Exercise 5-15A (20 minutes)

Periodic Inventory

Ending

Inventory

Cost of

Goods Sold

a. Specific Identification

(50 x $2.80) + (10 x $2.00) ……………………………….

$160.00

$2,540.00 [Goods Available] – $160.00 [Ending Inventory] …….

$2,380.00

b. Weighted Average ($2,540.00/1,000 = $2.54)

(60 x $2.54) …………………………………………………….

152.40

$2,540.00 [Goods Available] – $152.40 [Ending Inventory] …….

2,387.60

c. FIFO

(22 x $2.00) + (38 x 2.30) …………………………………

131.40

(138 x $3.00) + (300 x $2.80) + (502 x $2.30) …….

2,408.60

d. LIFO

(60 x $3.00) …………………………………………………….

180.00

(22 x $2.00) + (540 x $2.30) + (300 x $2.80) +

(78 x $3.00) ……………………………………………….

2,360.00

Income effect: LIFO provides the lowest cost of goods sold, the

highest gross profit, and the highest net income, which is not

unexpected during a period of declining costs.

Exercise 5-16B (20 minutes)

At Cost

At Retail

Goods available for sale

Beginning inventory …………………………………………...

$ 63,800

$128,400

Cost of goods purchased…………………………………....

115,060

196,800

Goods available for sale…………………………..………....

$178,860

325,200

Deduct net sales at retail………………………………………..

260,000

Ending inventory at retail ……………………………………....

$ 65,200

Cost ratio: ($178,860/$325,200) = 0.55 ………………………..

Ending inventory at cost ($65,200 x 55%) ……………....

$ 35,860

Exercise 5-17B (20 minutes)

Goods available for sale

Inventory, January 1 ………………………………………….….

$ 225,000

Net cost of goods purchased* …………………………….….

802,250

Goods available for sale …………………………………….….

1,027,250

Less estimated cost of goods sold

Net sales …………………………..……………………………….….

$1,000,000

Estimated cost of goods sold

[$1,000,000 x (1 – 30%)] …………………………………….

(700,000)

Estimated March 31 inventory ………………………………….

$ 327,250

* $795,000 – $11,550 + $18,800 = $802,250

Exercise 5-18 (15 minutes)

1. Samsung generally applies the (weighted) average cost assumption when

transit.

2. Under IFRS, Samsung would reverse inventory valuation losses if

inventory values increased in subsequent periods. Specifically, it would

2013.

PROBLEM SET A

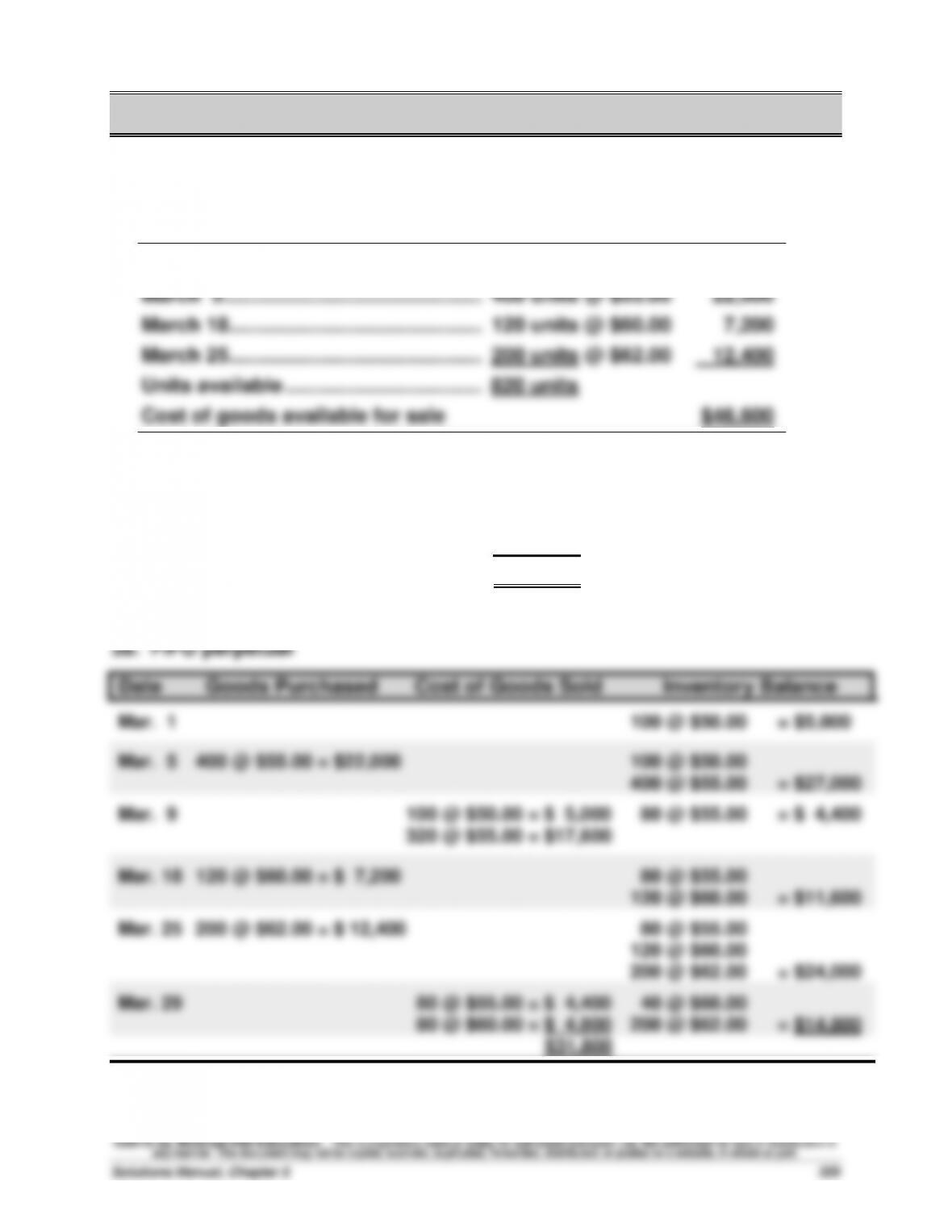

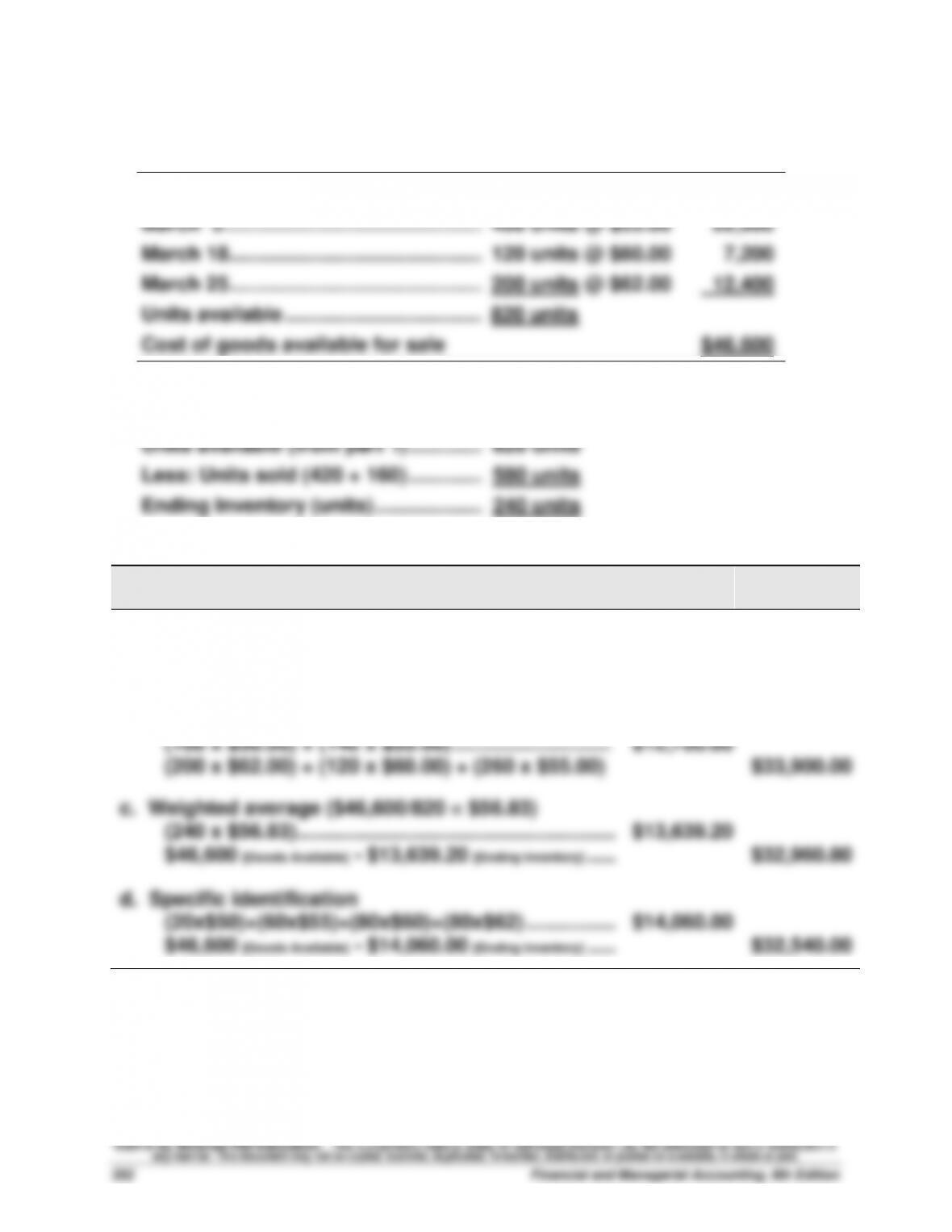

Problem 5-1A (40 minutes)

1. Compute cost of goods available for sale and units available for sale

Beginning inventory ……………………...

100 units @ $50.00

$ 5,000

March 5 ………………………………………...

400 units @ $55.00

22,000

March 18 ………………………………………..

120 units @ $60.00

7,200

March 25 ………………………………………..

200 units @ $62.00

12,400

Units available ……………………………….

820 units

Cost of goods available for sale

$46,600

2. Units in ending inventory

Units available (from part 1) …………..…………..

820 units

Less: Units sold (420 + 160) …………..…………..

580 units

Ending Inventory (units) ………………..…………

240 units

Problem 5-1A (Continued)

3b. LIFO perpetual

Date

Goods Purchased

Cost of Goods Sold

Inventory Balance

Mar. 1

100 @ $50.00 = $ 5,000

Mar. 5

400@ $55.00= $22,000

100 @ $50.00

400 @ $55.00 = $27,000

Mar. 9

400 @ $55.00 = $22,000

20 @ $50.00 = $ 1,000

80 @ $50.00 = $ 4,000

Mar. 18

120@ $60.00= $ 7,200

80 @ $50.00

120 @ $60.00 = $11,200

Mar. 25

200@ $62.00= $12,400

80 @ $50.00

120 @ $60.00

200 @ $62.00 = $23,600

Mar. 29

160 @ $62.00 = $ 9,920

80 @ $50.00

120 @ $60.00

40 @ $62.00 = $13,680

$32,920

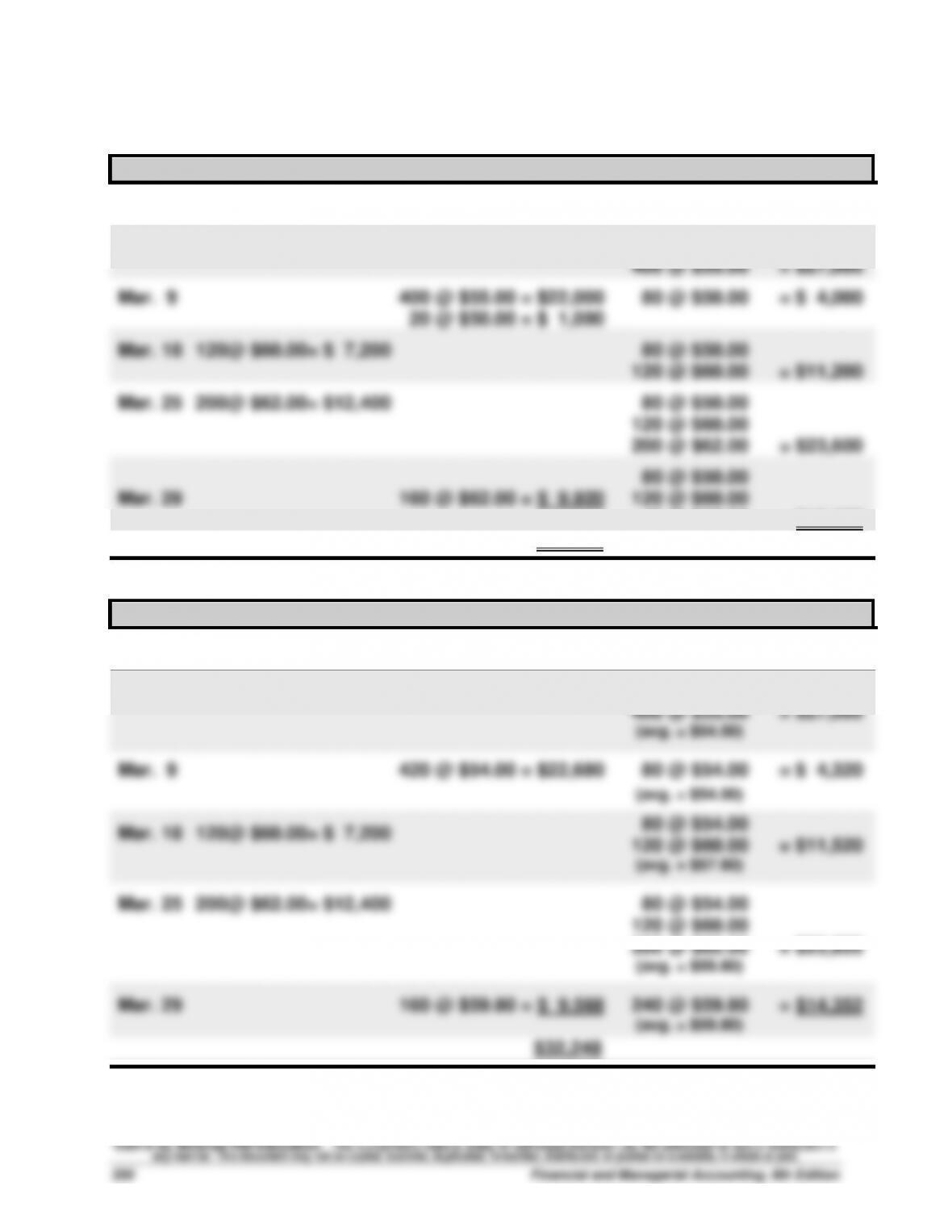

3c. Weighted Average perpetual

Date

Goods Purchased

Cost of Goods Sold

Inventory Balance

Mar. 1

100 @ $50.00 = $ 5,000

Mar. 5

400@ $55.00= $22,000

100 @ $50.00

400 @ $55.00 = $27,000

(avg. = $54.00)

Mar. 9

420 @ $54.00 = $22,680

80 @ $54.00 = $ 4,320

(avg. = $54.00)

Mar. 18

120@ $60.00= $ 7,200

80 @ $54.00

120 @ $60.00 = $11,520

(avg. = $57.60)

Mar. 25

200@ $62.00= $12,400

80 @ $54.00

120 @ $60.00

200 @ $62.00 = $23,920

(avg. = $59.80)

Mar. 29

160 @ $59.80 = $ 9,568

240 @ $59.80 = $14,352

(avg. = $59.80)

$32,248

Problem 5-1A (Concluded)

3d. Specific Identification

Date

Goods Purchased

Cost of Goods Sold

Inventory Balance

Mar. 1

100 @ $50.00 = $ 5,000

Mar. 5

400 @ $55.00 = $22,000

100 @ $50.00

400 @ $55.00 = $27,000

Mar. 9

80 @ $50.00 = $ 4,000

340 @ $55.00 = $18,700

20 @ $50.00

60 @ $55.00 = $ 4,300

Mar. 18

120 @ $60.00 = $ 7,200

20 @ $50.00

60 @ $55.00

120 @ $60.00 = $11,500

Mar. 25

200 @ $62.00 = $12,400

20 @ $50.00

60 @ $55.00

120 @ $60.00

200 @ $62.00 = $23,900

Mar. 29

40 @ $60.00 = $ 2,400

120 @ $62.00 = $ 7,440

20 @ $50.00

60 @ $55.00

80 @ $60.00

80 @ $62.00 = $14,060

$32,540

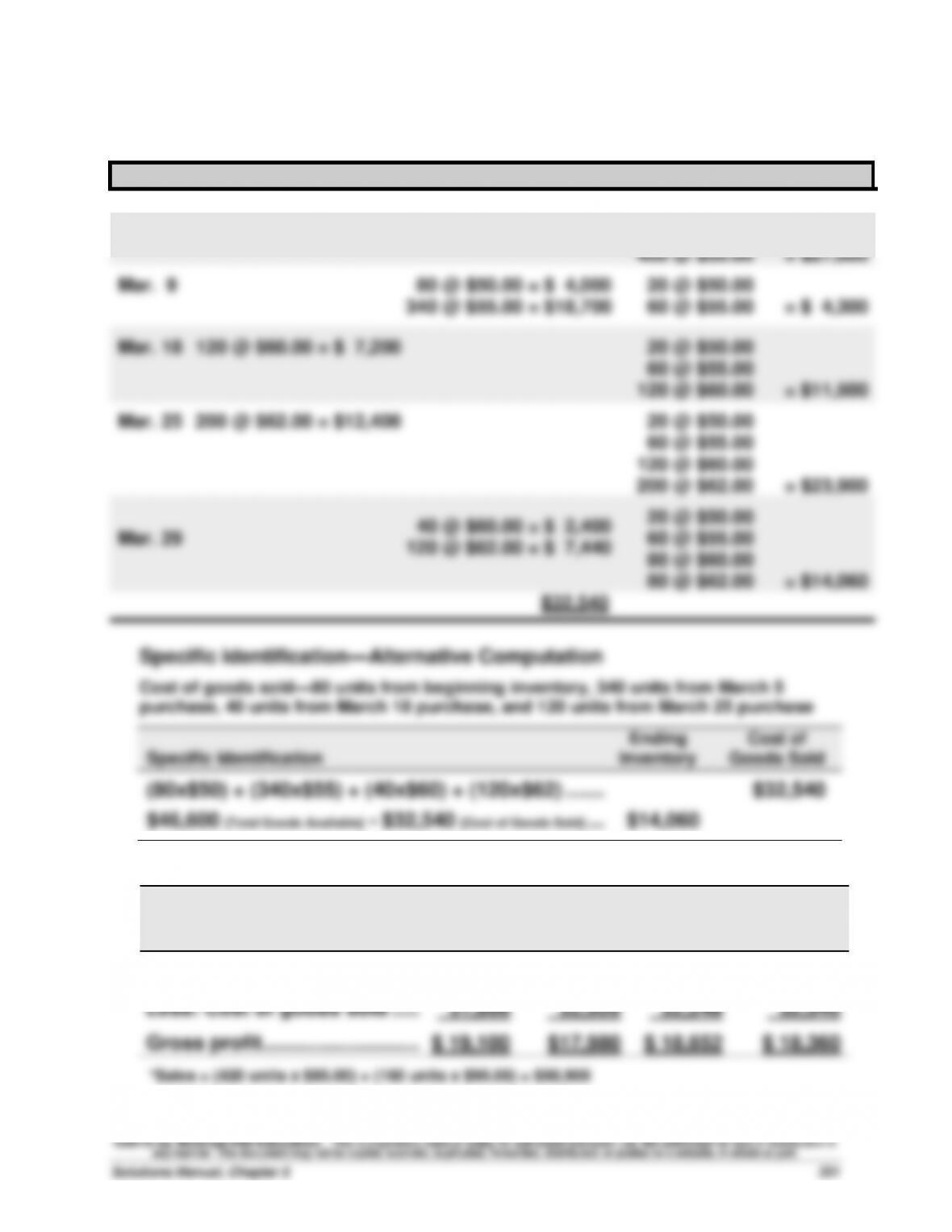

Specific identification—Alternative Computation

Cost of goods sold—80 units from beginning inventory, 340 units from March 5

purchase, 40 units from March 18 purchase, and 120 units from March 25 purchase

Ending Cost of

Specific Identification Inventory Goods Sold

(80x$50) + (340x$55) + (40x$60) + (120x$62) ……. $32,540

$46,600 [Total Goods Available] – $32,540 [Cost of Goods Sold] … $14,060

4.

FIFO

LIFO

Weighted

Average

Specific

Identifi-

cation

Sales* ………………………………..

$50,900

$50,900

$50,900

$50,900

Less: Cost of goods sold …...

31,800

32,920

32,248

32,540

Gross profit ………………………..

$ 19,100

$17,980

$ 18,652

$ 18,360

*Sales = (420 units x $85.00) + (160 units x $95.00) = $50,900

Problem 5-2A (40 minutes)

1. Compute cost of goods available for sale and units available for sale

Beginning inventory ……………………...

100 units @ $50.00

$ 5,000

March 5 ………………………………………...

400 units @ $55.00

22,000

March 18 ………………………………………..

120 units @ $60.00

7,200

March 25 ………………………………………..

200 units @ $62.00

12,400

Units available ……………………………….

820 units

Cost of goods available for sale

$46,600

2. Units in ending inventory

Units available (from part 1) …………..…………..

820 units

Less: Units sold (420 + 160) …………..…………..

580 units

Ending Inventory (units) ………………..…………

240 units

3.

Periodic Inventory

Ending

Inventory

Cost of

Goods Sold

a. FIFO

(200 x $62.00) + (40 x $60.00) ………………………….

$14,800.00

(100 x $50.00) + (400 x $55.00) + (80 x $60.00) …

$31,800.00

b. LIFO

(100 x $50.00) + (140 x $55.00) ……………………….

$12,700.00

(200 x $62.00) + (120 x $60.00) + (260 x $55.00)

$33,900.00

c. Weighted average ($46,600/820 = $56.83)

(240 x $56.83)…………………………..…………………….

$13,639.20

$46,600 [Goods Available] – $13,639.20 [Ending Inventory] …..

$32,960.80

d. Specific identification

(20x$50)+(60x$55)+(80x$60)+(80x$62) …………….

$14,060.00

$46,600 [Goods Available] – $14,060.00 [Ending Inventory] …..

$32,540.00

Problem 5-2A (Concluded)

4.

FIFO

LIFO

Weighted

Average

Specific

Identifi-

cation

Sales* ………………………………..

$50,900.00

$50,900.00

$50,900.00

$50,900.00

Less: Cost of goods sold …...

31,800.00

33,900.00

32,960.80

32,540.00

Gross profit ………………………..

$19,100.00

$17,000.00

$17,939.20

$18,360.00

*Sales = (420 units x $85.00) + (160 units x $95.00) = $50,900

Problem 5-3A (40 minutes)

1. Calculate cost of goods available for sale and units available for sale

Beginning inventory ……………………...

600 units @ $45.00

$27,000

Feb. 10 …………………………..……………..

400 units @ $42.00

16,800

Mar. 13 ………………………………………….

200 units @ $27.00

5,400

Aug. 21 ………………………………………….

100 units @ $50.00

5,000

Sept. 5 ………………………………………….

500 units @ $46.00

23,000

Units available ……………………………….

1,800 units

Cost of goods available for sale

$77,200

2. Units in ending inventory

Units available (from part 1) …………..…………..

1,800

Less: Units sold (800+600) …………….…………..

1,400

Ending Inventory (units) ………………..…………

400

Problem 5-3A (Continued)

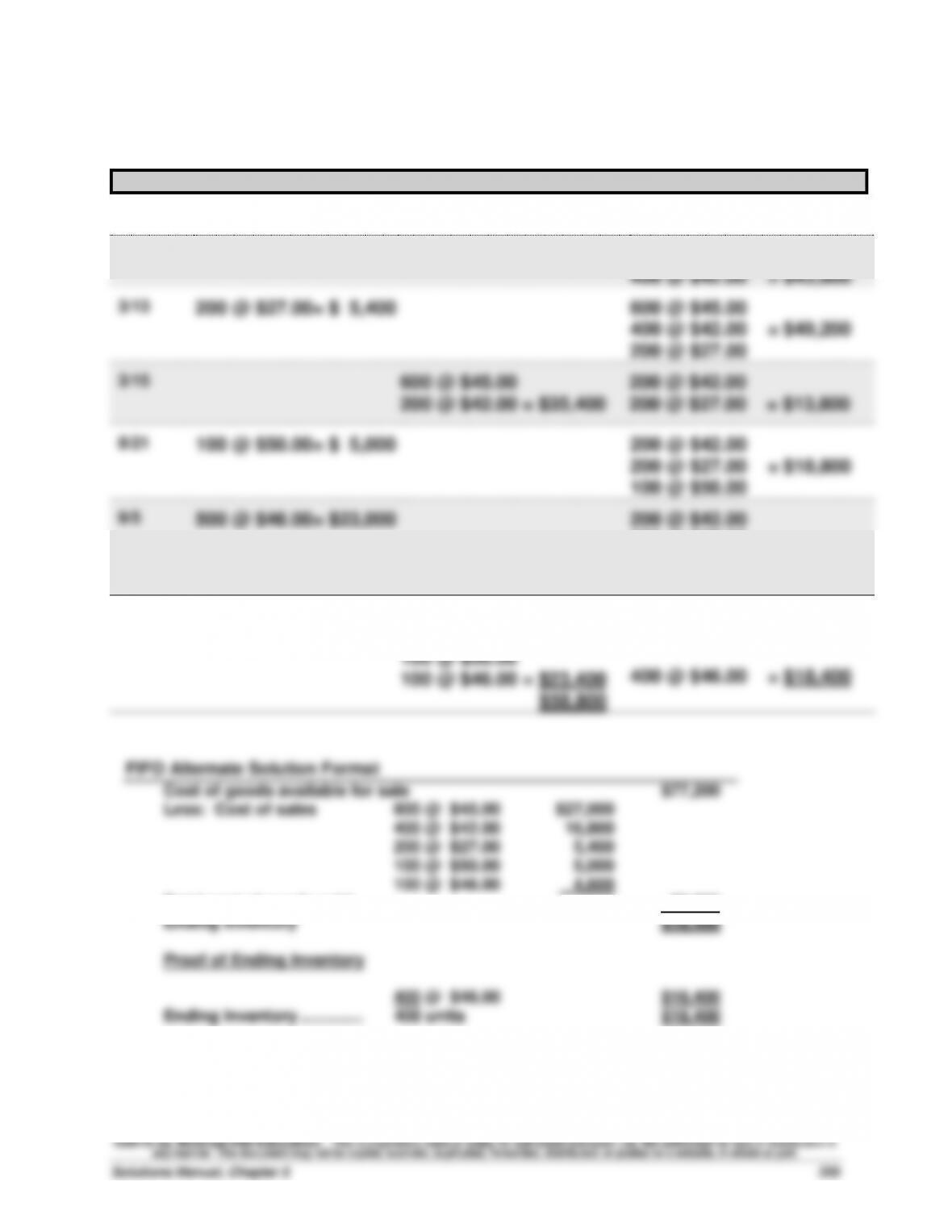

3a. FIFO perpetual

Date

Goods Purchasd

Cost of Goods Sold

Inventory Balance

1/1

600 @ $45.00 = $27,000

2/10

400 @ $42.00= $16,800

600 @ $45.00

400 @ $42.00 = $43,800

3/13

200 @ $27.00= $ 5,400

600 @ $45.00

400 @ $42.00 = $49,200

200 @ $27.00

3/15

600 @ $45.00

200 @ $42.00 = $35,400

200 @ $42.00

200 @ $27.00 = $13,800

8/21

100 @ $50.00= $ 5,000

200 @ $42.00

200 @ $27.00 = $18,800

100 @ $50.00

9/5

500 @ $46.00= $23,000

200 @ $42.00

200 @ $27.00

100 @ $50.00

500 @ $46.00 = $41,800

9/10

200 @ $42.00

200 @ $27.00

100 @ $50.00

100 @ $46.00 = $23,400

400 @ $46.00 = $18,400

$58,800

FIFO Alternate Solution Format

Cost of goods available for sale

$77,200

Less: Cost of sales

600 @ $45.00

$27,000

400 @ $42.00

16,800

200 @ $27.00

5,400

100 @ $50.00

5,000

100 @ $46.00

4,600

Total cost of goods sold

58,800

Ending Inventory

$18,400

Proof of Ending Inventory

400 @ $46.00

$18,400

Ending Inventory ……………..

400 units

$18,400

Problem 5-3A (Continued)

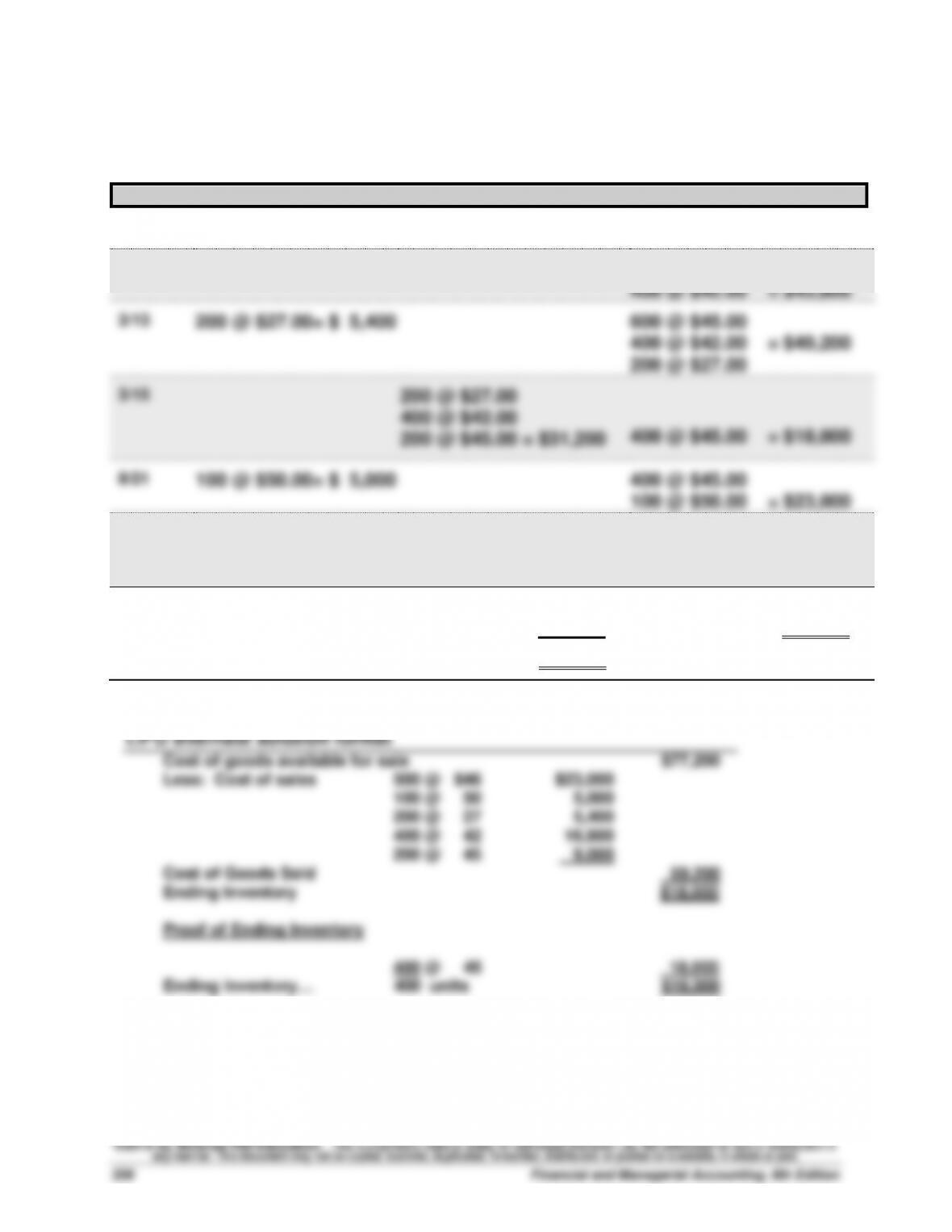

3b. LIFO perpetual

Date

Goods Purchased

Cost of Goods Sold

Inventory Balance

1/1

600 @ $45.00 = $27,000

2/10

400 @ $42.00= $16,800

600 @ $45.00

400 @ $42.00 = $43,800

3/13

200 @ $27.00= $ 5,400

600 @ $45.00

400 @ $42.00 = $49,200

200 @ $27.00

3/15

200 @ $27.00

400 @ $42.00

200 @ $45.00 = $31,200

400 @ $45.00 = $18,000

8/21

100 @ $50.00= $ 5,000

400 @ $45.00

100 @ $50.00 = $23,000

9/5

500 @ $46.00= $23,000

400 @ $45.00

100 @ $50.00

500 @ $46.00 = $46,000

9/10

500 @ $46.00

100 @ $50.00 = $28,000

400 @ $45.00 = $18,000

$59,200