PROBLEM SET B

Problem 24-1B (50 minutes)

Part 1

Annual straight-line depreciation = = $70,000

Part 2

Net

Net Cash

Income

Flow

Expected annual sales of new product ………………..…

$1,150,000

$1,150,000

Expected annual costs of new product

Direct materials ………………………………………………..…

300,000

300,000

Direct labor …………………………..…………………………..

420,000

420,000

Overhead excluding depr. on new asset ………………

210,000

210,000

Depreciation on new asset………………………………..…

70,000

Selling and administrative expenses ……………………

100,000

100,000

Income before taxes ………………………………………………

50,000

Income taxes (30%)……………………………………………..…

15,000

15,000

Net income ………………………………………………………….…

$ 35,000

Net cash flow* …………………………………………………….…

$ 105,000

*Alternatively, annual net cash flow can be computed as:

Net income + Depreciation = $35,000 + $70,000 = $105,000

$300,000 – $20,000

4 years

Problem 24–1B (Continued)

Part 3

Payback Period = = 2.86 years

Part 4

Accounting rate of return = = 21.88%

*Average investment

Asset cost …………………………..……………………....

$300,000

Final year’s book value ………………………………...

20,000

Sum ……………………………………………………………..

$320,000

Average (Sum /2) ………………………………………....

$160,000

Part 5

Present Value of Net Cash Flows

Present

Present

Value of

Net Cash

Flows

Value of

1 at 7%

Net Cash

Flows

Year 1 ……………………………………………………..

$105,000

0.9346

$ 98,133

Year 2 ……………………………………………………..

105,000

0.8734

91,707

Year 3 ……………………………………………………..

105,000

0.8163

85,712

Year 4* ……………………………………………………

125,000

0.7629

95,363

Totals ……………………………………………………..

$440,000

$ 370,915

Amount invested …………………………………….

(300,000)

Net present value ……………………………………

$ 70,915

* Year 4’s cash flow includes the $20,000 salvage value.

$35,000

$160,000*

$300,000

$105,000

Problem 24-2B (55 minutes)

Part 1

PROJECT A

Net income ………………………………………………………………………………..…

$39,900

Depreciation expense* …………………………………………………………………

60,000

Net cash flow …………………………………………………………………………….…

$99,900

$240,000 – $0

Problem 24–2B (Continued)

Part 3

PROJECT A

Accounting rate of return = = 33.3%

*Average investment

Asset cost ………………………………………….

$240,000

Average (Cost/2) ………………………………...

$120,000

PROJECT B

Accounting rate of return = = 21.6%

*Average investment

Asset cost ………………………………………….

$240,000

Average (Cost/2) ………………………………...

$120,000

$39,900

$120,000*

$25,900

$120,000*

Problem 24–2B (Continued)

Part 4

PROJECT A

Present Value of Net Cash Flows

Present

Present

Value of

Value of

Net Cash

Flows

1 at 8%

Annuity

Net Cash

Flows

Years 1-4 …………………………..…………………..

$99,900

3.3121

$330,879

Amount invested ……………………………………

(240,000)

Net present value …………………………..………

$ 90,879

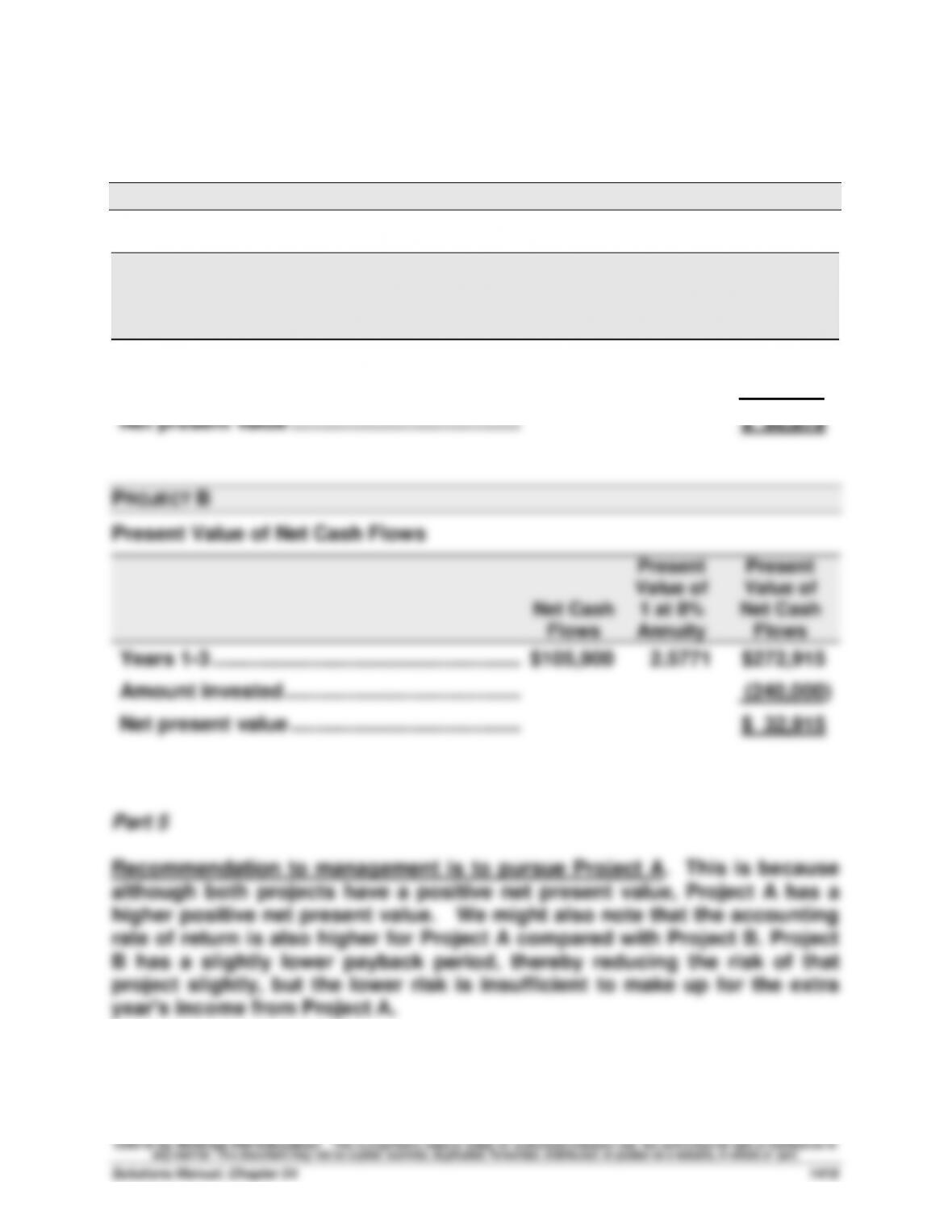

PROJECT B

Present Value of Net Cash Flows

Present

Present

Value of

Value of

Net Cash

Flows

1 at 8%

Annuity

Net Cash

Flows

Years 1-3 …………………………..…………………..

$105,900

2.5771

$272,915

Amount invested ……………………………………

(240,000)

Net present value …………………………..………

$ 32,915

Part 5

Recommendation to management is to pursue Project A. This is because

although both projects have a positive net present value, Project A has a

higher positive net present value. We might also note that the accounting

rate of return is also higher for Project A compared with Project B. Project

B has a slightly lower payback period, thereby reducing the risk of that

project slightly, but the lower risk is insufficient to make up for the extra

year’s income from Project A.

Problem 24-3B (60 minutes)

Part 1

RESULTS USING STRAIGHT-LINE DEPRECIATION

(a)

Income

Before

Deprec.

(b)

Straight–

Line

Deprec.

(c)

Taxable

Income

(a) – (b)

(d)

40%

Income

Taxes

(e)

Net Cash

Flows

(a) – (d)

Year 1 ……….………………

$12,000

$3,000

$ 9,000

$3,600

$8,400

Year 2 ……….………………

12,000

6,000

6,000

2,400

9,600

Year 3 ……….………………

12,000

6,000

6,000

2,400

9,600

Year 4 ……….………………

12,000

6,000

6,000

2,400

9,600

Year 5 ……….………………

12,000

6,000

6,000

2,400

9,600

Year 6 ……….………………

12,000

3,000

9,000

3,600

8,400

Part 2

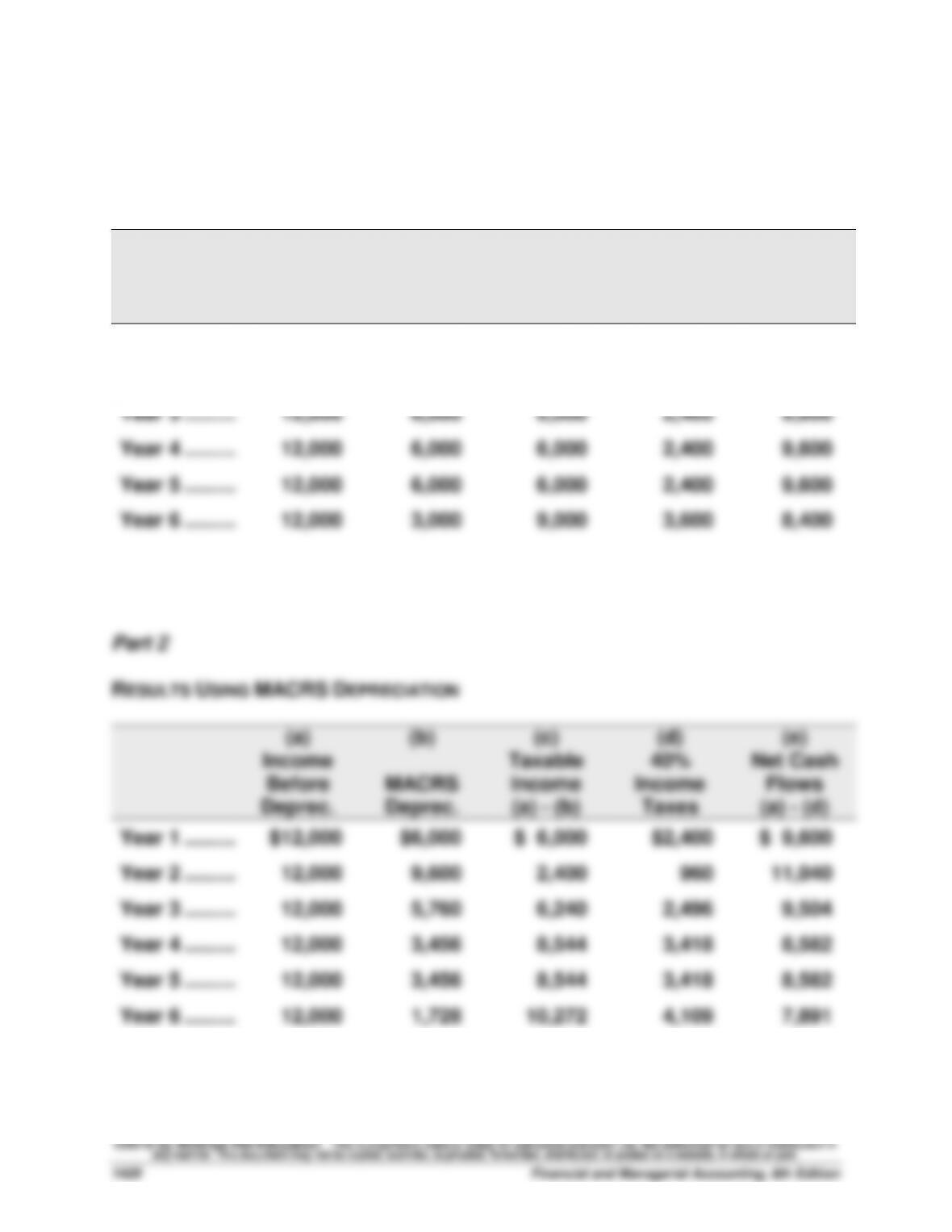

RESULTS USING MACRS DEPRECIATION

(a)

Income

Before

Deprec.

(b)

MACRS

Deprec.

(c)

Taxable

Income

(a) – (b)

(d)

40%

Income

Taxes

(e)

Net Cash

Flows

(a) – (d)

Year 1 ……….………………

$12,000

$6,000

$ 6,000

$2,400

$ 9,600

Year 2 ……….………………

12,000

9,600

2,400

960

11,040

Year 3 ……….………………

12,000

5,760

6,240

2,496

9,504

Year 4 ……….………………

12,000

3,456

8,544

3,418

8,582

Year 5 ……….………………

12,000

3,456

8,544

3,418

8,582

Year 6 ……….………………

12,000

1,728

10,272

4,109

7,891

Problem 24–3B (Continued)

Part 3

NET PRESENT VALUE OF ASSET USING STRAIGHT-LINE DEPRECIATION

Present

Present

Net Cash

Value of

Value of Net

Flows

1 at 10%

Cash Flows

Year 1 …………………………………………………..

$ 8,400

0.9091

$ 7,636

Year 2 …………………………………………………..

9,600

0.8264

7,933

Year 3 …………………………………………………..

9,600

0.7513

7,212

Year 4 …………………………………………………..

9,600

0.6830

6,557

Year 5 …………………………………………………..

9,600

0.6209

5,961

Year 6 …………………………………………………..

8,400

0.5645

4,742

Totals …………………………………………………..

$55,200

$40,041

Amount invested …………………………………..

(30,000)

Net present value …………………………..……..

$10,041

Part 4

NET PRESENT VALUE OF ASSET USING MACRS DEPRECIATION

Present

Present

Net Cash

Value of

Value of Net

Flows

1 at 10%

Cash Flows

Year 1 …………………………………………………..

$ 9,600

0.9091

$ 8,727

Year 2 …………………………………………………..

11,040

0.8264

9,123

Year 3 …………………………………………………..

9,504

0.7513

7,140

Year 4 …………………………………………………..

8,582

0.6830

5,862

Year 5 …………………………………………………..

8,582

0.6209

5,329

Year 6 …………………………………………………..

7,891

0.5645

4,454

Totals …………………………………………………..

$55,199

$40,635

Amount invested …………………………………..

(30,000)

Net present value …………………………..……..

$10,635

Part 5

Analysis: The net present value using MACRS depreciation is greater than the

net present value using straight-line depreciation because the cash flows are

larger in the earlier years of the asset’s life under MACRS depreciation. They

are larger because the depreciation deductions are larger, resulting in less

income taxes paid in the earlier years.

Problem 24-4B (45 minutes)

Part 1

Alternative 1: Keep the old freezer and have it repaired

Item

Period

Cash Flow

Present

Value Factor

at 10%

Present

Value of

Cash Flows

Revenues ………………………….

1 – 8

$63,000

5.3349

$ 336,099

Operating costs …………………

1 – 8

(55,000)

5.3349

(293,420)

Salvage value ……………………

8

3,000

0.4665

1,400

Total …………………………………

44,079

Cost of repair …………………….

(50,000)

Net present value ………………

$ (5,921)

*Note that the cost of the old machine is irrelevant because it is a sunk cost.

Part 2

Alternative 2: Sell the old freezer and buy a new one

Item

Period

Cash Flow

Present

Value Factor

at 10%

Present

Value of

Cash Flows

Revenues ………………………….

1 – 8

$68,000

5.3349

$ 362,773

Operating costs …………………

1 – 8

(30,000)

5.3349

(160,047)

Salvage value of new freezer

8

8,000

0.4665

3,732

Salvage value of old freezer.

now

5,000

5,000

Total …………………………………

211,458

Cost of new freezer ……………

(150,000)

Net present value ………………

$ 61,458

Part 3

Archer should sell the old freezer and buy a new one. The operating costs

of the old freezer are so much higher than that of the new freezer, even

after the old freezer has been repaired. Keeping the old freezer has a

negative net present value, and although the initial cash outlay is more to

buy the new freezer, it is the better investment.

Problem 24-5B (40 minutes)

Part 1: Payback period

Period

Cash flow

Cumulative cash flow

0 …………………………..………………………………………

$(800,000)

$(800,000)

1 …………………………..………………………………………

300,000

(500,000)

2 …………………………..………………………………………

350,000

(150,000)

3 …………………………..………………………………………

400,000

250,000

4 …………………………..………………………………………

450,000

700,000

$150,000 / $400,000 = 0.4

The payback period is about 2.4 years.

Part 2: Break-even time

Period

Cash Flow

Present Value

of 1 at 10%

Present Value

of Cash Flows

Cumulative

Present Value

of Cash Flows

0 ……………….

$(800,000)

1.0000

$(800,000)

$(800,000)

1 ……………….

300,000

0.9091

272,730

(527,270)

2 ……………….

350,000

0.8264

289,240

(238,030)

3 ……………….

400,000

0.7513

300,520

62,490

4 ……………….

450,000

0.6830

307,350

369,840

$238,030 / $300,520 = 0.8

The break-even time is about 2.8 years.

Part 3: Net present value

From the chart in part 2, we can see that the net present value of the

investment is $369,840.

Part 4

If the company requires a payback period of 2 years for any project, this

project fails that test. However, a case could be made for the project as the

net present value is positive. In this case, the cash flows continue to

increase over time, meaning the largest cash flows appear at the end of the

project. If Aster passes on this project, they will forego a profitable project.

Problem 24-6B (40 minutes)

Part 1: Payback period

Period

Cash flow

Cumulative cash flow

0 …………………………..………………………………………

$(800,000)

$(800,000)

1 …………………………..………………………………………

450,000

(350,000)

2 …………………………..………………………………………

400,000

50,000

3 …………………………..………………………………………

350,000

400,000

4 …………………………..………………………………………

300,000

700,000

$350,000 / $400,000 = 0.9 (rounded)

The payback period is about 1.9 years.

Part 2: Break-even time

Period

Cash Flow

Present Value

of 1 at 10%

Present Value

of Cash Flows

Cumulative

Present Value

of Cash Flows

0 ……………….

$(800,000)

1.0000

$(800,000)

$(800,000)

1 ……………….

450,000

0.9091

409,095

(390,905)

2 ……………….

400,000

0.8264

330,560

(60,345)

3 ……………….

350,000

0.7513

262,955

202,610

4 ……………….

300,000

0.6830

204,900

407,510

$60,345 / $262,955 = 0.2 (rounded)

The break-even time is about 2.2 years.

Part 3: Net present value

From the chart in part 2, we can see that the net present value of the

investment is $407,510.

Part 4

If the company requires a payback period of 2 years for any project, this

project passes that test. Its break-even time is slightly more than 2 years,

and the project has a positive net present value of $407,510. This project

should be undertaken.