EXERCISES

Exercise 4-1 (30 minutes)

Note: The original missing numbers are blocked.

(a)

(b)

(c)

(d)

(e)

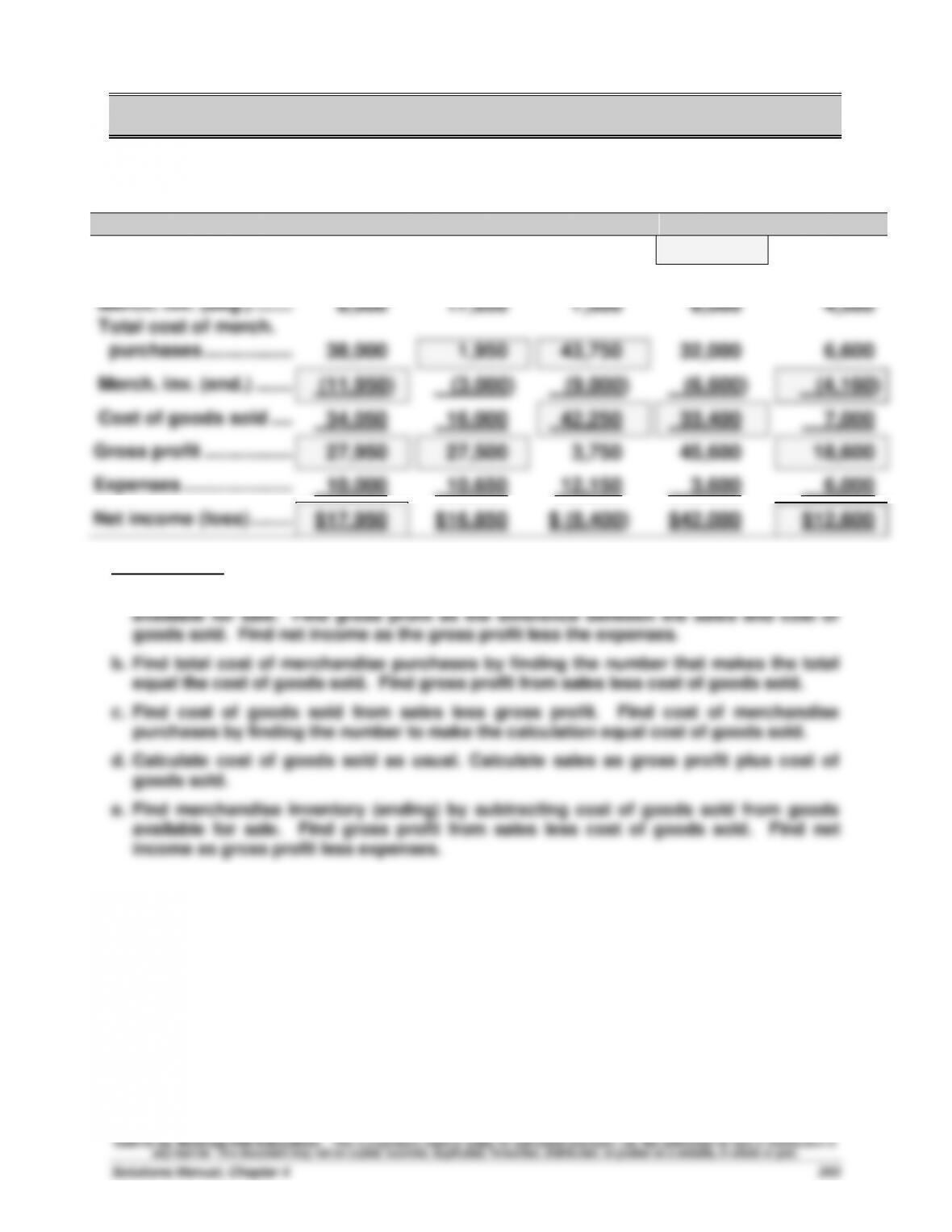

Sales ……………………….

$62,000

$43,500

$46,000

$79,000

$25,600

Cost of goods sold

Merch. inv. (beg.) …….

8,000

17,050

7,500

8,000

4,560

Total cost of merch.

purchases ……………..

38,000

1,950

43,750

32,000

6,600

Merch. inv. (end.) …….

(11,950)

(3,000)

(9,000)

(6,600)

(4,160)

Cost of goods sold ….

34,050

16,000

42,250

33,400

7,000

Gross profit ……………..

27,950

27,500

3,750

45,600

18,600

Expenses …………………

10,000

10,650

12,150

3,600

6,000

Net income (loss) ……..

$17,950

$16,850

$ (8,400)

$42,000

$12,600

Explanations:

a. Find merchandise inventory (ending) by subtracting cost of goods sold from goods

Exercise 4-2 (10 minutes)

Operating cycle of a merchandiser with credit sales follows (chronological):

Exercise 4-3 (20 minutes)

In today’s competitive world, organizations must concentrate on meeting their

customers’ needs and avoiding dissatisfaction. If these needs are not met

and dissatisfaction grows, the customers will deal with other companies or

entities. One measure of dissatisfaction of customers is the amount of sold

users.

Exercise 4-4 (30 minutes)

Apr. 2 Merchandise Inventory ………………………………. 4,600

Accounts Payable—Lyon …………………….. 4,600

Purchased merchandise on credit.

3 Merchandise Inventory ………………………………. 300

Exercise 4-5 (30 minutes)

May 5 Accounts Receivable ………………………………… 21,000

Sales …………………………..……………………… 21,000

Sold merchandise on credit (1,500 x $14).

5 Cost of Goods Sold …………………………………… 15,000

Exercise 4-6 (15 minutes)

May 5 Merchandise Inventory …………………………..…. 21,000

Accounts Payable ………………………………. 21,000

Purchased merchandise on credit (1,500 x $14).

a.

Exercise 4-7 (30 minutes)

1. BUYER- Santa Fe Company

a) Credit Purchase

Merchandise Inventory …………………………..…. 24,000

2. SELLER – Mesa Company

a) Credit Sale

Accounts Receivable ………………………………… 24,000

Sales…………………………..……………………… 24,000

3. Amount borrowed to pay with discount ………………….. $ 23,280

Annual rate of interest …………………………………………… x 8%

Exercise 4-8 (25 minutes)

1. Entries for Sydney Company (BUYER):

May 11 Merchandise Inventory ……………………………. 40,000

Accounts Payable ……………………………… 40,000

Purchased merchandise on credit.

2. Entries for Troy Corporation (SELLER):

May 11 Accounts Receivable ……………………………….. 40,000

Sales…………………………..…………………….. 40,000

Sold merchandise on account.

Exercise 4-9 (30 minutes)

Merchandise Inventory

Balance, Dec. 31, 2014…………..

25,000

Purchase discounts received ……..……………………

1,700

Invoice cost of purchases ……..

192,500

Purchase returns and allow. ……….………………….

4,000

Returns by customers …………..

2,100

Cost of sales transactions ………….……………….

196,000

Transportation-in ………………….

2,900

Shrinkage …………………………..……..……………………

800

Balance, Dec. 31, 2015

20,000

Cost of Goods Sold

Cost of sales transactions …….

Inventory shrinkage

recorded in December 31,

2015, adjusting entry …………..

196,000

800

Returns by customers and

restored to inventory ………………..…………

2,100

Balance, Dec. 31, 2015

194,700

Exercise 4-10 (20 minutes)

Perpetual

1)

Nov. 1 Merchandise Inventory ………………………………. 1,500

2)

Nov. 5 Accounts Payable …………………………..…………. 1,500

3)

Nov. 7 Cash …………………………..……………………………… 196

4)

Nov. 10 Merchandise Inventory ………………………………. 90

5)

Nov. 13 Accounts Receivable …………………………………. 1,600

Sales…………………………..………………………. 1,600

6)

Nov. 16 Sales Returns and Allowances …………………… 300

Accounts Receivable …………………………... 300

To record return of merchandise sold on credit.

Exercise 4-11 (25 minutes)

Adjusting entries

Dec. 31 Sales Salaries Expense …………………………….. 1,700

Salaries Payable ………………………………… 1,700

To record accrued salaries.

To close temporary accounts with

credit balances.

Dec. 31 Income Summary …………………………………… 444,750

Sales Returns and Allowances …………. 17,500

Sales Discounts ………………………………. 5,000