Quick Study 22–19 (5 minutes)

Average invested assets = (€12,888 + €13,099) / 2

EXERCISES

Exercise 22-1 (30 minutes)

(1) Items included in performance report

The following items definitely should be included in the performance

report for the auto service department manager because they are

(2) Items excluded from performance report

The following items definitely should be excluded from the performance

(3) Items that may or may not be included in performance report

The following items cannot be definitely included or definitely excluded

from the performance report because they may or may not be

completely under the manager’s control or strong influence:

Exercise 22-2 (20 minutes)

MARATHON RUNNING SHOP

Departmental Expense Allocation Spreadsheet

For Year Ended December 31, 2015

Allocation of Expenses to Departments .

Alloca–

tion

Base

Expense

Account

Balance

Adver-

tising

Dept.

Admini-

strative

Dept.

Shoes

Dept.

Clothing

Dept.

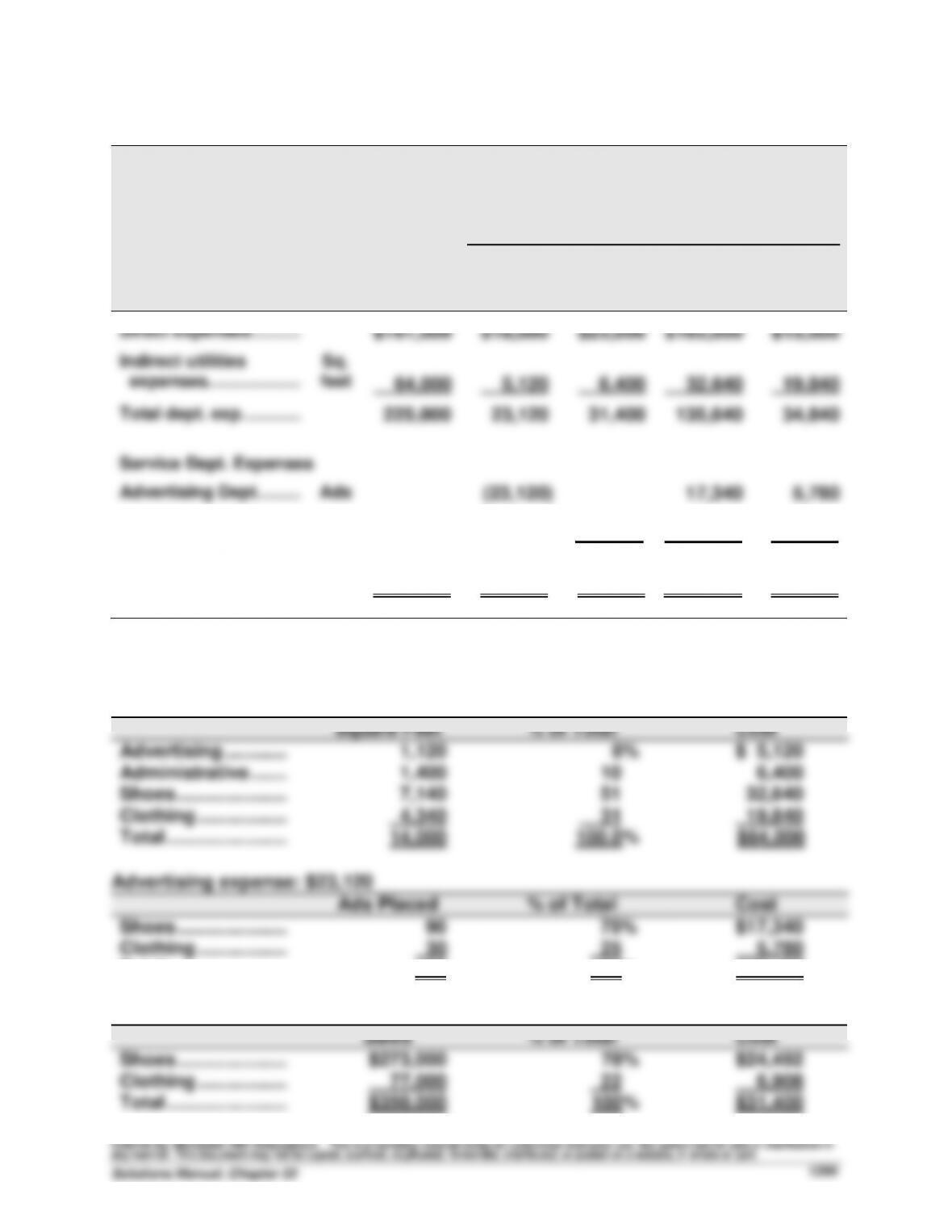

Direct expenses ………...

$161,000

$18,000

$25,000

$103,000

$15,000

Indirect utilities

expenses. ………………..

Sq.

feet

64,000

5,120

6,400

32,640

19,840

Total dept. exp. ………....

225,000

23,120

31,400

135,640

34,840

Service Dept. Expenses

Advertising Dept. ……....

Ads

(23,120)

17,340

5,780

Administrative Dept. ....

Sales

______

(31,400)

24,492

6,908

Total exp. allocated

to operating depts.. ....

$225,000

$ 0

$ 0

$177,472

$47,528

Supporting expense allocation calculations

Utilities expense: $64,000

Square Feet

% of Total

Cost

Advertising …………

1,120

8%

$ 5,120

Administrative …….

1,400

10

6,400

Shoes …………………

7,140

51

32,640

Clothing ……………..

4,340

31

19,840

Total …………………..

14,000

100.0%

$64,000

Advertising expense: $23,120

Ads Placed

% of Total

Cost

Shoes …………………

90

75%

$17,340

Clothing ……………..

30

25

5,780

Total …………………..

120

100%

$23,120

Administrative expense: $31,400

Sales

% of Total

Cost

Shoes …………………

$273,000

78%

$24,492

Clothing ……………..

77,000

22

6,908

Total …………………..

$350,000

100%

$31,400

Exercise 22-3 (25 minutes)

COZY BOOKSTORE

Departmental Expense Allocation Spreadsheet

For Period Ended _______

Allocation of Expenses to Departments .

Alloca–

tion Base

Exp.

Account

Balance

Adver–

tising

Dept.

Purch-

asing

Dept.

Books

Dept.

Maga-

zines

Dept.

News-

papers

Dept.

Total dept. exp. …….………….

$698,000

$24,000

$34,000

$425,000

$90,000

$125,000

Service Dept. Expenses

Advertising Dept. ..……………..

Sales

(24,000)

13,200

5,280

5,520

Purchasing

Dept. …………………………..

Purch.

orders

______

(34,000)

14,620

10,200

9,180

Total expenses

allocated to

operating depts.

$698,000

$ 0

$ 0

$452,820

$105,480

$139,700

Computations for allocations of service dept. costs to operating departments

Advertising: $24,000

Sales

% of Total

Cost

Books Dept. …………………..……..

$495,000

55%

$13,200

Magazines Dept. …………….……..

198,000

22

5,280

Newspapers Dept. ………….……..

207,000

23

5,520

Totals …………………………….……..

$900,000

100%

$24,000

Purchasing: $34,000

Purchase Orders

% of Total

Cost

Books Dept. …………………..……..

516

43%

$14,620

Magazines Dept. …………….……..

360

30

10,200

Newspapers Dept. ………….……..

324

27

9,180

Totals …………………………….……..

1,200

100%

$34,000

Exercise 22-4 (20 minutes)

Allocation of annual wages between the two departments

Hours Worked*

% of Total

Cost

Jewelry Dept. …………………………..

57

75%

$22,500

Hosiery Dept. …………………………..

19

25

$ 7,500

Totals …………………………………………

76

100%

$30,000

*Computation of hours worked in the two selling departments

Jewelry department

Selling …………………………………………………..

51

Arranging and stocking …………………..……..

6

57 hours

Hosiery department

Selling …………………………………………………..

12

Arranging and stocking …………………..……..

7

19 hours

Total hours ………………………………………..……..

76 hours

Instructor note: This analysis ignores idle time because neither department

receives any direct benefit from it. Accordingly, the total wages are allocated

between the departments in proportion to the time worked in each.

Exercise 22-5 (25 minutes)

1. Allocation of Indirect Expenses to Four Operating Departments

Supervision expenses

Department

Employees

% of Total

Cost

Materials …………………………..

27

18%

$14,850

Personnel ……………………..……

9

6

4,950

Manufacturing ……………………

63

42

34,650

Packaging …………………….……

51

34

28,050

Totals …………………………..

150

100%

$82,500

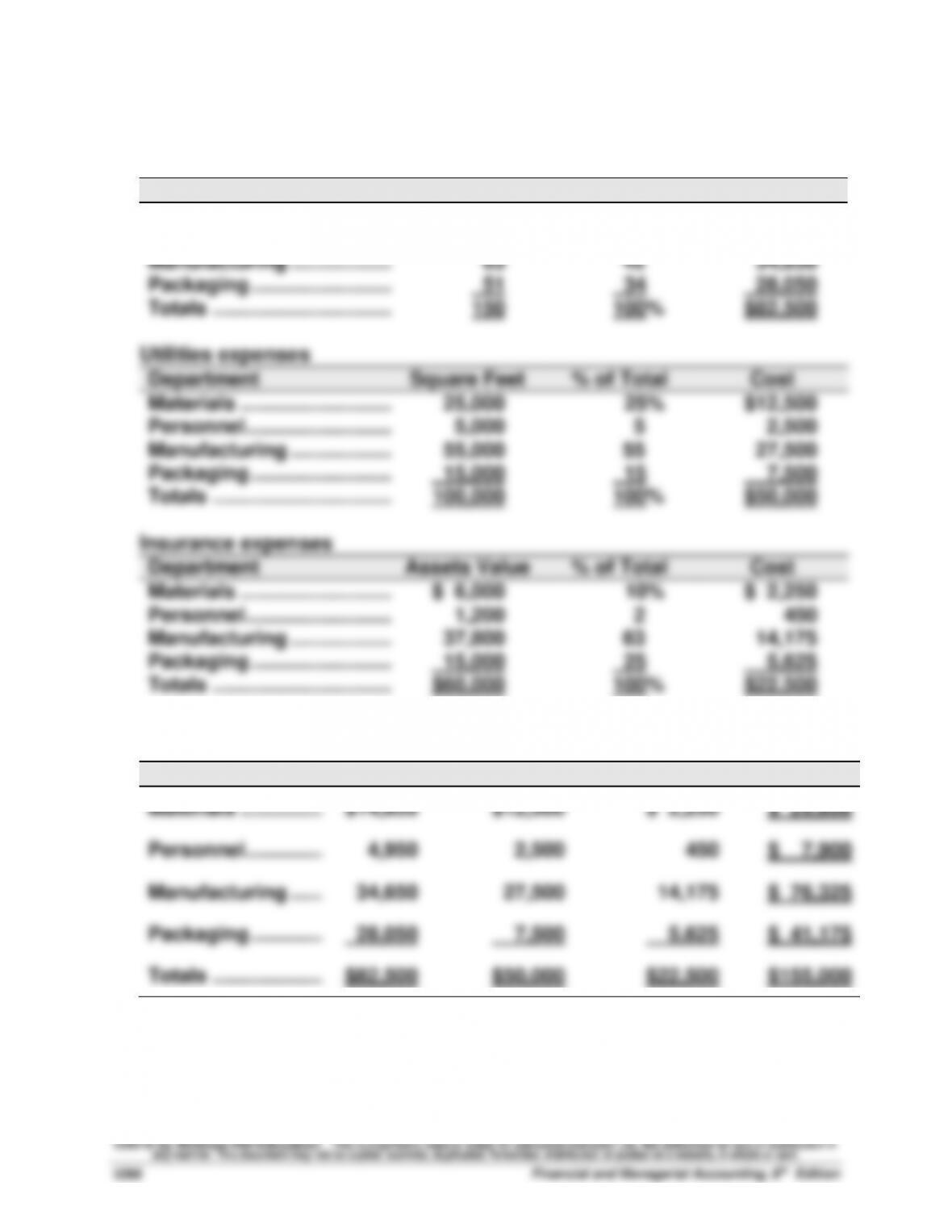

Utilities expenses

Department

Square Feet

% of Total

Cost

Materials …………………………..

25,000

25%

$12,500

Personnel ……………………..……

5,000

5

2,500

Manufacturing ……………………

55,000

55

27,500

Packaging …………………….……

15,000

15

7,500

Totals …………………………..

100,000

100%

$50,000

Insurance expenses

Department

Assets Value

% of Total

Cost

Materials …………………………..

$ 6,000

10%

$ 2,250

Personnel ……………………..……

1,200

2

450

Manufacturing ……………………

37,800

63

14,175

Packaging …………………….……

15,000

25

5,625

Totals …………………………..

$60,000

100%

$22,500

2. Report of Indirect Expenses Assigned to Four Operating Departments

Supervision

Utilities

Insurance

Total

Materials …………………………..

$14,850

$12,500

$ 2,250

$ 29,600

Personnel …………..………………

4,950

2,500

450

$ 7,900

Manufacturing ……………………

34,650

27,500

14,175

$ 76,325

Packaging ………….………………

28,050

7,500

5,625

$ 41,175

Totals ………………..…………

$82,500

$50,000

$22,500

$155,000

Exercise 22-6 (20 minutes)

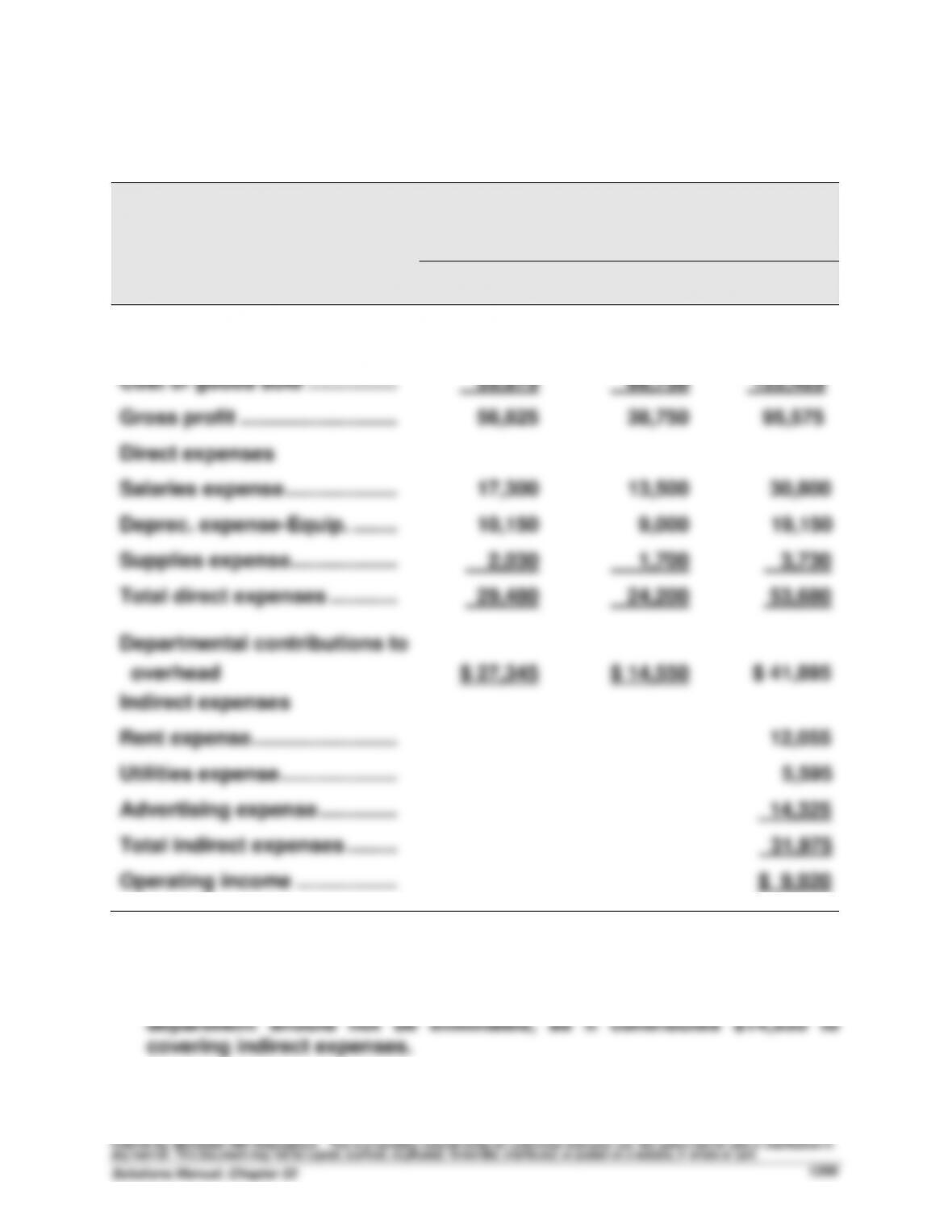

(1)

WHOLESALE GUITARS

Departmental Contribution Statements

For Year Ended December 31, 2015

Acoustic

Electric

Dept.

Dept.

Combined

Sales ………………………………….

$112,500

$105,500

$218,000

Cost of goods sold …………….

55,675

66,750

122,425

Gross profit ……………………….

56,825

38,750

95,575

Direct expenses

Salaries expense ………………..

17,300

13,500

30,800

Deprec. expense–Equip. ……..

10,150

9,000

19,150

Supplies expense……………….

2,030

1,700

3,730

Total direct expenses …………

29,480

24,200

53,680

Departmental contributions to

overhead

Indirect expenses

$ 27,345

$ 14,550

$ 41,895

Rent expense ……………………..

12,055

Utilities expense …………………

5,595

Advertising expense …………..

14,325

Total indirect expenses ………

31,975

Operating income ………………

$ 9,920

(2) Based on departmental contribution to overhead, the electric guitar

Exercise 22–7 (25 minutes)

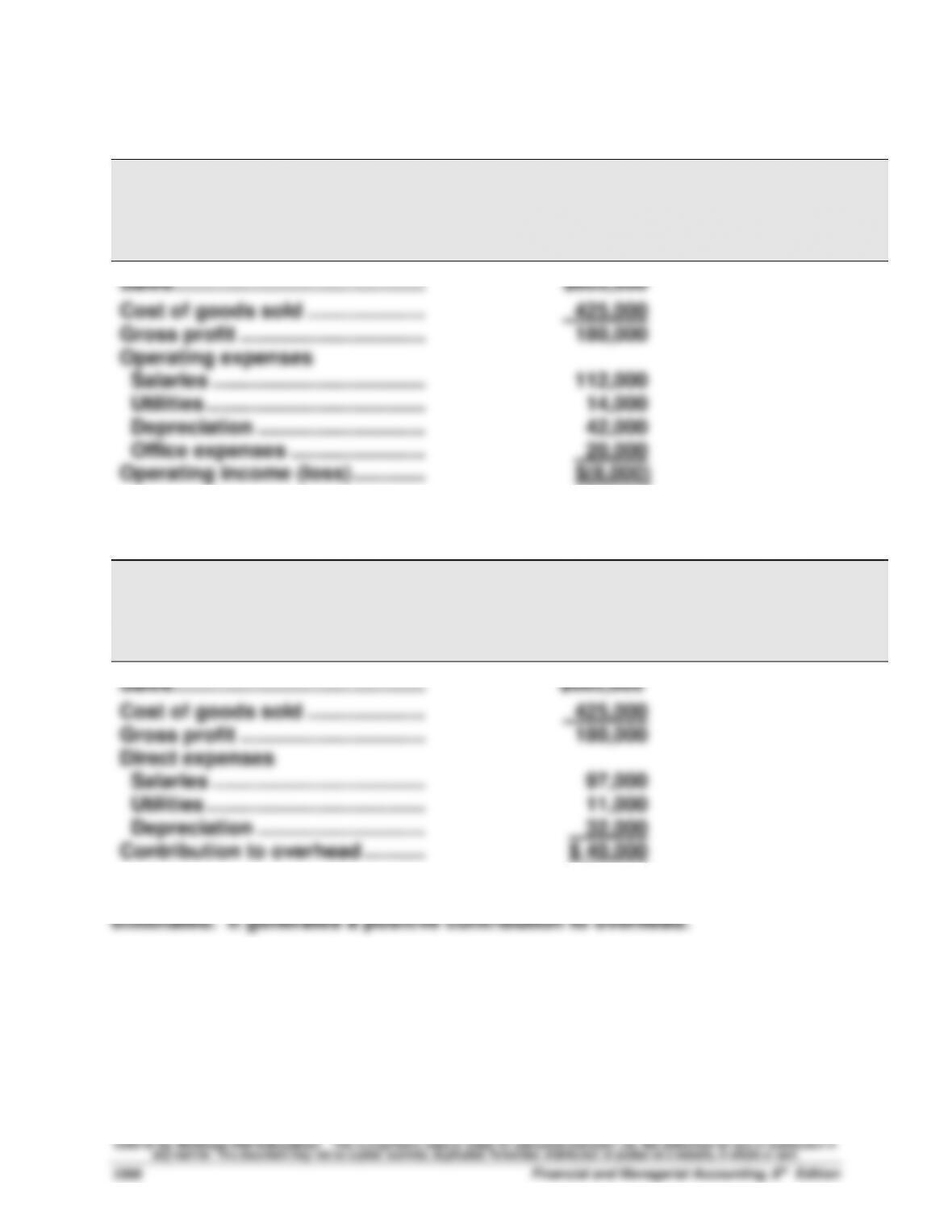

1.

JANSEN COMPANY

Departmental Income Statement—Ski Department

For Year Ended December 31, 2015

Ski Dept.

Sales ………………………………………

$605,000

Cost of goods sold …………………

425,000

Gross profit …………………………...

Operating expenses

Salaries …………………………..……

Utilities …………………………..…….

Depreciation …………………………

Office expenses ……………………

180,000

112,000

14,000

42,000

20,000

Operating income (loss) ………….

$(8,000)

2.

JANSEN COMPANY

Departmental Contribution to Overhead—Ski Department

For Year Ended December 31, 2015

Ski Dept.

Sales ………………………………………

$605,000

Cost of goods sold …………………

425,000

Gross profit …………………………...

Direct expenses

Salaries …………………………..……

Utilities …………………………..…….

Depreciation …………………………

Contribution to overhead ………..

180,000

97,000

11,000

32,000

$ 40,000

3. Based on these performance reports, the ski department should not be

Exercise 22-8 (15 minutes)

1.

Location

Net income

Average assets

Return on

investment

Location A …………..………

$160,000

$1,000,000

16%

Location B …………..………

$108,000

$ 600,000

18%

2. The recommendation is to pursue Location B because its return on

investment (assets) is 18%, compared to 16% at Location A. Moreover,

given the normal return of 18% for this chain, only Location B meets this

hurdle.

Exercise 22-9 (20 minutes)

(1)

Investment center

Income

Average assets

Return on

investment

Electronics …………….….

$2,880,000

$16,000,000

18%

Sporting Goods ……..….

2,040,000

12,000,000

17%

Comment: The electronics division is the superior investment center on the

basis of the investment center return on investment (assets).

Exercise 22-9 (continued)

(2)

Investment Center

Electronics

Sporting

Goods

Net income ………………..

$2,880,000

$2,040,000

Target net income

$16,000,000 x 12% …..

12,000,000 x 12% ……

(1,920,000)

(1,440,000)

Residual income……. $ 960,000 $ 600,000

Comment: The electronics department is the superior investment center on

the basis of investment center residual income.

(3) The electronics department should accept the new opportunity, since it

Exercise 22–10 (15 minutes)

Investment Center

Income

Sales

Profit margin

Electronics …………….….

$2,880,000

$40,000,000

7.20%

Sporting Goods ……..….

2,040,000

20,000,000

10.20%

Investment Center

Sales

Average assets

Investment

turnover

Electronics …………….….

$40,000,000

$ 16,000,000

2.50

Sporting Goods ……..….

20,000,000

12,000,000

1.67

Comments: The sporting goods department generates the most net income

per dollar of sales, as shown by its higher profit margin. The Electronics

department however is more efficient at generating sales from invested

assets, based on its higher investment turnover.