Problem 5-10AB (25 minutes)

WAYWARD COMPANY

Estimated Inventory at March 31

Goods available for sale

Inventory, January 1 …………………………………….…

$ 302,580

Cost of goods purchased ……………………………..…

941,040

Goods available for sale ……………………………….…

1,243,620

Less estimated cost of goods sold

Sales ………………………………………………………………

$1,211,160

Less sales returns ……………………………………….…

(8,410)

Net sales ……………………………………………………....

$1,202,750

Estimated cost of goods sold

[$1,202,750 x (1 – 34%)] ………………………………

(793,815)

Estimated March 31 inventory …………………………..

$ 449,805

Problem 5-1B (40 minutes)

1. Compute cost of goods available for sale and units available for sale

Beginning inventory ……………………...

20 units @ $3,000

$ 60,000

April 6 …………………………………………..

30 units @ $3,500

105,000

April 17 ………………………………………….

5 units @ $4,500

22,500

April 25 ………………………………………….

10 units @ $4,800

48,000

Units available ……………………………….

65 units

Cost of goods available for sale ……..

$235,500

2. Units in ending inventory

Units available (from part 1) …………..…………..

65 units

Less: Units sold (35 + 25) …………………………..

60 units

Ending Inventory (units) ………………..…………

5 units

Problem 5-1B (Continued)

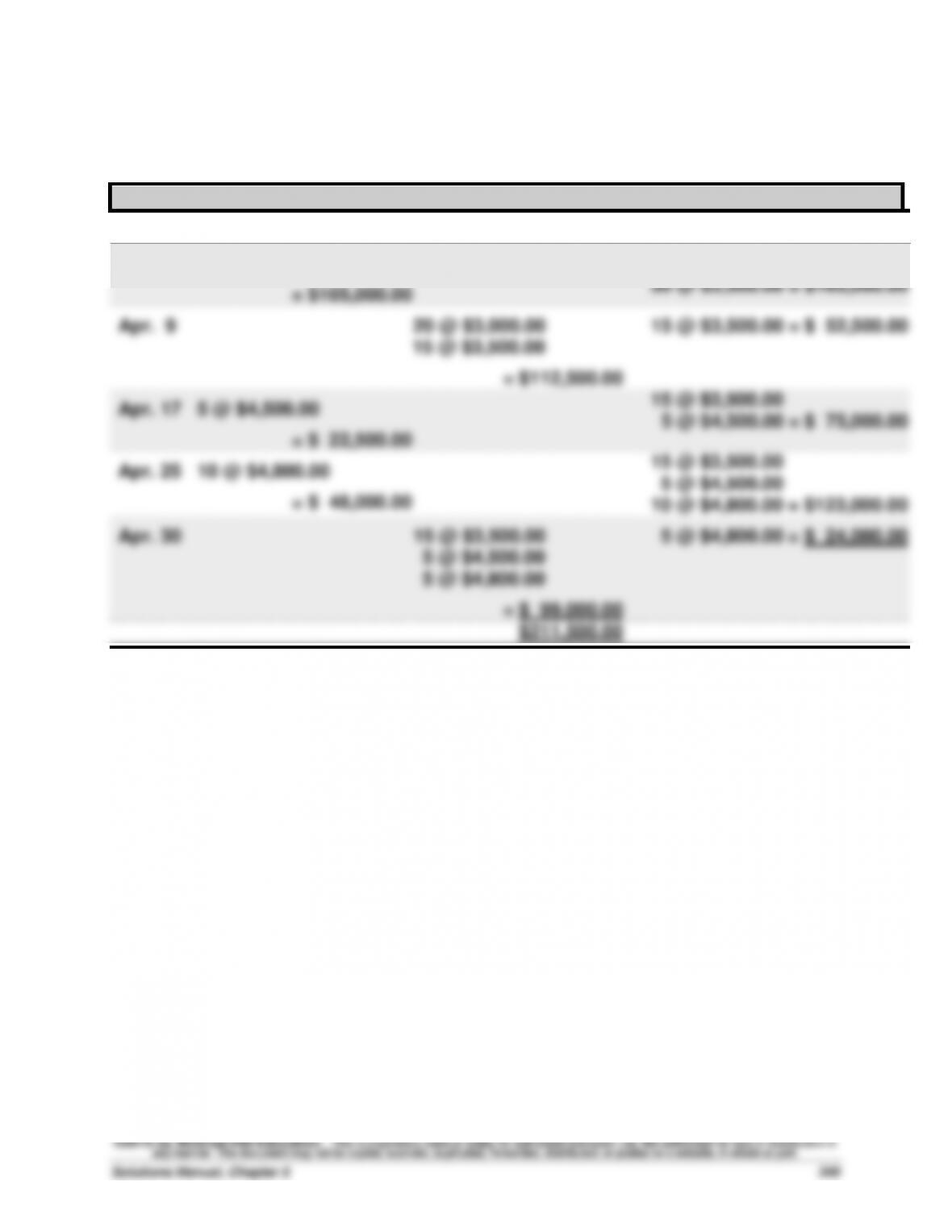

3a. FIFO perpetual

Date

Goods Purchased

Cost of Goods Sold

Inventory Balance

Apr. 1

20 @ $3,000.00 = $ 60,000.00

Apr. 6

30 @ $3,500.00

= $105,000.00

20 @ $3,000.00

30 @ $3,500.00 = $165,000.00

Apr. 9

20 @ $3,000.00

15 @ $3,500.00

= $112,500.00

15 @ $3,500.00 = $ 52,500.00

Apr. 17

5 @ $4,500.00

= $ 22,500.00

15 @ $3,500.00

5 @ $4,500.00 = $ 75,000.00

Apr. 25

10 @ $4,800.00

= $ 48,000.00

15 @ $3,500.00

5 @ $4,500.00

10 @ $4,800.00 = $123,000.00

Apr. 30

15 @ $3,500.00

5 @ $4,500.00

5 @ $4,800.00

= $ 99,000.00

5 @ $4,800.00 = $ 24,000.00

$211,500.00

Problem 5-1B (Continued)

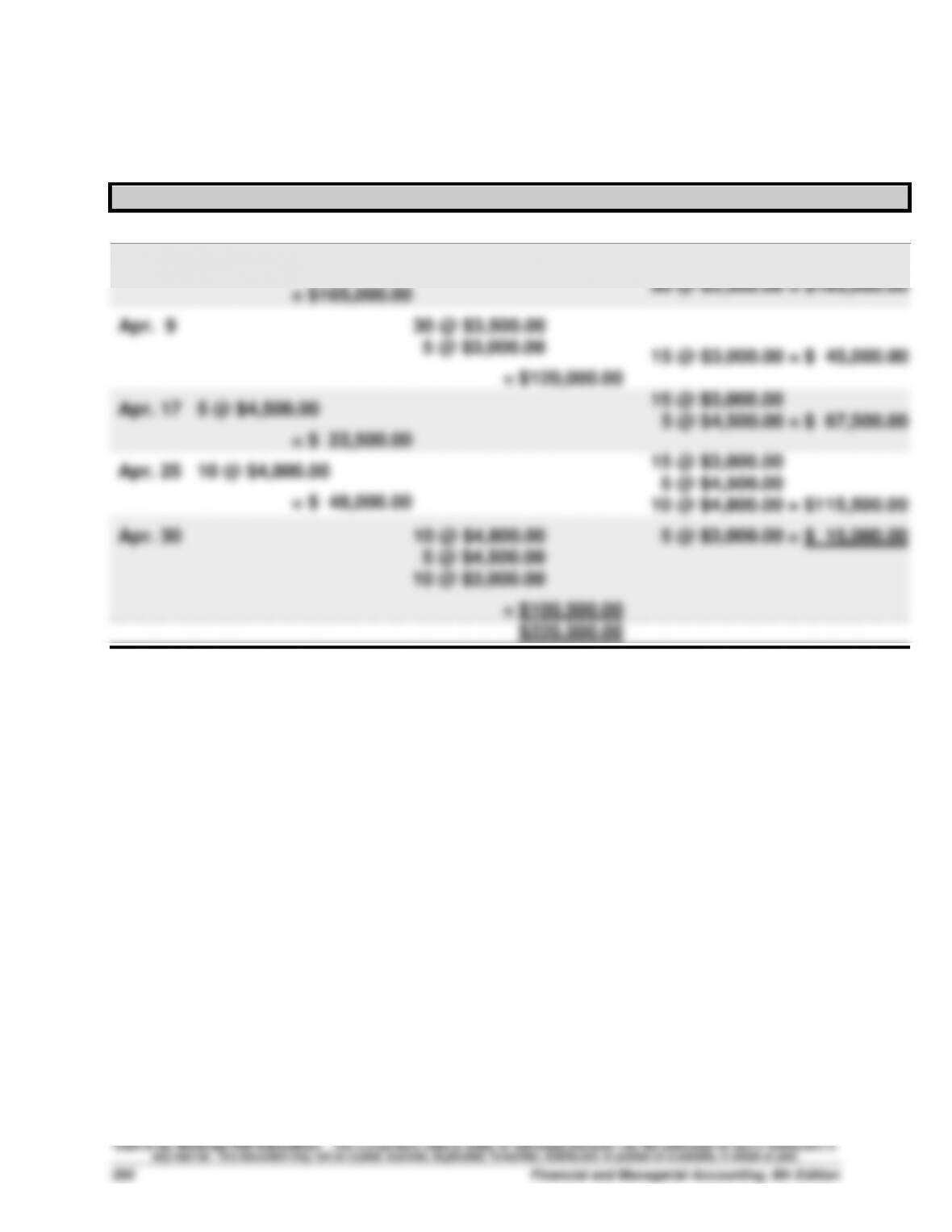

3b. LIFO perpetual

Date

Goods Purchased

Cost of Goods Sold

Inventory Balance

Apr. 1

20 @ $3,000.00 = $ 60,000.00

Apr. 6

30 @ $3,500.00

= $105,000.00

20 @ $3,000.00

30 @ $3,500.00 = $165,000.00

Apr. 9

30 @ $3,500.00

5 @ $3,000.00

= $120,000.00

15 @ $3,000.00 = $ 45,000.00

Apr. 17

5 @ $4,500.00

= $ 22,500.00

15 @ $3,000.00

5 @ $4,500.00 = $ 67,500.00

Apr. 25

10 @ $4,800.00

= $ 48,000.00

15 @ $3,000.00

5 @ $4,500.00

10 @ $4,800.00 = $115,500.00

Apr. 30

10 @ $4,800.00

5 @ $4,500.00

10 @ $3,000.00

= $100,500.00

5 @ $3,000.00 = $ 15,000.00

$220,500.00

Problem 5-1B (Continued)

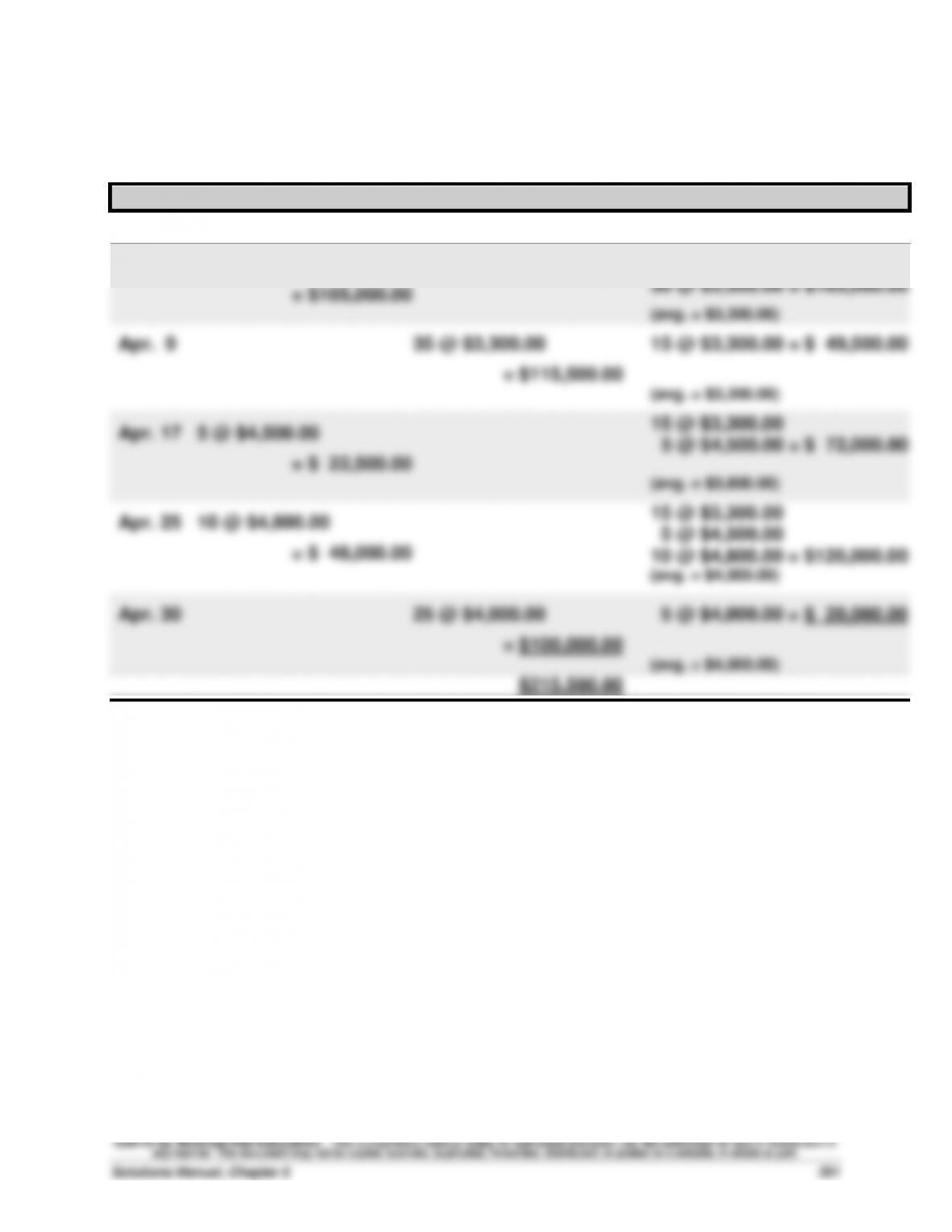

3c. Weighted Average perpetual

Date

Goods Purchased

Cost of Goods Sold

Inventory Balance

Apr. 1

20 @ $3,000.00 = $ 60,000.00

Apr. 6

30 @ $3,500.00

= $105,000.00

20 @ $3,000.00

30 @ $3,500.00 = $165,000.00

(avg. = $3,300.00)

Apr. 9

35 @ $3,300.00

= $115,500.00

15 @ $3,300.00 = $ 49,500.00

(avg. = $3,300.00)

Apr. 17

5 @ $4,500.00

= $ 22,500.00

15 @ $3,300.00

5 @ $4,500.00 = $ 72,000.00

(avg. = $3,600.00)

Apr. 25

10 @ $4,800.00

= $ 48,000.00

15 @ $3,300.00

5 @ $4,500.00

10 @ $4,800.00 = $120,000.00

(avg. = $4,000.00)

Apr. 30

25 @ $4,000.00

= $100,000.00

5 @ $4,000.00 = $ 20,000.00

(avg. = $4,000.00)

$215,500.00

Problem 5-1B (Concluded)

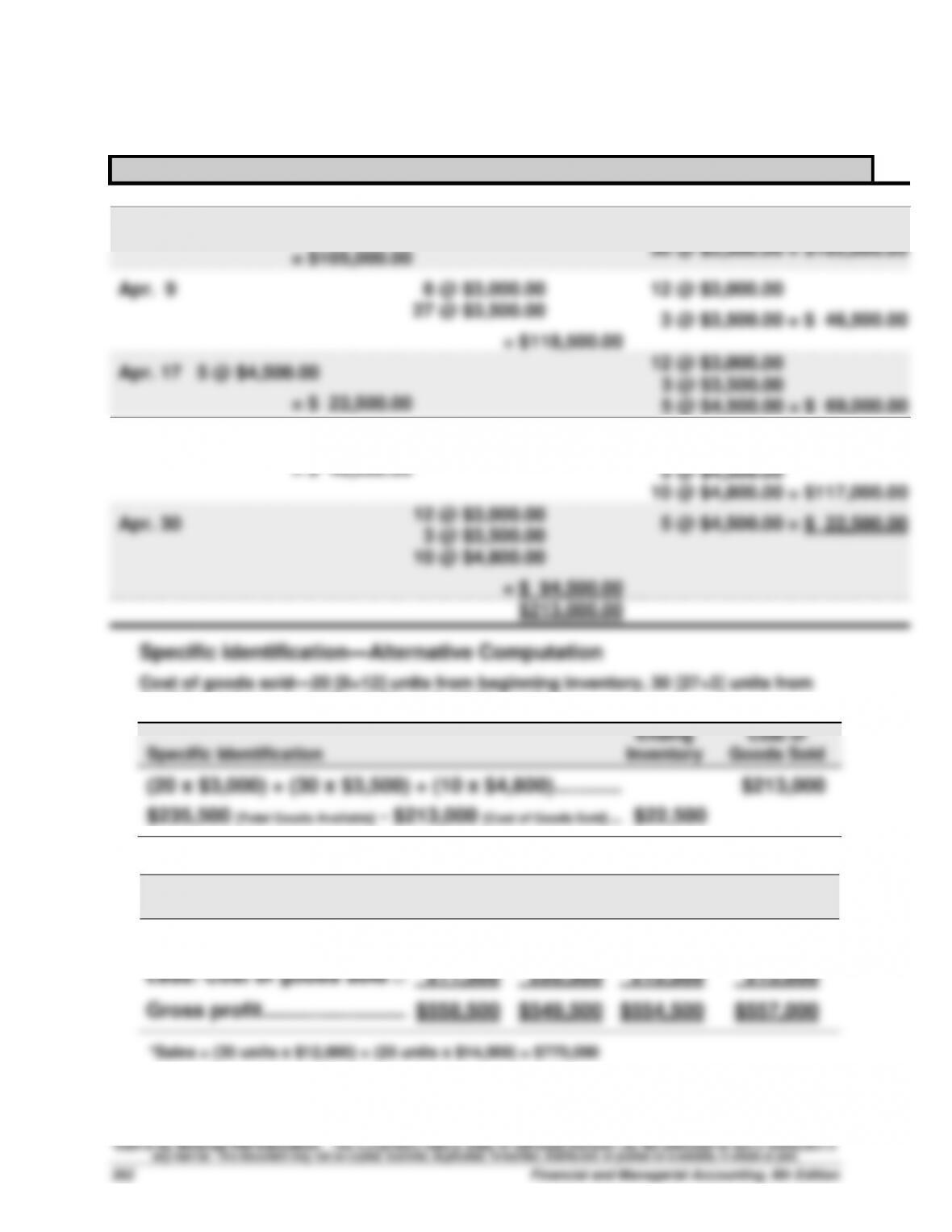

3d. Specific Identification

Date

Goods Purchased

Cost of Goods Sold

Inventory Balance

Apr. 1

20 @ $3,000.00 = $ 60,000.00

Apr. 6

30 @ $3,500.00

= $105,000.00

20 @ $3,000.00

30 @ $3,500.00 = $165,000.00

Apr. 9

8 @ $3,000.00

27 @ $3,500.00

= $118,500.00

12 @ $3,000.00

3 @ $3,500.00 = $ 46,500.00

Apr. 17

5 @ $4,500.00

= $ 22,500.00

12 @ $3,000.00

3 @ $3,500.00

5 @ $4,500.00 = $ 69,000.00

Apr. 25

10 @ $4,800.00

= $ 48,000.00

12 @ $3,000.00

3 @ $3,500.00

5 @ $4,500.00

10 @ $4,800.00 = $117,000.00

Apr. 30

12 @ $3,000.00

3 @ $3,500.00

10 @ $4,800.00

= $ 94,500.00

5 @ $4,500.00 = $ 22,500.00

$213,000.00

Specific identification—Alternative Computation

Cost of goods sold—20 [8+12] units from beginning inventory, 30 [27+3] units from

April 6 purchase, and 10 units from April 25 purchase

4.

FIFO

LIFO

Weighted

Average

Specific

Identification

Sales* ……………………………..…

$770,000

$770,000

$770,000

$770,000

Less: Cost of goods sold ……

211,500

220,500

215,500

213,000

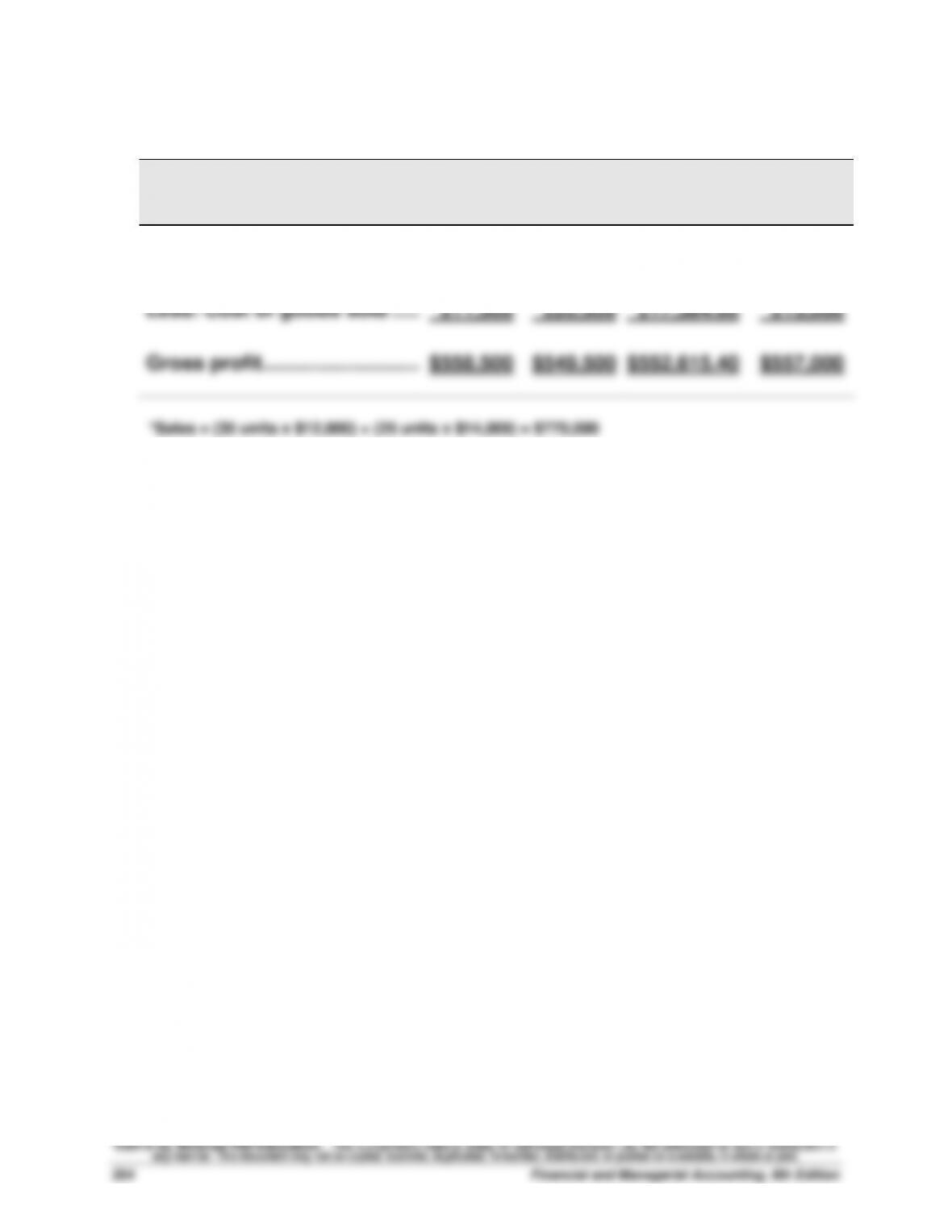

Gross profit ……………………..…

$558,500

$549,500

$554,500

$557,000

*Sales = (35 units x $12,000) + (25 units x $14,000) = $770,000

Problem 5-2B (40 minutes)

1. Compute cost of goods available for sale and units available for sale

Beginning inventory ……………………...

20 units @ $3,000

$ 60,000

April 6 …………………………………………..

30 units @ $3,500

105,000

April 17 …………………………..……………..

5 units @ $4,500

22,500

April 25 …………………………..……………..

10 units @ $4,800

48,000

Units available …………………………..…..

65 units

Cost of goods available for sale ……..

$235,500

2. Units in ending inventory

Units available (from part 1) …………..…………..

65 units

Less: Units sold (35 + 25) …………………………..

60 units

Ending Inventory (units) ………………..…………

5 units

3.

Periodic Inventory

Ending

Inventory

Cost of

Goods Sold

a. FIFO

(5 x $4,800) ……………………………………………………….

$24,000.00

(20x$3,000)+(30x$3,500)+(5x$4,500)+(5x$4,800) …

$211,500.00

b. LIFO

(5 x $3,000) ………………………………………………………

$15,000.00

(15x$3,000)+(30x$3,500)+(5x$4,500)+(10x$4,800)

$220,500.00

c. Weighted average ($235,500/65=$3,623.08 [rounded])

(5 x $3,623.08)…………………………..………………………

$18,115.40

$235,500 [Goods Available] – $18,115.40 [Ending Inventory] ……

$217,384.60

d. Specific identification

(5 x $4,500) ……………………………………………………….

$22,500.00

$235,500 [Goods Available] – $22,500 [Ending Inventory] ………..

$213,000.00

Problem 5-2B (Concluded)

4.

FIFO

LIFO

Weighted

Average

Specific

Identifi-

cation

Sales* ………………………………..

$770,000

$770,000

$770,000.00

$770,000

Less: Cost of goods sold …...

211,500

220,500

217,384.60

213,000

Gross profit ………………………..

$558,500

$549,500

$552,615.40

$557,000

*Sales = (35 units x $12,000) + (25 units x $14,000) = $770,000

Problem 5-3B (40 minutes)

1. Compute cost of goods available for sale and units available for sale

Beginning inventory ……………………...

150 units @ $300

$ 45,000

May 6 …………………………………………...

350 units @ $350

122,500

May 17 …………………………………………..

80 units @ $450

36,000

May 25 …………………………………………..

100 units @ $458

45,800

Units available ……………………………….

680 units

Cost of goods available for sale ……..

$249,300

2. Units in ending inventory

Units available (from part 1) …………..…………..

680 units

Less: Units sold (180 + 300) …………..…………..

480 units

Ending Inventory (units) ………………..…………

200 units

Problem 5-3B (Continued)

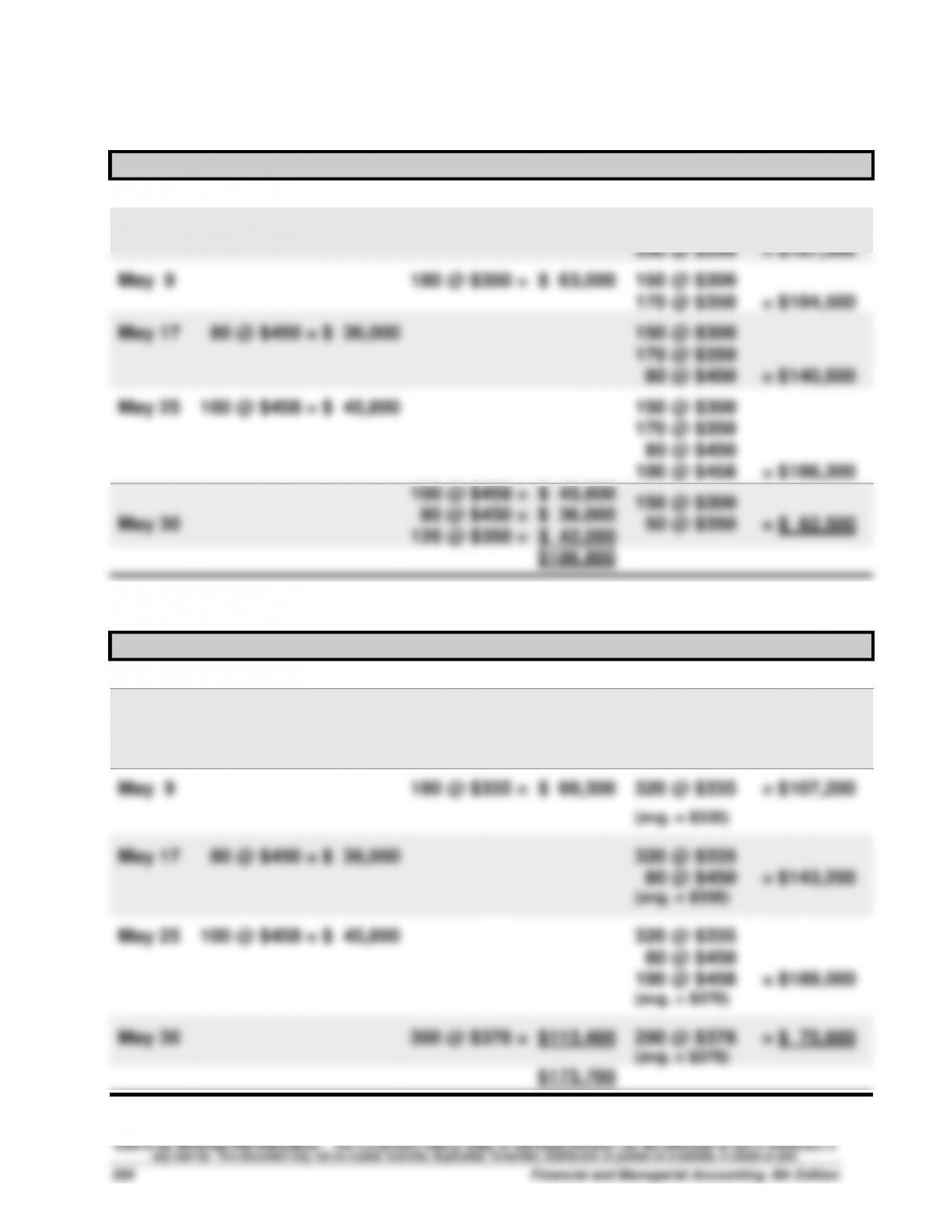

3b. LIFO perpetual

Date

Goods Purchased

Cost of Goods Sold

Inventory Balance

May 1

150 @ $300 = $ 45,000

May 6

350 @ $350 = $122,500

150 @ $300

350 @ $350 = $167,500

May 9

180 @ $350 = $ 63,000

150 @ $300

170 @ $350 = $104,500

May 17

80 @ $450 = $ 36,000

150 @ $300

170 @ $350

80 @ $450 = $140,500

May 25

100 @ $458 = $ 45,800

150 @ $300

170 @ $350

80 @ $450

100 @ $458 = $186,300

May 30

100 @ $458 = $ 45,800

80 @ $450 = $ 36,000

120 @ $350 = $ 42,000

150 @ $300

50 @ $350 = $ 62,500

$186,800

3c. Weighted Average perpetual

Date

Goods Purchased

Cost of Goods Sold

Inventory Balance

May 1

150 @ $300 = $ 45,000

May 6

350 @ $350 = $122,500

150 @ $300

350 @ $350 = $167,500

(avg. = $335)

May 9

180 @ $335 = $ 60,300

320 @ $335 = $107,200

(avg. = $335)

May 17

80 @ $450 = $ 36,000

320 @ $335

80 @ $450 = $143,200

(avg. = $358)

May 25

100 @ $458 = $ 45,800

320 @ $335

80 @ $450

100 @ $458 = $189,000

(avg. = $378)

May 30

300 @ $378 = $113,400

200 @ $378 = $ 75,600

(avg. = $378)

$173,700