Chapter Outline

B. Work sheet Applications and Analysis – does not substitute for

financial statements. It is a tool used at the end of the period to help

organize data and prepare financial statements.

XI. Appendix 3C—Reversing Entries

A. Accounting without reversing entries

1. To construct proper entries when the cash receipt/payment

occurs in the new accounting period, the related accrual or

deferral adjustment must be recalled and considered.

2. With or without reversing entries use, it will yield the same

result.

B. Accounting with reversing entries (an optional step)

1. Linked to asset and liability account balances that arose from

the accrual of revenues and expenses.

2. Purpose is to simplify recordkeeping.

3. They are prepared after closing entries and dated the first day

of the new period.

4. Procedure is to transfer accrued asset and liability account

balances to related revenue and expense accounts creating an

abnormal balance in these accounts.

5. The full subsequent cash receipts (and payments) are recorded

as increases in revenue (and expense) accounts creating a net

balance equal to the amount earned or incurred in that period.

Notes

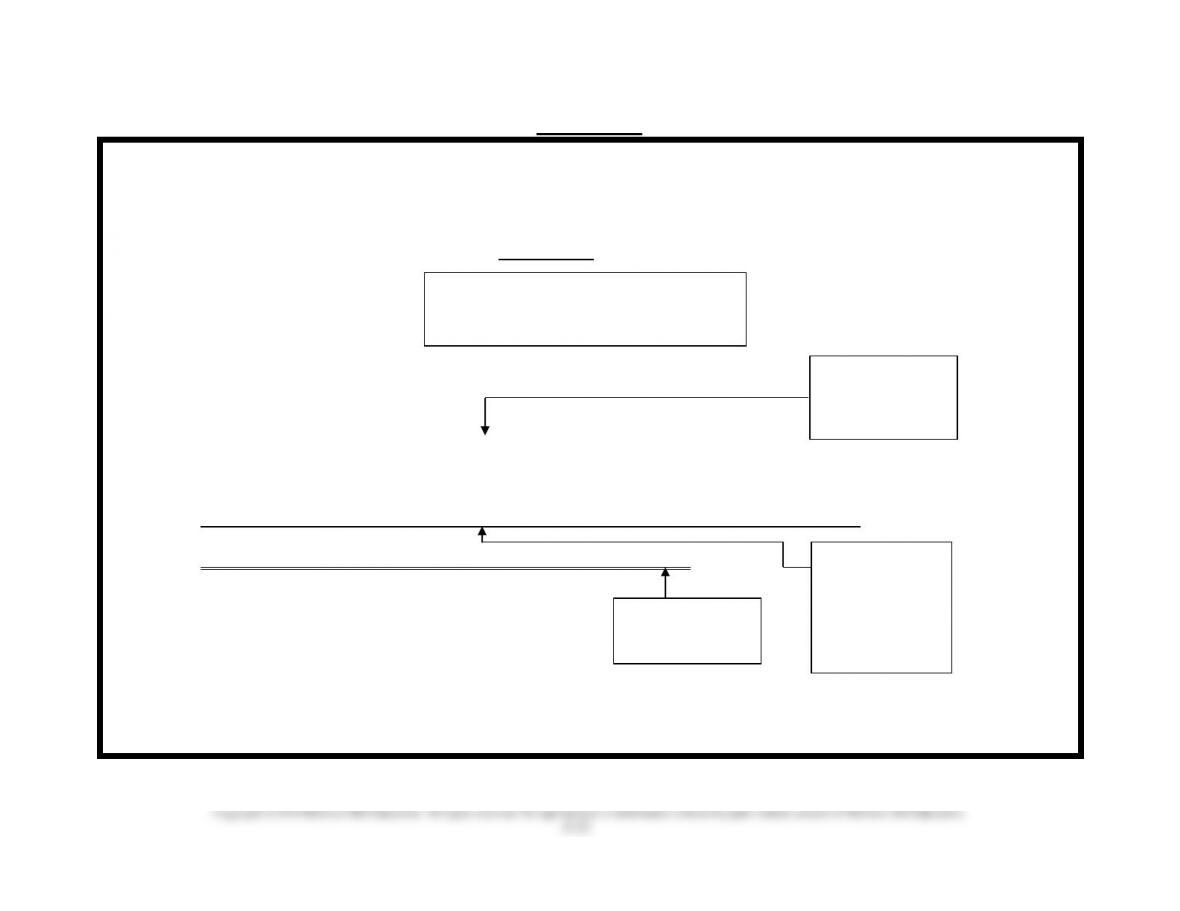

VISUAL #3-1

ACCRUAL BASIS ACCOUNTING

(Follows GAAP)

Requires that the

Income Statement

(for a period)

report

ALL REVENUES EARNED in period (Collected or Not)

Minus ALL EXPENSES INCURRED in period (Paid or Not)

Equals Net Income or Net Loss for the period

ACCOUNTS MUST BE ADJUSTED TO FOLLOW PRINCIPLES

GAAP

Revenue

Recognition

GAAP

Periodicity

GAAP

Expense

Recognition

(or Matching)

GAAP

Expense

Recognition

or Matching

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

3-13

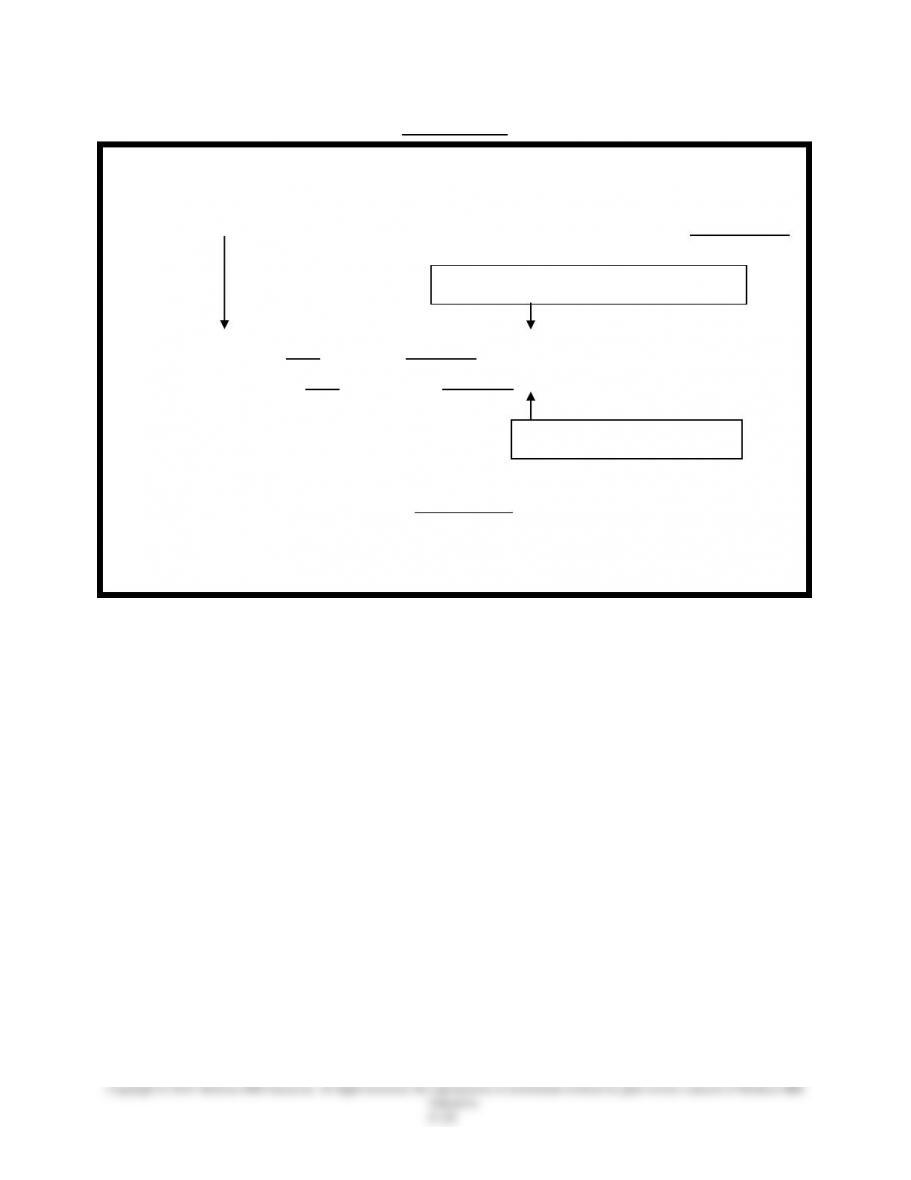

VISUAL #3-2

DEFERRALS

The converse of statements in Visual #3-1 also applies.

Revenue not earned or expense not incurred results in Deferrals*

UNEARNED = LIABILITY *

A REVENUE not earned cannot be shown, even if collected.

An EXPENSE not incurred cannot be shown, even if paid.

PREPAID = ASSET *

*We defer or postpone the reporting of the collected revenues

(as revenues) and prepaid expenses (as expenses) until the

revenue is earned and the expense is incurred.

Copyright © 2016 McGraw-Hill Education. All rights reserved. No reproduction or distribution without the prior written consent of McGraw-Hill

Education.

3-15

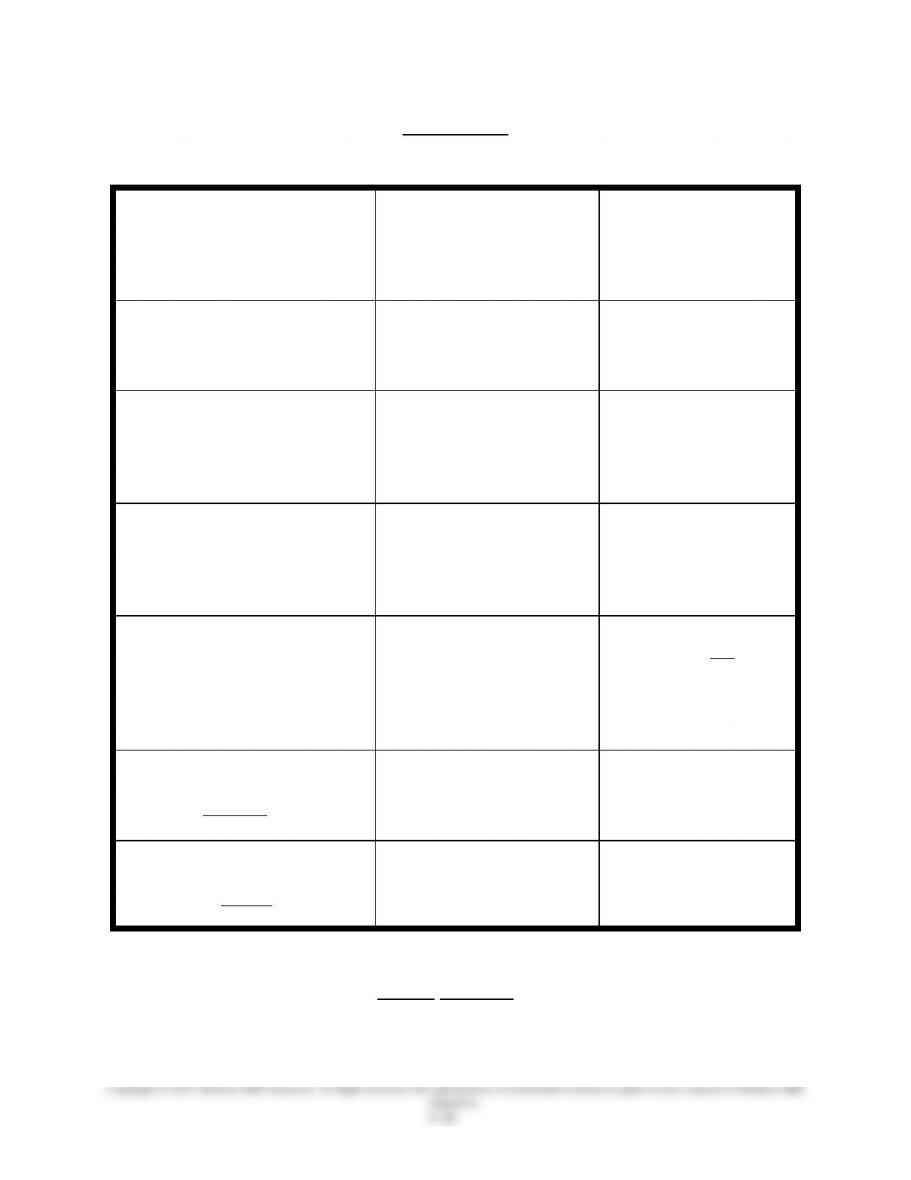

VISUAL #3-3

ADJUSTMENTS

TYPE

GENERALIZED*

ENTRY

AMOUNT

1A. Prepaid (deferred)

expenses—initially recorded as

assets

Dr. _________ Expense

Cr. the Asset* acct.

Amount used, or

consumed, or expired

1B. Prepaid (deferred)

expenses—that are depreciable

(plant assets)

Dr. Depreciation Expense

Cr. Accumulated

Depreciation

Portion of cost

allocated to this period

as depreciation

1C. Prepaid (deferred)

expenses—initially recorded as

expenses (alternate treatment—

appendix)

Dr. the Asset** acct.

Cr. ________ Expense

Amount left, or

not consumed, or

unexpired

2A. Unearned revenues—

(revenue received in advance)

initially record as liability

(unearned account)

Dr. Unearned ________

Cr. the Revenue** acct.

Amount earned to date

2B. Unearned revenues—

(revenue received in advance)

initially recorded as a revenue

(alternate treatment—

appendix)

Dr. the Revenue** acct.

Cr. Unearned________

Amount still not

earned

3. Accrued expenses—

(expenses incurred but not yet

recorded)

Dr. _________ Expense

Cr. _________ Payable

Amount accrued

4. Accrued revenues

(revenues earned but not

yet recorded)

Dr. ________ Receivable

Cr. the Revenue** acct.

Amount accrued

*Note: (1) Each adjustment affects a Balance Sheet Account and an Income

Statement Account and (2) CASH NEVER appears in an adjustment.

**Title or account name varies.