Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Exercise 22-11 (20 minutes)

(1)

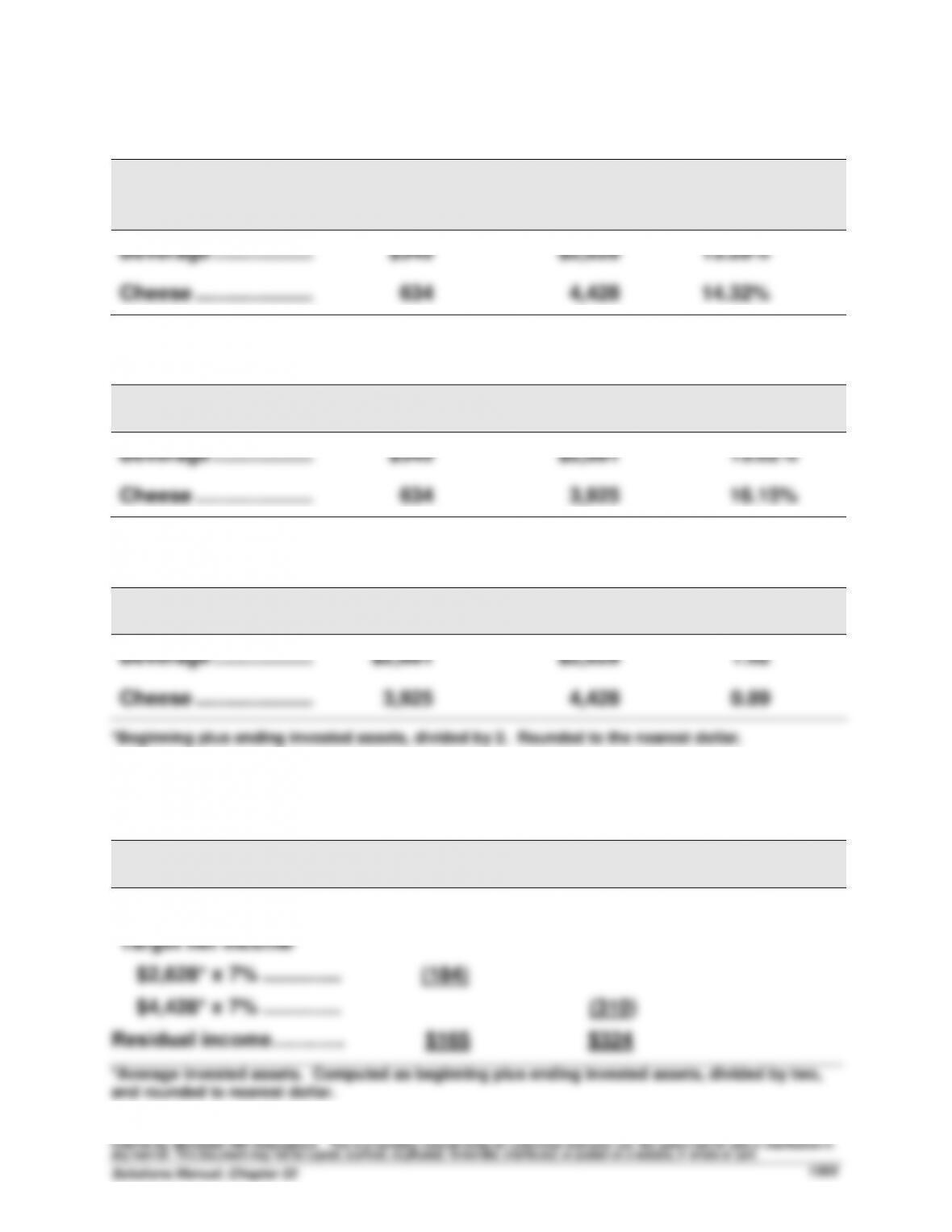

Investment center

Operating

income

Average assets*

Return on

investment

Beverage .......................

$349

$2,628

13.28%

Cheese ..........................

634

4,428

14.32%

(2)

Investment center

Operating

income

Sales

Profit margin

Beverage .......................

$349

$2,681

13.02%

Cheese ..........................

634

3,925

16.15%

(3)

Investment center

Sales

Average assets*

Investment

turnover

Beverage .......................

$2,681

$2,628

1.02

Cheese ..........................

3,925

4,428

0.89

*Beginning plus ending invested assets, divided by 2. Rounded to the nearest dollar.

Exercise 22-12 (10 minutes)

($ millions)

Beverage

Cheese

Operating income ........

$349

$634

Target net income

$2,628* x 7% ..............

$4,428* x 7% ..............

(184)

(310)

Residual income…….…. $165 $324

*Average invested assets. Computed as beginning plus ending invested assets, divided by two,

and rounded to nearest dollar.

Exercise 22-13 (15 minutes)

Investment center

Operating

income

Sales

Profit margin

Americas .......................

$22,817

$62,739

36.4%

Europe ...........................

13,025

37,883

34.4%

China .............................

8,541

25,417

33.6%

Exercise 22-14 (20 minutes)

1. Return on investment = $1,000,000/$12,500,000 = 8%

2. Profit margin = $1,000,000/$5,000,000 = 20%

3. Predicted 2016 sales = $5,000,000 x 120% = $6,000,000

4. Predicted 2016 investment turnover = $6,000,000/$12,500,000 = 0.48

Exercise 22-15 (20 minutes)

1. F 8. P

2. C 9. C

3. C 10. I

4. C 11. P

5. I 12. P

6. F 13. F

7. F 14. F

Exercise 22-16 (15 minutes)

Part 1

Process time ..............................................................................

6.0 days

Inspection time ..........................................................................

0.8 days

Move time ...................................................................................

3.2 days

Wait time ....................................................................................

5.0 days

Manufacturing cycle time .........................................................

15.0 days

Part 2

Manufacturing cycle efficiency (6.0 days/ 15.0 days) ............

0.40

This means that Oakwood is spending 40% of its time in value-added

activities, and 60% of its time on non-value-added activities.

Part 3

If move time is reduced by 1.2 days and wait time is reduced by 2.8 days,

manufacturing cycle time will be reduced to 11.0 days. Manufacturing

cycle efficiency will be 0.545, computed as 6.0 days divided by 11.0 days.

Exercise 22-17 (15 minutes)

Part 1

Process time ..............................................................................

16.0 hours

Inspection time ..........................................................................

3.5 hours

Move time ...................................................................................

9.0 hours

Wait time ....................................................................................

21.5 hours

Manufacturing cycle time .........................................................

50.0 hours

Exercise 22-17 (continued)

Part 2

Manufacturing cycle efficiency (16.0 hours/ 50.0 hours) ......

0.32

This means that Best Ink is spending 32% of its time in value-added

Exercise 22-18A (15 minutes)

1. If the trailer division is currently operating at full capacity, its manager

2. If the trailer division is currently producing 20,000 trailers and the

assembly division will order 15,000 more trailers, the Trailer division will

Exercise 22-18A (continued)

3. The trailer division would prefer a transfer price of $140 per trailer, since

it provides a $60 ($140 - $80) contribution margin per trailer. At a transfer

price of $80 the trailer division reports a contribution margin of $0 per

Exercise 22-19B (20 minutes)

Preliminary calculations

Land cost ................................................................

$4,000,000

Improvements ................................................................

3,500,000

Total cost of lots ............................................................

$7,500,000

Exercise 22-20B (25 minutes)

Preliminary calculations

Lobster cost (2,400 lbs. x $4.50) ......................

$10,800

Labor cost ..........................................................

1,800

Total cost of processed lobsters ....................

$12,600

Exercise 22-21 (20 minutes)

(1) Profit margin = Income/Sales

Investment center

Income*

Sales*

Profit margin

Professional products ..........

€ 552

€2,717

20.32%

Consumer products ..............

1,765

9,530

18.52%

Luxury products ....................

791

4,507

17.55%

Active cosmetics...................

278

1,386

20.06%

*In € millions

The professional products department has the highest profit margin.

(2) Investment turnover = Sales/Average invested assets

Investment center

Sales*

Avg. assets*

Investment

turnover

Professional products ..........

€2,717

€2,570

1.06

Consumer products ..............

9,530

5,745

1.66

Luxury products ....................

4,507

3,855

1.17

Active cosmetics...................

1,386

824

1.68

*In € millions. Avg. assets = Beginning assets plus ending assets, divided by two.

Note: Profit margin and investment turnover amounts are rounded to two decimal places.

The Active cosmetics department has the highest investment turnover.

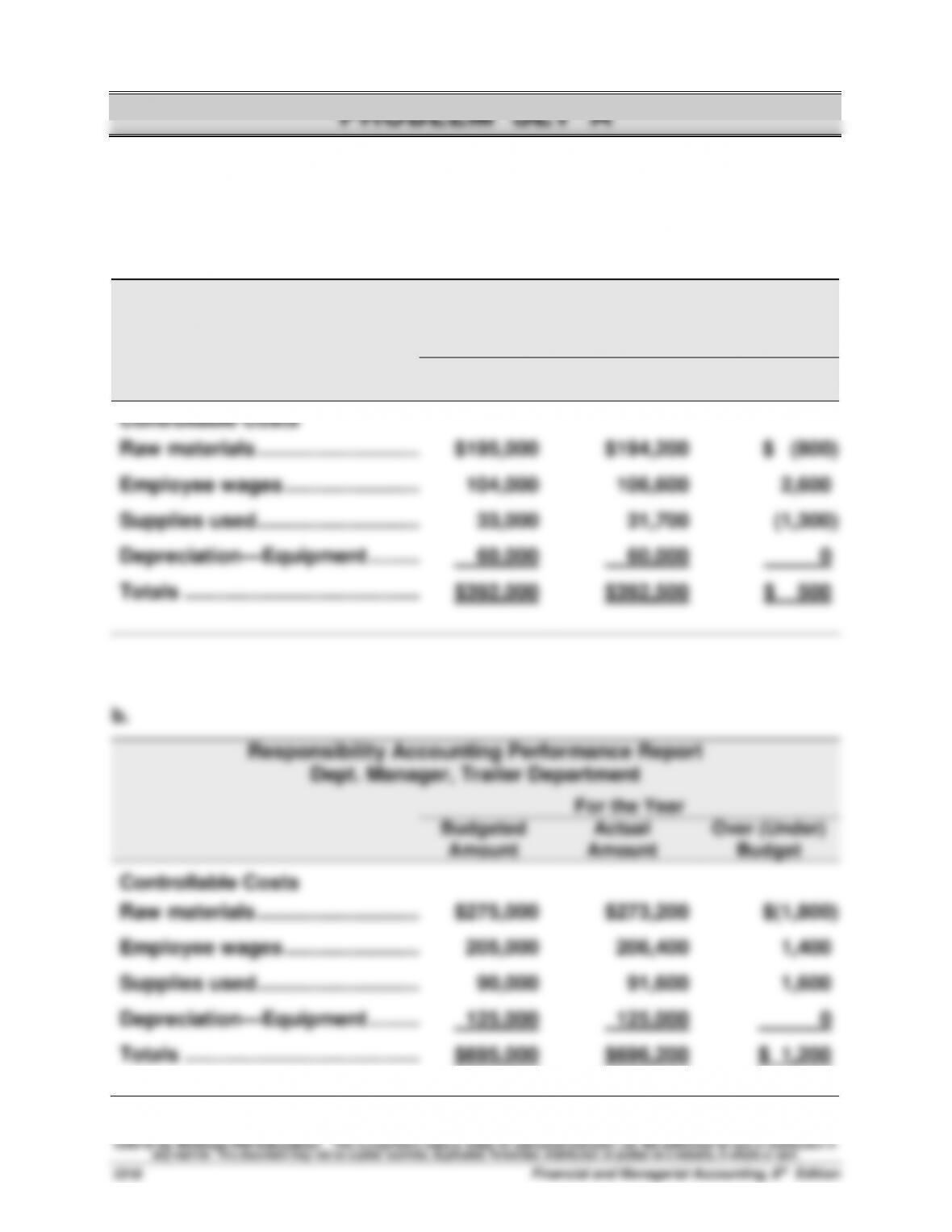

Problem 22-1A (50 minutes)

Part 1

a.

Responsibility Accounting Performance Report

Dept. Manager, Camper Department

For the Year

Budgeted

Actual

Over (Under)

Amount

Amount

Budget

Controllable Costs

Raw materials ................................

$195,000

$194,200

$ (800)

Employee wages ..............................

104,000

106,600

2,600

Supplies used ................................

33,000

31,700

(1,300)

Depreciation—Equipment ...............

60,000

60,000

0

Totals ................................................

$392,000

$392,500

$ 500

Problem 22-1A (Continued)

c.

Responsibility Accounting Performance Report

Plant Manager, Indiana Plant

For the Year

Budgeted

Actual

Over (Under)

Amount

Amount

Budget

Controllable Costs

Dept. manager salaries.................

$ 95,000

$ 97,500

$ 2,500

Utilities ...........................................

9,000

8,300

(700)

Building rent ................................

15,000

14,000

(1,000)

Other office salaries .....................

32,500

30,100

(2,400)

Other office costs .........................

25,000

23,000

(2,000)

Camper department ......................

392,000

392,500

500

Trailer department ........................

695,000

696,200

1,200

Total ...............................................

$1,263,500

$1,261,600

$ (1,900)

Part 2

The plant manager did a better job of controlling costs and meeting the

budget. She came in under budget for the plant even though she paid the

department managers more than budgeted and had to absorb the amounts

over budget in their departments. This is because she spent less than the

budget amount on utilities, building rent, other office salaries, and other

office costs. Each of the department managers came in over budget.

Problem 22-2A (60 minutes)

Part 1

Average occupancy cost = $66,000 / 8,000 sq. ft. = $8.25 per sq. ft.

These costs are assigned to the two departments as follows

Department

Square Footage

Rate

Total

Linder’s Dept. ...............

1,000

$8.25

$ 8,250

Chiro’s Dept. .................

1,800

8.25

$14,850

*A total of $23,100 ($8,250 + $14,850) in occupancy costs is allocated to these

departments. The company would follow a similar approach in allocating the remaining

occupancy costs ($42,900, computed as $66,000 - $23,100) to its other departments (not

shown in this problem).

Part 2

Market rates are used to allocate occupancy costs for depreciation,

interest, and taxes. Heating, lighting, and maintenance costs are allocated

to the departments on both floors at the average rate per square foot.

These costs are separately assigned to each class as follows:

Total

Costs

Value-Based

Costs

Usage-Based

Costs

Depreciation—Building ...................

$18,000

$18,000

Interest—Building mortgage...........

27,000

27,000

Taxes—Building and land ...............

9,000

9,000

Gas (heating) expense.....................

3,000

$ 3,000

Lighting expense .............................

3,000

3,000

Maintenance expense ......................

6,000

______

6,000

Total ..................................................

$66,000

$54,000

$12,000