Exercise 21-15 (25 minutes)

Part 1

Direct materials price variance:

Actual cost of direct materials used (16,000 x $4.05) ……………….…………

$ 64,800

Actual quantity used x Standard price (16,000 x $4.00) ………………………

64,000

Direct materials price variance (unfavorable) …………………………..

$ 800

Actual quantity used x Standard price (16,000 x $4.00) ………………………

$ 64,000

Standard quantity x Standard price (15,000* x $4.00) ……………….…………

60,000

Direct materials quantity variance (unfavorable) ……………………..……

$ 4,000

*30,000 units x ½ pound per unit = 15,000 pounds

Part 2

Direct labor rate variance:

Actual hours x Actual rate per hour (5,545 x $19.00***) ………………………

$105,355

Actual hours x Standard rate per hour (5,545 x $20.00) ………………………

110,900

Direct labor rate variance (favorable) …………………………………………………

$ 5,545

Direct labor efficiency variance:

Actual hours x Standard rate per hour (5,545 x $20.00) ………………………

$110,900

Standard hours x Standard rate per hour (5,000** x $20.00) ……..…………

100,000

Direct labor efficiency variance (unfavorable) …………………………..

$ 10,900

**30,000 units x 1/6 hour per unit = 5,000 hours

***$105,355/5,545 hours

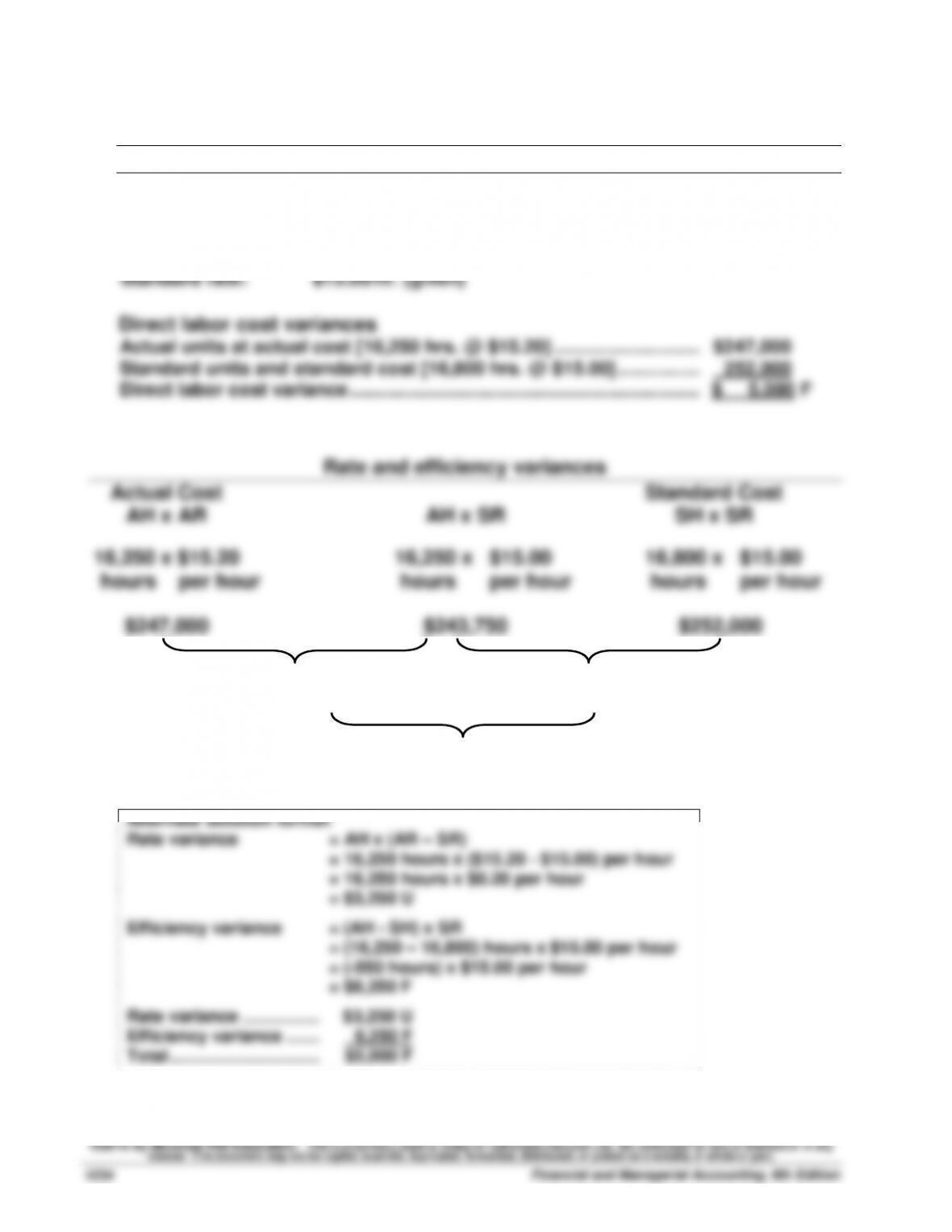

Exercise 21–16 (30 minutes)

1.

October variances

Preliminary computations

Actual hours: 16,250 hours (given)

Standard hours: 5,600 units x 3 hrs./unit = 16,800 hrs.

Actual rate: $247,000/16,250 hours = $15.20/hr.

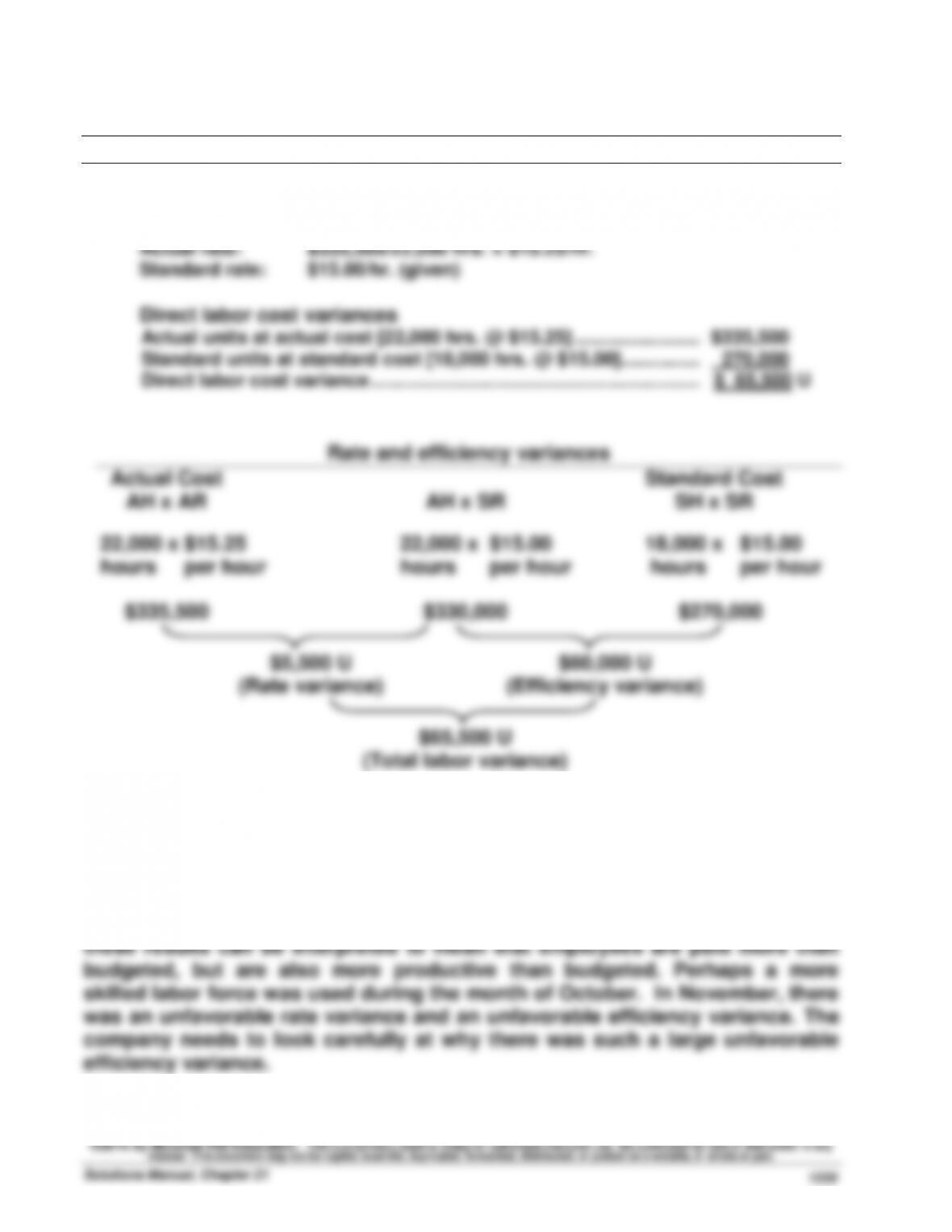

Exercise 21–16 (Concluded)

November variances

Preliminary computations

Actual hours: 22,000 hours (given)

Standard hours: 6,000 units x 3 hrs./unit = 18,000 hours

Exercise 21–17 (20 minutes)

1. Predetermined overhead rate computations

Expected volume …………………………………………………………….

75%

Expected total overhead………………………………………………….

$2,100,000

Expected hours ……………………………………………………………...

375,000 hrs.

Variable cost per hour ($1,500,000/ 375,000) …………………….

$4.00

Fixed cost per hour ($600,000/ 375,000) …………………………..

$1.60

Total cost per hour ($2,100,000/ 375,000) ………………………...

$5.60

2. Variable overhead cost variance

Variable overhead cost incurred [given] …………………………..

$1,375,000

Variable overhead cost applied [350,000 hrs. @ $4.00] ………………………

1,400,000

Variable overhead cost variance …………………………………….…………………

$ 25,000 F

Fixed overhead cost variance

Fixed overhead cost incurred [given] ……………………………..………..

$ 628,600

Fixed overhead cost applied [350,000 hrs. @ $1.60] ………..………..

560,000

Fixed overhead cost variance ………………………………………..………..

$ 68,600 U

Exercise 21–18A (20 minutes)

1.

Variable overhead spending and efficiency variances

Actual Overhead

AH x AVR

AH x SVR

Applied Overhead

SH x SVR

(Given)

340,000 x $4.00

350,000 x $4.00

hours per hour

hours per hour

$1,375,000

$1,360,000

$1,400,000

Exercise 21–18A (continued)

2.

Fixed overhead spending and volume variances

Actual Overhead

Budgeted Overhead

Applied Overhead

(Given)

(Given)

350,000 x $1.60

hours per hour

$628,600

$600,000

$560,000

$28,600 U

(Spending variance)

$40,000 U

(Volume variance)

$68,600 U

(Total fixed overhead variance)

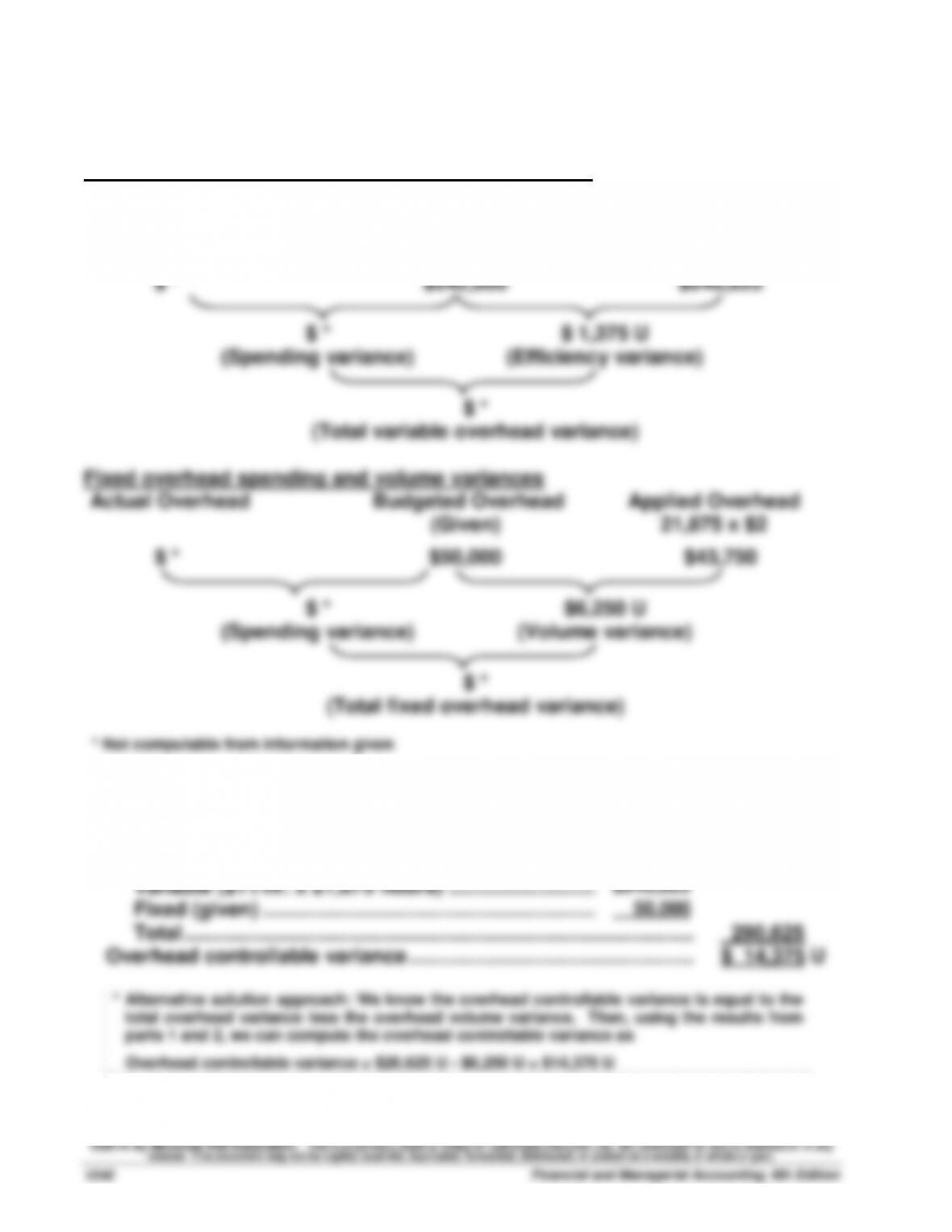

Interpretation

The $28,600 unfavorable spending variance means actual cost of fixed

overhead is more than budgeted.

The $40,000 unfavorable volume variance is the result of the company actually

operating at 70% capacity rather than the budgeted 75% capacity. Not all of

the budgeted fixed overhead is applied to production because actual volume

fell below budgeted volume.

3. The controllable variance is computed as:

Variable overhead spending variance ……………………………..

$15,000 U

Variable overhead efficiency variance ……………………………..

40,000 F

Fixed overhead spending variance …………………………..……..

28,600 U

Controllable variance……………………………………………………...

$ 3,600 U

The controllable variance refers to activities that are considered within

management’s control. The unfavorable controllable variance of $3,600

indicates that overall, management performed relatively poorly in controlling

overhead costs.

Exercise 21-19 (20 minutes)

Information given

1. Total overhead planned at 80% level (25,000 direct labor hours)

Predetermined

Cost

Cost per

Hour

Fixed overhead …………………………...

$ 50,000

$ 2.00

Variable overhead ……………………….

275,000

11.00

Total overhead …………………………...

$325,000

$13.00

2. Total overhead variance

Total actual overhead (given) …………………………..………………….……….

$305,000

Applied overhead ($13/hr. x 21,875 hours)…………………………………………

284,375

Total overhead variance ……………………………………………………….

$ 20,625 U

Exercise 21–20 (30 minutes)

1. Preliminary variance computations

Variable overhead spending and efficiency variances

Actual Overhead

AH x AVR

AH x SVR

Applied Overhead

SH x SVR

22,000 x $11

21,875 x $11

$ *

$242,000

$240,625

$ *

(Spending variance)

$ 1,375 U

(Efficiency variance)

$ *

(Total variable overhead variance)

Fixed overhead spending and volume variances

Actual Overhead

Budgeted Overhead

Applied Overhead

(Given)

21,875 x $2

$ *

$50,000

$43,750

$ *

(Spending variance)

$6,250 U

(Volume variance)

$ *

(Total fixed overhead variance)

* Not computable from information given

2. Overhead controllable variance*

Total actual overhead (given)

$305,000

Flexible budget overhead

Variable ($11/hr. x 21,875 hours) …………………………

$240,625

Fixed (given) ………………………………………………………

50,000

Total ……………………………………………………………………………….…..

290,625

Overhead controllable variance ……………………………………………………….

$ 14,375 U

* Alternative solution approach: We know the overhead controllable variance is equal to the

total overhead variance less the overhead volume variance. Then, using the results from

parts 1 and 2, we can compute the overhead controllable variance as

Overhead controllable variance = $20,625 U – $6,250 U = $14,375 U

EX

Exercise 21-21 (25 minutes)

Preliminary calculations:

Variable overhead rate per DL hour = $48,000/24,000 = $2 per hour

Fixed overhead rate per DL hour = $44,400/24,000 = $1.85 per hour

Exercise 21–21 (continued)

Part 3

JAMES CORP.

Overhead Variance Report

For Month Ended May 31

Volume Variance

Expected production level …………………………………………….

80% of capacity

Production level achieved …………………………………………….

90% of capacity

Volume variance …………………………………………………….…

$5,550 (favorable)

Flexible

Actual

Controllable Variance

Budget

Results

Variances*

Variable overhead costs

Indirect materials …………………………..

$16,875

$15,000

$1,875

F

Indirect labor …………………………….……….

27,000

26,500

500

F

Power ……………………………………….……….

6,750

6,750

0

Maintenance ……………………………..……….

3,375

4,000

625

U

Total variable costs …………………..………

54,000

52,250

1,750

F

Fixed overhead costs

Rent of factory building …………….……….

15,000

15,000

0

Depreciation—Machinery …………..……….

10,000

10,000

0

Supervisory salaries ………………….……….

19,400

22,000

2,600

U

Total fixed costs………………………..…

44,400

47,000

2,600

U

Total overhead costs …………………..………

$98,400

$99,250

$ 850

U

* F = Favorable variance; and U = Unfavorable variance.