Problem 24-1A (Continued)

Part 4

Accounting rate of return = = 21.56%

* Average investment

Asset cost ………………………………………………………………..……..

$480,000

Final year’s book value ……………………………………………..……..

20,000

Sum ………………………………………………………………………………..

$500,000

Average (Sum /2) ……………………………………………………….

$250,000

Part 5

Present Value of Net Cash Flows

Present

Present

Net Cash

Value of

Value of Net

Flows

1 at 7%

Cash Flows

Year 1 ………………………………………………….

$168,900

0.9346

$ 157,854

Year 2 ………………………………………………….

168,900

0.8734

147,517

Year 3 ………………………………………………….

168,900

0.8163

137,873

Year 4* ……………………………………………..….

188,900

0.7629

144,112

Totals ………………………………………………….

$695,600

587,356

Amount invested ………………………………….

(480,000)

Net present value ……………………………..….

$ 107,356

* Year 4’s cash flow includes the $20,000 salvage value.

$53,900

$250,000*

Problem 24-2A (55 minutes)

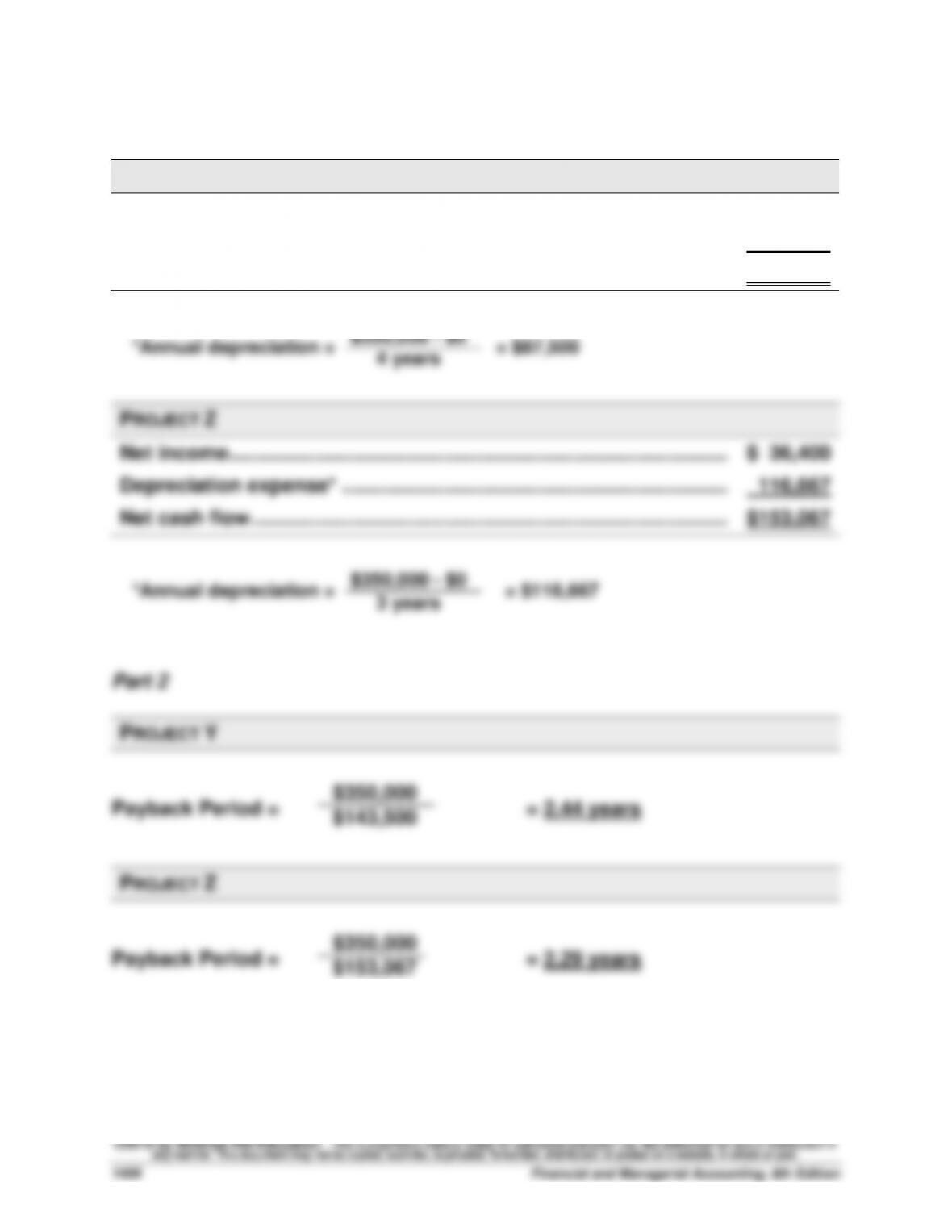

Part 1

PROJECT Y

Net income ……………………………………………………………………………...

$ 56,000

Depreciation expense* …………………………………………………………….

87,500

Net cash flow …………………………………………………………………………..

$143,500

Depreciation expense* …………………………………………………………….

Net cash flow …………………………………………………………………………..

PROJECT Y

PROJECT Z

$350,000 – $0

Problem 24–2A (Continued)

Part 3

PROJECT Y

Accounting rate of return = = 32%

*Average investment

Asset cost …………………………………………

$350,000

Average (Cost/2) ……………………..……

$175,000

PROJECT Z

Accounting rate of return = = 20.8%

*Average investment

Asset cost …………………………………………

$350,000

Average (Cost/2) ……………………..……

$175,000

$56,000

$175,000*

$36,400

$175,000*

Problem 24–2A (Continued)

Part 4

PROJECT Y

Present Value of Net Cash Flows

Present

Present

Value of

Value of

Net Cash

Flows

1 at 8%

Annuity

Net Cash

Flows

Years 1-4 ………………………………………………

$143,500

3.3121

$475,286

Amount invested …………………………………..

(350,000)

Net present value ………………………………….

$125,286

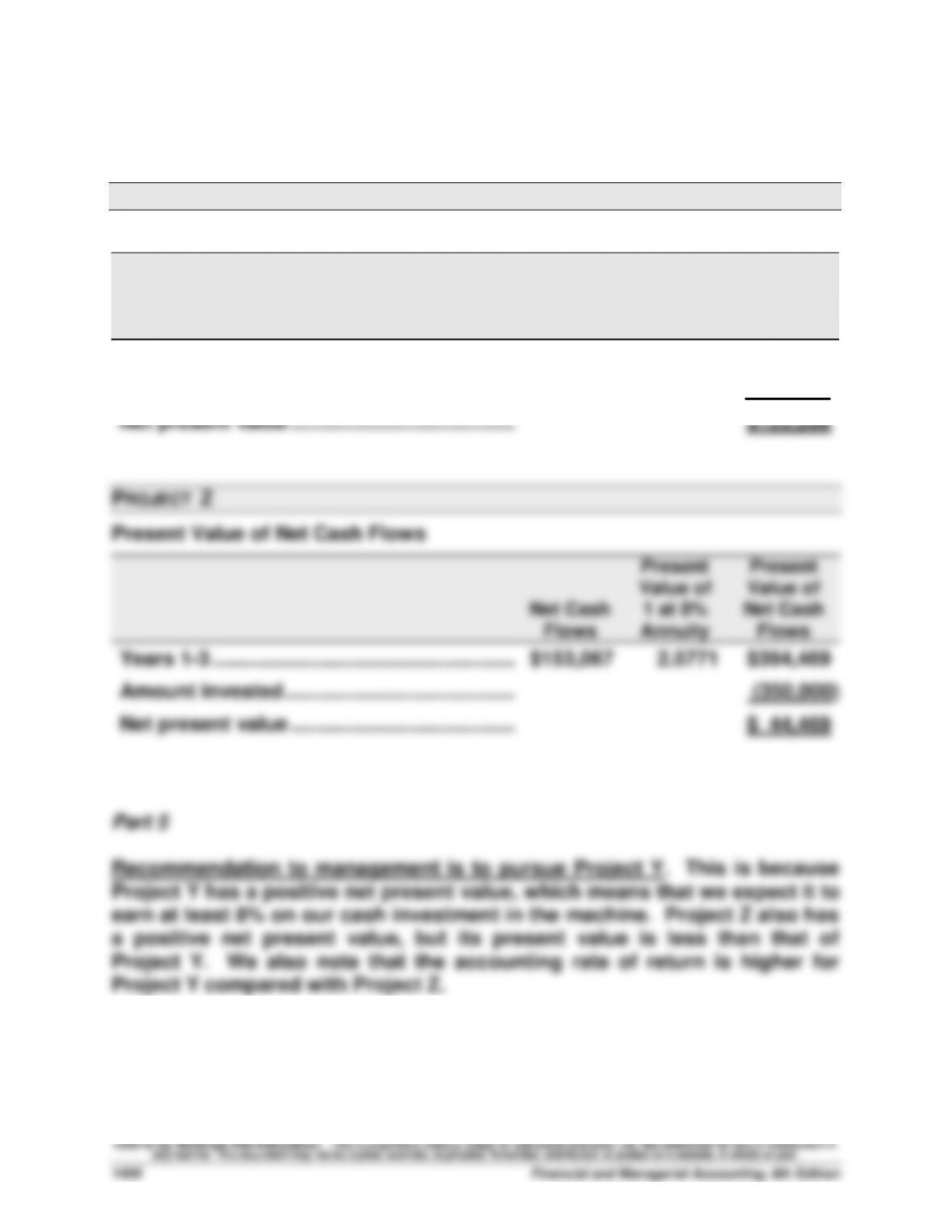

PROJECT Z

Present Value of Net Cash Flows

Present

Present

Value of

Value of

Net Cash

Flows

1 at 8%

Annuity

Net Cash

Flows

Years 1-3 …………………………..………………….

$153,067

2.5771

$394,469

Amount invested …………………………………..

(350,000)

Net present value ………………………………….

$ 44,469

Part 5

Recommendation to management is to pursue Project Y. This is because

Project Y has a positive net present value, which means that we expect it to

earn at least 8% on our cash investment in the machine. Project Z also has

a positive net present value, but its present value is less than that of

Project Y. We also note that the accounting rate of return is higher for

Project Y compared with Project Z.

Problem 24-3A (60 minutes)

Part 1

RESULTS USING STRAIGHT-LINE DEPRECIATION

(a)

Income

Before

Deprec.

(b)

Straight–

Line

Deprec.

(c)

Taxable

Income

(a) – (b)

(d)

40%

Income

Taxes

(e)

Net Cash

Flows

(a) – (d)

Year 1 ……….………………

$66,000

$ 9,000

$57,000

$22,800

$43,200

Year 2 ……….………………

66,000

18,000

48,000

19,200

46,800

Year 3 ……….………………

66,000

18,000

48,000

19,200

46,800

Year 4 ……….………………

66,000

18,000

48,000

19,200

46,800

Year 5 ……….………………

66,000

18,000

48,000

19,200

46,800

Year 6 ……….………………

66,000

9,000

57,000

22,800

43,200

Part 2

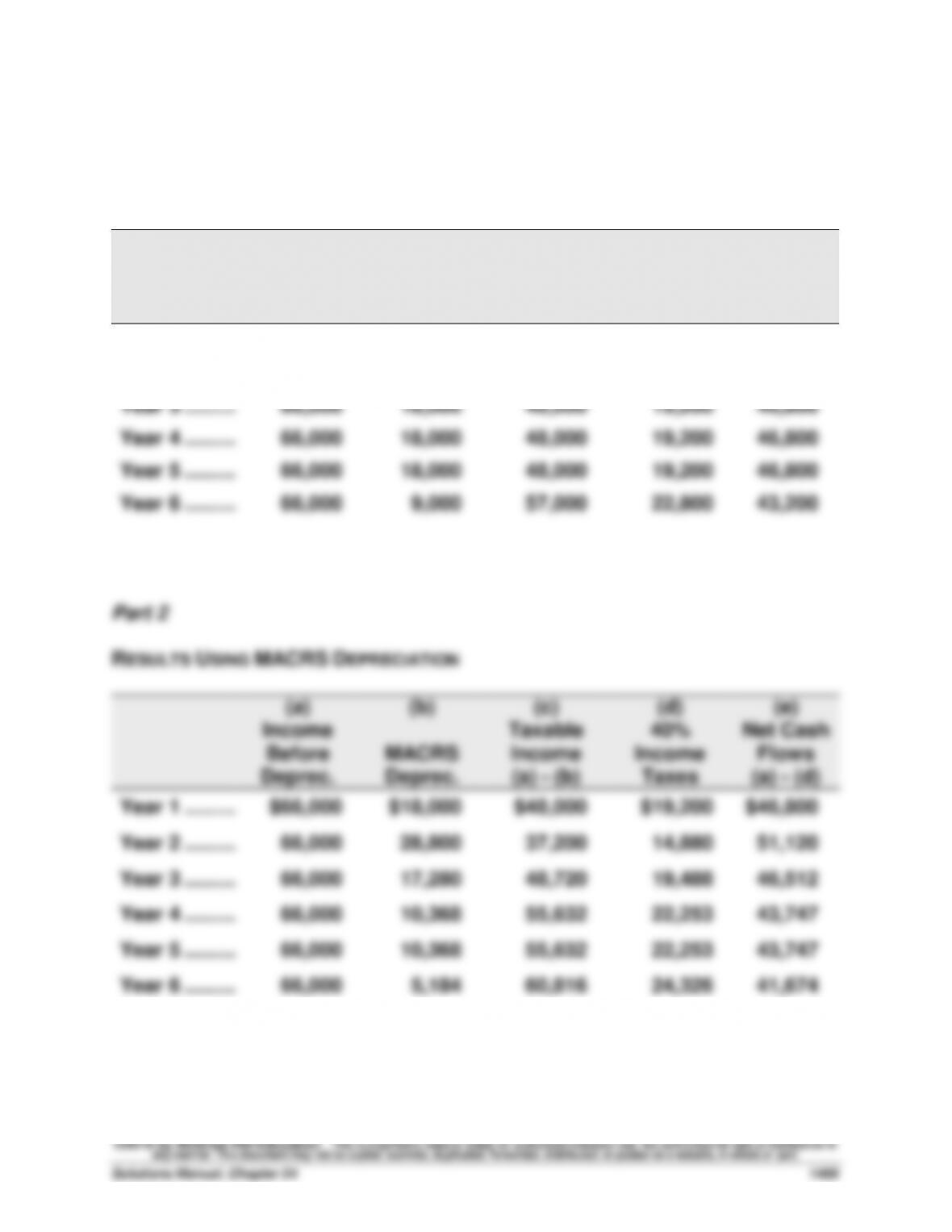

RESULTS USING MACRS DEPRECIATION

(a)

Income

Before

Deprec.

(b)

MACRS

Deprec.

(c)

Taxable

Income

(a) – (b)

(d)

40%

Income

Taxes

(e)

Net Cash

Flows

(a) – (d)

Year 1 ……….………………

$66,000

$18,000

$48,000

$19,200

$46,800

Year 2 ……….………………

66,000

28,800

37,200

14,880

51,120

Year 3 ……….………………

66,000

17,280

48,720

19,488

46,512

Year 4 ……….………………

66,000

10,368

55,632

22,253

43,747

Year 5 ……….………………

66,000

10,368

55,632

22,253

43,747

Year 6 ……….………………

66,000

5,184

60,816

24,326

41,674

Problem 24–3A (Continued)

Part 3

NET PRESENT VALUE OF ASSET USING STRAIGHT-LINE DEPRECIATION

Present

Present

Value of

Net Cash

Flows

Value of

1 at 10%

Net Cash

Flows

Year 1 ………………………………………………….

$ 43,200

0.9091

$ 39,273

Year 2 ………………………………………………….

46,800

0.8264

38,676

Year 3 ………………………………………………….

46,800

0.7513

35,161

Year 4 ………………………………………………….

46,800

0.6830

31,964

Year 5 ………………………………………………….

46,800

0.6209

29,058

Year 6 ………………………………………………….

43,200

0.5645

24,386

Totals ………………………………………………….

$273,600

198,518

Amount invested ………………………………….

(90,000)

Net present value …………………………………

$108,518

Part 4

NET PRESENT VALUE OF ASSET USING MACRS DEPRECIATION

Present

Present

Value of

Net Cash

Flows

Value of

1 at 10%

Net Cash

Flows

Year 1 ………………………………………………….

$ 46,800

0.9091

$ 42,546

Year 2 ………………………………………………….

51,120

0.8264

42,246

Year 3 ………………………………………………….

46,512

0.7513

34,944

Year 4 ………………………………………………….

43,747

0.6830

29,879

Year 5 ………………………………………………….

43,747

0.6209

27,163

Year 6 ………………………………………………….

41,674

0.5645

23,525

Totals ………………………………………………….

$273,600

200,303

Amount invested ………………………………….

(90,000)

Net present value …………………………………

$110,303

Part 5

Analysis: The net present value using MACRS depreciation is greater than the

net present value using straight-line depreciation because the cash flows are

larger in the earlier years of the asset’s life under MACRS depreciation. They

are larger because the depreciation deductions are larger, resulting in less

income taxes paid in the earlier years.

Problem 24-4A (45 minutes)

Part 1

Alternative 1: Keep the old machine and have it overhauled

Item

Period

Cash

Flow

Present

Value Factor

at 10%

Present

Value of

Cash Flows

Revenues …………………………..

1 – 5

$95,000

3.7908

$360,126

Operating costs ………………….

1 – 5

(42,000)

3.7908

(159,214)

Salvage value ……………………..

5

15,000

0.6209

9,314

Total …………………………………..

210,226

Cost of overhaul …………………

(150,000)

Net present value ……………….

$ 60,226

*Note that the cost of the old machine is irrelevant because it is a sunk cost.

Part 2

Alternative 2: Sell the old machine and buy a new one

Item

Period

Cash

Flow

Present

Value Factor

at 10%

Present

Value of

Cash Flows

Revenues …………………………..

1 – 5

$100,000

3.7908

$379,080

Operating costs ………………….

1 – 5

(32,000)

3.7908

(121,306)

Salvage value of new

machine …………………………..…

5

20,000

0.6209

12,418

Salvage value of old

machine …………………………..…

now

29,000

29,000

Total …………………………………..

299,192

Cost of new machine ………….

(300,000)

Net present value ……………….

$ (808)

Part 3

Interstate should keep the old machine and overhaul it. The cost savings

and additional revenue generated on the new machine are not enough to

overcome the high initial cost of the new machine.

Problem 24-5A (40 minutes)

Part 1: Payback period

Period

Cash flow

Cumulative cash flow

0 …………………………..………………………………………

$(250,000)

$(250,000)

1 …………………………..………………………………………

47,000

(203,000)

2 …………………………..………………………………………

52,000

(151,000)

3 …………………………..………………………………………

75,000

(76,000)

4 …………………………..………………………………………

94,000

18,000

5 …………………………..………………………………………

125,000

143,000

$76,000 / $94,000 = 0.8 (rounded)

The payback period is about 3.8 years.

Part 2: Break-even time

Period

Cash Flow

Present Value

of 1 at 10%

Present Value

of Cash Flows

Cumulative

Present Value

of Cash Flows

0 ……………….

$(250,000)

1.0000

$(250,000)

$(250,000)

1 ……………….

47,000

0.9091

42,728

(207,272)

2 ……………….

52,000

0.8264

42,973

(164,299)

3 ……………….

75,000

0.7513

56,348

(107,951)

4 ……………….

94,000

0.6830

64,202

(43,749)

5 ……………….

125,000

0.6209

77,613

33,864

$43,749 / $77,613 = 0.6 (rounded)

The break-even time is about 4.6 years.

Part 3: Net present value

From the chart in part 2, we can see that the net present value of the

investment is $33,864.

Part 4

If the company requires a payback period of 3 years for any project, this

project fails that test. However, a case could be made for the project as the

net present value is positive. In this case, the cash flows continue to

increase over time, meaning the largest cash flows appear at the end of the

project. If Sentinel passes on this project, they will forego a profitable

project.

Problem 24-6A (40 minutes)

Part 1: Payback period

Period

Cash flow

Cumulative cash flow

0 …………………………..………………………………………

$(250,000)

$(250,000)

1 …………………………..………………………………………

125,000

(125,000)

2 …………………………..………………………………………

94,000

(31,000)

3 …………………………..………………………………………

75,000

44,000

4 …………………………..………………………………………

52,000

96,000

5 …………………………..………………………………………

47,000

143,000

$31,000 / $75,000 = 0.4 (rounded)

The payback period is about 2.4 years.

Part 2: Break-even time

Period

Cash Flow

Present Value

of 1 at 10%

Present Value

of Cash Flows

Cumulative

Present Value

of Cash Flows

0 ……………….

$(250,000)

1.0000

$(250,000)

$(250,000)

1 ……………….

125,000

0.9091

113,638

(136,362)

2 ……………….

94,000

0.8264

77,682

(58,680)

3 ……………….

75,000

0.7513

56,348

(2,332)

4 ……………….

52,000

0.6830

35,516

33,184

5 ……………….

47,000

0.6209

29,182

62,366

$2,332 / $35,516 = 0.1 (rounded)

The break-even time is about 3.1 years.

Part 3: Net present value

From the chart in part 2, we can see that the net present value of the

investment is $62,366.

Part 4

If the company requires a payback period of 3 years for any project, this

project passes that test. Its break-even time is slightly more than 3 years,

and the project has a positive net present value of $62,366. This project

should be undertaken.

Problem 24-6A (Concluded)

Part 5

While the total cash flows are identical to those in Problem 24-5A, the cash