Exercise 21-22 (25 minutes)

Preliminary calculations:

Variable overhead rate per DL hour = $32,000/32,000 = $1 per hour

Fixed overhead rate per DL hour = $48,000/32,000 = $1.50 per hour

Exercise 21–22 (continued)

Part 3

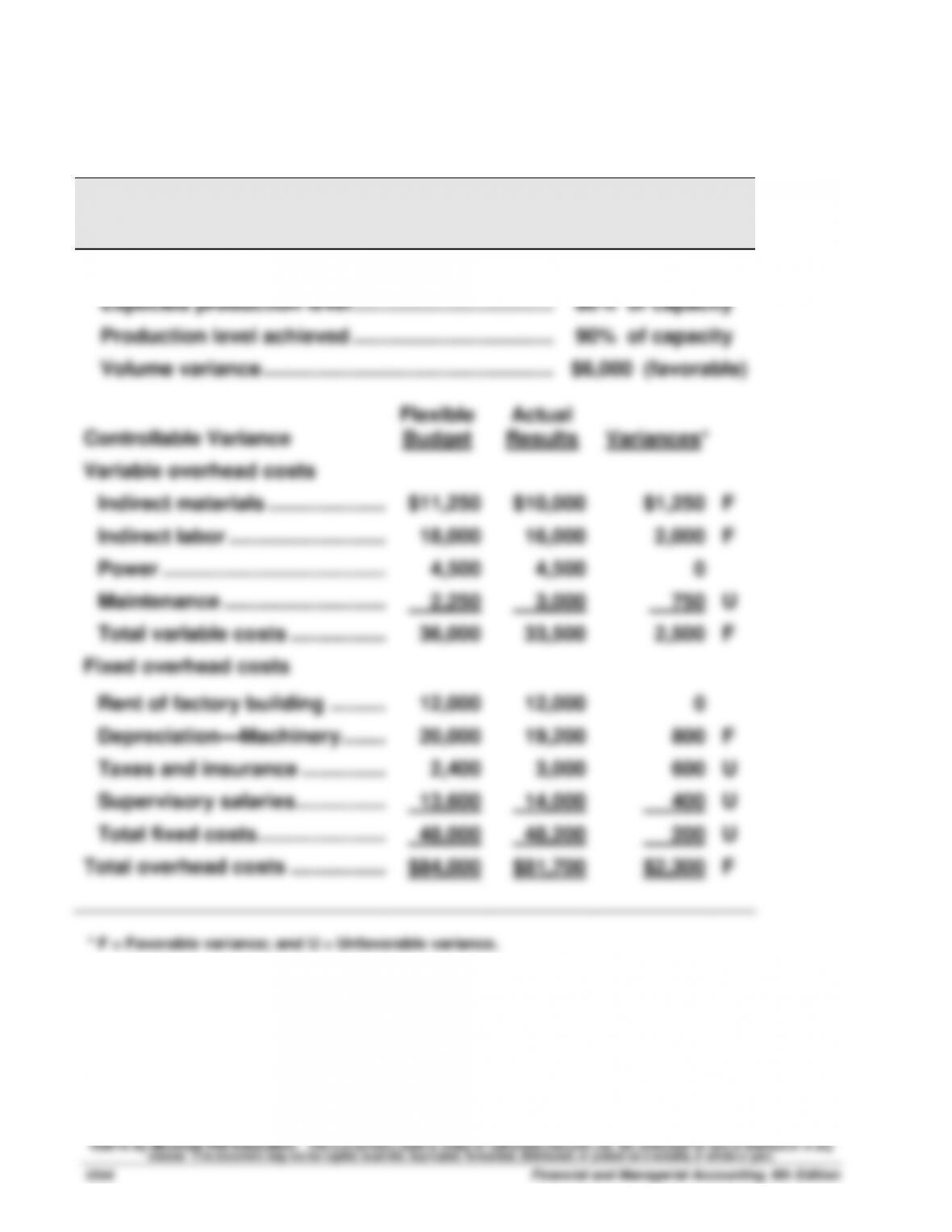

BLAZE CORP.

Overhead Variance Report

For Month Ended March 31

Volume Variance

Expected production level ……………………………………

80% of capacity

Production level achieved ……………………………………

90% of capacity

Volume variance …………………………………………….……

$6,000 (favorable)

Flexible

Actual

Controllable Variance

Budget

Results

Variances*

Variable overhead costs

Indirect materials ………………………

$11,250

$10,000

$1,250

F

Indirect labor ……………………….….

18,000

16,000

2,000

F

Power ………………………………….……

4,500

4,500

0

Maintenance ………………………..…

2,250

3,000

750

U

Total variable costs ……………..……

36,000

33,500

2,500

F

Fixed overhead costs

Rent of factory building ……….……

12,000

12,000

0

Depreciation—Machinery ……..……

20,000

19,200

800

F

Taxes and insurance …………………

2,400

3,000

600

U

Supervisory salaries …………….……

13,600

14,000

400

U

Total fixed costs…………………..……

48,000

48,200

200

U

Total overhead costs ……………..……

$84,000

$81,700

$2,300

F

* F = Favorable variance; and U = Unfavorable variance.

Exercise 21–23 (25 minutes)

1. Sales price and sales volume variances

Sales Actual Sales

Flexible Budget

Fixed Budget

Units 350

350

365

Price/unit $1,200

$1,100

$1,100

(350 x $1,200)

(350 x $1,100)

(365 x $1,100)

Total $420,000

$385,000

$401,500

$35,000 F

(Sales price variance)

$16,500 U

(Sales volume variance)

2. Interpretation

The $35,000 favorable sales price variance implies it sold computers for a

increase.

©2016 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any

manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or par t.

Financial and Managerial Accounting, 6th Edition

1246

PROBLEM SET A

Problem 21-1A (60 minutes)

Part 1

Variable or Fixed Classification

Amount

per unit

Variable sales (total divided by 15,000 units)

Sales ……………………………………………………………………………………..

$ 200.00

Variable costs (total divided by 15,000 units)

Direct materials ……………………………………………………….…………….

$ 65.00

Direct labor …………………………………………………………………………...

15.00

Machinery repairs ………………………………………………………………….

4.00

Utilities ($45,000 variable) ……………………………………………………...

3.00

Packaging …………………………..………………………………………………...

5.00

Shipping ………………………………………………………………………………..

7.00

Total variable costs………………………………………………………………..

$ 99.00

Fixed costs

Depreciation—Plant equipment …………………………..………………….

$ 300,000

Utilities ($195,000 – $45,000 variable) ……………………………………...

150,000

Plant management salaries …………………………………………………….

200,000

Sales salary …………………………………………………………………………..

250,000

Advertising expense ……………………………………………………………...

125,000

Salaries ………………………………………………………………………………...

241,000

Entertainment expense…………………………………………………………..

90,000

Total fixed costs …………………………………………………………………….

$1,356,000

Problem 21-1A (Continued)

Part 2

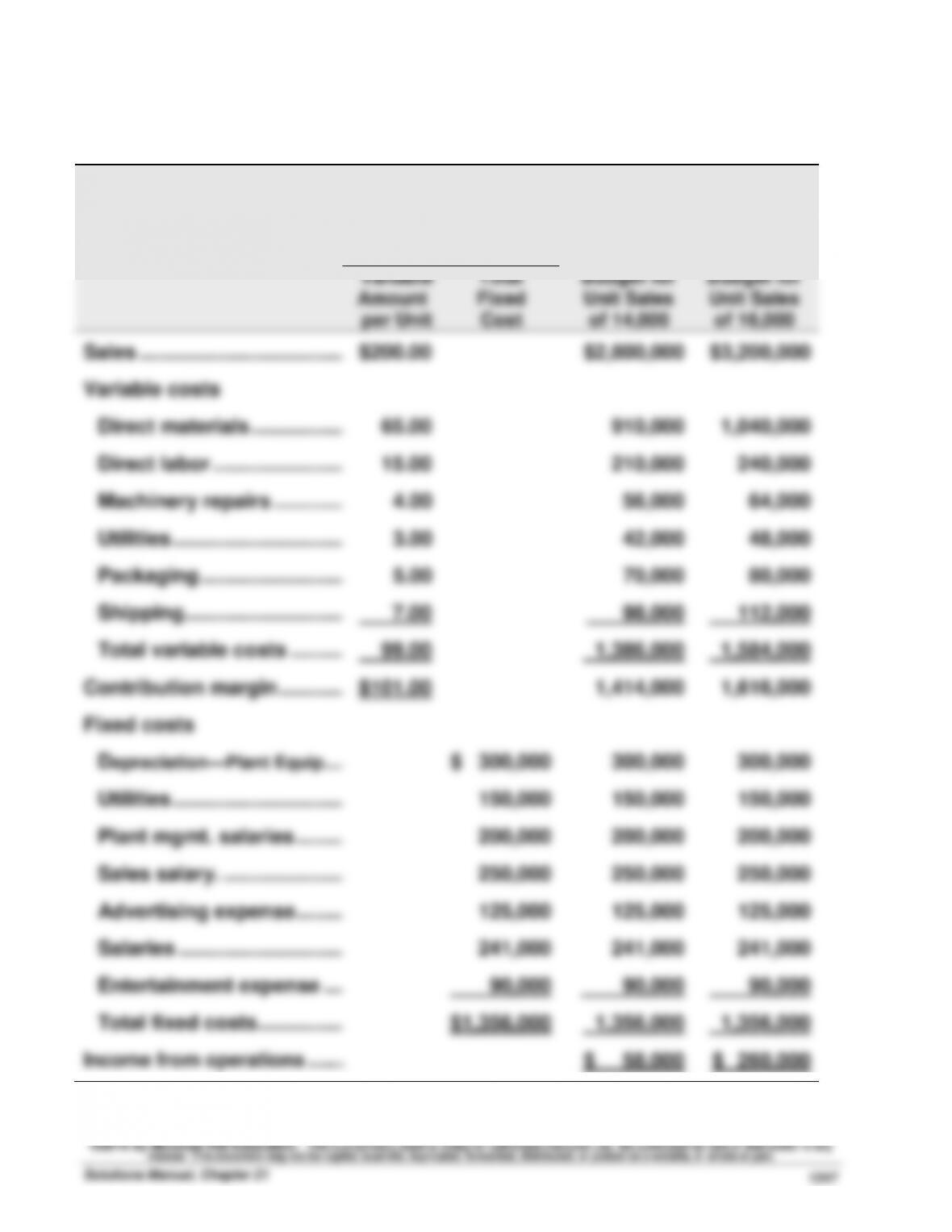

PHOENIX COMPANY

Flexible Budgets

For Year Ended December 31, 2015

Flexible Budget

Flexible

Flexible

Variable

Amount

per Unit

Total

Fixed

Cost

Budget for

Unit Sales

of 14,000

Budget for

Unit Sales

of 16,000

Sales ……………………………….

$200.00

$2,800,000

$3,200,000

Variable costs

Direct materials ……………..

65.00

910,000

1,040,000

Direct labor ……………………

15.00

210,000

240,000

Machinery repairs ………….

4.00

56,000

64,000

Utilities ………………………….

3.00

42,000

48,000

Packaging ……………………..

5.00

70,000

80,000

Shipping………………………..

7.00

98,000

112,000

Total variable costs ……….

99.00

1,386,000

1,584,000

Contribution margin …………

$101.00

1,414,000

1,616,000

Fixed costs

Depreciation—Plant Equip ….

$ 300,000

300,000

300,000

Utilities ………………………….

150,000

150,000

150,000

Plant mgmt. salaries ………

200,000

200,000

200,000

Sales salary. ………………….

250,000

250,000

250,000

Advertising expense ………

125,000

125,000

125,000

Salaries …………………………

241,000

241,000

241,000

Entertainment expense ….

90,000

90,000

90,000

Total fixed costs…………….

$1,356,000

1,356,000

1,356,000

Income from operations ……..

$ 58,000

$ 260,000

Problem 21-1A (Continued)

Part 3

Operating income increase for a 15,000 to 18,000 unit sales increase

Possible sales (units) ………………………………………………………

18,000

Units

Contribution margin per unit ……………………………………………

x $101

Total contribution margin …………………………………………..……

$1,818,000

Less: Fixed costs ……………………………………………………....

(1,356,000)

Potential operating income ………………………………………..……

$ 462,000

vs. Budgeted income for 2015 …………………………………………

159,000

Increase …………………………………………………………………….……

$ 303,000*

*Alternate solution format

Unit increase ……………………………………………………….…………….………..

3,000

Units

Contribution margin per unit ……………………………………………….………

x $101

Increase in contribution margin …………………………..………………………..

$303,000

Since there is no increase in fixed costs, the expected increase in operating

income is the same $303,000.

Part 4

Operating income (loss) at 12,000 units

Possible sales (units) ………………………………………………………

12,000

Units

Contribution margin per unit ……………………………………………

x $101

Total contribution margin …………………………………………..……

$1,212,000

Less: Fixed costs ……………………………………………………....

(1,356,000)

Potential operating loss ……………………………………………..……

$ (144,000)

Problem 21-2A (45 minutes)

Part 1

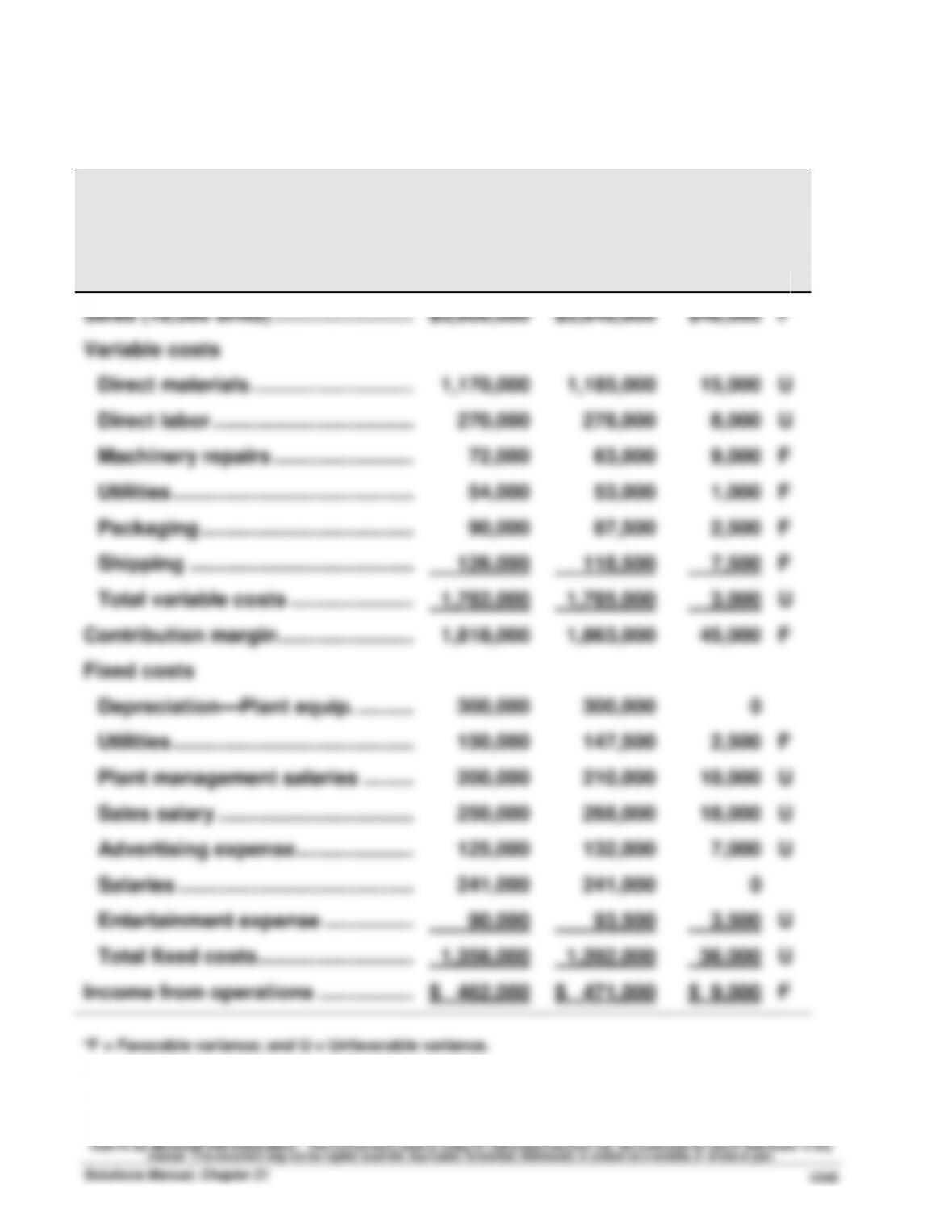

PHOENIX COMPANY

Flexible Budget Performance Report

For Year Ended December 31, 2015

Flexible

Actual

Budget

Results

Variances*

Sales (18,000 units) ……………………..

$3,600,000

$3,648,000

$48,000

F

Variable costs

Direct materials ………………………...

1,170,000

1,185,000

15,000

U

Direct labor ……………………………….

270,000

278,000

8,000

U

Machinery repairs ……………………..

72,000

63,000

9,000

F

Utilities ……………………………………..

54,000

53,000

1,000

F

Packaging ………………………………...

90,000

87,500

2,500

F

Shipping …………………………………..

126,000

118,500

7,500

F

Total variable costs …………………..

1,782,000

1,785,000

3,000

U

Contribution margin …………………….

1,818,000

1,863,000

45,000

F

Fixed costs

Depreciation—Plant equip. ………..

300,000

300,000

0

Utilities ……………………………………..

150,000

147,500

2,500

F

Plant management salaries ……….

200,000

210,000

10,000

U

Sales salary ……………………………...

250,000

268,000

18,000

U

Advertising expense ………………….

125,000

132,000

7,000

U

Salaries …………………………………….

241,000

241,000

0

Entertainment expense ……………..

90,000

93,500

3,500

U

Total fixed costs………………………..

1,356,000

1,392,000

36,000

U

Income from operations ……………...

$ 462,000

$ 471,000

$ 9,000

F

*F = Favorable variance; and U = Unfavorable variance.

Problem 21-2A (Continued)

Part 2

(a) Analysis of sales variance

Total

Per unit

Budgeted sales ……………………………………………………..

$3,600,000

$200.00

Actual sales …………………………..……………………….….

3,648,000

202.67*

Sales variance (favorable)……………………………….……..

$ 48,000

$ 2.67

* (rounded)

Interpretation: The sales variance is favorable because the actual price was

higher than planned.

(b) Analysis of direct materials variance

Total

Per unit

Budgeted materials………………………………………………..

$1,170,000

$ 65.00

Actual materials used ……………………………………..……..

1,185,000

65.83

Direct materials variance (unfavorable) …………..……..

$ 15,000

$ 0.83

Interpretation: The direct materials variance is unfavorable for two

possible reasons. (1) The quantity of materials used may have been more

than the quantity budgeted, and/or (2) the amount paid for the materials

might have been more than the budgeted purchase price.

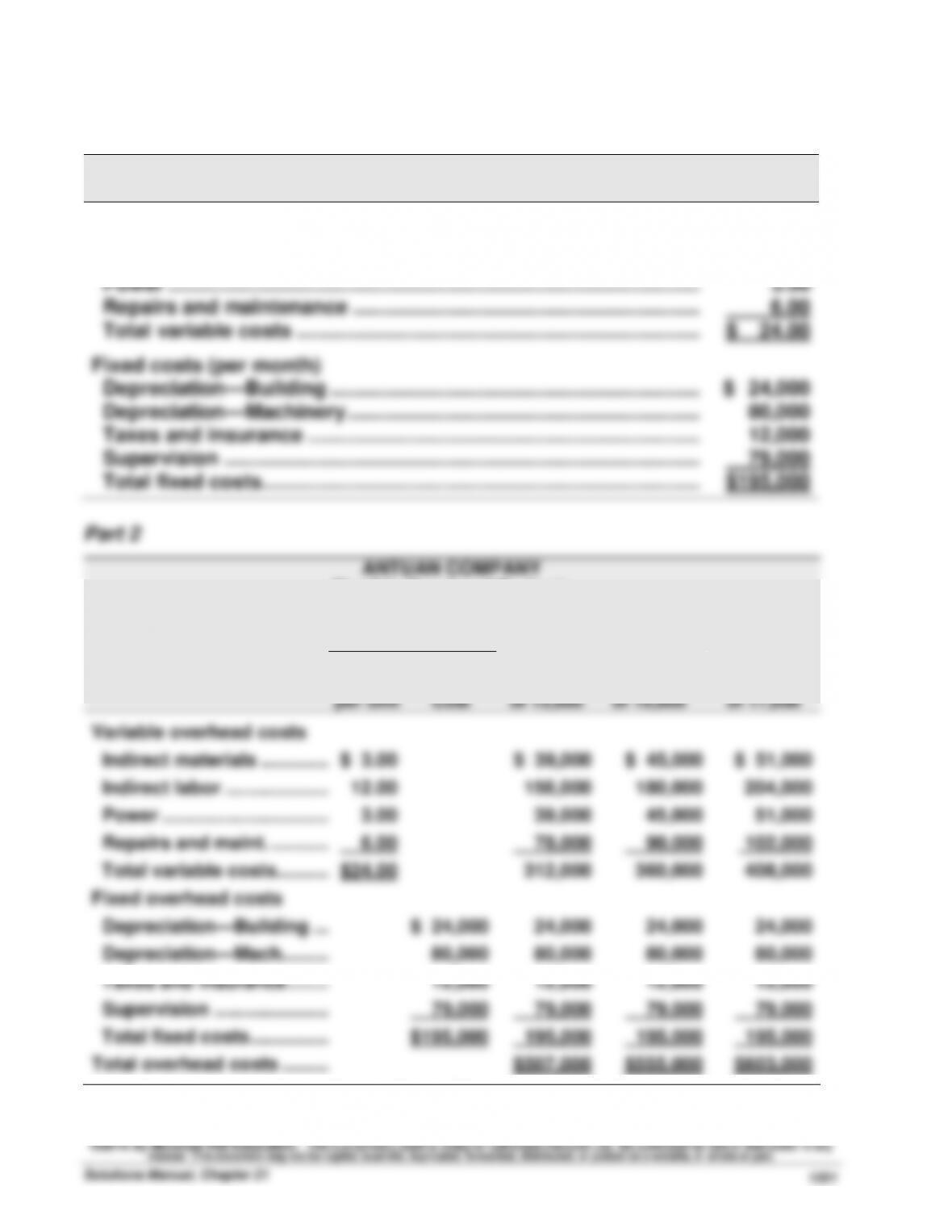

Problem 21-3A (60 minutes)

Part 1

Variable or Fixed Classification

Amount

Variable costs (total divided by 15,000 units)

Indirect materials …………………………..……………………………………...

$ 3.00

Indirect labor …………………………..…………………………………………….

12.00

Power ……………………………………………………….…………………………..

3.00

Repairs and maintenance ……………………………………………………...

6.00

Total variable costs ……………………………………………………………….

$ 24.00

Fixed costs (per month)

Depreciation—Building ………………………………………………………....

$ 24,000

Depreciation—Machinery ……………………………………………………….

80,000

Taxes and insurance ……………………………………………………………..

12,000

Supervision …………………………………………………………………………..

79,000

Total fixed costs …………………………………………………………………….

$195,000

Part 2

ANTUAN COMPANY

Flexible Overhead Budgets

For Month Ended October 31

Flexible Budget

Flexible

Flexible

Flexible

Variable

Amount

per Unit

Total

Fixed

Cost

Budget for

Unit Sales

of 13,000

Budget for

Unit Sales

of 15,000

Budget for

Unit Sales

of 17,000

Variable overhead costs

Indirect materials …………...

$ 3.00

$ 39,000

$ 45,000

$ 51,000

Indirect labor ………………....

12.00

156,000

180,000

204,000

Power …………………………..

3.00

39,000

45,000

51,000

Repairs and maint. ………....

6.00

78,000

90,000

102,000

Total variable costs………...

$24.00

312,000

360,000

408,000

Fixed overhead costs

Depreciation—Building …..

$ 24,000

24,000

24,000

24,000

Depreciation—Mach. ……....

80,000

80,000

80,000

80,000

Taxes and insurance ……....

12,000

12,000

12,000

12,000

Supervision …………………...

79,000

79,000

79,000

79,000

Total fixed costs ……………..

$195,000

195,000

195,000

195,000

Total overhead costs ………..

$507,000

$555,000

$603,000

Problem 21-3A (Continued)

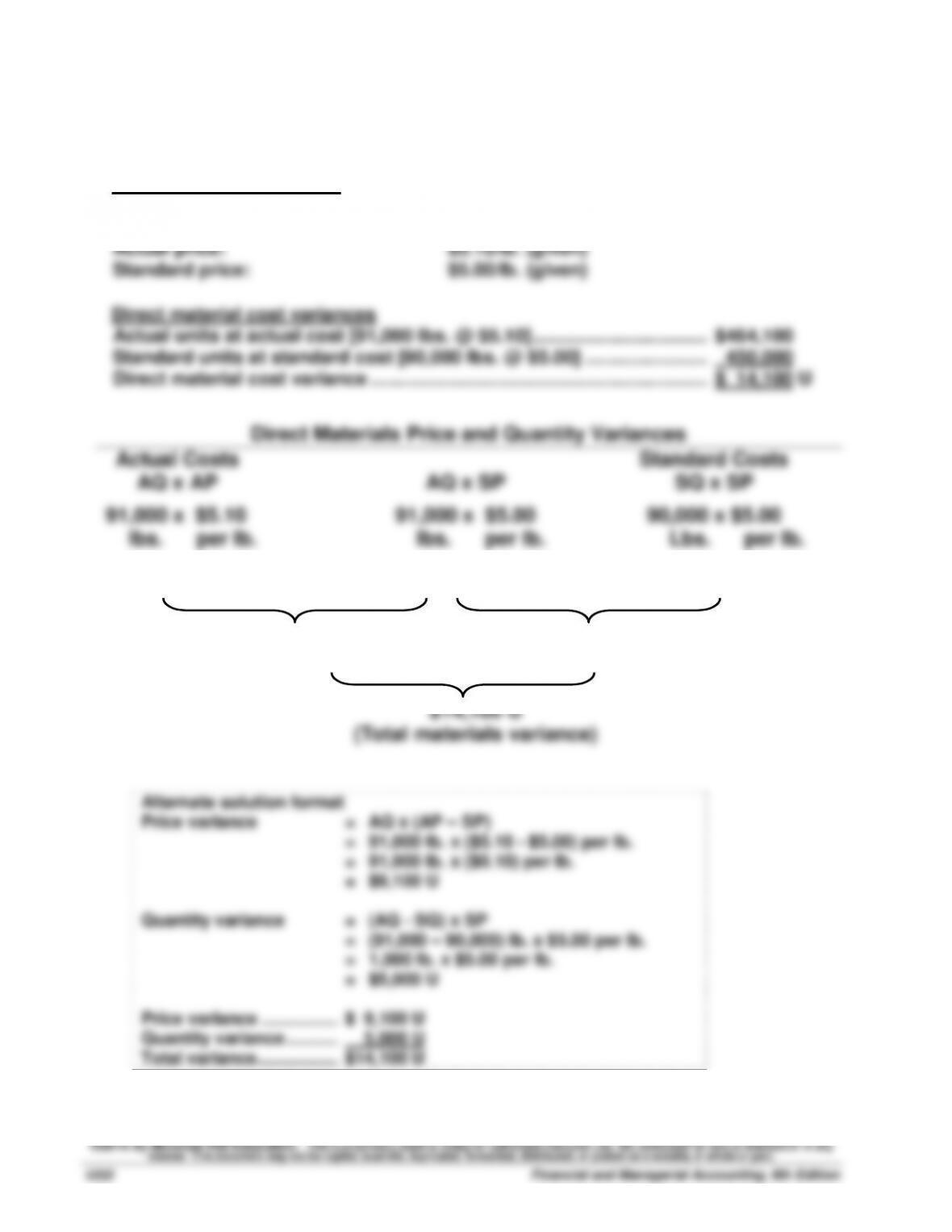

Part 3 Direct Materials Variances

Preliminary computations

Actual material used:

91,000 lbs. (given)

Standard quantity of materials:

15,000 units x 6 lb./unit = 90,000 lb.

Actual price:

$5.10/lb. (given)

Standard price:

$5.00/lb. (given)

Actual units at actual cost [91,000 lbs. @ $5.10] …………………………….…

$464,100

Standard units at standard cost [90,000 lbs. @ $5.00] ………………………

450,000

Direct material cost variance ………………………………………………………..…

$ 14,100 U

Direct Materials Price and Quantity Variances

Actual Costs

AQ x AP

AQ x SP

Standard Costs

SQ x SP

91,000 x $5.10

91,000 x $5.00

90,000 x $5.00

lbs. per lb.

lbs. per lb.

Lbs. per lb.

$464,100

$455,000

$450,000

$9,100 U

(Price variance)

$5,000 U

(Quantity variance)

$14,100 U

(Total materials variance)

Alternate solution format

Price variance

=

AQ x (AP – SP)

=

91,000 lb. x ($5.10 – $5.00) per lb.

=

91,000 lb. x ($0.10) per lb.

=

$9,100 U

Quantity variance

=

(AQ – SQ) x SP

=

(91,000 – 90,000) lb. x $5.00 per lb.

=

1,000 lb. x $5.00 per lb.

=

$5,000 U

Price variance …………….…..

$ 9,100 U

Quantity variance ………..…..

5,000 U

Total variance ……………..…..

$14,100 U