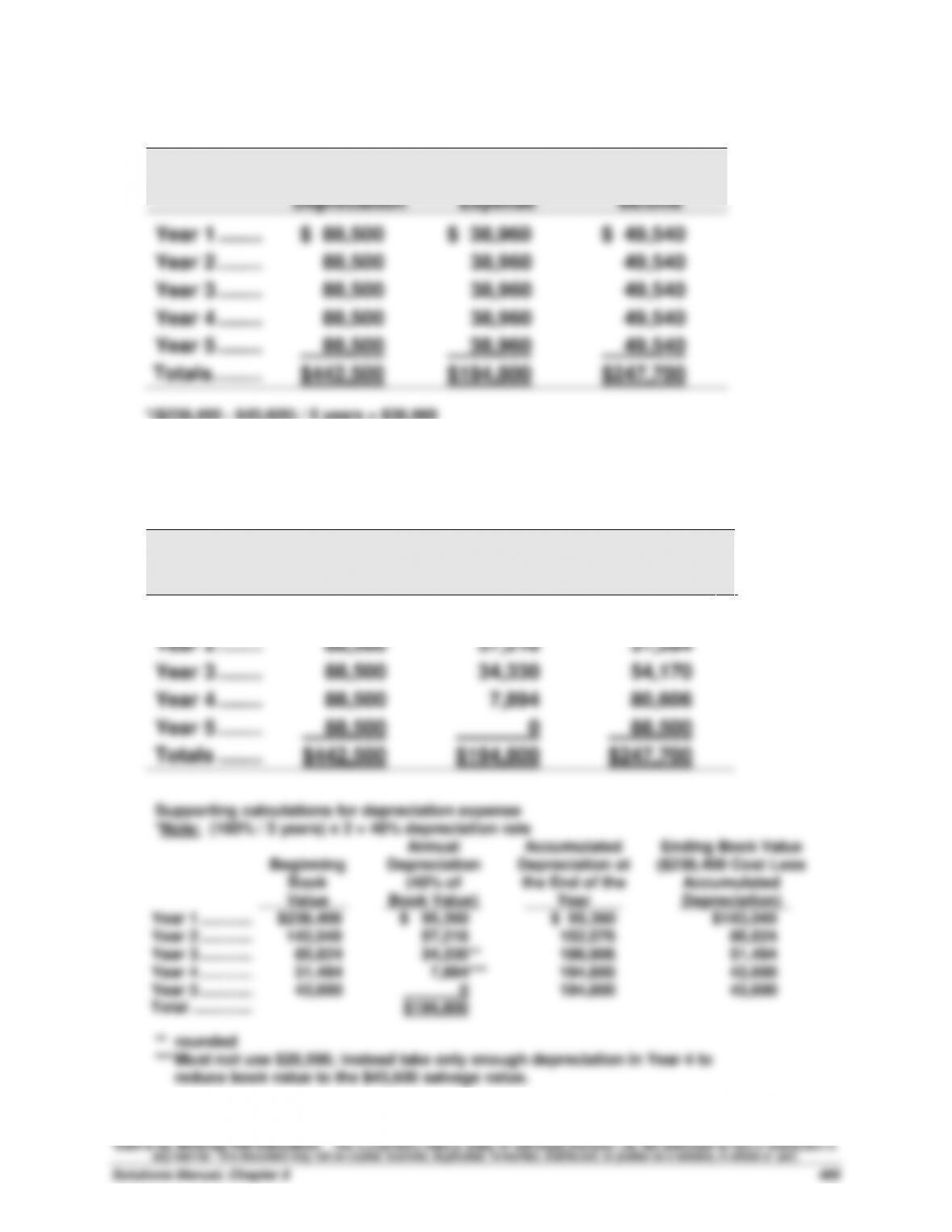

Exercise 8-9 (30 minutes)

Straight–line depreciation

Income

before

Depreciation

Depreciation

Expense*

Net

Income

Year 1 ……..

$ 88,500

$ 38,960

$ 49,540

Year 2 ……..

88,500

38,960

49,540

Year 3 ……..

88,500

38,960

49,540

Year 4 ……..

88,500

38,960

49,540

Year 5 ……..

88,500

38,960

49,540

Totals………

$442,500

$194,800

$247,700

*($238,400 – $43,600) / 5 years = $38,960

Exercise 8-10 (30 minutes)

Double–declining-balance depreciation

Income

before

Depreciation

Depreciation

Expense*

Net

Income

Year 1 ……..

$ 88,500

$ 95,360

$ (6,860)

Year 2 ……..

88,500

57,216

31,284

Year 3 ……..

88,500

34,330

54,170

Year 4 ……..

88,500

7,894

80,606

Year 5 ……..

88,500

0

88,500

Totals ……..

$442,500

$194,800

$247,700

Supporting calculations for depreciation expense

*Note: (100% / 5 years) x 2 = 40% depreciation rate

Beginning

Book

Value

Annual

Depreciation

(40% of

Book Value)

Accumulated

Depreciation at

the End of the

Year

Ending Book Value

($238,400 Cost Less

Accumulated

Depreciation)

Year 1 …………..

$238,400

$ 95,360

$ 95,360

$143,040

Year 2 …………..

143,040

57,216

152,576

85,824

Year 3 …………..

85,824

34,330**

186,906

51,494

Year 4 …………..

51,494

7,894***

194,800

43,600

Year 5 …………..

43,600

0

194,800

43,600

Total …………....

$194,800

** rounded

*** Must not use $20,598; instead take only enough depreciation in Year 4 to

reduce book value to the $43,600 salvage value.

Exercise 8-11 (10 minutes)

Straight–line depreciation for 2014

Exercise 8-12 (15 minutes)

Double–declining-balance depreciation for 2014 and 2015:

Rate = (100% / 5 years) x 2 = 40%

Depreciation for 2014 ($280,000 x 40% x 9/12) ……………

$ 84,000

Book value at January 1, 2015 ($280,000 – $84,000) ……

$196,000

Depreciation for 2015 ($196,000 x 40%) ……………………..

$ 78,400

Alternate calculation

2014 depreciation ($280,000 x 40% x 9/12) …………………………....

$ 84,000

2015 depreciation

$280,000 x 40% x 3/12 ………………………………………………………

$ 28,000

($280,000 – $84,000 – $28,000) x 40% x 9/12 ……………………….

50,400

Total 2015 depreciation …………………………………………………………

$ 78,400

Exercise 8-13 (15 minutes)

1.

Original cost of machine …………………………………………..………..

$ 23,860

Less two years’ accumulated depreciation

[($23,860 – $2,400) / 4 years] x 2 years …………………….…….

(10,730)

Book value at end of second year ……………………………..………..

$ 13,130

2.

Book value at end of second year ……………………………..………..

$ 13,130

Less revised salvage value ……………………………………….………..

(2,000)

Remaining depreciable cost ……………………………………..………..

$ 11,130

Revised annual depreciation = $11,130 / 3 years = $3,710

Exercise 8-14 (15 minutes)

1.

Equipment ………………………………………………………..….

22,000

Cash …………………………………………………………..….

22,000

To record betterment.

2.

Repairs Expense ……………………………………………….….

6,250

Cash …………………………………………………………..….

6,250

To record ordinary repairs.

3.

Equipment …………………………..……………………………….

14,870

Cash …………………………………………………………..….

14,870

To record extraordinary repairs.

Exercise 8-15 (25 minutes)

1. Annual depreciation = $572,000 / 20 years = $28,600 per year

2. Entry to record the extraordinary repairs

Building ……………………………………………………………..….

68,350

Cash …………………………………………………………..….

68,350

To record extraordinary repairs.

3.

Cost of building

Before repairs ……………………………………………………….

$572,000

Add cost of repairs …………………………………………………

68,350

$640,350

Less accumulated depreciation …………………………..

429,000

Revised book value of building …………………………..

$211,350

4.

Revised book value of building (part 3) ………………………

$211,350

New estimate of useful life (20 – 15 + 5) ………………………

10 years

Revised annual depreciation ……………………………..………

$ 21,135

Journal entry

Depreciation Expense…………………………………………….

21,135

Accumulated Depreciation–Building …………………..

21,135

To record depreciation.

Exercise 8-16 (20 minutes)

1. Disposed at no value

Jan. 3

Loss on Disposal of Milling Machine …………………….

68,000

Accumulated Depreciation—Milling Machine ….…….

182,000

Milling Machine ………………………………………….…….

250,000

To record disposal of milling machine.

2. Sold for $35,000 cash

Jan. 3

Cash…………………………………………………………………….

35,000

Loss on Sale of Milling Machine ……………………..……

33,000

Accumulated Depreciation—Milling Machine ….…….

182,000

Milling Machine ………………………………………….…….

250,000

To record cash sale of milling machine.

3. Sold for $68,000 cash

Jan. 3

Cash…………………………………………………………………….

68,000

Accumulated Depreciation—Milling Machine ….…….

182,000

Milling Machine ………………………………………….…….

250,000

To record cash sale of milling machine.

4. Sold for $80,000 cash

Jan. 3

Cash…………………………………………………………………….

80,000

Accumulated Depreciation—Milling Machine ….…….

182,000

Gain on Sale of Milling Machine ………………….…….

12,000

Milling Machine ………………………………………….…….

250,000

To record cash sale of milling machine.

Exercise 8-17 (25 minutes)

2019

July 1

Depreciation Expense …………………………..………….

7,500

Accumulated Depreciation—Machinery …………

7,500

To record one-half year depreciation.*

*Annual depreciation = $105,000 / 7 years = $15,000

Depreciation for 6 months in 2019 = $15,000 x 6/12 = $7,500

1. Sold for $45,500 cash

July 1

Cash……………………………………………………………….……

45,500

Accumulated Depreciation—Machinery …………..……

67,500

Gain on Sale of Machinery…………………………………

8,000

Machinery ……………………………………………………….

105,000

To record sale of machinery.*

*Total accumulated depreciation at date of disposal:

Four years 2015-2018 (4 x $15,000) …….. $60,000

Partial year 2019 (6/12 x $15,000) ………… 7,500

Total accumulated depreciation …………. $67,500

Book value of machinery = $105,000 – $67,500 = $37,500

2. Destroyed by fire with $25,000 cash insurance settlement

July 1

Cash……………………………………………………………….……

25,000

Loss from Fire …………………………..…………………………

12,500

Accumulated Depreciation—Machinery …………..……

67,500

Machinery ……………………………………………………….

105,000

To record disposal of machinery from fire.

Exercise 8-18 (10 minutes)

Dec. 31

Depletion Expense—Mineral Deposit ……………..…….

405,528

Accumulated Depletion—Mineral Deposit …..…….

405,528

To record depletion [$3,721,000/1,525,000 tons =

$2.44 per ton; 166,200 tons x $2.44 = $405,528].

Dec. 31

Depreciation Expense—Machinery ………………..…….

23,268

Accumulated Depreciation—Machinery ……..…….

23,268

To record depreciation [$213,500/1,525,000 tons=

$0.14 per ton; 166,200 tons x $0.14 = $23,268].

Exercise 8-19 (10 minutes)

Jan. 1

Copyright ……………………………………………………….

418,000

Cash…………………………..……………………………..…….

418,000

To record purchase of copyright.

Dec. 31

Amortization Expense—Copyright ……………………….

41,800

Accumulated Amortization—Copyright …………….

41,800

To record amortization of copyright

[$418,000 / 10 years].

Exercise 8-20 (10 minutes)

1. Goodwill = $2,500,000 – $1,800,000 = $700,000

2. Goodwill is not amortized. Instead, Robinson must test the value of the

3. Goodwill is only recorded when it is purchased. Goodwill is not

Exercise 8-21 (15 minutes)

1. $7,358 million cash for property and equipment

2. $2,781 million for

depreciation and amortization

3. $13,679 million cash used in investing activities

Exercise 8-22 (15 minutes)

(4.59 – 3.36) more times in 2015 than in 2014. This increase indicates that the

company became more efficient in using its assets. Moreover, it has improved its

$5,856,480

Exercise 8-23A (15 minutes)

1. Book value of the old tractor ($96,000 – $52,500) …………………….. $ 43,500

2. Loss on the exchange

3. Debit to new Tractor account

Cash paid + Trade-in allowance ($83,000 + $29,000) ………….. $112,000

Alternatively, answers can be taken from the following journal entry:

Tractor (new)* …………………………………………………………………...

112,000

Loss on Exchange of Assets ……………………………………………...

14,500

Accumulated Depreciation–Tractor …………………………………….

52,500

Tractor (old) ……………………………………………………………….

96,000

Cash ………………………………………………………………………….

83,000

To record asset exchange. *($29,000 + $83,000)

Exercise 8-24A (25 minutes)

1. Sold for $18,250 cash

Jan. 2

Cash…………………………………………………………………….

18,250

Loss on Sale of Machinery …………………………..

1,125

Accumulated Depreciation—Machinery (old) ..……….

24,625

Machinery (old) ……………………………………….……….

44,000

To record cash sale of machine.

2. $25,000 trade-in allowance exceeds book value; but no gain is

recognized on an asset exchange that lacks commercial substance

($5,625 gain is ‘buried’ in the cost of the new machinery)

Jan. 2

Machinery (new)* ………………………………………………….

54,575

Accumulated Depreciation—Machinery (old) ..……….

24,625

Machinery (old) ……………………………………….……….

44,000

Cash** …………………………………………………….…

35,200

To record asset exchange.

*[$60,200 – ($25,000 – $19,375)] **($60,200 – $25,000)

3. $15,000 trade-in allowance is less than book value (yielding a loss)

Jan. 2

Machinery (new) ………………………………………….……….

60,200

Loss on Exchange of Machinery ………………….……….

4,375

Accumulated Depreciation—Machinery (old) ..……….

24,625

Machinery (old) ……………………………………….……….

44,000

Cash* ……………………………………………………....

45,200

To record asset exchange. *($60,200 – $15,000)

Exercise 8-25 (20 minutes)

1.

Depreciation expense …………………………………………….

6,689

Accumulated depreciation—Property, plant

and equipment……………………………………………..

6,689

To record depreciation on property, plant and

equipment.

2.

Property, plant and equipment …………………………..…..

11,061

Cash ……………………………………………………………….

11,061

To record betterments (improvements) on property,

plant and equipment.

3.

Cash …………………………..…………………………………………

700

Loss on disposal of property, plant and equipment ..

500

Accumulated Depreciation—Property, plant and

equipment …………………………..………………………………

1,162

Property, plant and equipment …………………………

2,362

To record asset disposals.

4. Volkswagen would decrease its property, plant and equipment account

©2016 by McGraw–Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in

any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

Solutions Manual, Chapter 8

477

PROBLEM SET A

Problem 8-1A (50 minutes)

Part 1

Estimated

Market Value

Percent

of Total

Apportioned

Cost

Building ……………………..

$508,800

53%

$477,000

Land …………………………..

297,600

31

279,000

Land improvements …...

28,800

3

27,000

Vehicles ……………………..

124,800

13

117,000

Total …………………………..

$960,000

100%

$900,000

2015

Jan. 1

Building …………………………………………………….…

477,000

Land ……………………………………………………………………..

279,000

Land Improvements …………………………………..…………..

27,000

Vehicles ……………………………………………………….

117,000

Cash …………………………..……………………….….

900,000

To record asset purchases.

Part 2

Year 2015 straight-line depreciation on building

[($477,000 – $27,000) / 15 years] = $30,000

Part 3

Year 2015 double-declining-balance depreciation on land improvements

(100% / 5 years) x 2 = 40% rate

$27,000 x 40% = $10,800

Part 4

Accelerated depreciation does not lower the total amount of taxes paid over

the asset’s life. Instead, it defers or postpones taxes to the later years of an

asset’s useful life. This is because accelerated methods charge a higher

portion of asset costs against revenue in earlier years and a lower portion in

later years. The result is to reduce taxable income more in earlier years but

less in later years. [Note: From a present value perspective, there is a tax

savings from use of accelerated depreciation. The company gets to use the

tax deferred amounts for investment purposes until they are due.]

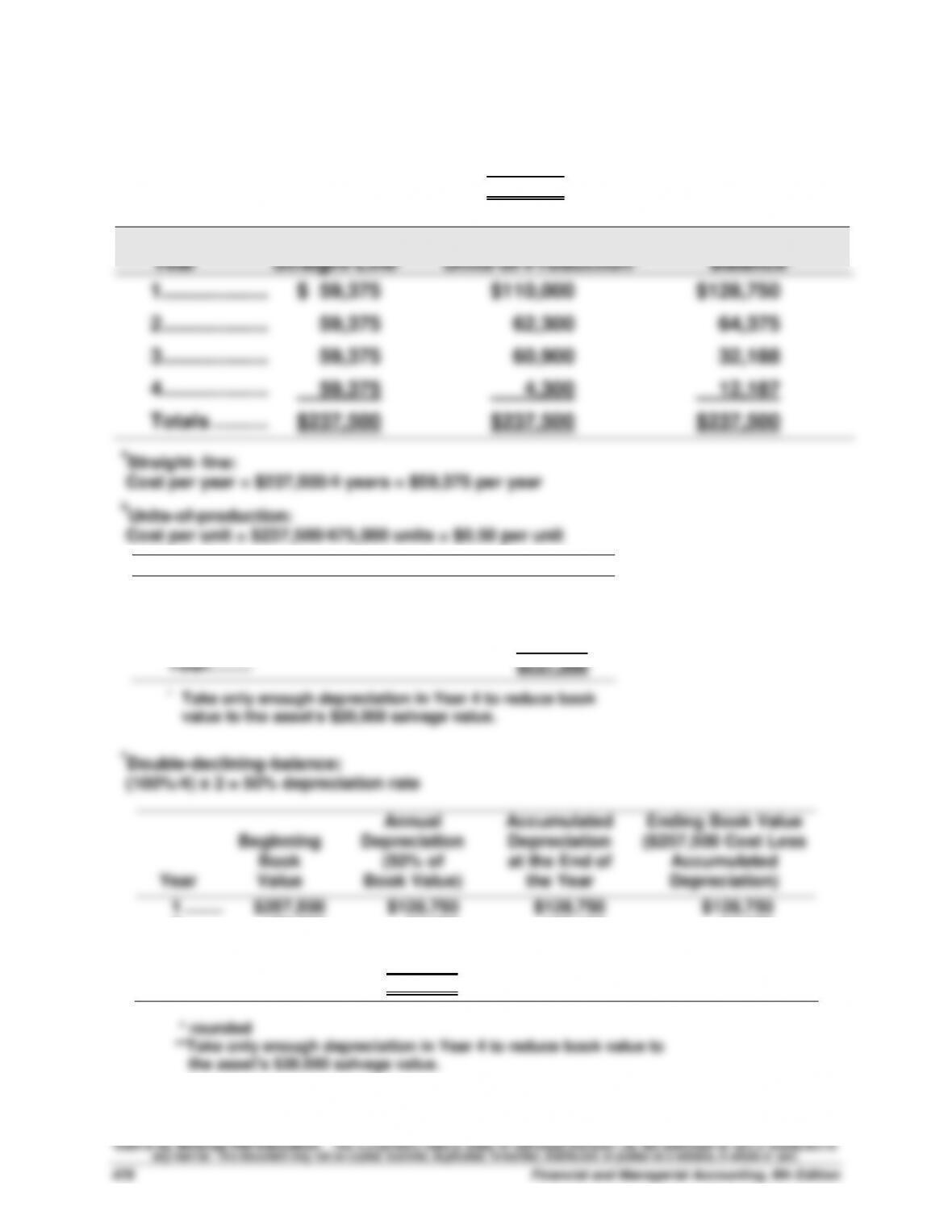

Problem 8-2A (25 minutes)

Cost of machine ……………………………….…………………….

$257,500

Less estimated salvage value …………………………..

20,000

Total depreciable cost …………………………..

$237,500

Year

Straight–Linea

Units–of–Productionb

Double–Declining–

Balancec

1 ………………....

$ 59,375

$110,000

$128,750

2 ………………....

59,375

62,300

64,375

3 ………………....

59,375

60,900

32,188

4 ………………....

59,375

4,300

12,187

Totals ………....

$237,500

$237,500

$237,500

aStraight- line:

Cost per year = $237,500/4 years = $59,375 per year

bUnits-of-production:

Cost per unit = $237,500/475,000 units = $0.50 per unit

Year

Units

Unit Cost

Depreciation

1 …………….

220,000

$0.50

$110,000

2 …………….

124,600

0.50

62,300

3 …………….

121,800

0.50

60,900

4 …………….

15,200

0.50

4,300*

Total……….

$237,500

* Take only enough depreciation in Year 4 to reduce book

value to the asset’s $20,000 salvage value.

cDouble-declining-balance:

(100%/4) x 2 = 50% depreciation rate

Year

Beginning

Book

Value

Annual

Depreciation

(50% of

Book Value)

Accumulated

Depreciation

at the End of

the Year

Ending Book Value

($257,500 Cost Less

Accumulated

Depreciation)

1 ……..

$257,500

$128,750

$128,750

$128,750

2 ……..

128,750

64,375

193,125

64,375

3 ……..

64,375

32,188*

225,313

32,187

4 ……..

32,187

12,187**

237,500

20,000

Total ..

$237,500