EXERCISES

Exercise 5-1 (10 minutes)

1. The title will pass at “destination” which is Harlow Company’s

2. The consignor is Harris Company. The consignee is Harlow Company.

Exercise 5-2 (10 minutes)

Cost of inventory (estate’s contents)

Price …………………………………………………………………………….

$75,000

Transportation-in ………………………………………………………….

2,400

Insurance on shipment ………………………………………………….

300

Cleaning and refurbishing……………………………………………..

980

Total cost of inventory…………………………..……………………...

$78,680

Exercise 5-3 (45 minutes)

a. Specific identification

Exercise 5-3 (continued)

b. Weighted Average—Perpetual

Date

Goods Purchased

Cost of Goods Sold

Inventory Balance

1/1

140 @ $6.00

= $ 840.00

1/10

100 @ $6.00 = $ 600.00

40 @ $6.00

= $ 240.00

1/20

60 @ $5.00

40 @ $6.00

= $ 540.00

60 @ $5.00

(avg. cost is $5.40)

1/25

80 @ $5.40 = $ 432.00

20 @ $5.40

= $ 108.00

1/30

180 @ $4.50

20 @ $5.40

= $ 918.00

$1,032.00

180 @ $4.50

(avg. cost is $4.59)

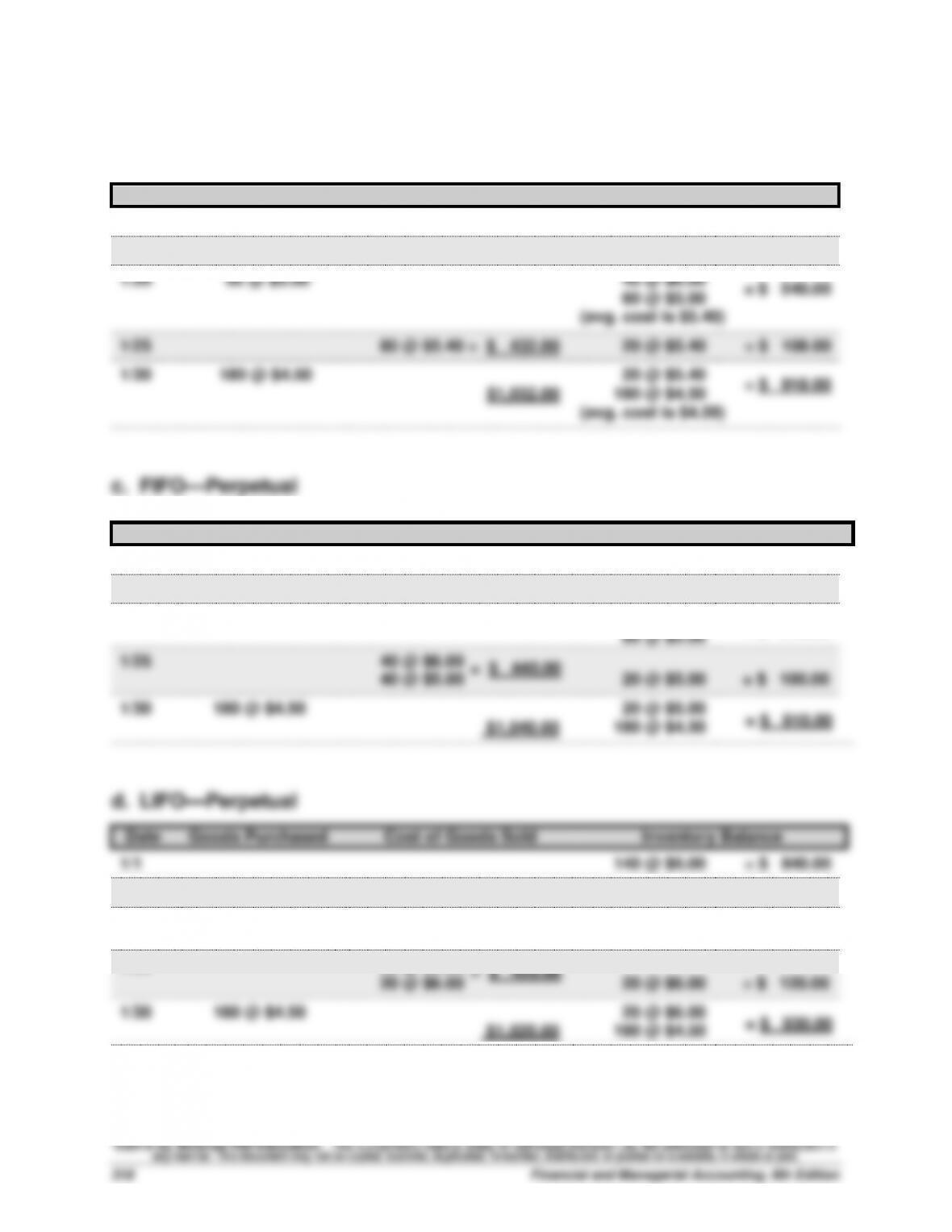

c. FIFO—Perpetual

Date

Goods Purchased

Cost of Goods Sold

Inventory Balance

1/1

140 @ $6.00

= $ 840.00

1/10

100 @ $6.00 = $ 600.00

40 @ $6.00

= $ 240.00

1/20

60 @ $5.00

40 @ $6.00

= $ 540.00

60 @ $5.00

1/25

40 @ $6.00

40 @ $5.00

20 @ $5.00

= $ 100.00

1/30

180 @ $4.50

20 @ $5.00

= $ 910.00

$1,040.00

180 @ $4.50

1/1

140 @ $6.00

= $ 840.00

1/10

40 @ $6.00

= $ 240.00

1/20

40 @ $6.00

= $ 540.00

60 @ $5.00

1/25

1/30

20 @ $6.00

180 @ $4.50

= $ 440.00

Exercise 5-3 (Concluded)

Alternate Solution Format for FIFO and LIFO Perpetual

Ending Cost of

Exercise 5-4 (20 minutes)

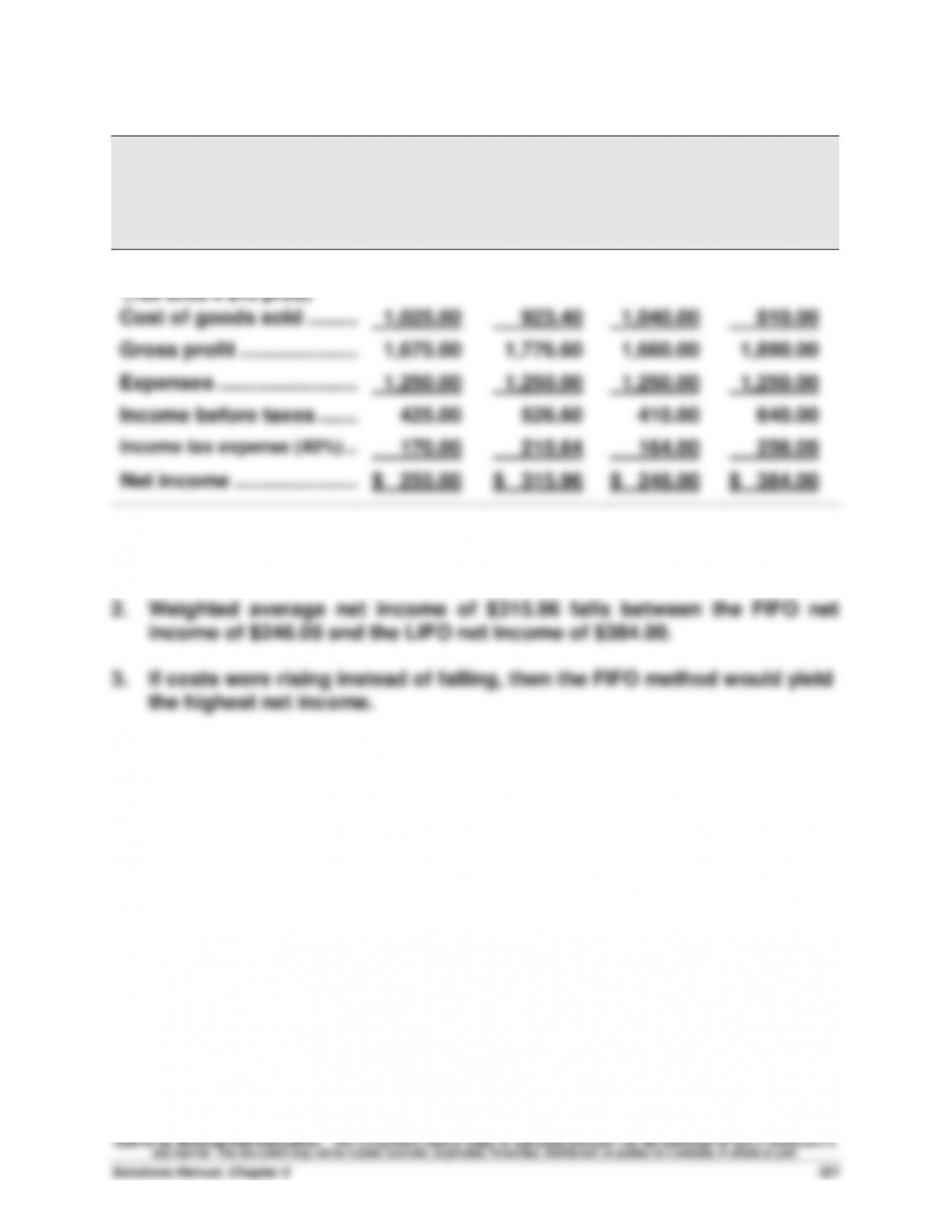

LAKER COMPANY

Income Statements

For Month Ended January 31

Specific

Identification

Weighted

Average

FIFO

LIFO

Sales ………………………………..

$2,700.00

$2,700.00

$2,700.00

$2,700.00

(180 units x $15 price)

Cost of goods sold …………..

1,025.00

1,032.00

1,040.00

1,020.00

Gross profit ……………………..

1,675.00

1,668.00

1,660.00

1,680.00

Expenses …………………….…..

1,250.00

1,250.00

1,250.00

1,250.00

Income before taxes …….…..

425.00

418.00

410.00

430.00

Income tax expense (40%) ………

170.00

167.20

164.00

172.00

Net income ………………….…..

$ 255.00

$ 250.80

$ 246.00

$ 258.00

1. LIFO method results in the highest net income of $258.00.

Exercise 5-5A (35 minutes)

Ending Cost of

Periodic Inventory Computations Inventory Goods Sold

a. Specific Identification—Periodic

Exercise 5-6 (20 minutes)

LAKER COMPANY

Income Statements

For Month Ended January 31

Specific

Identification

Weighted

Average

FIFO

LIFO

Sales ………………………………..

$2,700.00

$2,700.00

$2,700.00

$2,700.00

(180 units x $15 price)

Cost of goods sold …………..

1,025.00

923.40

1,040.00

810.00

Gross profit ……………………..

1,675.00

1,776.60

1,660.00

1,890.00

Expenses …………………….…..

1,250.00

1,250.00

1,250.00

1,250.00

Income before taxes …….…..

425.00

526.60

410.00

640.00

Income tax expense (40%) ………

170.00

210.64

164.00

256.00

Net income ………………….…..

$ 255.00

$ 315.96

$ 246.00

$ 384.00

1. LIFO method results in the highest net income of $384.00.

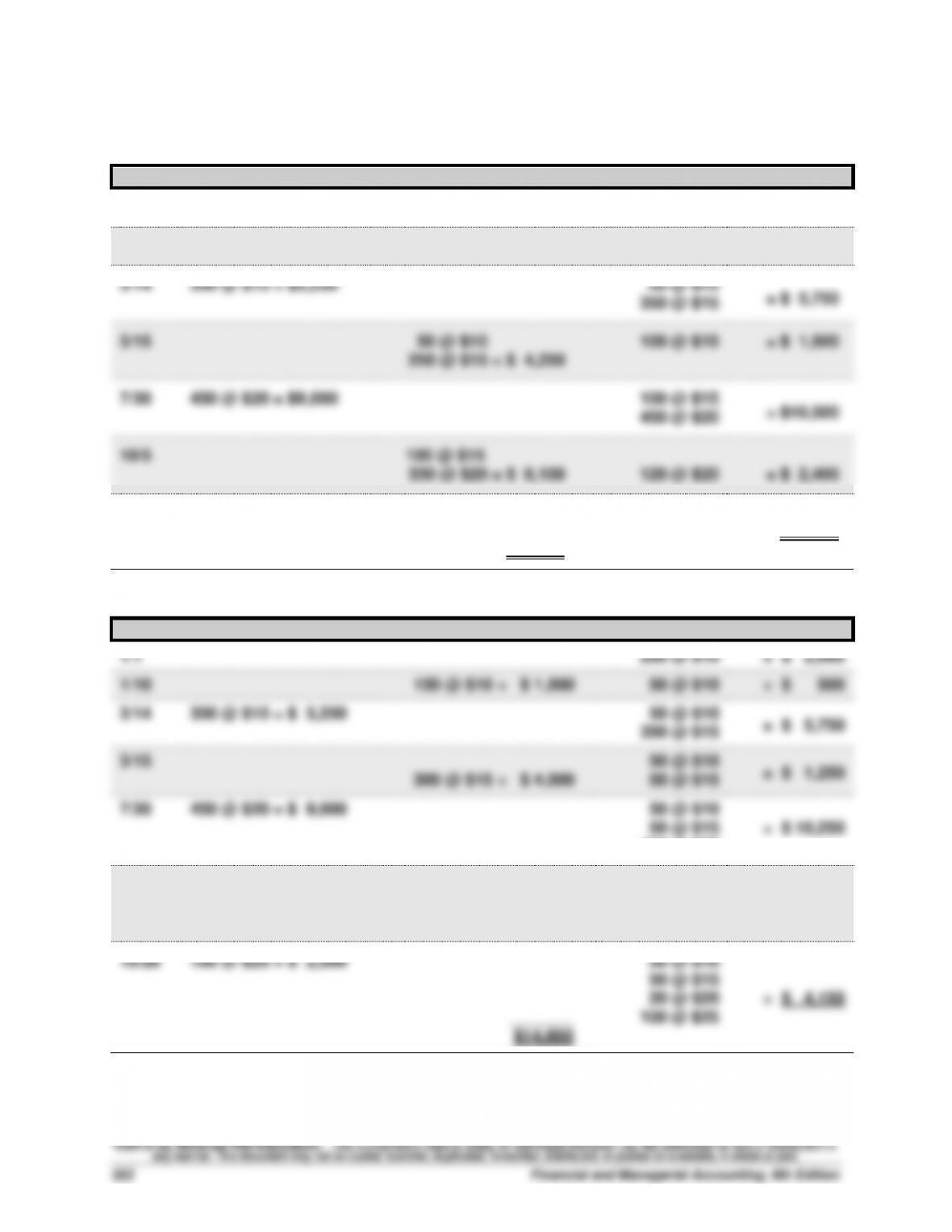

Exercise 5-7 (20 minutes)

a. FIFO—Perpetual

Date

Goods Purchased

Cost of Goods Sold

Inventory Balance

1/1

200 @ $10

= $ 2,000

1/10

150 @ $10 = $ 1,500

50 @ $10

= $ 500

3/14

350 @ $15 = $5,250

50 @ $10

= $ 5,750

350 @ $15

3/15

50 @ $10

100 @ $15

= $ 1,500

250 @ $15 = $ 4,250

7/30

450 @ $20 = $9,000

100 @ $15

= $10,500

450 @ $20

10/5

100 @ $15

330 @ $20 = $ 8,100

120 @ $20

= $ 2,400

10/26

100 @ $25 = $2,500

120 @ $20

______

100 @ $25

= $ 4,900

$13,850

b. LIFO—Perpetual

Date

Goods Purchased

Cost of Goods Sold

Inventory Balance

1/1

200 @ $10

= $ 2,000

1/10

150 @ $10 = $ 1,500

50 @ $10

= $ 500

3/14

350 @ $15 = $ 5,250

50 @ $10

= $ 5,750

350 @ $15

3/15

50 @ $10

= $ 1,250

300 @ $15 = $ 4,500

50 @ $15

7/30

450 @ $20 = $ 9,000

50 @ $10

50 @ $15

= $ 10,250

450 @ $20

10/5

50 @ $10

430 @ $20 = $8,600

50 @ $15

= $ 1,650

20 @ $20

10/26

100 @ $25 = $ 2,500

50 @ $10

50 @ $15

20 @ $20

= $ 4,150

_______

100 @ $25

$14,600

Exercise 5-7 (Concluded)

Alternate Solution Format

Ending Cost of

Inventory Goods Sold

a. FIFO

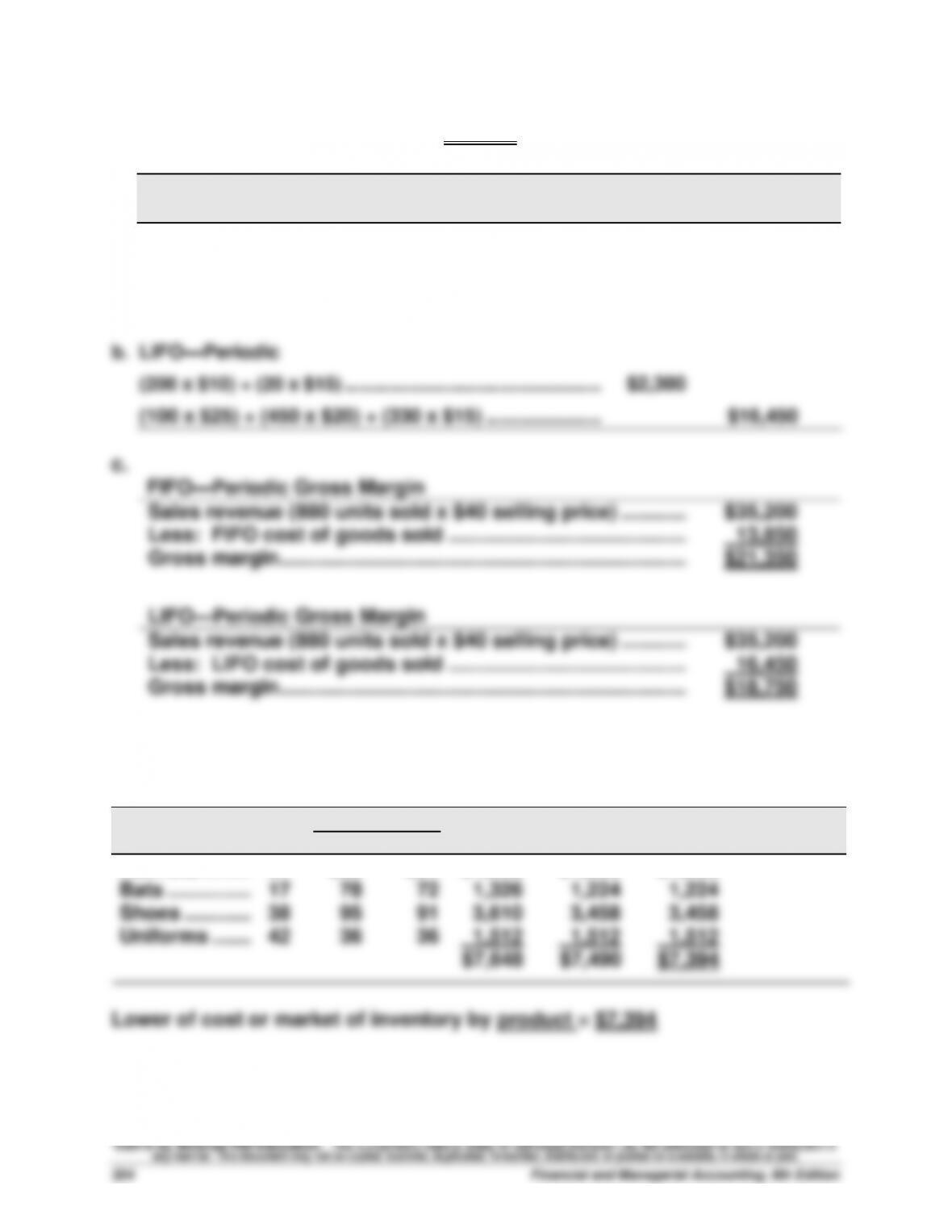

Exercise 5-9A (20 minutes)

Cost of goods available for sale = $18,750 (given in Exercise 5-7)

Ending Cost of

Periodic Inventory System Inventory Goods Sold

a. FIFO—Periodic

(100 x $25) + (120 x $20) ……………………………………… $4,900

(200 x $10) + (350 x $15) + (330 x $20) …………………. $13,850

Exercise 5-10 (15 minutes)

Per Unit

Total

Total

LCM Applied

to Items

Inventory Items

Units

Cost

Market

Cost

Market

Helmets ………..

24

$50

$54

$1,200

$1,296

$1,200

Bats ……………..

17

78

72

1,326

1,224

1,224

Shoes …………..

38

95

91

3,610

3,458

3,458

Uniforms ……...

42

36

36

1,512

1,512

1,512

$7,648

$7,490

$7,394

Lower of cost or market of inventory by product = $7,394

Exercise 5-11 (20 minutes)

1. a. LIFO ratio computations

LIFO current ratio (2015) = $220/$200 = 1.1

LIFO inventory turnover (2015) = $740/ [($110+$160)/2] = 5.5

2. The use of LIFO versus FIFO for Cruz markedly impacts the ratios computed.

Specifically, LIFO makes Cruz appear worse in comparison to FIFO numbers

on the current ratio (1.1 vs. 1.5) but better on inventory turnover (5.5 vs. 3.8)

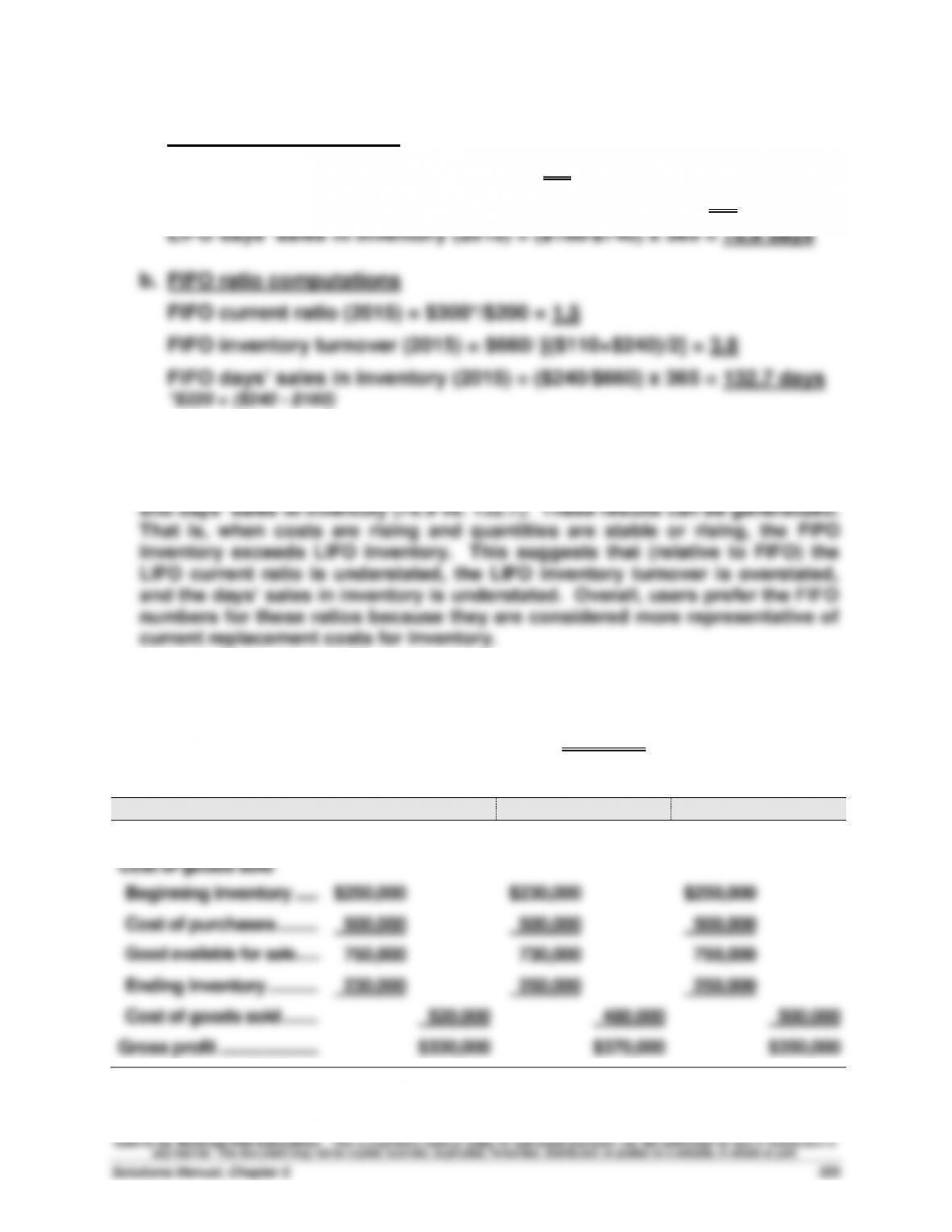

Exercise 5-12 (25 minutes)

1. Correct gross profit = $850,000 – $500,000 = $350,000 (for each year)

2. Reported income figures

Year 2014

Year 2015

Year 2016

Sales …………………………….

$850,000

$850,000

$850,000

Cost of goods sold

Beginning inventory …..

$250,000

$230,000

$250,000

Cost of purchases ………

500,000

500,000

500,000

Good available for sale ……

750,000

730,000

750,000

Ending inventory ………..

230,000

250,000

250,000

Cost of goods sold ……..

520,000

480,000

500,000

Gross profit ………………….

$330,000

$370,000

$350,000

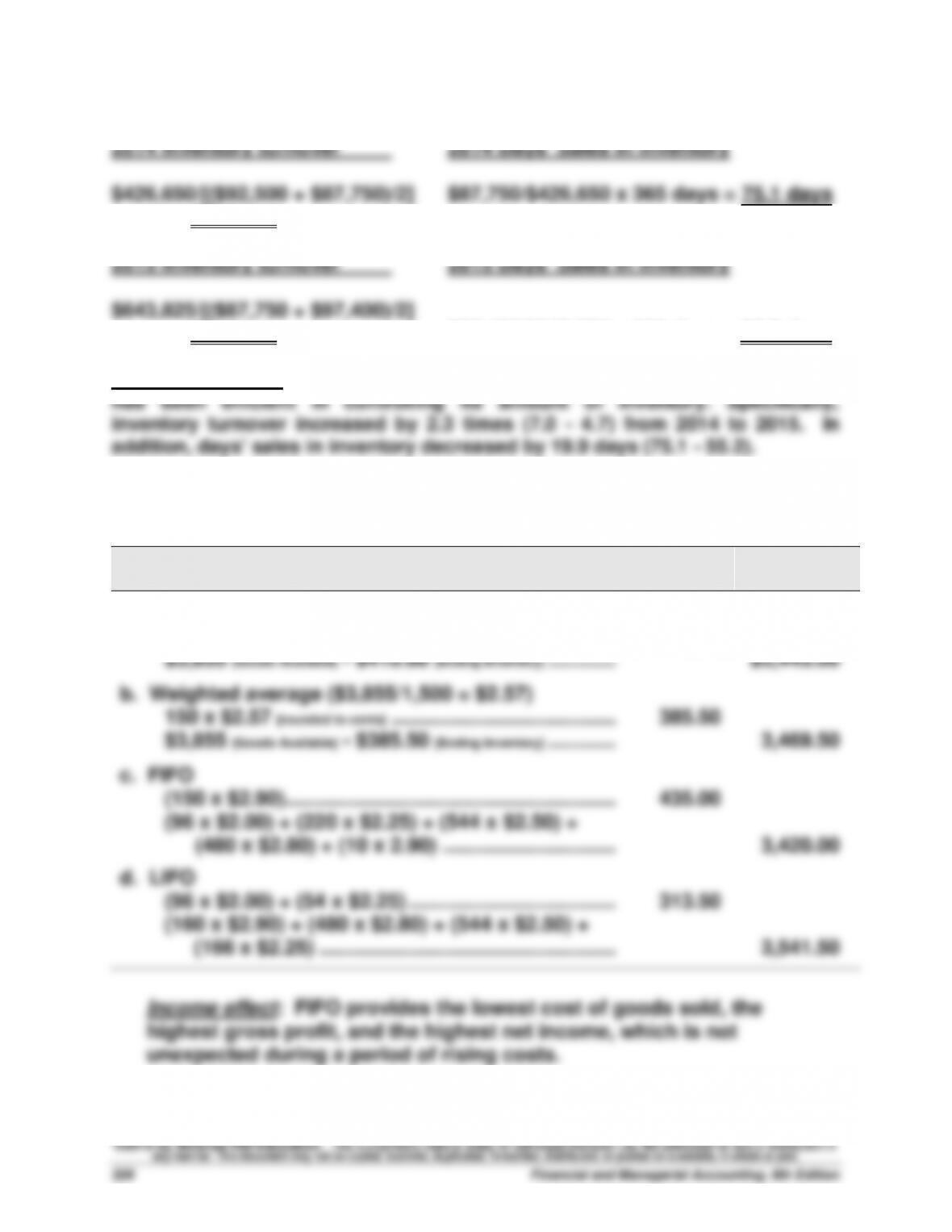

Exercise 5-13 (20 minutes)

= 4.7 times

= 7.0 times $97,400/$643,825 x 365 days = 55.2 days

Analysis comment: It appears that during a period of increasing sales, Palmer

Exercise 5-14A (20 minutes)

Ending

Inventory

Cost of

Goods Sold

a. Specific identification

(50 x $2.90) + (50 x $2.80) + (50 x $2.50) ………….

$410.00

$3,855 [Goods Available] – $410.00 [Ending Inventory] …………

$3,445.00

b. Weighted average ($3,855/1,500 = $2.57)

150 x $2.57 [rounded to cents] ………………………………….

385.50

$3,855 [Goods Available] – $385.50 [Ending Inventory] …………

3,469.50

c. FIFO

(150 x $2.90)…………………………..………………………

435.00

(96 x $2.00) + (220 x $2.25) + (544 x $2.50) +

(480 x $2.80) + (10 x 2.90) ………………………….

3,420.00

d. LIFO

(96 x $2.00) + (54 x $2.25) ……………………………….

313.50

(160 x $2.90) + (480 x $2.80) + (544 x $2.50) +

(166 x $2.25) …………………………..…………………

3,541.50

Income effect: FIFO provides the lowest cost of goods sold, the

highest gross profit, and the highest net income, which is not

unexpected during a period of rising costs.