Problem 20-7A (Continued)

Part 4

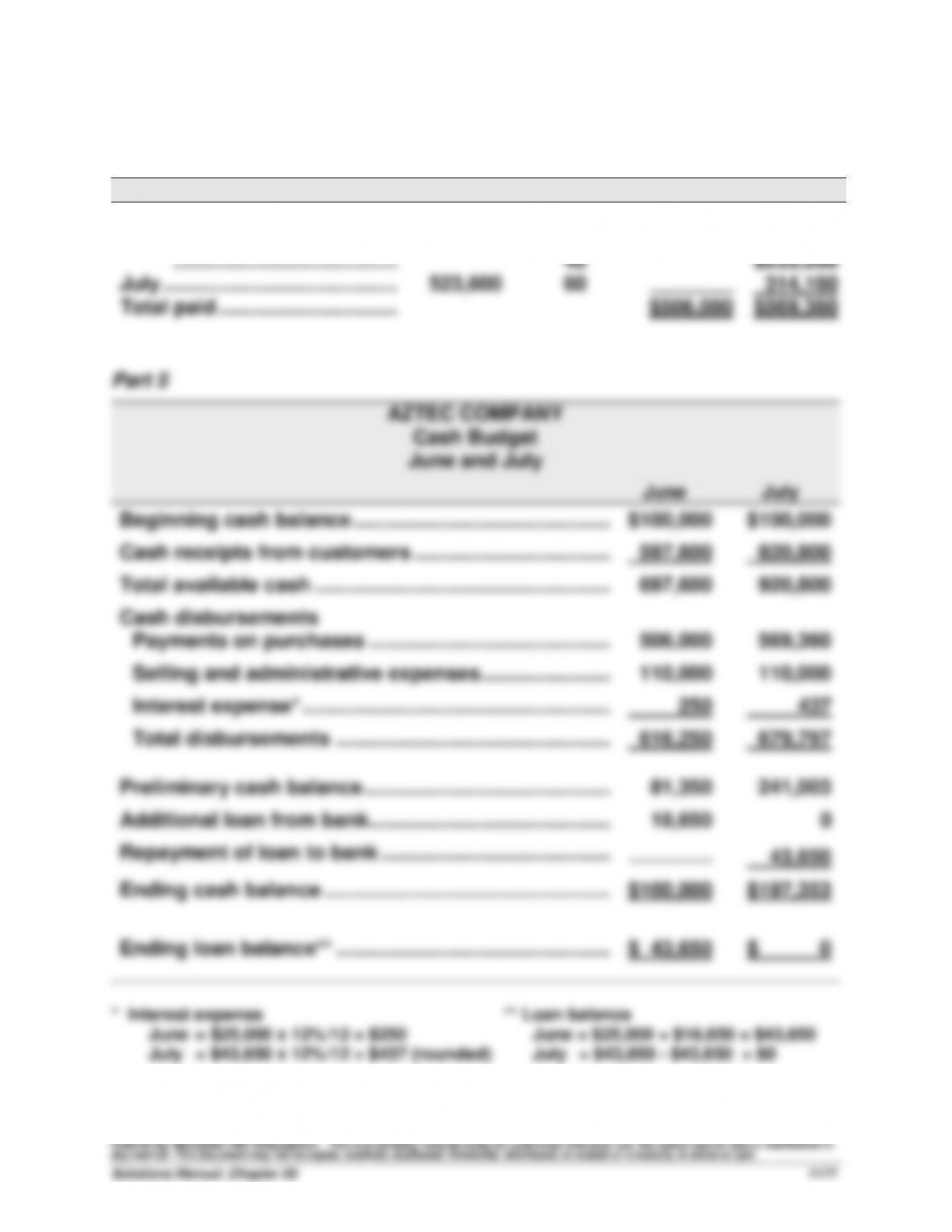

Cash payments on product purchases (for June and July)

From purchases in

Total

% Paid

June

July

May …………………………………….…..

$308,000

40%

$123,200

June ………………………………………..

638,000

60

382,800

…………………………………..…..

40

$255,200

July …………………………………….…..

523,600

60

________

314,160

Total paid ………………………………..

$506,000

$569,360

Part 5

AZTEC COMPANY

Cash Budget

June and July

June

July

Beginning cash balance ………………………………………...

$100,000

$100,000

Cash receipts from customers …………………………..…..

597,600

820,800

Total available cash ……………………………………………....

697,600

920,800

Cash disbursements

Payments on purchases ……………………………………...

506,000

569,360

Selling and administrative expenses …………………....

110,000

110,000

Interest expense* ………………………………………………...

250

437

Total disbursements …………………………………………...

616,250

679,797

Preliminary cash balance ……………………………………....

81,350

241,003

Additional loan from bank……………………………………...

18,650

0

Repayment of loan to bank …………………………………....

________

43,650

Ending cash balance ……………………………………………..

$100,000

$197,353

Ending loan balance** …………………………………………...

$ 43,650

$ 0

* Interest expense ** Loan balance

June = $25,000 x 12%/12 = $250 June = $25,000 + $18,650 = $43,650

July = $43,650 x 12%/12 = $437 (rounded) July = $43,650 – $43,650 = $0

Problem 20-7A (Concluded)

Part 6

Information about the need for cash in the near future would be helpful to

the management of Aztec Company because they would be able to enter

into negotiations with potential lenders well ahead of any immediate need

Problem 20-8A (130 minutes)

Part 1

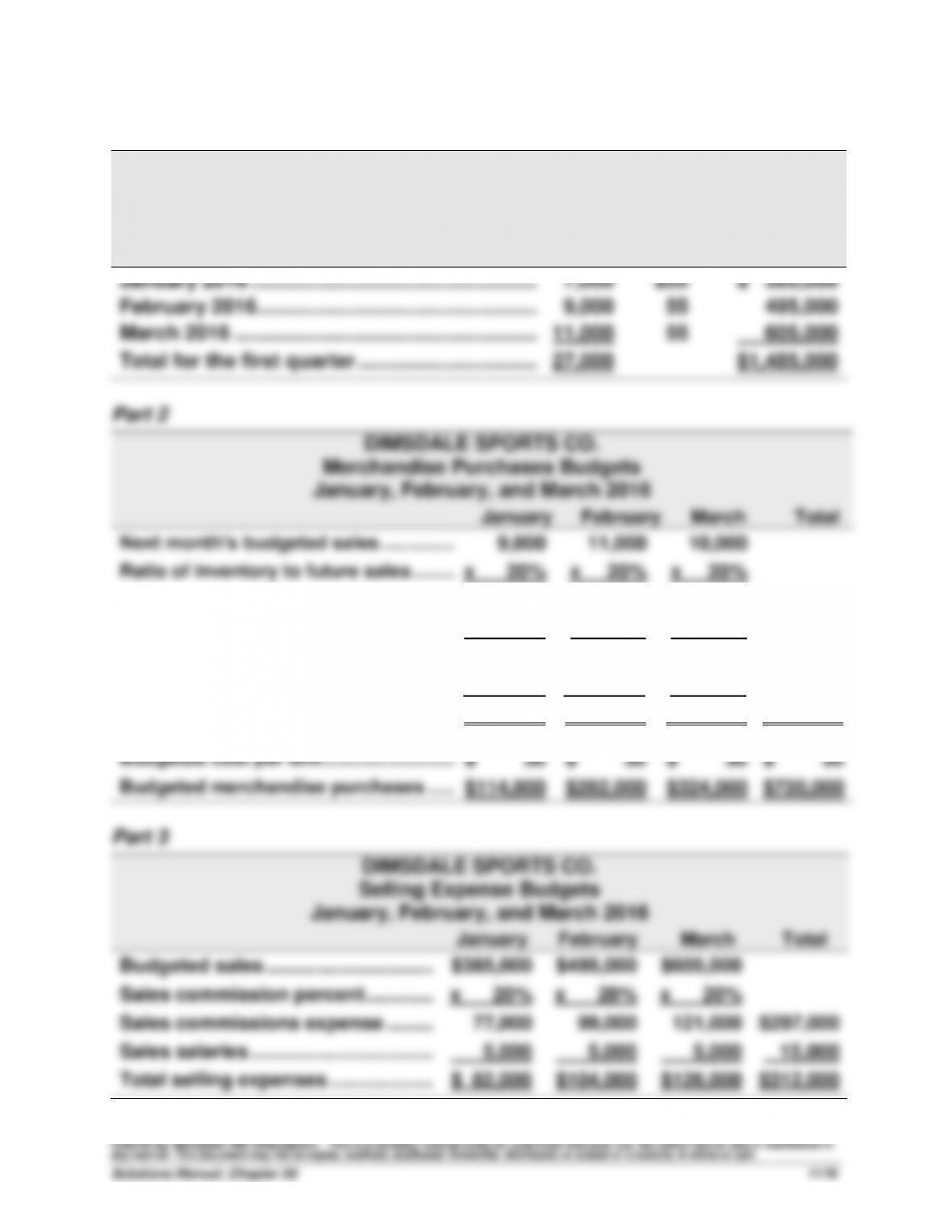

DIMSDALE SPORTS CO.

Sales Budgets

January, February, and March 2016

Budgeted

Units

Budgeted

Unit Price

Budgeted

Total Dollars

January 2016 …………………………………………….….

7,000

$55

$ 385,000

February 2016 ……………………………………………….

9,000

55

495,000

March 2016 ……………………………………………….….

11,000

55

605,000

Total for the first quarter ……………………………….

27,000

$1,485,000

Part 2

DIMSDALE SPORTS CO.

Merchandise Purchases Budgets

January, February, and March 2016

January

February

March

Total

Next month’s budgeted sales …………...

9,000

11,000

10,000

Ratio of inventory to future sales ……...

x 20%

x 20%

x 20%

Budgeted ending inventory ……………...

1,800

2,200

2,000

Add budgeted sales ………………………….

7,000

9,000

11,000

Required available merchandise ……….

8,800

11,200

13,000

Deduct beginning inventory ……………..

(5,000)

(1,800)

(2,200)

Units to be purchased ……………………...

3,800

9,400

10,800

24,000

Budgeted cost per unit ……………………..

$ 30

$ 30

$ 30

$ 30

Budgeted merchandise purchases …...

$114,000

$282,000

$324,000

$720,000

DIMSDALE SPORTS CO.

Selling Expense Budgets

January, February, and March 2016

January

February

March

Total

Budgeted sales …………………………..

$385,000

$495,000

$605,000

Sales commission percent ………….……

x 20%

x 20%

x 20%

Sales commissions expense ……………

77,000

99,000

121,000

$297,000

Sales salaries ……………………………..……

5,000

5,000

5,000

15,000

Total selling expenses ………………..……

$ 82,000

$104,000

$126,000

$312,000

Problem 20-8A (Continued)

Part 4

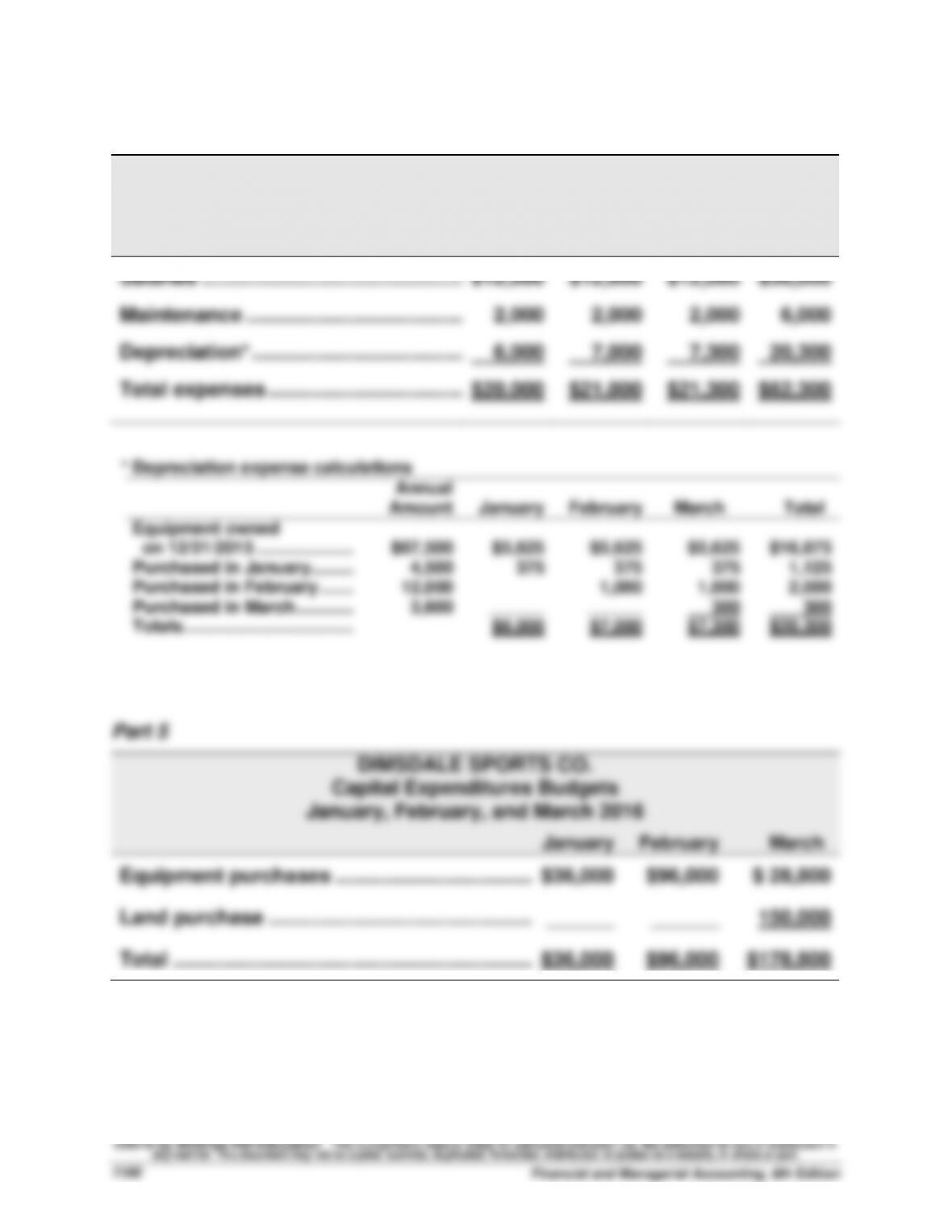

DIMSDALE SPORTS CO.

General and Administrative Expense Budgets

January, February, and March 2016

January

February

March

Total

Salaries …………………………..…………………..

$12,000

$12,000

$12,000

$36,000

Maintenance …………………………..…….……..

2,000

2,000

2,000

6,000

Depreciation* ………………………………..……..

6,000

7,000

7,300

20,300

Total expenses ……………………………..……..

$20,000

$21,000

$21,300

$62,300

* Depreciation expense calculations

Annual

Amount

January

February

March

Total

Equipment owned

on 12/31/2015 ………………..

$67,500

$5,625

$5,625

$5,625

$16,875

Purchased in January………

4,500

375

375

375

1,125

Purchased in February …….

12,000

1,000

1,000

2,000

Purchased in March …………

3,600

______

______

300

300

Totals ……………………………..

$6,000

$7,000

$7,300

$20,300

Part 5

DIMSDALE SPORTS CO.

Capital Expenditures Budgets

January, February, and March 2016

January

February

March

Equipment purchases ……………………………..……

$36,000

$96,000

$ 28,800

Land purchase ………………………………………..……

______

______

150,000

Total ……………………………………………………….

$36,000

$96,000

$178,800

Problem 20-8A (Continued)

Part 6

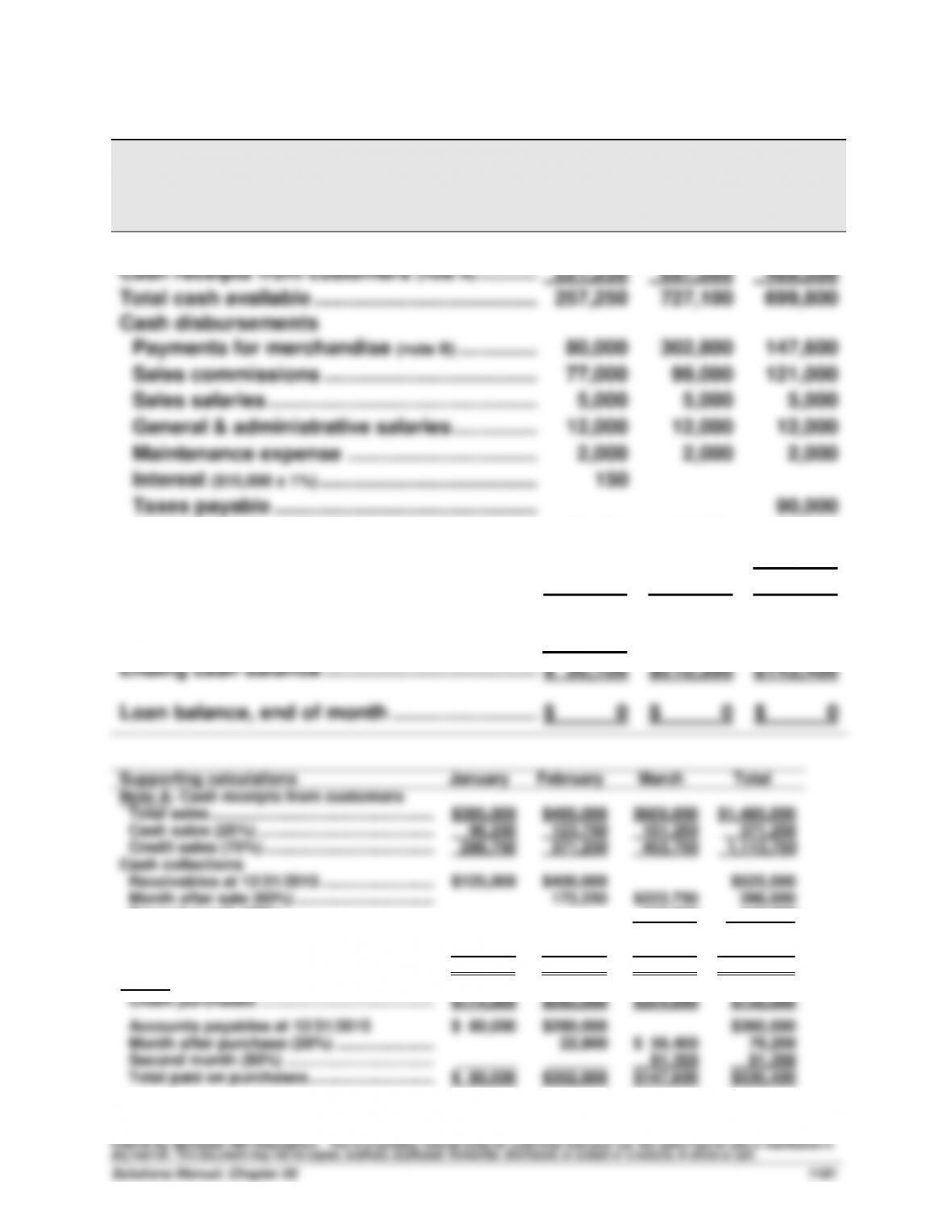

DIMSDALE SPORTS CO.

Cash Budgets

January, February, and March 2016

January

February

March

Beginning cash balance …………………………….….

$ 36,000

$ 30,100

$210,300

Cash receipts from customers (note A) …………….

221,250

697,000

489,500

Total cash available …………………………………..….

257,250

727,100

699,800

Cash disbursements

Payments for merchandise (note B) ……………….

80,000

302,800

147,600

Sales commissions …………………………………….

77,000

99,000

121,000

Sales salaries …………………………..……………..….

5,000

5,000

5,000

General & administrative salaries …………….….

12,000

12,000

12,000

Maintenance expense ……………………………..….

2,000

2,000

2,000

Interest ($15,000 x 1%) …………………………..……..….

150

Taxes payable …………………………………………….

90,000

Purchases of equipment …………………………..

36,000

96,000

28,800

Purchase of land ……………………………………..….

________

________

150,000

Total cash disbursements…………………………..

212,150

516,800

556,400

Preliminary cash balance …………………………..

45,100

210,300

143,400

Repayment of loan to bank ………………………..…

(15,000)

_______

________

Ending cash balance …………………………………….

$ 30,100

$210,300

$143,400

Loan balance, end of month ………………………….

$ 0

$ 0

$ 0

Supporting calculations

January

February

March

Total

Note A: Cash receipts from customers

Total sales …………………………………………..….

$385,000

$495,000

$605,000

$1,485,000

Cash sales (25%) …………………………………….

96,250

123,750

151,250

371,250

Credit sales (75%) ………………………………..….

288,750

371,250

453,750

1,113,750

Cash collections

Receivables at 12/31/2015 …………………….….

$125,000

$400,000

$525,000

Month after sale (60%) …………………………..

173,250

$222,750

396,000

Second month (40%) ……………………………….

_______

_______

115,500

115,500

Total from credit customers ………………….….

125,000

573,250

338,250

1,036,500

Cash sales …………………………………………..….

96,250

123,750

151,250

371,250

Total cash received ……………………………..…..

$221,250

$697,000

$489,500

$1,407,750

Note B: Cash payments for merchandise

Credit purchases …………………………………….

$114,000

$282,000

$324,000

$720,000

Accounts payables at 12/31/2015

$ 80,000

$280,000

$360,000

Month after purchase (20%) ………………….….

22,800

$ 56,400

79,200

Second month (80%) ……………………………….

_______

_______

91,200

91,200

Total paid on purchases ……………………….….

$ 80,000

$302,800

$147,600

$530,400

Problem 20-8A (Continued)

Part 7

DIMSDALE SPORTS CO.

Budgeted Income Statement

For Three Months Ended March 31, 2016

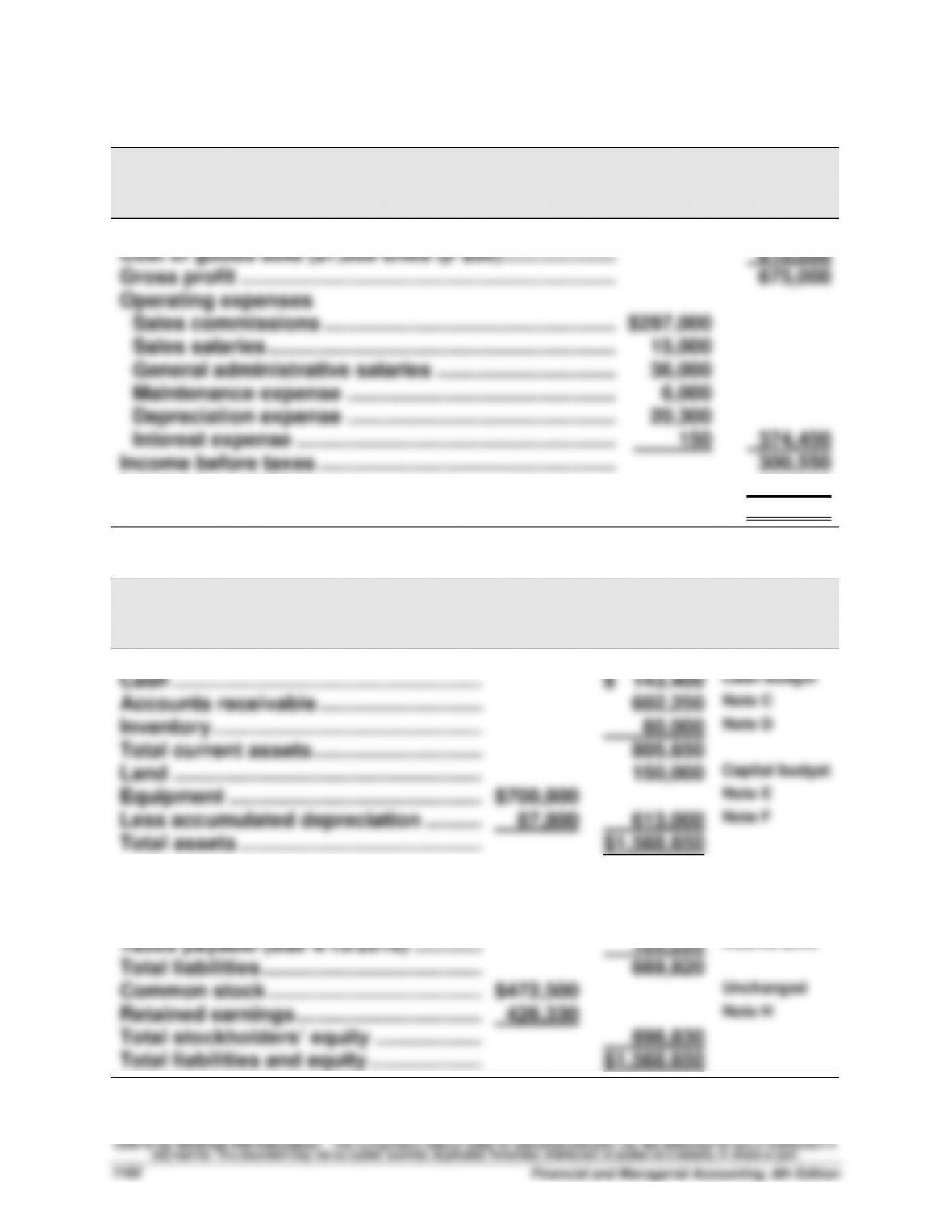

Sales ……………………………………………………………………..

$1,485,000

Cost of goods sold (27,000 units @ $30) ………………...

810,000

Gross profit …………………………………………………………..

675,000

Operating expenses

Sales commissions ……………………………………………..

$297,000

Sales salaries …………………………..………………………….

15,000

General administrative salaries …………………………..

36,000

Maintenance expense ………………………………………….

6,000

Depreciation expense ………………………………………….

20,300

Interest expense ………………………………………………….

150

374,450

Income before taxes ……………………………………………...

300,550

Income taxes (40%)………………………………………………..

120,220

Net income …………………………..………………………………..

$180,330

Part 8

DIMSDALE SPORTS CO.

Budgeted Balance Sheet

March 31, 2016

ASSETS

Cash ………………………………………………..….

$ 143,400

Cash budget

Accounts receivable …………………………..

602,250

Note C

Inventory ………………………………………….….

60,000

Note D

Total current assets …………………………..

805,650

Land ………………………………………………..….

150,000

Capital budget

Equipment …………………………..…………..….

$700,800

Note E

Less accumulated depreciation ………..….

87,800

613,000

Note F

Total assets ……………………………………..….

$1,568,650

LIABILITIES AND EQUITY

Accounts payable …………………………….….

$ 549,600

Note G

Bank loan payable ……………………………….

0

Cash budget

Taxes payable (due 4/15/2016) ………….….

120,220

Income stmt.

Total liabilities ………………………………….….

669,820

Common stock …………………………………….

$472,500

Unchanged

Retained earnings …………………………….….

426,330

Note H

Total stockholders’ equity ………………..….

898,830

Total liabilities and equity …………………….

$1,568,650

Problem 20-8A (Concluded)

Supporting Footnotes

Note C

Beginning receivables …………………………………………..….

$ 525,000

Credit sales …………………………..………………………………….

1,113,750

Less collections ……………………………………………………….

(1,036,500)

Ending receivables ………………………………………………..….

$ 602,250

Note D

Beginning inventory ………………………………………………….

$ 150,000

Purchases …………………………………………………………….….

720,000

Less cost of goods sold ………………………………………..….

(810,000)

Ending inventory* ………………………………………………….….

$ 60,000

*Also equals 2,000 units @ $30 = $60,000

Note E

Beginning equipment …………………………………………….….

$ 540,000

Purchased in January ……………………………………………….

36,000

Purchased in February…………………………………………..….

96,000

Purchased in March ………………………………………………….

28,800

Total …………………………………………………………………….….

$ 700,800

Note F

Beginning accumulated depreciation ……………………..….

$ 67,500

Depreciation expense ……………………………………………….

20,300

Total …………………………………………………………………….….

$ 87,800

Note G

Beginning accounts payable ………………………………….….

$ 360,000

Purchases …………………………………………………………….….

720,000

Payments …………………………..…………………………………….

(530,400)

Ending accounts payable ………………………………………….

$ 549,600

Note H

Beginning retained earnings ………………………………….….

$ 246,000

Net income ……………………………………………………………….

180,330

Total …………………………………………………………………….….

$ 426,330

Problem 20-1B (30 minutes)

Part 1

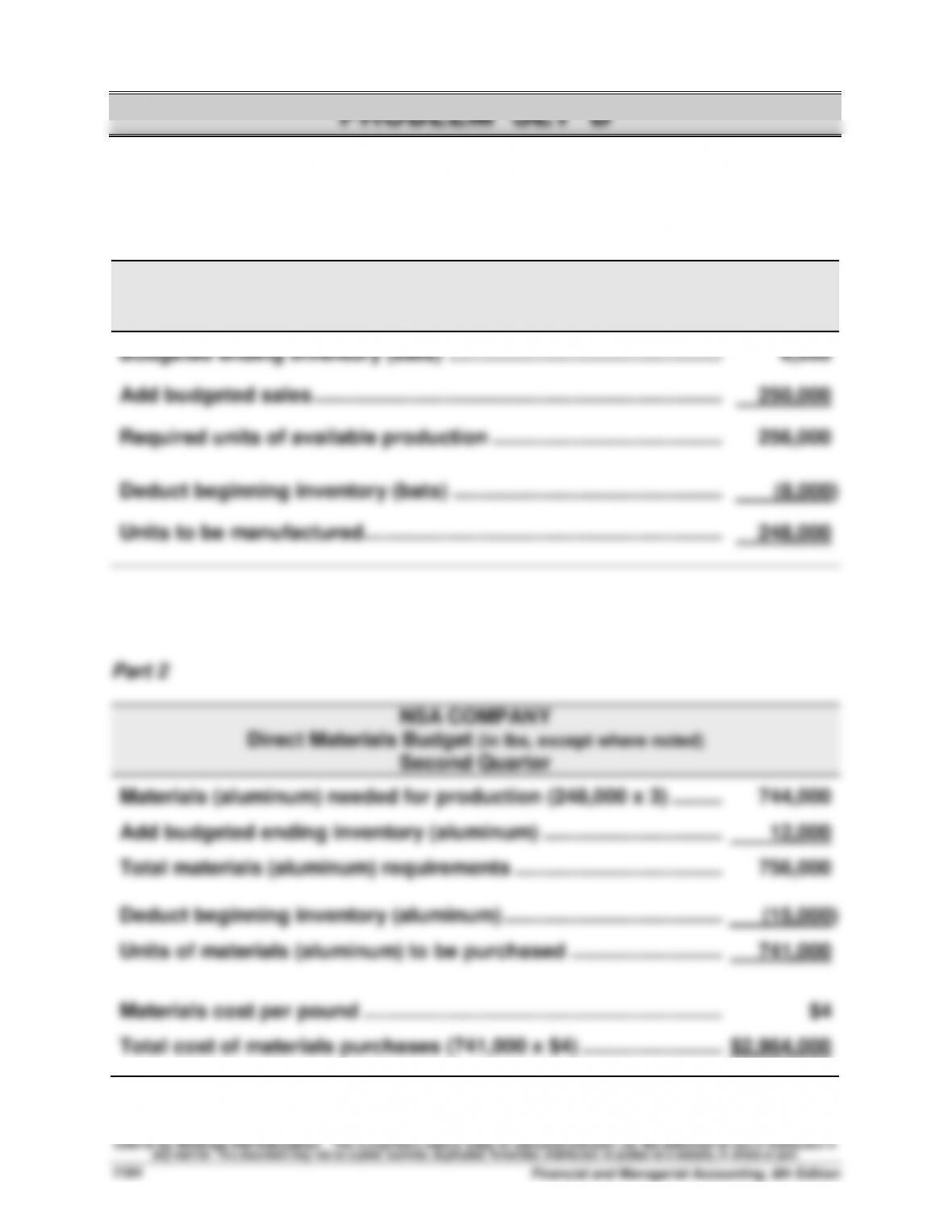

NSA COMPANY

Production Budget (in units)

Second Quarter

Budgeted ending inventory (bats) ………………………………………….…….

6,000

Add budgeted sales ……………………………………………………………….…….

250,000

Required units of available production …………………………………..…….

256,000

Deduct beginning inventory (bats) ……………………………………………….

(8,000)

Units to be manufactured……………………………………………………….

248,000

Part 2

NSA COMPANY

Direct Materials Budget (in lbs, except where noted)

Second Quarter

Materials (aluminum) needed for production (248,000 x 3) …………

744,000

Add budgeted ending inventory (aluminum) …………………………..

12,000

Total materials (aluminum) requirements ……………………………….…

756,000

Deduct beginning inventory (aluminum) ……………………………………

(15,000)

Units of materials (aluminum) to be purchased …………………………

741,000

Materials cost per pound ……………………………………………………….

$4

Total cost of materials purchases (741,000 x $4) …………………….…

$2,964,000

Problem 20-1B (concluded)

Part 3

NSA COMPANY

Direct Labor Budget

Second Quarter

Units to be produced ………………………………………………………

248,000

Labor requirements per unit (hours) …………………………..

x 0.50

Total labor hours needed …………………………………………..……

124,000

Labor rate (per hour) …………………………..…………………….……

x $18

Labor dollars …………………………………………………………….……

$2,232,000

Part 4

NSA COMPANY

Factory Overhead Budget

Second Quarter

Total labor hours needed …………………………………………..……

124,000

Variable overhead rate per direct labor hour ……………………

x $12

Budgeted variable overhead ……………………………………………

$1,488,000

Budgeted fixed overhead …………………………………………..……

1,776,000

Budgeted total overhead …………………………………………………

$3,264,000

Problem 20-2B (30 minutes)

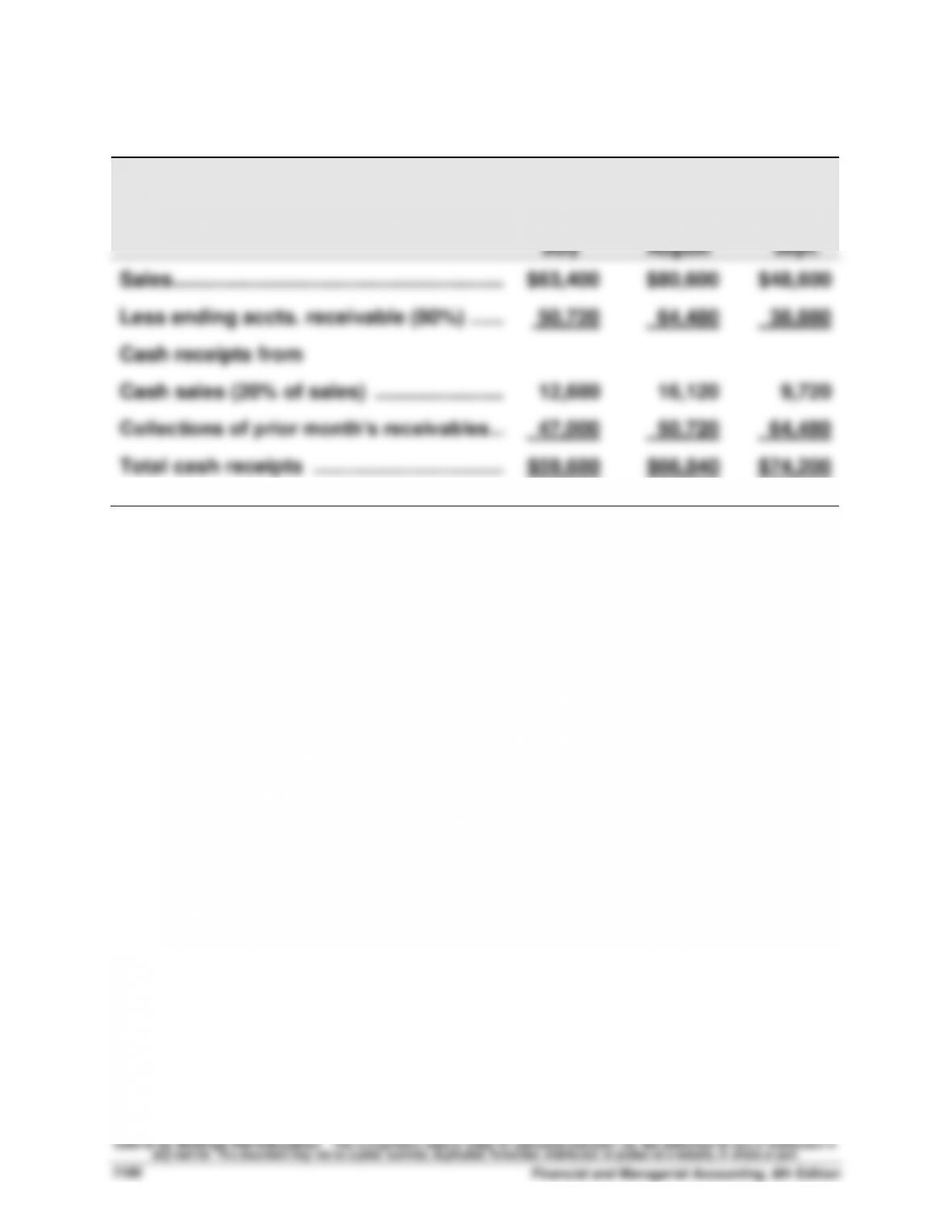

(1)

A1 MANUFACTURING

Cash Receipts Budget

For July, August, and September

July

August

Sept.

Sales …………………………………………………..…

$63,400

$80,600

$48,600

Less ending accts. receivable (80%) ………

50,720

64,480

38,880

Cash receipts from

Cash sales (20% of sales) …………………..…

12,680

16,120

9,720

Collections of prior month’s receivables ……

47,000

50,720

64,480

Total cash receipts …………………………….…

$59,680

$66,840

$74,200