CHAPTER 23

RELEVANT COSTING FOR MANAGERIAL DECISIONS

Related Assignment Materials

Student Learning Objectives

Questions

Quick

Studies*

Exercises*

Problems*

Beyond the

Numbers

Conceptual objectives:

C1. Describe the importance of

relevant costs for short-term

decisions.

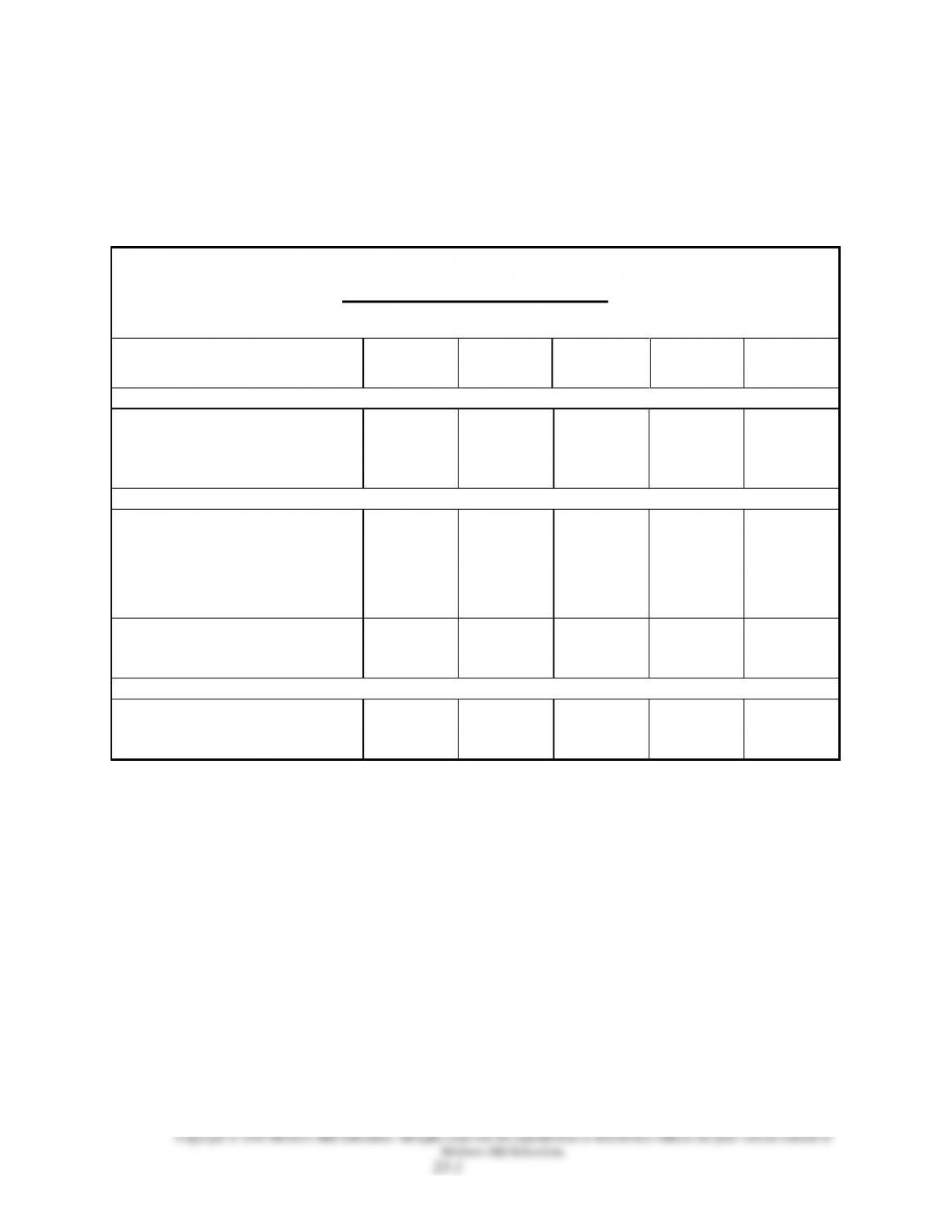

23-1,23-2,

23-3, 23-4,

23-5, 23-7,

23-8

23-5

23-1

23-1, 23-2,

23-3, 23-9

Analytical objectives:

A1. Evaluate short-term managerial

decisions using relevant costs.

23-9

23-2, 23-4,

23-6, 23-7,

23-8, 23-9,

23-10, 23-11,

23-12, 23-13,

23-14, 23-15

23-2, 23-3,

23-4, 23-5,

23-6, 23-7,

23-8, 23-9,

23-10, 23-11,

23-12, 23-13

23-1, 23-2,

23-3, 23-4,

23-5, 23-6

23-5, 23-7

A2. Determine product selling

price based on total costs.

23–10

Procedural objectives:

P1. Identify relevant costs and

apply them to managerial

decisions.

23-3, 23-4,

23-5, 23-6,

23-7, 23-8

23-1, 23-32

23-2, 23-3,

23-4

23-1, 23-4,

23-6, 23-8,

* See additional information on next page that pertains to these quick studies, exercises and problems.

Additional Information on Related Assignment Material

Connect (Available on the instructor’s course-specific website) repeats all numerical Quick Studies, all

Exercises and Problems Set A. Connect provides new numbers each time the Quick Study, Exercise or

Problem is worked. It allows instructors to monitor, promote, and assess student learning. It can be used

in practice, homework, or exam mode.

Synopsis of Chapter Revision

Charlies Brownies—New opener

Expanded discussion and exhibits for short-term decisions, including additional

business, make or buy, scrap or rework, sell or process further, sales mix, and segment

elimination

Added a Need-to-Know illustration for each short-term decision

New Global View on segment elimination

Added 3 Quick Studies

Chapter Outline

Decisions and Information

Emphasis is on use of quantitative measures to make important short-term

decisions. Costs and other factors relevant to decision must be identified.

I. Decisions and Information

A. Decision Making

1. Five steps involved in managerial decision making.

a. Define the decision task

b. Identify alternative courses of action.

c. Collect relevant information and evaluate each alternative.

d. Select the preferred course of action.

e. Analyze and assess the decision.

2. Both managerial and financial accounting information play

important role in making decisions

a. Accounting system provides primarily financial

information such as performance reports and budget

analyses.

b. Non-financial information is also relevant, such as

environmental effects, political sensitivities, and social

responsibility.

B. Relevant Costs and Benefits

1. Most financial measures from cost accounting systems are

based on historical amounts; however, relevant costs, or

avoidable costs, are especially useful. Three types of costs:

a. Sunk cost arises from a past decision; cannot be avoided or

changed, and not relevant to future decisions.

b. Out-of-pocket cost requires future outlay of cash and

results from result of management’s decisions; is relevant.

c. Opportunity cost is a potential benefit lost by taking

specific action when two or more alternative choices are

available; consideration is important.

2. Relevant costs in making decisions are the incremental, also

called differential costs, which are the additional costs

incurred if a company pursues a certain course of action.

3. Relevant benefits are additional or incremental revenue

generated by selecting a particular course of action over

another; relevant to decision-making.

Notes

Chapter Outline

II. Managerial Decision Scenariosconsider each decision task

discussed below independent from the others.

A. Additional Business

1. Effect on net income must be considered when deciding

whether to accept or reject an order; reject if loss results.

2. Historical costs are not relevant to this decision.

3. Incremental or additional costs (also called differential costs)

are additional costs incurred if company pursues certain

course of action; relevant to this decision.

4. Minimum acceptable price per unit can be determined by

dividing incremental cost by the number of units in the order.

5. Incremental costs of additional volume are relevant.

6. If additional volume approaches or exceeds existing available

capacity of factory, incremental costs required to expand

capacity may quickly exceed incremental revenue.

7. Accepting order may cause existing sales to decline; the

contribution margin lost from the decline in sales is an

opportunity cost and is relevant (if future cash flows over

several time periods are affected, net present value should be

computed).

8. Note – Allocated overhead costs, which are historical costs,

should not automatically be considered; only incremental costs

to be incurred are relevant.

9. Key point: management must not blindly use historical costs,

especially allocated to overhead costs. Instead the accounting

system needs to provide incremental cost information if the

additional business is accepted.

B. Make or Buy

1. When determining whether to make or buy a component of a

product, only incremental costs are relevant.

2. Only incremental (additional) overhead costs are relevant; an

incremental overhead rate should be determined.

3. If the incremental costs of making the component exceed the

purchase price paid to buy the component, decision rule would

be to buy; however, several other factors should be

considered.

a. Product quality.

b. Timeliness of delivery (especially in JIT settings).

c. Reactions of customers and suppliers.

d. Other intangibles (employee morale and workload).

e. Must also consider if making the part will require

incremental fixed costs to expand plant capacity.

4. Make or buy decision for component parts can also be used for

decisions about the outsourcing of services.

Notes

Chapter Outline

C. Scrap or Rework

1. Costs already incurred in manufacturing units of product not

meeting quality are sunk costs and are irrelevant in any

decision on whether to sell to substandard units as scrap or

rework to meet quality standards.

2. Incremental revenues, incremental costs of reworking defects,

and opportunity costs (the contribution margin lost if sales of

other units are given up) are all relevant.

D. Sell or Process Further

1. Partially completed products can be sold as is or they can be

processed further and then sold as other products.

2. Compute incremental revenue from further processing

(amount of revenue after further processing less revenue from

selling the products as partially completed)

3. Compute incremental cost from further processing.

4. Process further and sell if incremental revenue from further

processing exceeds related incremental costs.

E. Sales Mix Selection

1. When more that one product is sold, some are likely to be

more profitable than others; management should concentrate

sales efforts on more profitable products.

2. If production facilities or other factors are limited, an increase

in production and sale of one product usually requires

reduction in production and sale of others.

3. The most profitable combination, or sales mix, of products

should be determined. To identify the best sales mix,

management focuses on the contribution margin per unit of

scarce resource. The scarce resource could be the machines

used to make the products.

4. Determine the contribution margin of each product, the

facilities required to produce these products and any

constraints on facilities and markets for the products.

5. If demand is unlimited and the products use the same inputs

then the product with the highest contribution margin should

be produced.

6. If demand is unlimited but the products use different inputs

then determine contribution margin per unit of the constraint

(the factor that limits capacity, such as machine time

required); produce the product with the highest contribution

margin per unit of the constraint.

7. If demand is limited then the company should first produce the

most profitable product, up to the point of the total demand.

The remaining capacity should be used to produce the next

most profitable product.

Notes

Chapter Outline

F. Segment Elimination

1. If segment, division, or store is performing poorly,

management must consider eliminating it.

2. It is not sufficient to base the decision on net income (loss) or

its contribution to overhead.

3. Need to consider avoidable and unavoidable expenses:

a. Avoidable (or escapable) expenses are costs or expenses

that would not be incurred if the segment is eliminated.

b. Unavoidable (or inescapable) expenses are costs or

expenses that would continue even if the segment is

eliminated.

4. Decision rule – Segment is candidate for elimination if its

revenues are less than its avoidable expenses.

5. Should also assess impact of elimination on other segments.

a. An unprofitable segment might contribute to another

segment’s revenue and expenses

b. A profitable segment might be eliminated if its space,

assets and staff can be more profitably used by another

segment or new segment.

G. Keep or Replace Equipment

1. Must decide whether the reduction in variable manufacturing

costs over its life is greater than the net purchase price of the

new equipment.

a. Net purchase price is the cost of the new equipment less

any trade in allowance given or cash receipt for the old

equipment.

b. Book value of the old equipment is not used. It is a sunk

cost.

III. Decision AnalysisSetting Product Price

A. Relevant costs are useful to management in determining prices for

special short-term decisions.

B. Longer run pricing decisions need to cover both variable and fixed

costs and yield a profit.

C. Methods to help in setting prices include cost-plus methods, where

management sets price equal to product’s total costs plus desired

profit.

D. Four-step process includes:

1. Determine total costs

2. Determine total cost per unit

3. Determine dollar markup per unit

4. Determine selling price per unit

Notes

Chapter 23: Alternate Demonstration Problem

Modern Company manufactures wood desks. They have the opportunity to

buy handles for the desks at $8 per unit. This purchase would affect costs

as follows:

Make Buy

Unit selling price: $340 $340

Volume (monthly) 500 500

Unit variable cost $ 95 $ 88

Price to purchase $ 0 $ 8

Fixed costs $5,500 $4,700

Decide whether the part should be made or purchased.

Solution: Chapter 23 Alternate Demonstration Problem

Buy Make

Revenue $170,000 $170,000

Less:

Variable costs 48,000 47,500

Contribution Margin $ 122,000 $ 122,500

Less:

Fixed Costs 4,700 5,500

Operating Profit $ 117,300 $ 117,000

Operating Profit is $300 higher if Modern purchases the handles instead of

making them.