Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Exercise 23-6 (15 minutes)

Scrap

Rework

Sale of scrapped/reworked units .......................

$55,000

$187,000

Less out-of-pocket costs to rework ...................

Less opportunity cost of not making new

units (22,000 @ $2.50) .........................................

----

----

(99,000)

(55,000)

Total ................................................................

$55,000

$ 33,000

(1) The incremental income from selling as scrap is $55,000 (22,000 x $2.50).

(2) The incremental income from reworking is $33,000.

(3) The product should not be reworked as the $33,000 income from

Exercise 23-7 (15 minutes)

INCREMENTAL REVENUE AND COST OF ADDITIONAL PROCESSING

Revenue if processed further (7,000 x $25) ...............................................

$175,000

Revenue if sold as is (7,000 x $8) ...............................................................

56,000

Incremental revenue ....................................................................................

119,000

Less incremental cost of processing .........................................................

125,000

Incremental net income ...............................................................................

$ (6,000)

RECOMMENDATION: Varto should not process these units further, as they will

be $6,000 worse off if they do so. (Note that the $22 per unit manufacturing

cost is not relevant because it is a sunk cost.)

Exercise 23-8 (25 minutes)

Sell as is

Process

further

Incremental revenue ............................................

$700,000

$1,372,000*

Incremental costs ................................................

----

(420,000)

Income ................................................................

$700,000

$ 952,000

*Revenue from processed products

Units

Price

Total

Product B ..............................................................................

5,600

$105

$ 588,000

Product C ..............................................................................

11,200

70

784,000

Total revenue from processed products ............................

$1,372,000

ALTERNATE SOLUTION FORMAT

Net income (loss) from processed products

Revenue if processed further ..................................................

$1,372,000

Less: Additional costs of processing ..................................

$(420,000)

Opportunity cost (lost sales of Product A) ................

(700,000)

(1,120,000)

Net benefit to processing.........................................................

$ 252,000

RECOMMENDATION: This analysis shows that the company will be better off

by $252,000 if it chooses to process Product A into the two products of B

and C. (Note that the $28 per unit cost of manufacturing Product A is sunk

and irrelevant to this decision.)

Exercise 23-9 (30 minutes)

Preliminary computations

Contribution margin per hour

Product TLX

Product MTV

Selling price per unit .................................................

$15.00

$ 9.50

Variable costs per unit ..............................................

4.80

5.50

Contribution per unit .................................................

$10.20

$ 4.00

Machine-hours to produce 1 unit .............................

0.50

0.20

Contribution margin per machine-hour

(or contribution/hours per unit) ..............................

$20.40

$20.00

Exercise 23-9 (continued)

1. FOR PRODUCT TLX

Maximum sales ................................................................

4,700

units

Hours needed per unit ............................................................

0.50

Total hours used (4,700 x 0.50) ..............................................

2,350

hours

Exercise 23-10 (30 minutes)

1. DEPARTMENTS WITH EXPECTED NET LOSSES ELIMINATED

Total

M

N

O

P

T

Sales ................................

$119,000

$63,000

$ 0

$56,000

$ 0

$ 0

Expenses

Avoidable ................................

32,200

9,800

0

22,400

0

0

Unavoidable ................................

107,800

51,800

12,600

4,200

29,400

9,800

Total expenses ................................

140,000

61,600

12,600

26,600

29,400

9,800

Net income (loss) ................................

$ (21,000)

$ 1,400

$(12,600)

$29,400

$(29,400)

$(9,800)

Explanation: This income statement reflects elimination of Departments N,

P, and T. The sales and avoidable expenses are the combined amounts for

Departments M and O. The net loss has actually increased because the

excess of sales dollars over avoidable expenses has declined and less

remains to cover unavoidable expenses.

2. DEPARTMENTS WITH LESS SALES THAN AVOIDABLE EXPENSES ELIMINATED

Total

M

N

O

P

T

Sales ................................

$161,000

$63,000

$ 0

$56,000

$42,000

$ 0

Expenses

Avoidable ................................

46,200

9,800

0

22,400

14,000

0

Unavoidable ................................

107,800

51,800

12,600

4,200

29,400

9,800

Total expenses ................................

154,000

61,600

12,600

26,600

43,400

9,800

Net income (loss) ................................

$ 7,000

$ 1,400

$(12,600)

$29,400

$ (1,400)

$(9,800)

Explanation: This income statement reflects the Departments M, O, and P.

Departments N and T are eliminated because their sales dollars do not

cover their avoidable costs.

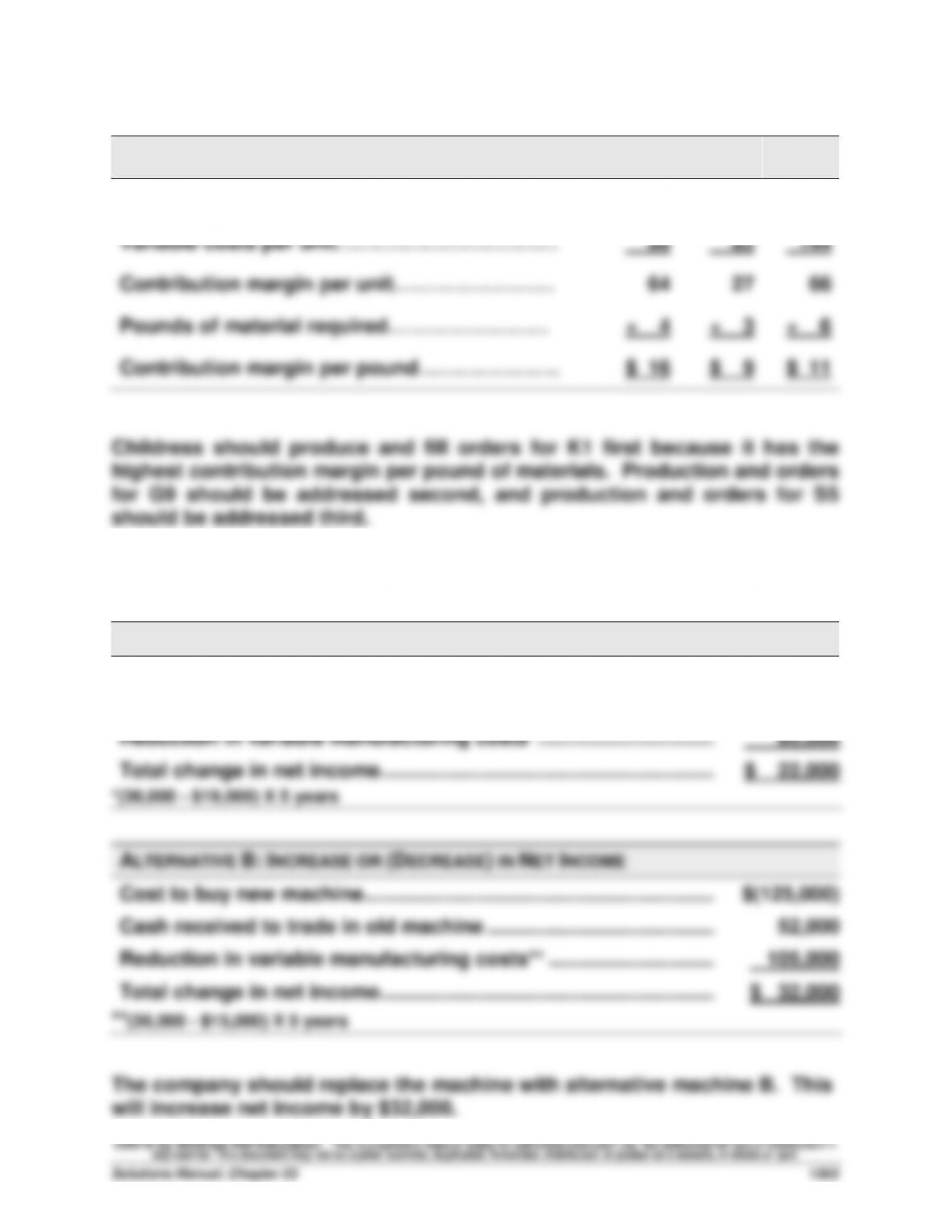

Exercise 23-11 (30 minutes)

K1

S5

G9

Selling price per unit………………………………

$160

$112

$210

Variable costs per unit……………………………

96

85

144

Contribution margin per unit……………………

64

27

66

Pounds of material required……………………

÷ 4

÷ 3

÷ 6

Contribution margin per pound…………………

$ 16

$ 9

$ 11

Childress should produce and fill orders for K1 first because it has the

highest contribution margin per pound of materials. Production and orders

for G9 should be addressed second, and production and orders for S5

should be addressed third.

Exercise 23-12 (20 minutes)

ALTERNATIVE A: INCREASE OR (DECREASE) IN NET INCOME

Cost to buy new machine................................................................

$(115,000)

Cash received to trade in old machine ......................................................

52,000

Reduction in variable manufacturing costs* ................................

85,000

Total change in net income................................................................

$ 22,000

*(36,000 - $19,000) X 5 years

ALTERNATIVE B: INCREASE OR (DECREASE) IN NET INCOME

Cost to buy new machine................................................................

$(125,000)

Cash received to trade in old machine ......................................................

52,000

Reduction in variable manufacturing costs** ................................

105,000

Total change in net income................................................................

$ 32,000

**(36,000 - $15,000) X 5 years

The company should replace the machine with alternative machine B. This

will increase net income by $32,000.

Exercise 23-13 (15 minutes)

If canoes are discontinued

Revenue lost ...................................................................

$2,000,000

Variable costs saved

Direct materials ............................................................

$450,000

Direct labor ...................................................................

500,000

Variable overhead ........................................................

300,000

Variable selling & administrative ...............................

200,000

Total variable costs saved ............................................

1,450,000

Contribution margin lost ...............................................

550,000

Direct fixed costs saved ................................................

375,000

Income lost .....................................................................

$ 175,000

Based on the above analysis, the canoes should not be discontinued.

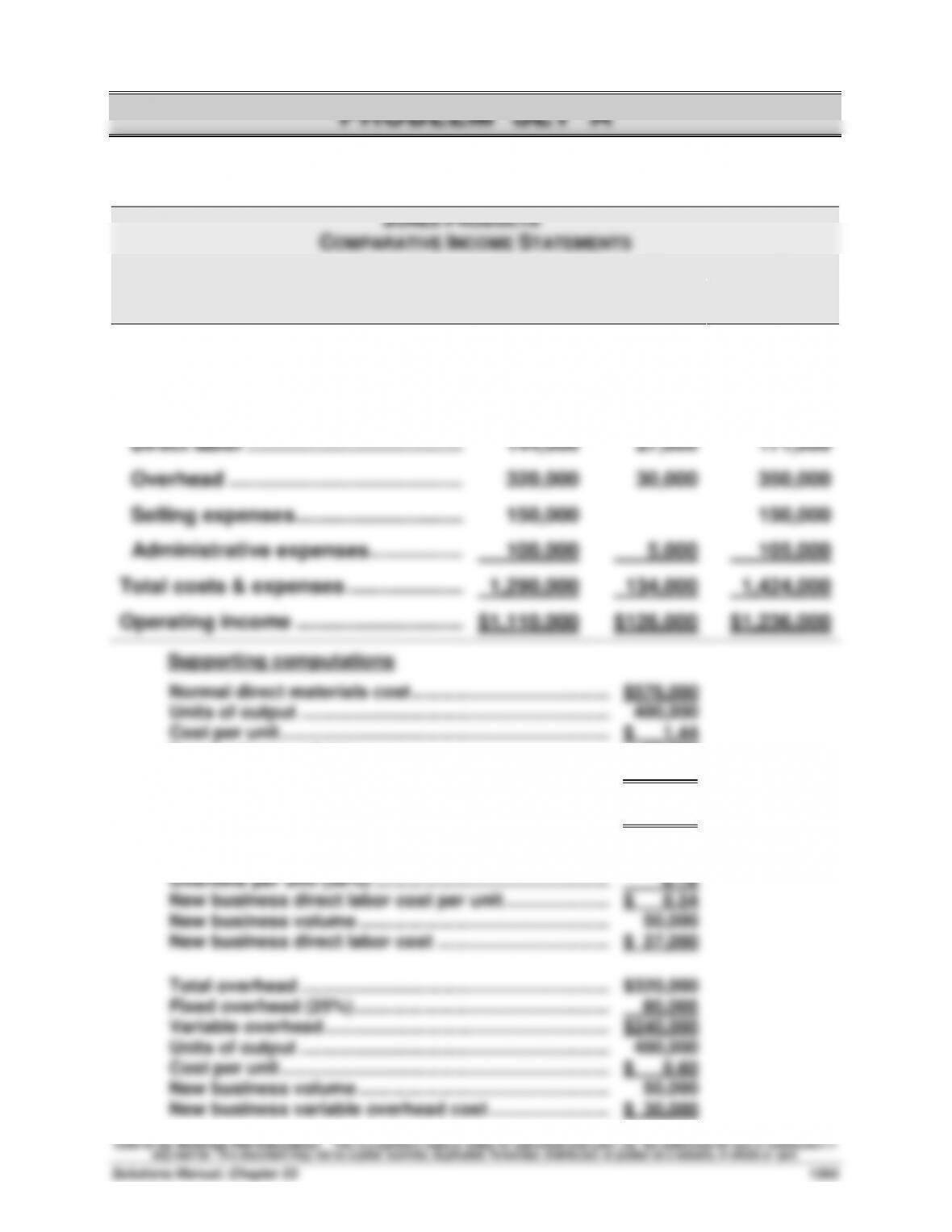

Problem 23-1A (45 minutes)

JONES PRODUCTS

COMPARATIVE INCOME STATEMENTS

(1)

(2)

(3)

Normal

New

Volume

Business

Combined

Sales ............................................................

$2,400,000

$260,000

$2,660,000

Costs and expenses

Direct materials ................................

576,000

72,000

648,000

Direct labor ...............................................

144,000

27,000

171,000

Overhead ..................................................

320,000

30,000

350,000

Selling expenses ................................

150,000

150,000

Administrative expenses.........................

100,000

5,000

105,000

Total costs & expenses .............................

1,290,000

134,000

1,424,000

Operating income ................................

$1,110,000

$126,000

$1,236,000

Supporting computations

Normal direct materials cost ..........................................

$576,000

Units of output ................................................................

400,000

Cost per unit .....................................................................

$ 1.44

New business volume .....................................................

50,000

New business direct materials cost ..............................

$ 72,000

Normal direct labor cost .................................................

$144,000

Units of output ................................................................

400,000

Cost per unit .....................................................................

$ 0.36

Overtime per unit (50%) ..................................................

0.18

New business direct labor cost per unit .......................

$ 0.54

New business volume .....................................................

50,000

New business direct labor cost .....................................

$ 27,000

Total overhead ................................................................

$320,000

Fixed overhead (25%) ......................................................

80,000

Variable overhead ............................................................

$240,000

Units of output ................................................................

400,000

Cost per unit .....................................................................

$ 0.60

New business volume .....................................................

50,000

New business variable overhead cost ..........................

$ 30,000

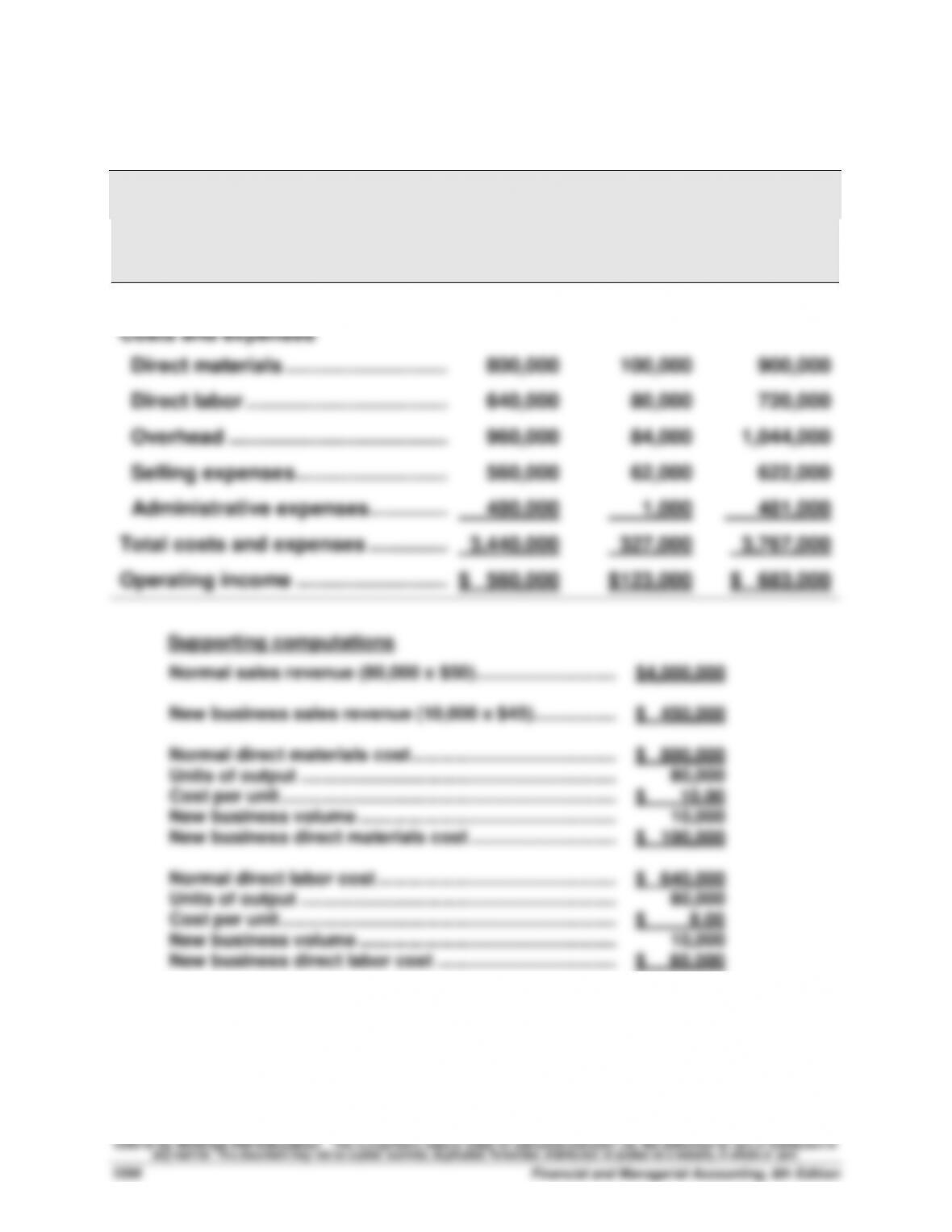

Problem 23-2A (50 minutes)

Part 1

CALLA COMPANY

COMPARATIVE INCOME STATEMENTS

(a)

(b)

(c)

Normal

New

Volume

Business

Combined

Sales ..................................................

$4,000,000

$450,000

$4,450,000

Costs and expenses

Direct materials ..............................

800,000

100,000

900,000

Direct labor .....................................

640,000

80,000

720,000

Overhead ........................................

960,000

84,000

1,044,000

Selling expenses ............................

560,000

62,000

622,000

Administrative expenses...............

480,000

1,000

481,000

Total costs and expenses ...............

3,440,000

327,000

3,767,000

Operating income ............................

$ 560,000

$123,000

$ 683,000

Supporting computations

Normal sales revenue (80,000 x $50).............................

$4,000,000

New business sales revenue (10,000 x $45) .................

$ 450,000

Normal direct materials cost ..........................................

$ 800,000

Units of output .................................................................

80,000

Cost per unit .....................................................................

$ 10.00

New business volume .....................................................

10,000

New business direct materials cost ..............................

$ 100,000

Normal direct labor cost .................................................

$ 640,000

Units of output .................................................................

80,000

Cost per unit .....................................................................

$ 8.00

New business volume .....................................................

10,000

New business direct labor cost .....................................

$ 80,000

Problem 23-2A (concluded)

Total overhead .................................................................

$ 960,000

Fixed overhead (30%) ......................................................

288,000

Variable overhead ............................................................

$ 672,000

Units of output .................................................................

80,000

Cost per unit .....................................................................

$ 8.40

New business volume .....................................................

10,000

New business variable overhead cost ..........................

$ 84,000

Total selling expenses ....................................................

$ 560,000

Fixed selling expenses (40%) .........................................

224,000

Variable selling expenses ...............................................

336,000

Units of output .................................................................

80,000

Cost per unit .....................................................................

$ 4.20

Plus additional selling expenses per unit ....................

2.00

Total selling cost per unit for this order .......................

$ 6.20

New business volume .....................................................

10,000

New business selling expenses.....................................

$ 62,000

Part 2

Based on the financial analysis above, Calla should accept the order. The

order provides additional income of $123,000. Other factors that Calla

should consider are:

Will the customer expect additional skateboards at this special price?

Will regular customers demand a reduction in their price?

Can Calla maintain quality and production at full capacity?

Part 3

If the new customer demands 15,000 units instead of 10,000, this will mean

that Calla will lose sales of 5,000 units at the regular price. They will have

to consider the contribution margin lost on these units, as well as whether

their regular customers will go elsewhere to obtain their skateboards. This

could lead to a permanent loss of volume at the regular price of $50 per

unit.

Problem 23-3A (30 minutes)

Part 1

INCREMENTAL COST OF MAKING RX5

Variable costs:

Direct materials (50,000 units x $5.00 per unit) ............................

$250,000

Direct labor (50,000 units x $8.00 per unit) ...................................

400,000

Variable overhead ($450,000* x 20%) ............................................

90,000

Total incremental cost of making 50,000 units ...............................

$740,000

* Total overhead = 50,000 units x $9.00 per unit = $450,000

INCREMENTAL COST OF BUYING THE PART

Cost per unit to buy ...........................................................................

$ 18.00

Total incremental cost of buying 50,000 units ................................

$900,000

Haver is better off making RX5.

Part 2

Other factors Haver should consider besides cost are:

Will the supplier provide the quality that Haver needs?

Will the supplier provide the RX5 on a timely basis?

Will the supplier’s cost remain at $18 per unit or will it go up or down?

What can Haver do in the space that is now used to produce RX5? Can

they produce something that will provide additional income?