Exercise 7-8 (20 minutes)

Feb. 1

Allowance for Doubtful Accounts ……………………..….

6,800

Accounts Receivable—Oakley Co ……………….….

900

Accounts Receivable—Brookes Co …………….….

5,900

To write off specific accounts.

June 5

Accounts Receivable—Oakley …………………………..

900

Allowance for Doubtful Accounts ………………..….

900

To reinstate an account.

June 5

Cash ………………………………………………………………..….

900

Accounts Receivable—Oakley …………………….….

900

To record cash received on account.

Exercise 7-9 (25 minutes)

a. Expense is 3.0% of credit sales

Dec. 31

Bad Debts Expense………………………………………..

9,000

Allowance for Doubtful Accounts ……………..

9,000

To record estimated bad debts

[$300,000 x .03].

b. Expense is 1.0% of total sales

Dec. 31

Bad Debts Expense………………………………………..

12,000

Allowance for Doubtful Accounts ……………..

12,000

To record estimated bad debts

[($300,000 + $900,000) x .01].

c. Allowance is 6% of accounts receivable

Dec. 31

Bad Debts Expense………………………………………..

12,500

Allowance for Doubtful Accounts ……………..

12,500

To record estimated bad debts.*

* Unadjusted balance ……………………………….…………….

$ 5,000 debit.

Estimated balance ($125,000 x 6%) ………….…………….

7,500 credit

Required adjustment …………………………………………….

$12,500 credit

Exercise 7-10 (10 minutes)

2014

Dec. 13

Notes Receivable—M. Lee………………………

9,500

Accounts Receivable—M. Lee …………..

9,500

To record receipt of note on account.

Dec. 31

Interest Receivable ………………………………..

38

Interest Revenue ………………………………

38

To record interest earned [$9,500 x .08 x 18/360].

Exercise 7-11 (15 minutes)

2015

Jan. 27

Cash …………………………………………………………..…

9,595

Interest Revenue* …………………………………..…

57

Interest Receivable ………………………………..…

38

Notes Receivable—M. Lee…………………………

9,500

To record cash received on note plus interest.

* [$9,500 x .08 x (45-18)/360 = $57]

Mar. 3

Notes Receivable—Tomas Co. …………………….…

5,000

Accounts Receivable-Tomas Co …………….…

5,000

To record receipt of note on account.

17

Notes Receivable—H. Cheng ……………………….…

2,000

Accounts Receivable—H. Cheng ………………

2,000

To record receipt of note on account.

Apr. 16

Accounts Receivable—H. Cheng ……………………

2,015

Interest Revenue ………………………………………

15

Notes Receivable—H. Cheng ………………….…

2,000

To record receivable for dishonored

note plus interest [$2,000 x .09 x 30/360].

May 1

Allowance for Doubtful Accounts ………………..…

2,015

Accounts Receivable—H. Cheng ………………

2,015

To write off account.

June 1

Cash …………………………………………………………..…

5,125

Interest Revenue ………………………………………

125

Notes Receivable—Tomas Co ………………..…

5,000

To record cash received on note with

interest [$5,000 x .10 x 90/360].

Exercise 7-12 (15 minutes)

Nov. 1

Notes Receivable—K. White ………………………..

6,000

Accounts Receivable—K. White ……………..

6,000

To record receipt of note on account.

Dec. 31

Interest Receivable ……………………………………..

80

Interest Revenue ……………………………………

80

To record interest earned

[$6,000 x .08 x 60/360].

Apr. 30

Cash …………………………………………………………..

6,240

Notes Receivable—K. White …………………..

6,000

Interest Revenue* …………………………………..

160

Interest Receivable ………………………………..

80

To record cash received on note plus

interest earned. *[$6,000 x .08 x 120/360]

Exercise 7-13 (20 minutes)

Mar. 21

Notes Receivable—T. Jackson …………………….…

9,500

Accounts Receivable—T. Jackson ………….…

9,500

To record receipt of note on account.

Sept. 17

Accounts Receivable—T. Jackson ……………….…

9,880

Interest Revenue ………………………………………

380

Notes Receivable—T. Jackson ……………….…

9,500

To record note dishonored plus interest

earned [$9,500 x .08 x 180/360 = $380].

Dec. 31

Allowance for Doubtful Accounts ………………..…

9,880

Accounts Receivable—T. Jackson ………….…

9,880

To write off an account.

Exercise 7-14 (20 minutes)

July 4

Accounts Receivable ……………………………………..

7,245

Sales ……………………………………………………….

7,245

To record sales on credit.

4

Cost of Goods Sold ………………………………………………

5,000

Merchandise Inventory ……………………………………

5,000

To record cost of sales.

9

Cash ……………………………………………………………..

19,200

Factoring Fee Expense* ………………………………...

800

Accounts Receivable ………………………………..

20,000

To record sale of receivable. *($20,000 x .04)

17

Cash ……………………………………………………………..

5,859

Accounts Receivable ………………………………..

5,859

To record cash received on account.

27

Cash ……………………………………………………………..

10,000

Notes Payable…………………………………………..

10,000

To record cash from a loan.

Note to Financial Statements

Accounts receivable in the amount of $12,500 are pledged

as security for a $10,000 note payable to Main Bank.

Exercise 7-15 (15 minutes)

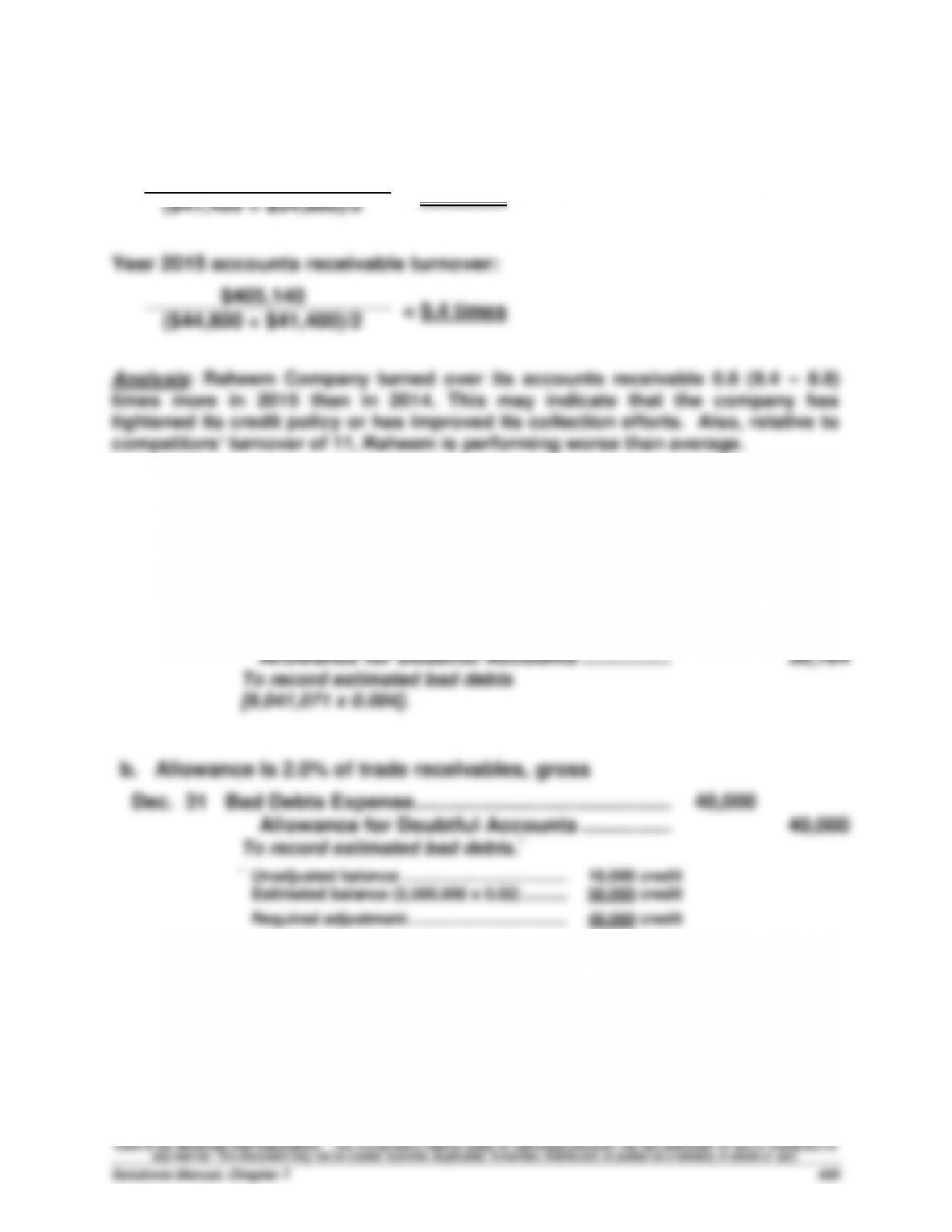

Year 2014 accounts receivable turnover:

= 8.8 times

Exercise 7-16 (25 minutes)

(¥ in millions)

a. Expense is 0.4% of total revenues

Dec. 31

Bad Debts Expense………………………………………..

36,164

Allowance for Doubtful Accounts ……………..

36,164

To record estimated bad debts

[9,041,071 x 0.004].

b. Allowance is 2.0% of trade receivables, gross

Dec. 31

Bad Debts Expense………………………………………..

40,000

Allowance for Doubtful Accounts ……………..

40,000

To record estimated bad debts.*

* Unadjusted balance ……………………………….…………….

10,000 credit

Estimated balance (2,500,000 x 0.02) ……….…………….

50,000 credit

Required adjustment …………………………………………….

40,000 credit

$335,280

($41,400 + $34,800)/2

Problem 7-1A (30 minutes)

June 4

Accounts Receivable—N. Morris ………………………...

650

Sales ……………………………………………………………..

650

To record sales on credit.

4

Cost of Goods Sold …………………………………………..………

400

Merchandise Inventory …………………………..……………

400

To record cost of sales.

5

Cash …………………………………………………………………...

6,693

Credit card expense* …………………………………………..

207

Sales ……………………………………………………………..

6,900

To record credit card sales less fee. *($6,900 x .03)

5

Cost of Goods Sold …………………………………………..………

4,200

Merchandise Inventory …………………………..……………

4,200

To record cost of sales.

6

Accounts Receivable—Access …………………………..

5,733

Credit card expense* …………………………………………..

117

Sales ……………………………………………………………..

5,850

To record credit card sales less fee. *($5,850 x .02)

6

Cost of Goods Sold …………………………………………..………

3,800

Merchandise Inventory …………………………..……………

3,800

To record cost of sales.

8

Accounts Receivable—Access …………………………..

4,263

Credit card expense* …………………………………………..

87

Sales ……………………………………………………………..

4,350

To record credit card sales less fee. *($4,350 x .02)

8

Cost of Goods Sold …………………………………………..………

2,900

Merchandise Inventory …………………………..……………

2,900

To record cost of sales.

10

No journal entry required.

13

Allowance for Doubtful Accounts ……………………....

429

Accounts Receivable—A. McKee …………………..

429

To write off account due.

17

Cash …………………………………………………………………...

9,996

Accounts Receivable—Access ……………………...

9,996

To record cash received from credit card co. ($5,733+$4,263)

18

Cash …………………………………………………………………...

637

Sales Discounts* ………………………………………………...

13

Accounts Receivable—N. Morris …………………...

650

To record cash received less discount. *($650 x .02)

Problem 7-2A (35 minutes)

Part 1

a. Expense is 1.5% of credit sales

Dec. 31

Bad Debts Expense………………………………..………

85,230

Allowance for Doubtful Accounts ……..………

85,230

To record estimated bad debts

[$5,682,000 x .015].

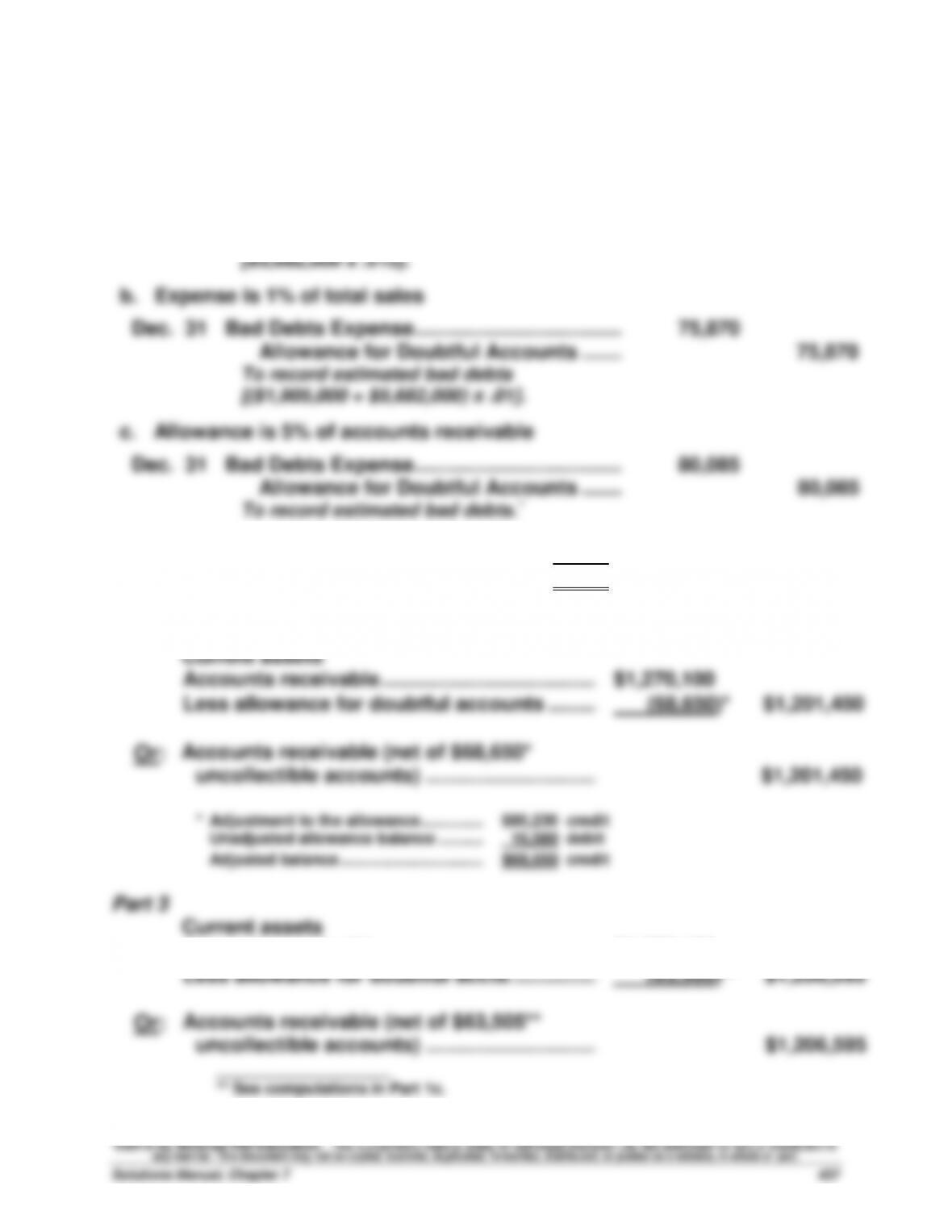

b. Expense is 1% of total sales

Dec. 31

Bad Debts Expense………………………………..………

75,870

Allowance for Doubtful Accounts ……..………

75,870

To record estimated bad debts

[($1,905,000 + $5,682,000) x .01].

c. Allowance is 5% of accounts receivable

Dec. 31

Bad Debts Expense………………………………..………

80,085

Allowance for Doubtful Accounts ……..………

80,085

To record estimated bad debts.*

* Unadjusted balance……………………………..……………….

$16,580 debit

Estimated balance ($1,270,100 x 5%) …….……………….

63,505 credit

Required adjustment …………………………………………….

$80,085 credit

Part 2

Adjusted balance …………………………..

Problem 7-3A (35 minutes)

Part 1

Calculation of the estimated balance of the allowance for uncollectibles

Not due:

$830,000 x .0125 =

$10,375

1 to 30:

254,000 x .0200 =

5,080

31 to 60:

86,000 x .0650 =

5,590

61 to 90:

38,000 x .3275 =

12,445

Over 90:

12,000 x .6800 =

8,160

$41,650

credit

Part 2

Dec. 31

Bad Debts Expense……………………………………....

27,150

Allowance for Doubtful Accounts …………....

27,150

To record estimated bad debts.*

* Unadjusted balance ……………………..

$14,500 credit

Estimated balance ……………………….

41,650 credit

Required adjustment ……………………

$27,150 credit

Part 3

Writing off the account receivable in 2016 will not directly affect year 2016

net income. The entry to write off an account involves a debit to Allowance

for Doubtful Accounts and a credit to Accounts Receivable, both of which

are balance sheet accounts. Net income is affected only by the annual

recognition of the estimated bad debts expense, which is journalized as an

adjusting entry. Net income for Year 2015 (the year of the original sale)

included an estimated expense for write–offs such as this one.

Problem 7-4A (35 minutes)

2014

a.

Accounts Receivable …………………………..……...

1,345,434

Sales ……………………………………………………..

1,345,434

To record sales on account.

Cost of Goods Sold ………………………………………………

975,000

Merchandise Inventory …………………………..

975,000

To record cost of sales.

b.

Allowance for Doubtful Accounts ………………...

18,300

Accounts Receivable ………………………….....

18,300

To write off accounts.

c.

Cash …………………………………………………………...

669,200

Accounts Receivable ………………………….....

669,200

To record cash received on account.

d.

Bad Debts Expense …………………………..………...

28,169

Allowance for Doubtful Accounts …………..

28,169

To record estimated bad debts.*

*Beginning receivables ………………….

$ 0

Credit sales …………………………………

1,345,434

Collections ………………………………….

(669,200)

Write-offs …………………………………….

(18,300)

Ending receivables ………………………

657,934

Percent uncollectible ……………………

x 1.5%

Required ending allowance …………..

9,869**

Cr.

Unadjusted balance ……………………..

18,300

Dr.

Adjustment to the allowance ………..

$ 28,169

Cr.

** rounded to nearest dollar

Problem 7-4A (Concluded)

2015

e.

Accounts Receivable …………………………………….…

1,525,634

Sales ……………………………………………………….

1,525,634

To record sales on account.

Cost of Goods Sold ……………………………………….……..

1,250,000

Merchandise Inventory …………………………….……..

1,250,000

To record cost of sales.

f.

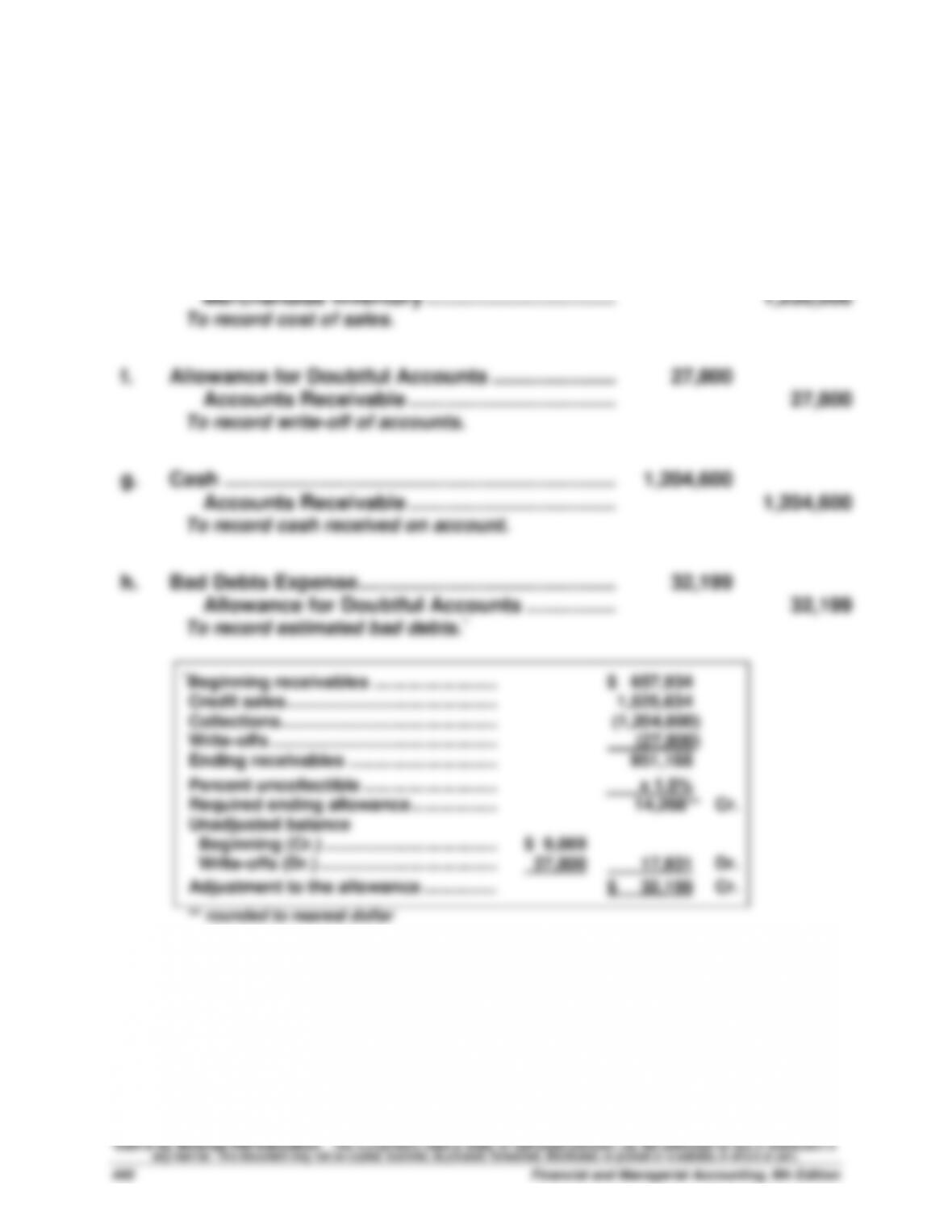

Allowance for Doubtful Accounts ………………….…

27,800

Accounts Receivable ……………………………….…

27,800

To record write-off of accounts.

g.

Cash …………………………..………………………………..…

1,204,600

Accounts Receivable ……………………………….…

1,204,600

To record cash received on account.

h.

Bad Debts Expense……………………………………….…

32,199

Allowance for Doubtful Accounts …………….…

32,199

To record estimated bad debts.*

*Beginning receivables ……………………....

$ 657,934

Credit sales …………………………..…………..

1,525,634

Collections ………………………………………..

(1,204,600)

Write-offs ………………………………………....

(27,800)

Ending receivables …………………………..

951,168

Percent uncollectible ………………………...

x 1.5%

Required ending allowance ………………..

14,268**

Cr.

Unadjusted balance

Beginning (Cr.) ………………………………..

$ 9,869

Write-offs (Dr.) ………………………………...

27,800

17,931

Dr.

Adjustment to the allowance ……………...

$ 32,199

Cr.

** rounded to nearest dollar