Problem 23-4A (30 minutes)

Alternative 1: Sell to a second-hand shop

Incremental revenue (5,000 x $6.00) ………………………………………….

$ 30,000

Incremental cost ………………………………………………………………………

0

Incremental income ………………………………………………………………….

$ 30,000

Alternative 2: Disassemble and sell to a recycler

Incremental revenue (5,000 x $12.00) ………………………………………..

$ 60,000

Incremental cost ………………………………………………………………………

32,000

Incremental income ………………………………………………………………….

$ 28,000

Alternative 3: Rework and sell at regular prices

Incremental revenue (3,000 x $45.00) ………………………………………..

$135,000

Incremental cost ………………………………………………………………………

102,000

Incremental income ………………………………………………………………….

$ 33,000

Decision: Harold should choose alternative 3, as this provides the highest

incremental income.

Problem 23-5A (55 minutes)

Part 1

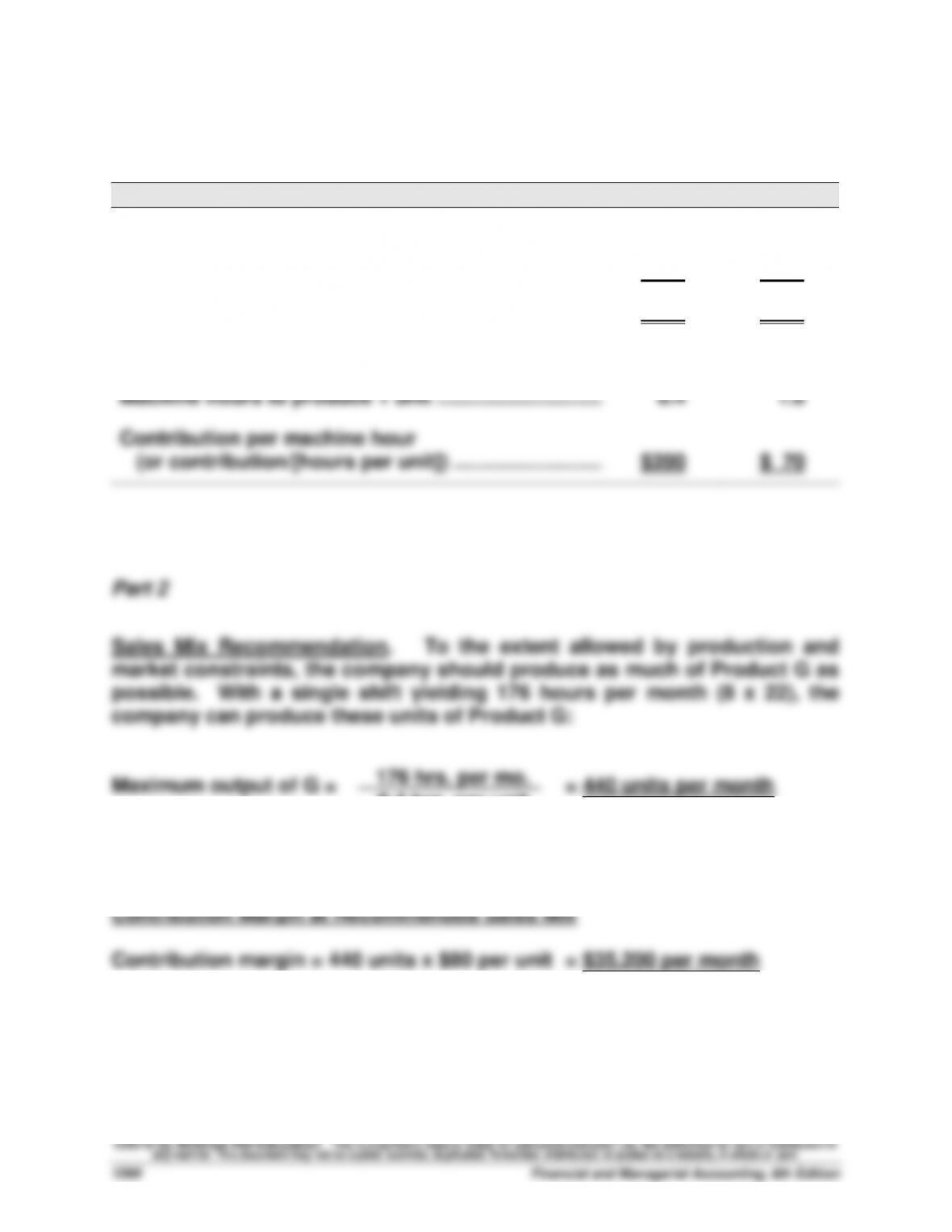

Product G

Product B

Selling price per unit …………………………………………..…

$120

$160

Variable costs per unit ………………………………………..…

40

90

Contribution margin per unit ……………………………….…

$ 80

$ 70

Machine hours to produce 1 unit …………………………..

0.4

1.0

Contribution per machine hour

(or contribution/[hours per unit]) …………………………

$200

$ 70

Part 2

Sales Mix Recommendation. To the extent allowed by production and

market constraints, the company should produce as much of Product G as

possible. With a single shift yielding 176 hours per month (8 x 22), the

company can produce these units of Product G:

Maximum output of G = = 440 units per month

176 hrs. per mo.

0.4 hrs. per unit

Problem 23-5A (Continued)

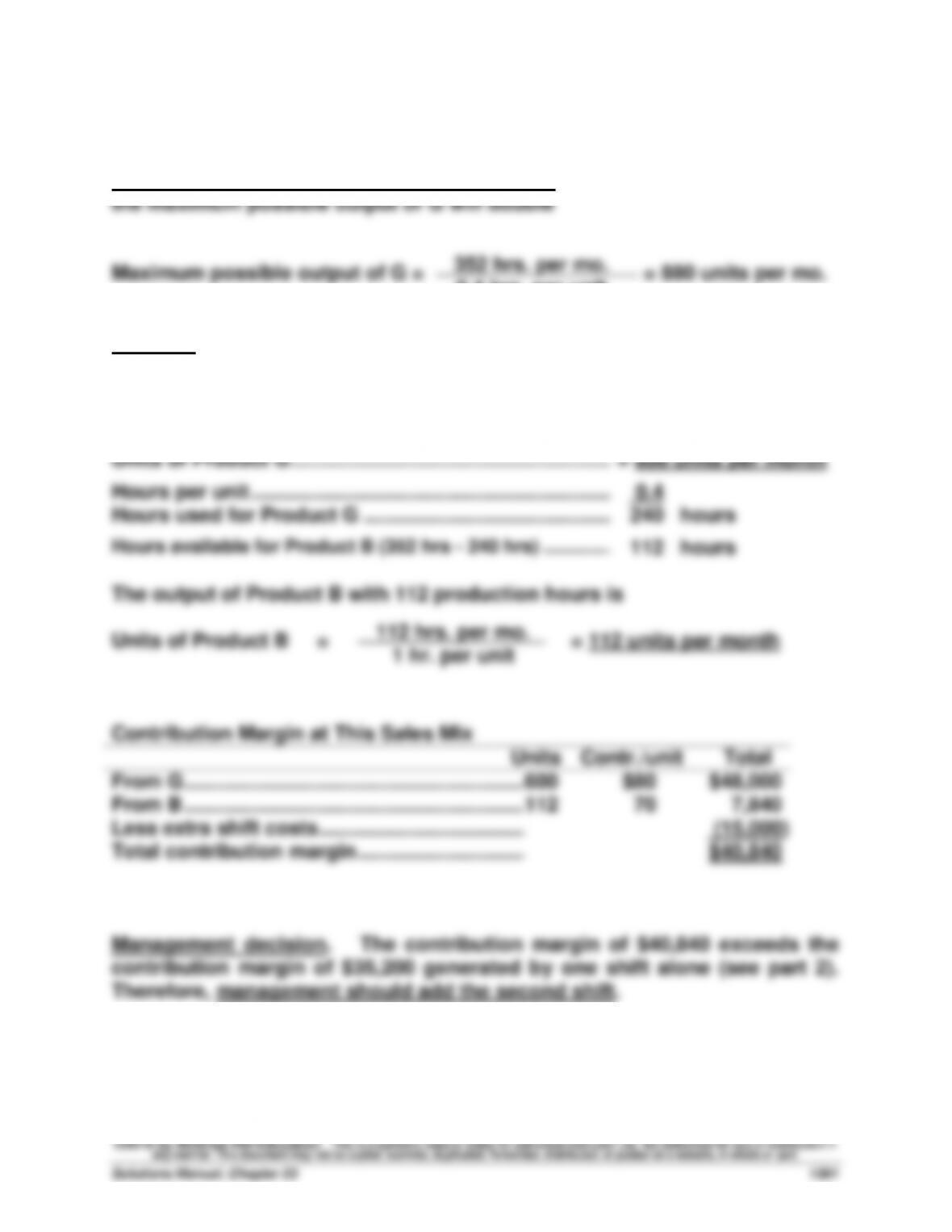

Part 3

Sales Mix Recommendation with Second Shift. If the second shift is added,

However, this level of output exceeds the company’s market constraint of

600 units of G per month. This means the company should produce 600

units of Product G, and commit the remainder of the productive capacity to

Product B. This is computed as follows

Units of Product G …………………………..…………………….……

= 600 units per month

Hours per unit …………………………..…………………………..

0.4

Hours used for Product G ……………………………………..……

240

hours

Hours available for Product B (352 hrs – 240 hrs) ………….……

112

hours

The output of Product B with 112 production hours is

Units of Product B = = 112 units per month

Contribution Margin at This Sales Mix

Units

Contr./unit

Total

From G …………………………………………………….…

600

$80

$48,000

From B …………………………………………………….…

112

70

7,840

Less extra shift costs ……………………………….…..

(15,000)

Total contribution margin …………………………..

$40,840

Management decision. The contribution margin of $40,840 exceeds the

contribution margin of $35,200 generated by one shift alone (see part 2).

Therefore, management should add the second shift.

0.4 hrs. per unit

112 hrs. per mo.

1 hr. per unit

Problem 23-5A (Continued)

Part 4

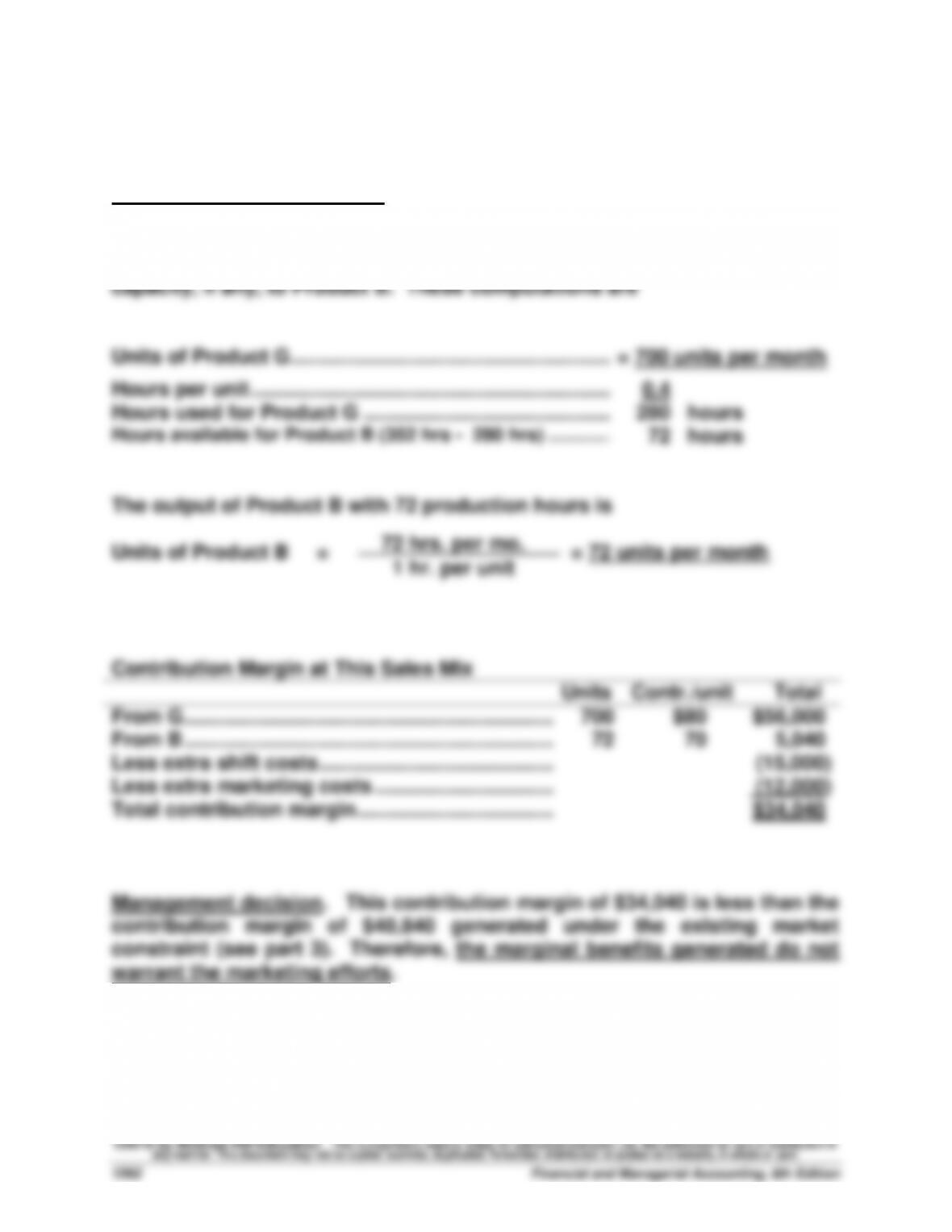

Sales Mix Recommendation. By incurring additional marketing cost, the

company can relax the market constraint for sales of Product G up to the

point where 700 units can be sold. This means the company can produce

700 units of Product G, and commit the remainder of its productive

Problem 23-6A (60 minutes)

Part 1

ELEGANT DECOR COMPANY

Analysis of Expenses under Elimination of Department 200

Total

Eliminated

Continuing

Expenses

Expenses

Expenses

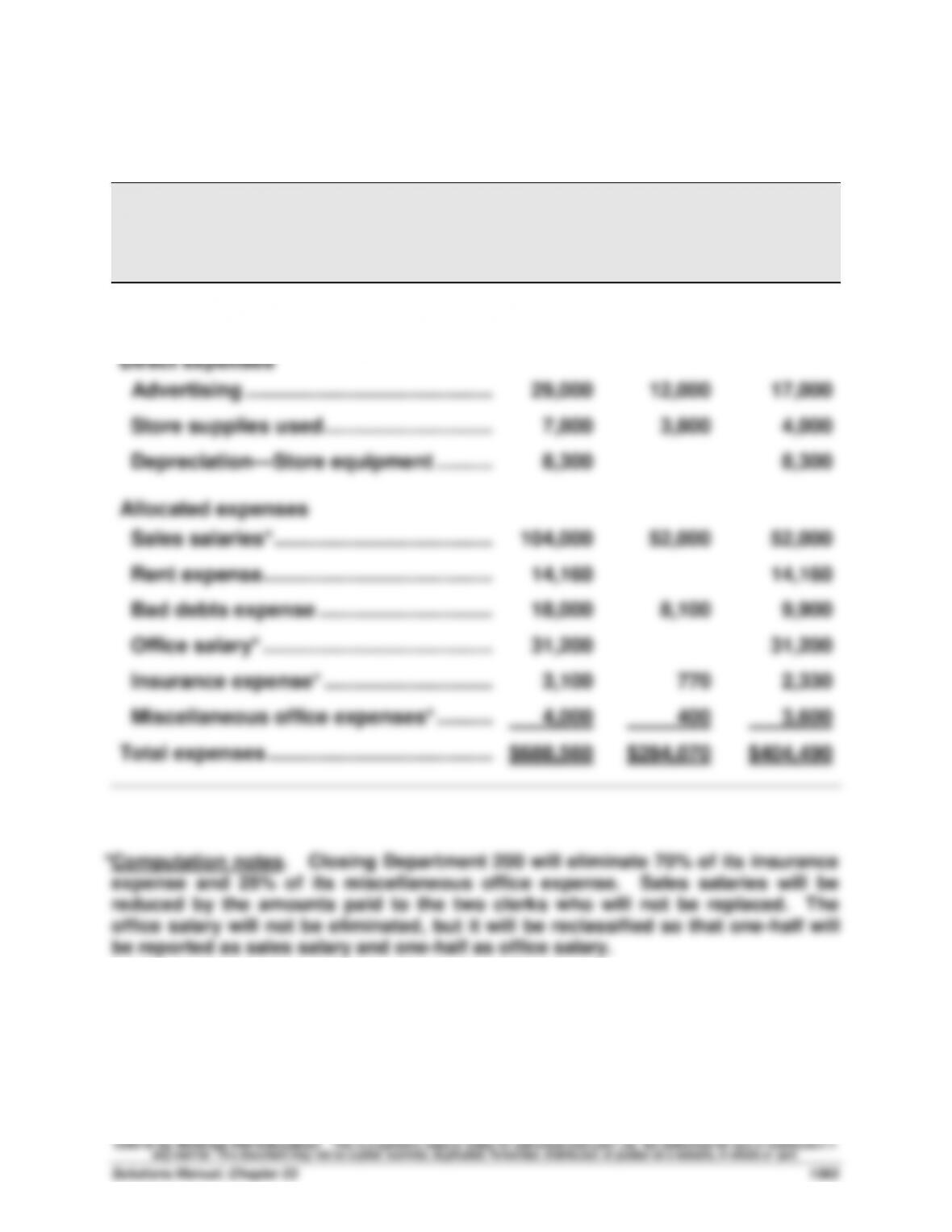

Cost of goods sold ……………………………………….

$469,000

$207,000

$262,000

Direct expenses

Advertising ……………………………………..………….

29,000

12,000

17,000

Store supplies used …………………………..

7,800

3,800

4,000

Depreciation—Store equipment ……….………….

8,300

8,300

Allocated expenses

Sales salaries* …………………………..…….………….

104,000

52,000

52,000

Rent expense …………………………………..………….

14,160

14,160

Bad debts expense …………………………..

18,000

8,100

9,900

Office salary* …………………………………..………….

31,200

31,200

Insurance expense* …………………………..

3,100

770

2,330

Miscellaneous office expenses* ……….………….

4,000

400

3,600

Total expenses ………………………………….………….

$688,560

$284,070

$404,490

*Computation notes. Closing Department 200 will eliminate 70% of its insurance

expense and 25% of its miscellaneous office expense. Sales salaries will be

reduced by the amounts paid to the two clerks who will not be replaced. The

office salary will not be eliminated, but it will be reclassified so that one-half will

be reported as sales salary and one-half as office salary.

Problem 23-6A (Continued)

Part 2

ELEGANT DECOR COMPANY

Forecasted Annual Income Statement

Under Plan to Eliminate Department 200

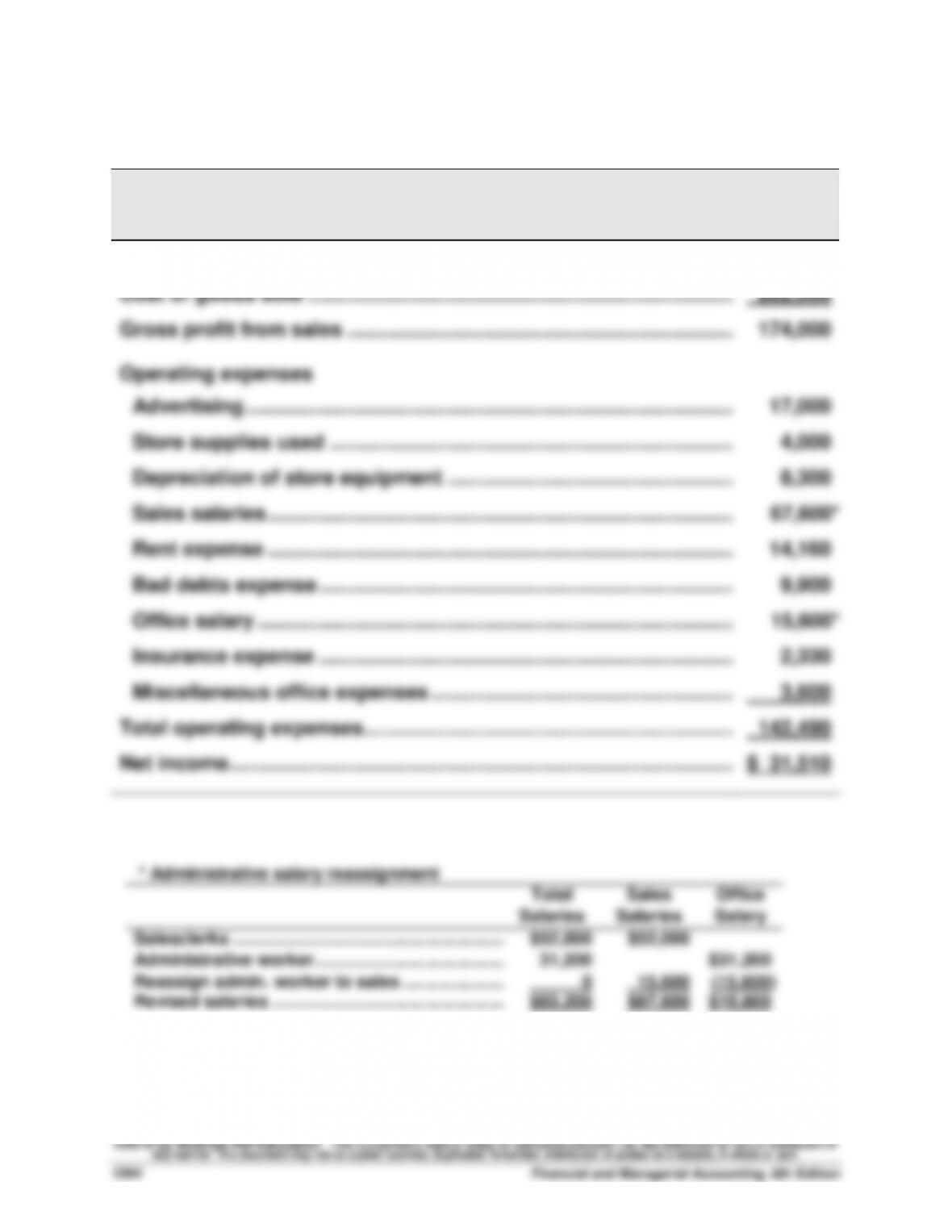

Sales ………………………………………………………………………………………..….

$436,000

Cost of goods sold …………………………………………………………………..….

262,000

Gross profit from sales …………………………………………………………….….

174,000

Operating expenses

Advertising …………………………………………………………………………….….

17,000

Store supplies used ……………………………………………………………….….

4,000

Depreciation of store equipment …………………………………………….….

8,300

Sales salaries …………………………………………………………………………….

67,600*

Rent expense ……………………………………………………….………………..….

14,160

Bad debts expense ……………………………………………………….………..….

9,900

Office salary …………………………………………………………………………..….

15,600*

Insurance expense …………………………………………………………………….

2,330

Miscellaneous office expenses ……………………………………………….….

3,600

Total operating expenses…………………………..……………………………..….

142,490

Net income ……………………………………………………………………………….….

$ 31,510

* Administrative salary reassignment

Total

Sales

Office

Salaries

Salaries

Salary

Salesclerks ………………………………………………..……..

$52,000

$52,000

Administrative worker ……………………………………………….

31,200

$31,200

Reassign admin. worker to sales …………………………..

0

15,600

(15,600)

Revised salaries ……………………………………………………….

$83,200

$67,600

$15,600

Problem 23-6A (Continued)

Part 3

ELEGANT DECOR COMPANY

Reconciliation of Combined Income With Forecasted Income

Combined net income …………………………………………………………….…

$ 37,440

Less Dept. 200’s lost sales ……………………………………………………….

(290,000)

Plus Dept. 200’s eliminated expenses…………………………………………

284,070

Forecasted net income ………………………………………………………………

$ 31,510

ANALYSIS

Department 200’s avoidable expenses of $284,070 are $5,930 less than its

revenues of $290,000. This means the company’s annual net income would

be $5,930 less from eliminating Department 200. This analysis suggests

the department should probably not be eliminated.

©2016 by McGraw–Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in

any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

Financial and Managerial Accounting, 6th Edition

1366

PROBLEM SET B

Problem 23–1B (45 minutes)

WINDMIRE COMPANY

COMPARATIVE INCOME STATEMENTS

(1)

(2)

(3)

Normal

New

Volume

Business

Combined

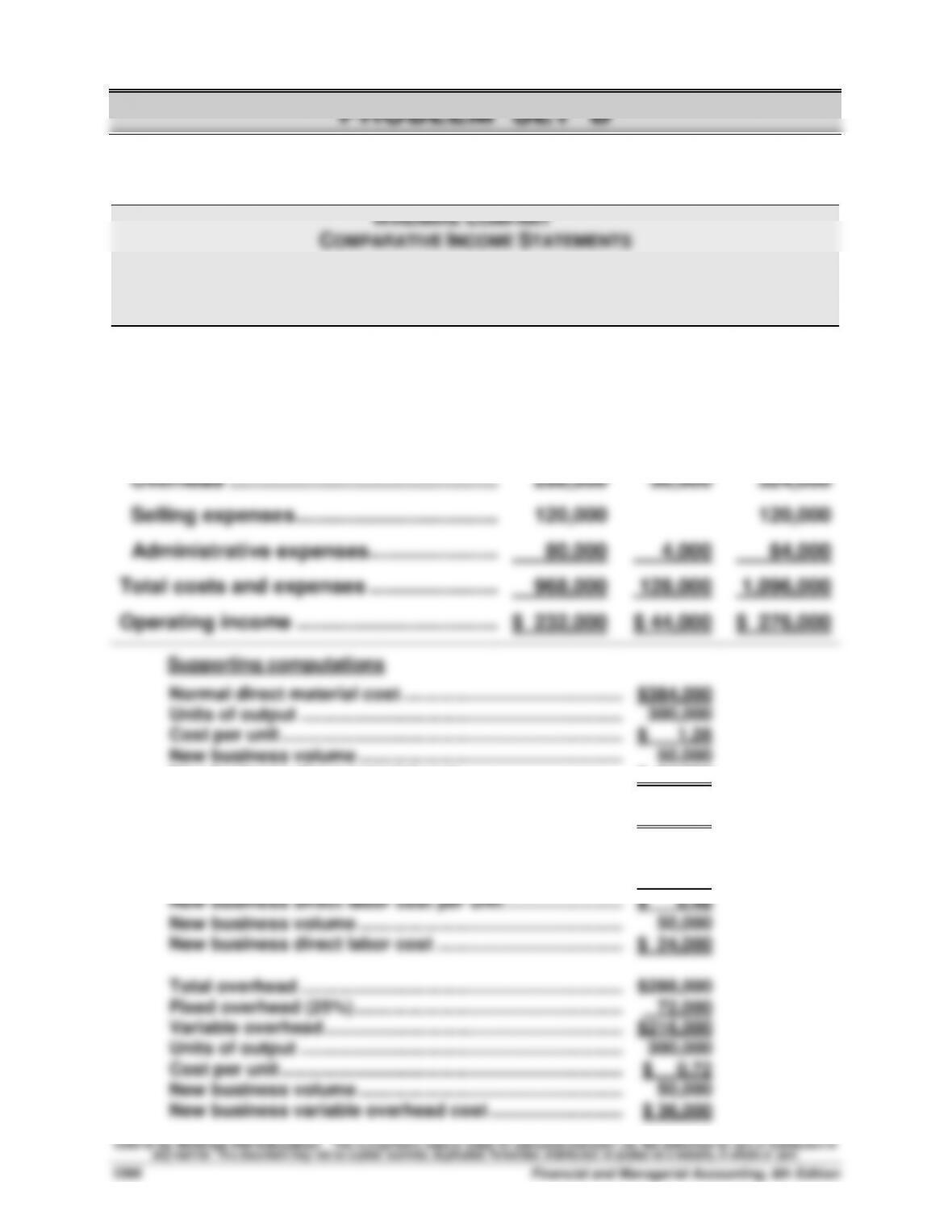

Sales …………………………………………………...

$1,200,000

$172,000

$1,372,000

Costs and expenses

Direct materials ………………………………....

384,000

64,000

448,000

Direct labor ………………………………………..

96,000

24,000

120,000

Overhead …………………………………………..

288,000

36,000

324,000

Selling expenses ………………………………..

120,000

120,000

Administrative expenses…………………....

80,000

4,000

84,000

Total costs and expenses …………………....

968,000

128,000

1,096,000

Operating income …………………………..…...

$ 232,000

$ 44,000

$ 276,000

Supporting computations

Normal direct material cost ……………………………………….………

$384,000

Units of output ………………………………………………………….………

300,000

Cost per unit ……………………………………………………………..………

$ 1.28

New business volume ……………………………………………….………

50,000

New business direct material cost …………………………....………

$ 64,000

Normal direct labor cost ……………………………………………………

$ 96,000

Units of output ………………………………………………………….………

300,000

Cost per unit ……………………………………………………………..………

$ 0.32

Overtime per unit (50%) …………………………………………….………

0.16

New business direct labor cost per unit …………………….…….

$ 0.48

New business volume ……………………………………………….………

50,000

New business direct labor cost …………………………………………

$ 24,000

Total overhead ………………………………………………………….………

$288,000

Fixed overhead (25%) ………………………………………………..……..

72,000

Variable overhead ……………………………………………………....

$216,000

Units of output ………………………………………………………….………

300,000

Cost per unit ……………………………………………………………..………

$ 0.72

New business volume ……………………………………………….………

50,000

New business variable overhead cost ……………………….….

$ 36,000

Problem 23-2B (50 minutes)

Part 1

MERVIN COMPANY

COMPARATIVE INCOME STATEMENTS

(a)

(b)

(c)

Normal

New

Volume

Business

Combined

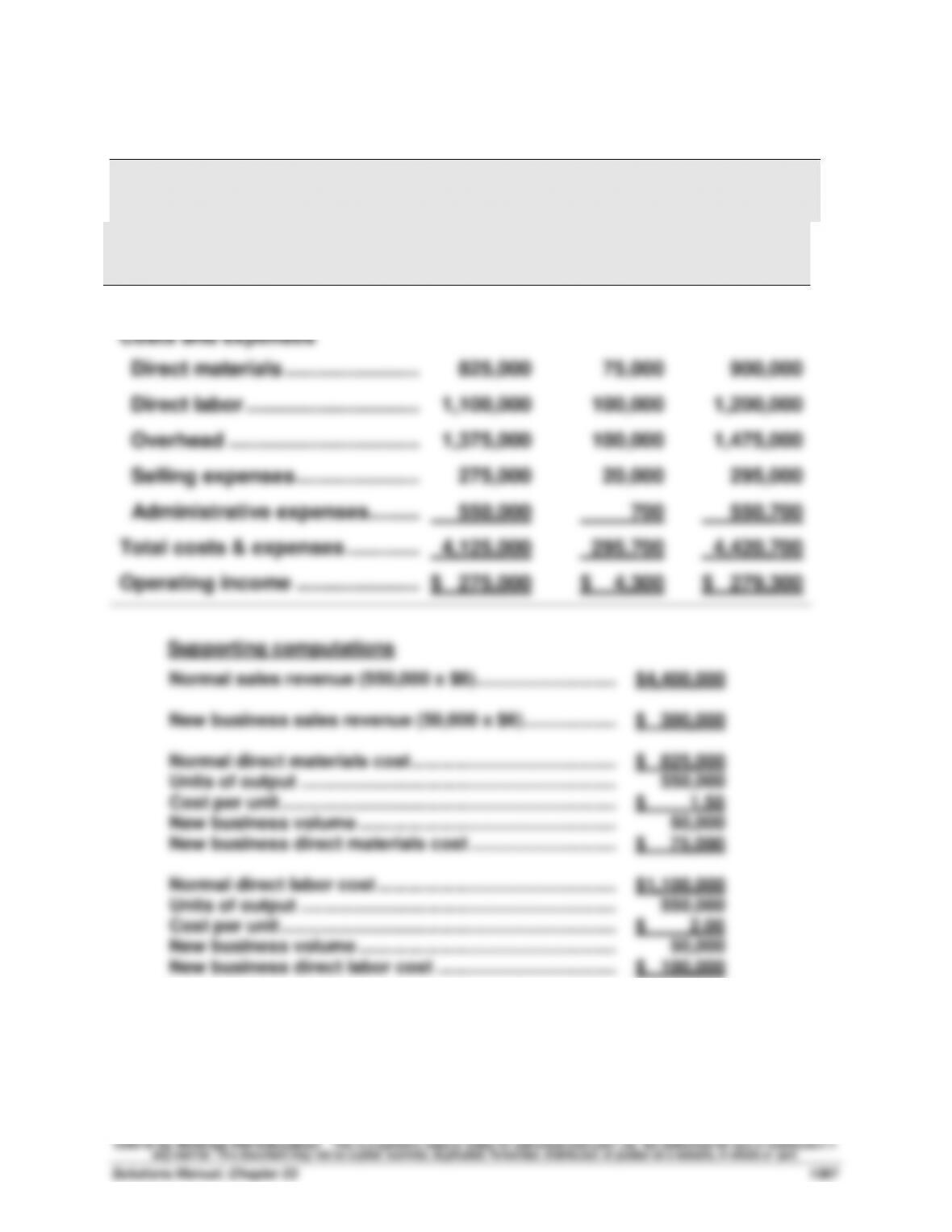

Sales ……………………………………..……

$4,400,000

$300,000

$4,700,000

Costs and expenses

Direct materials …………………………

825,000

75,000

900,000

Direct labor …………………………..

1,100,000

100,000

1,200,000

Overhead …………………………….……

1,375,000

100,000

1,475,000

Selling expenses ………………….……

275,000

20,000

295,000

Administrative expenses……………

550,000

700

550,700

Total costs & expenses ………….……

4,125,000

295,700

4,420,700

Operating income ………………….……

$ 275,000

$ 4,300

$ 279,300

Supporting computations

Normal sales revenue (550,000 x $8)………………………..

$4,400,000

New business sales revenue (50,000 x $6) ……………….

$ 300,000

Normal direct materials cost ……………………………………

$ 825,000

Units of output ………………………………………………………..

550,000

Cost per unit ……………………………………………………………

$ 1.50

New business volume ……………………………………………..

50,000

New business direct materials cost …………………………

$ 75,000

Normal direct labor cost ………………………………………….

$1,100,000

Units of output ………………………………………………………..

550,000

Cost per unit ……………………………………………………………

$ 2.00

New business volume ……………………………………………..

50,000

New business direct labor cost ……………………………….

$ 100,000

Problem 23-2B (concluded)

Total overhead ………………………………………………………..

$1,375,000

Fixed overhead (20%) ………………………………………………

275,000

Variable overhead ……………………………………………………

$1,100,000

Units of output ………………………………………………………..

550,000

Cost per unit ……………………………………………………………

$ 2.00

New business volume ……………………………………………..

50,000

New business variable overhead cost ……………………..

$ 100,000

Total selling expenses …………………………………………….

$ 275,000

Fixed selling expenses (60%) …………………………………..

165,000

Variable selling expenses ………………………………………..

110,000

Units of output ………………………………………………………..

550,000

Cost per unit ……………………………………………………………

$ 0.20

Plus additional selling expenses per unit ………………..

0.20

Total selling cost per unit for this order …………………..

$ 0.40

New business volume ……………………………………………..

50,000

New business selling expenses……………………………….

$ 20,000

Part 2

Based on the financial analysis above, Mervin should accept the order.

The order provides additional income of $4,300. Other factors that Mervin

should consider are:

Will the customer expect additional circuit boards at this special price?

Will regular customers demand a reduction in their price?

Can Mervin maintain quality and production at full capacity?

Part 3

If the new customer demands 100,000 units instead of 50,000, this will

mean that Mervin will lose sales of 50,000 units at the regular price. They

will have to consider the contribution margin lost on these units, as well as

whether their regular customers will go elsewhere to obtain their circuit

boards. This could lead to a permanent loss of volume at the regular price

of $8 per unit.