Problem 20-4A (130 minutes)

Part 1

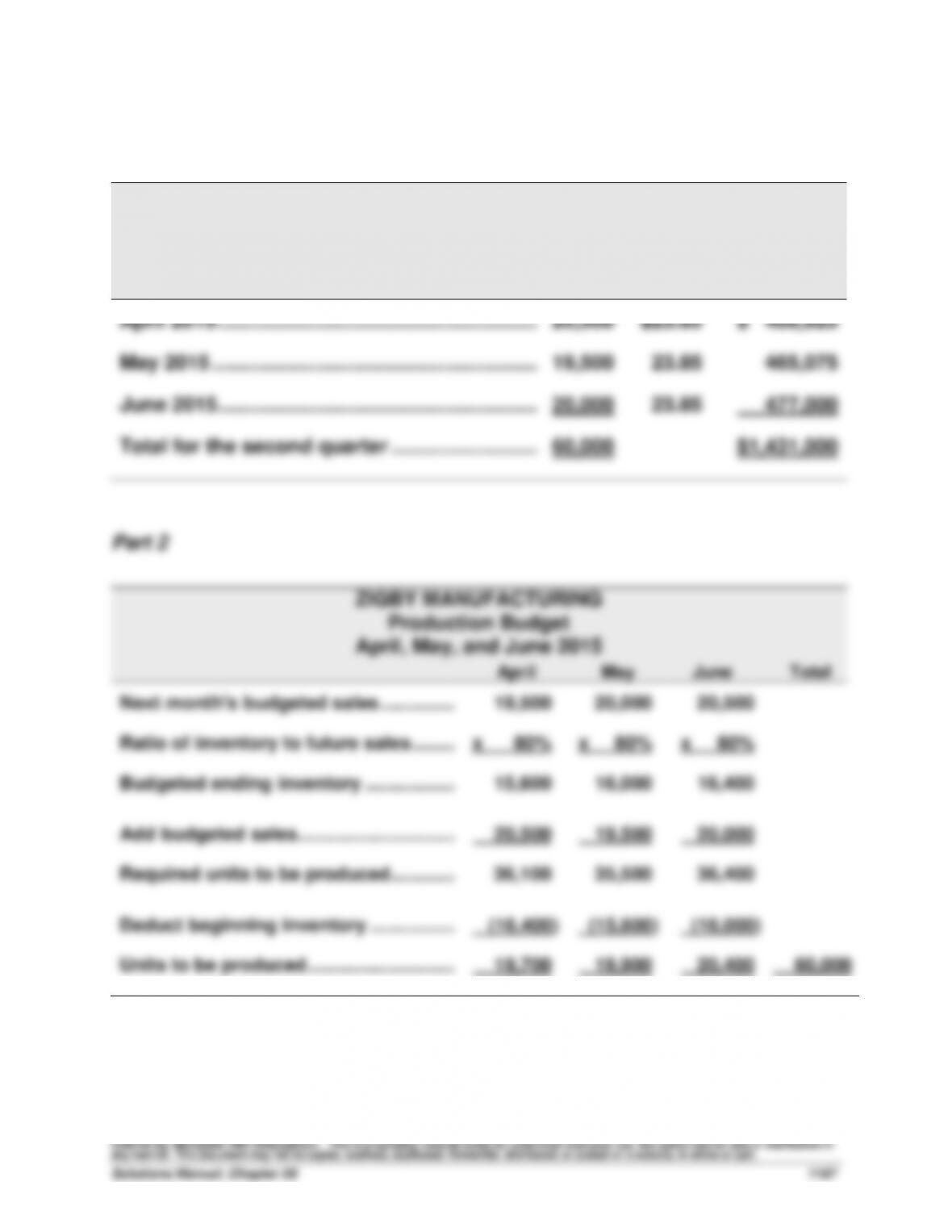

ZIGBY MANUFACTURING

Sales Budgets

April, May, and June 2015

Budgeted

Units

Budgeted

Unit Price

Budgeted

Total Dollars

April 2015 ………………………………………………….….

20,500

$23.85

$ 488,925

May 2015 …………………………………………………..….

19,500

23.85

465,075

June 2015 ………………………………………………….….

20,000

23.85

477,000

Total for the second quarter ………………………….

60,000

$1,431,000

Part 2

ZIGBY MANUFACTURING

Production Budget

April, May, and June 2015

April

May

June

Total

Next month’s budgeted sales …………...

19,500

20,000

20,500

Ratio of inventory to future sales ……...

x 80%

x 80%

x 80%

Budgeted ending inventory ……………...

15,600

16,000

16,400

Add budgeted sales ………………………….

20,500

19,500

20,000

Required units to be produced ………….

36,100

35,500

36,400

Deduct beginning inventory ……………..

(16,400)

(15,600)

(16,000)

Units to be produced ………………………..

19,700

19,900

20,400

60,000

Problem 20-4A (continued)

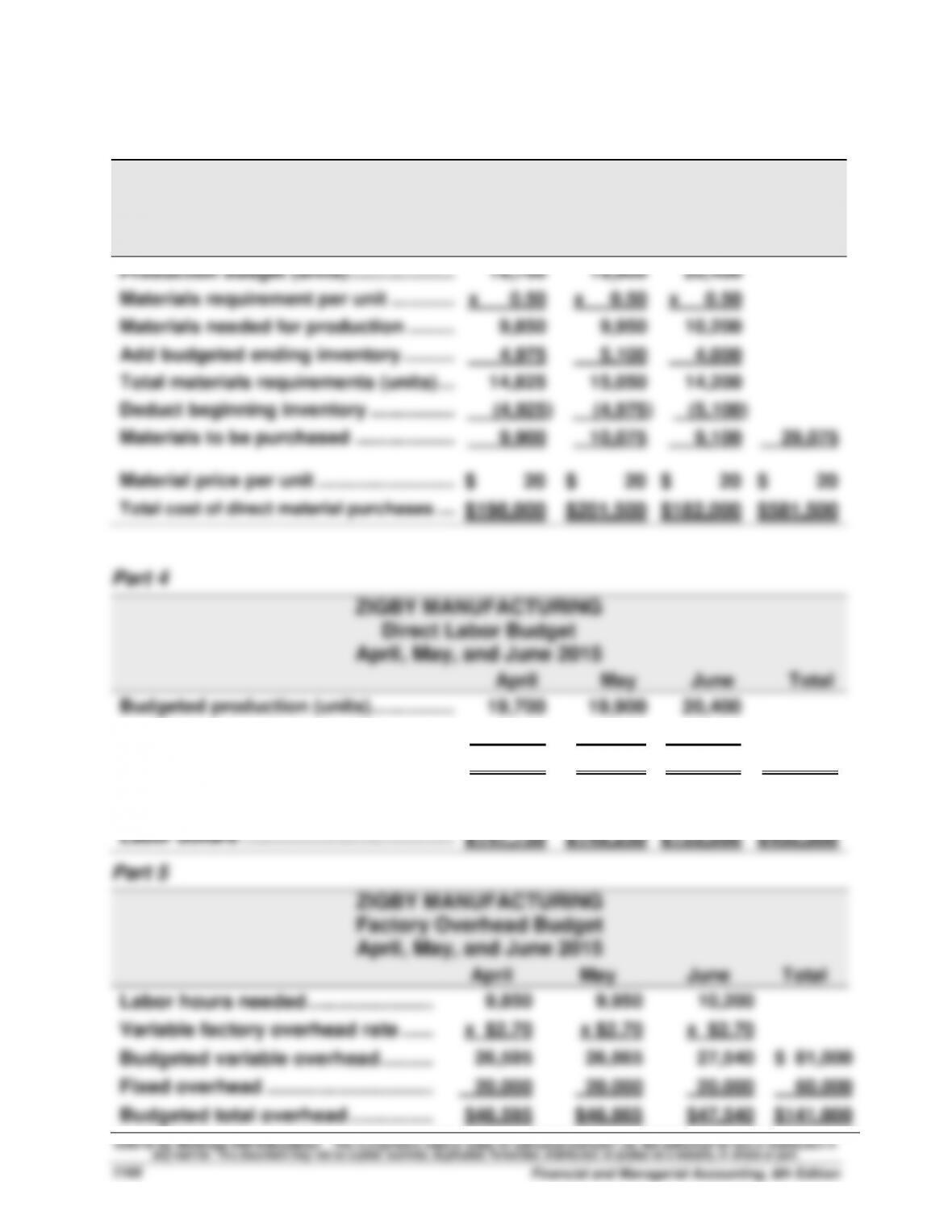

Part 3

ZIGBY MANUFACTURING

Raw Materials Budget

April, May, and June 2015

April

May

June

Total

Production budget (units) ………………...

19,700

19,900

20,400

Materials requirement per unit ………….

x 0.50

x 0.50

x 0.50

Materials needed for production ……….

9,850

9,950

10,200

Add budgeted ending inventory ………..

4,975

5,100

4,000

Total materials requirements (units) ….

14,825

15,050

14,200

Deduct beginning inventory ……………..

(4,925)

(4,975)

(5,100)

Materials to be purchased ………………..

9,900

10,075

9,100

29,075

Material price per unit ……………………...

$ 20

$ 20

$ 20

$ 20

Total cost of direct material purchases …..

$198,000

$201,500

$182,000

$581,500

April, May, and June 2015

April

May

June

Total

x 0.50

$ 15

$ 15

$ 15

$ 15

ZIGBY MANUFACTURING

Factory Overhead Budget

Labor hours needed …………………………

Variable factory overhead rate …………

Problem 20-4A (continued)

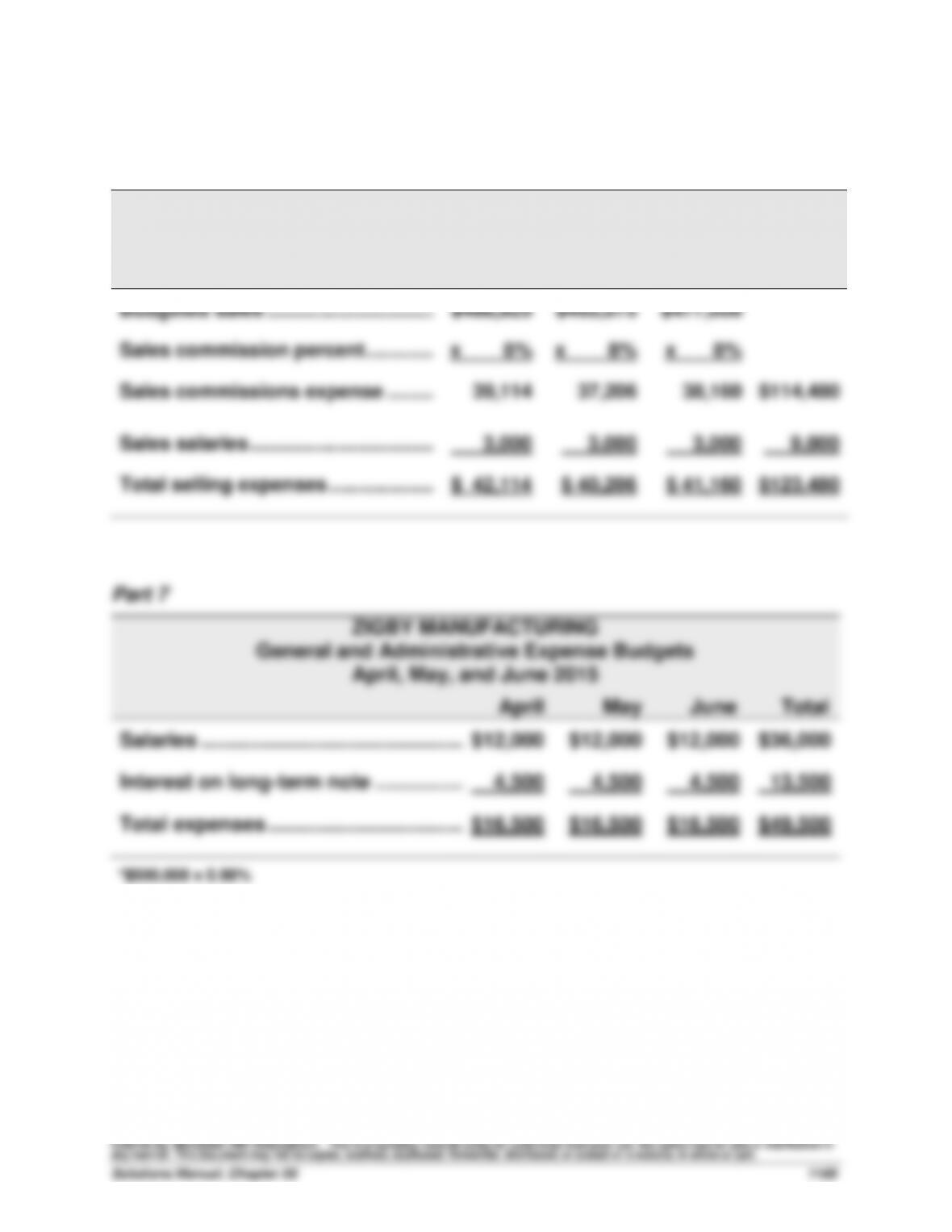

Part 6

ZIGBY MANUFACTURING

Selling Expense Budgets

April, May, and June 2015

April

May

June

Total

Budgeted sales …………………………..

$488,925

$465,075

$477,000

Sales commission percent ………….……

x 8%

x 8%

x 8%

Sales commissions expense ……………

39,114

37,206

38,160

$114,480

Sales salaries ……………………………..……

3,000

3,000

3,000

9,000

Total selling expenses ………………..……

$ 42,114

$ 40,206

$ 41,160

$123,480

Part 7

ZIGBY MANUFACTURING

General and Administrative Expense Budgets

April, May, and June 2015

April

May

June

Total

Salaries ………………………………………..……..

$12,000

$12,000

$12,000

$36,000

Interest on long-term note …………….……..

4,500

4,500

4,500

13,500

Total expenses ……………………………..……..

$16,500

$16,500

$16,500

$49,500

*$500,000 x 0.90%

Problem 20-4A (Continued)

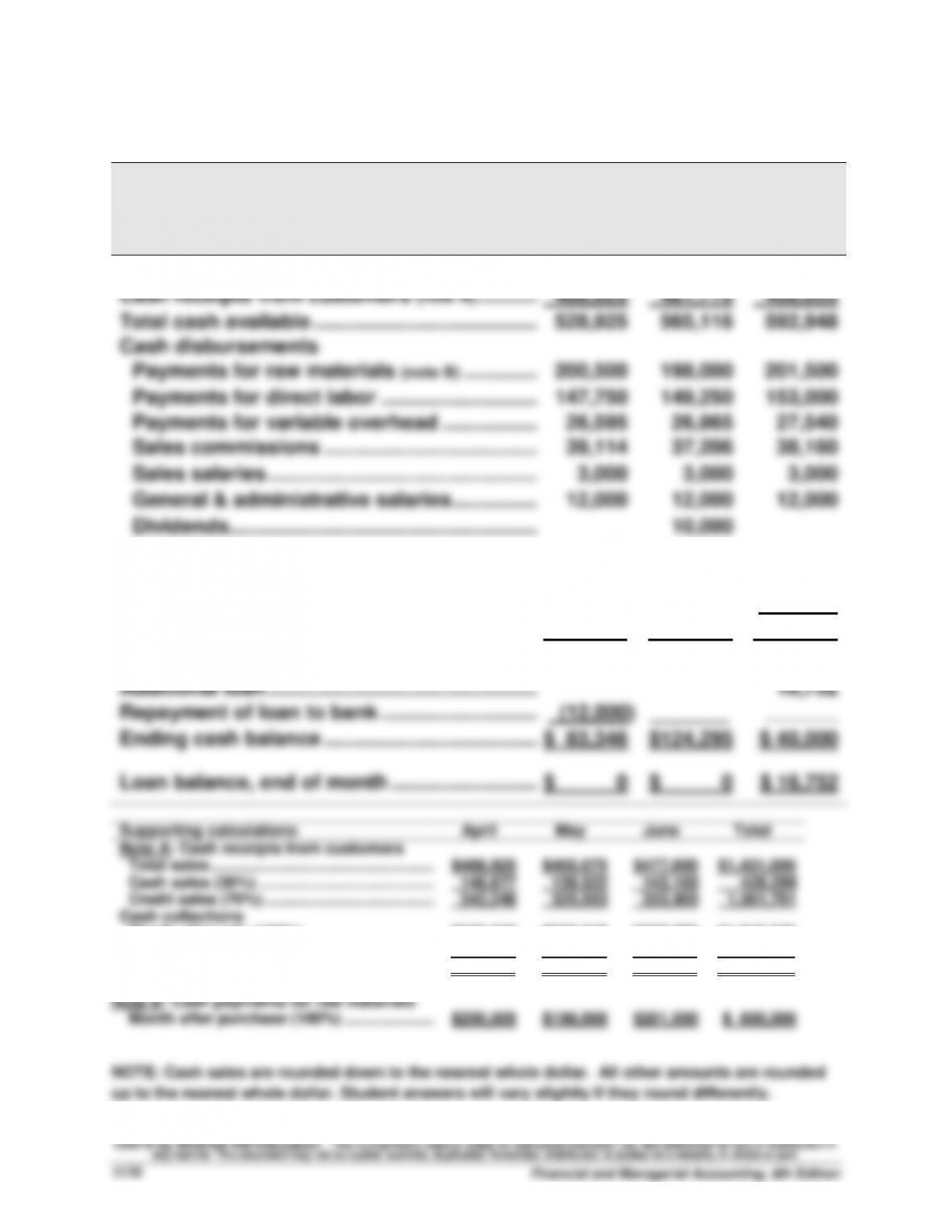

Part 8

ZIGBY MANUFACTURING

Cash Budgets

April, May, and June 2015

April

May

June

Beginning cash balance …………………………….….

$ 40,000

$ 83,346

$124,295

Cash receipts from customers (note A) …………….

488,925

481,770

468,653

Total cash available …………………………………..….

528,925

565,116

592,948

Cash disbursements

Payments for raw materials (note B) …………..….

200,500

198,000

201,500

Payments for direct labor ………………………..…

Payments for variable overhead ………………….

Sales commissions …………………………………….

147,750

26,595

39,114

149,250

26,865

37,206

153,000

27,540

38,160

Sales salaries ………………………………………….….

3,000

3,000

3,000

General & administrative salaries …………….….

12,000

12,000

12,000

Dividends………………………………………………..….

10,000

Loan interest ($12,000 x 1%) …………………………..

120

Long-term note interest ($500,000 x .0.9%) ……..….

Purchase of equipment ……………………………….

4,500

_______

4,500

_______

4,500

130,000

Total cash disbursements…………………………..

433,579

440,821

569,700

Preliminary cash balance …………………………..

95,346

124,295

23,248

Additional loan ………………………………………….….

Repayment of loan to bank ………………………..…

(12,000)

_______

16,752

_______

Ending cash balance …………………………………….

$ 83,346

$124,295

$ 40,000

Loan balance, end of month ………………………….

$ 0

$ 0

$ 16,752

Supporting calculations

April

May

June

Total

Note A: Cash receipts from customers

Total sales …………………………..………………….

$488,925

$465,075

$477,000

$1,431,000

Cash sales (30%) …………………………………….

146,677

139,522

143,100

429,299

Credit sales (70%) ………………………………..….

342,248

325,553

333,900

1,001,701

Cash collections

Month after sale (100%) ………………………..…

$342,248

$342,248

$325,553

$1,010,049

Cash sales …………………………………………..….

146,677

139,522

143,100

429,299

Total cash received ……………………………..…..

$488,925

$481,770

$468,653

$1,439,348

Month after purchase (100%) ………………..….

Problem 20-4A (Continued)

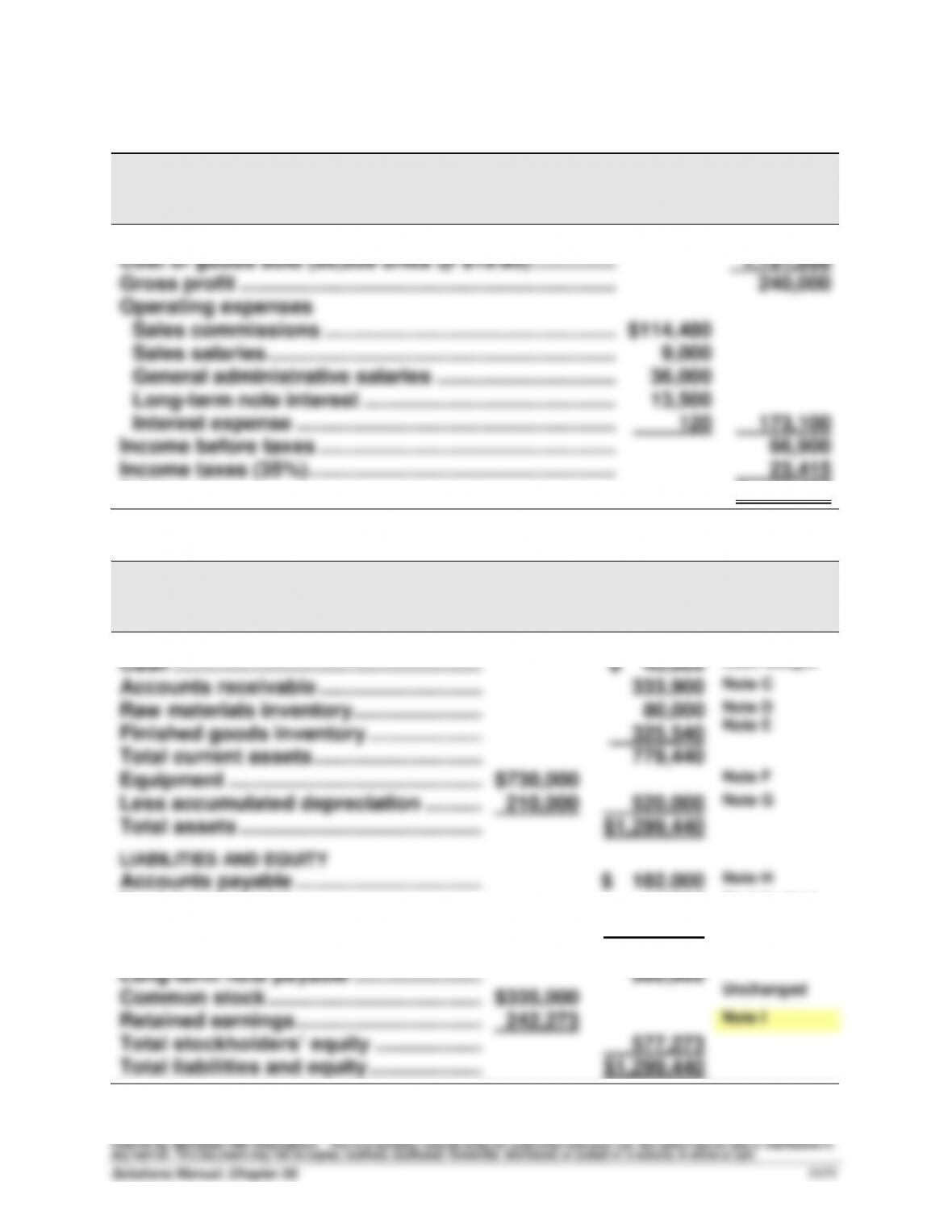

Part 9

ZIGBY MANUFACTURING

Budgeted Income Statement

For Three Months Ended June 30, 2015

Sales ……………………………………………………………………..

$1,431,000

Cost of goods sold (60,000 units @ $19.85) …………….

1,191,000

Gross profit …………………………………………………………..

240,000

Operating expenses

Sales commissions ……………………………………………..

$114,480

Sales salaries ……………………………………………………...

9,000

General administrative salaries …………………………..

36,000

Long-term note interest ……………………………………….

13,500

Interest expense …………………………..……………………..

120

173,100

Income before taxes ……………………………………………...

66,900

Income taxes (35%)………………………………………………..

23,415

Net income ……………………………………………………….…...

$ 43,485

Part 10

ZIGBY MANUFACTURING

Budgeted Balance Sheet

June 30, 2015

ASSETS

Cash …………………………..……………………….

$ 40,000

Cash budget

Accounts receivable …………………………..

333,900

Note C

Raw materials inventory……………………….

Finished goods inventory …………………….

80,000

325,540

Note D

Note E

Total current assets …………………………..

779,440

Equipment ……………………………………….….

$730,000

Note F

Less accumulated depreciation ………..….

210,000

520,000

Note G

Total assets …………………………..…………….

$1,299,440

LIABILITIES AND EQUITY

Accounts payable …………………………....….

$ 182,000

Note H

Bank loan payable ……………………………….

16,752

Cash budget

Taxes payable ………………………………….….

23,415

Income stmt.

Total current liabilities………………………….

222,167

Long-term note payable ……………………….

Common stock …………………………………….

$335,000

500,000

Unchanged

Retained earnings …………………………….….

242,273

Note I

Total stockholders’ equity ………………..….

577,273

Total liabilities and equity …………………….

$1,299,440

Problem 20-4A (Concluded)

Supporting Footnotes

Note C

Beginning receivables …………………………………………..….

$ 342,248

Credit sales ……………………………………………………….….….

1,001,701

Less collections ……………………………………………………….

(1,010,049)

Ending receivables …………………………..……………………….

$ 333,900

Note D

Beginning raw materials inventory …………………………..

$ 98,500

Purchases of raw materials ……………………………………….

581,500

Less materials used in production** ……………………….….

(600,000)

Ending raw materials inventory* …………………………….….

$ 80,000

*Also equals 4,000 units @ $20 = $80,000

**30,000 units x $20 per unit

Note E

Beginning finished goods inventory ……………………….….

$ 325,540

Cost of goods completed during the period…………….….

1,191,000

Less cost of goods sold during the period ……………..….

(1,191,000)

Ending finished goods inventory*…………………………..

$ 325,540

*Also equals 16,400 units @ $19.85 = $325,540

Note F

Beginning equipment …………………………………………….….

$ 600,000

Purchased in June ………………………………………………..….

130,000

Total …………………………………………………………………….….

$ 730,000

Note G

Beginning accumulated depreciation ……………………..….

$ 150,000

Depreciation expense ……………………………………………….

60,000

Total …………………………………………………………………….….

$ 210,000

Note H

Beginning accounts payable ………………………………….….

$ 200,500

Purchases of raw materials ……………………………………….

581,500

Payments for raw materials ……………………………………….

(600,000)

Ending accounts payable ………………………………………….

$ 182,000

Note I

Retained earnings, beginning ……………………. $208,788

Problem 20-5A (60 minutes)

Part 1

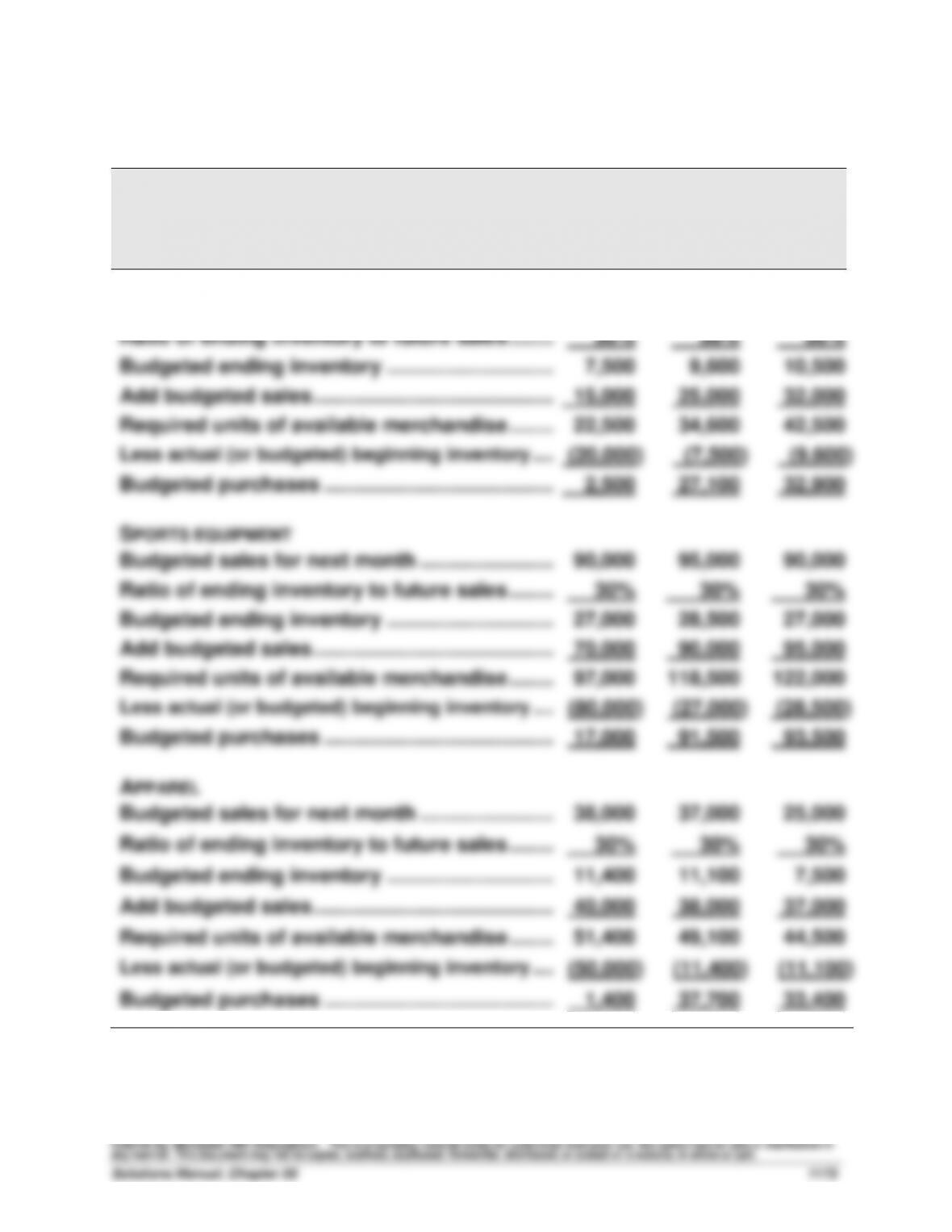

KEGGLER’S SUPPLY

Merchandise Purchases Budgets

For March, April, and May

March

April

May

FOOTWEAR

Budgeted sales for next month ………………………

25,000

32,000

35,000

Ratio of ending inventory to future sales ……..…

30%

30%

30%

Budgeted ending inventory …………………………..

7,500

9,600

10,500

Add budgeted sales …………………………………….…

15,000

25,000

32,000

Required units of available merchandise ……..…

22,500

34,600

42,500

Less actual (or budgeted) beginning inventory ….…

(20,000)

(7,500)

(9,600)

Budgeted purchases …………………………………..…

2,500

27,100

32,900

SPORTS EQUIPMENT

Budgeted sales for next month ………………………

90,000

95,000

90,000

Ratio of ending inventory to future sales ……..…

30%

30%

30%

Budgeted ending inventory …………………………..

27,000

28,500

27,000

Add budgeted sales …………………………………….…

70,000

90,000

95,000

Required units of available merchandise ……..…

97,000

118,500

122,000

Less actual (or budgeted) beginning inventory ….…

(80,000)

(27,000)

(28,500)

Budgeted purchases …………………………………..…

17,000

91,500

93,500

APPAREL

Budgeted sales for next month ………………………

38,000

37,000

25,000

Ratio of ending inventory to future sales ……..…

30%

30%

30%

Budgeted ending inventory …………………………..

11,400

11,100

7,500

Add budgeted sales …………………………………….…

40,000

38,000

37,000

Required units of available merchandise ……..…

51,400

49,100

44,500

Less actual (or budgeted) beginning inventory ….…

(50,000)

(11,400)

(11,100)

Budgeted purchases …………………………………..…

1,400

37,700

33,400

Problem 20-5A (Continued)

Part 2. Analysis Component

The factor that causes the first month’s purchases to be so much smaller is

the excess inventory that accumulated just prior to the budgeting period.

For example, 20,000 units of footwear are in March’s beginning inventory;

however, March sales are budgeted at only 15,000 units. Accordingly,

Problem 20-6A (50 minutes)

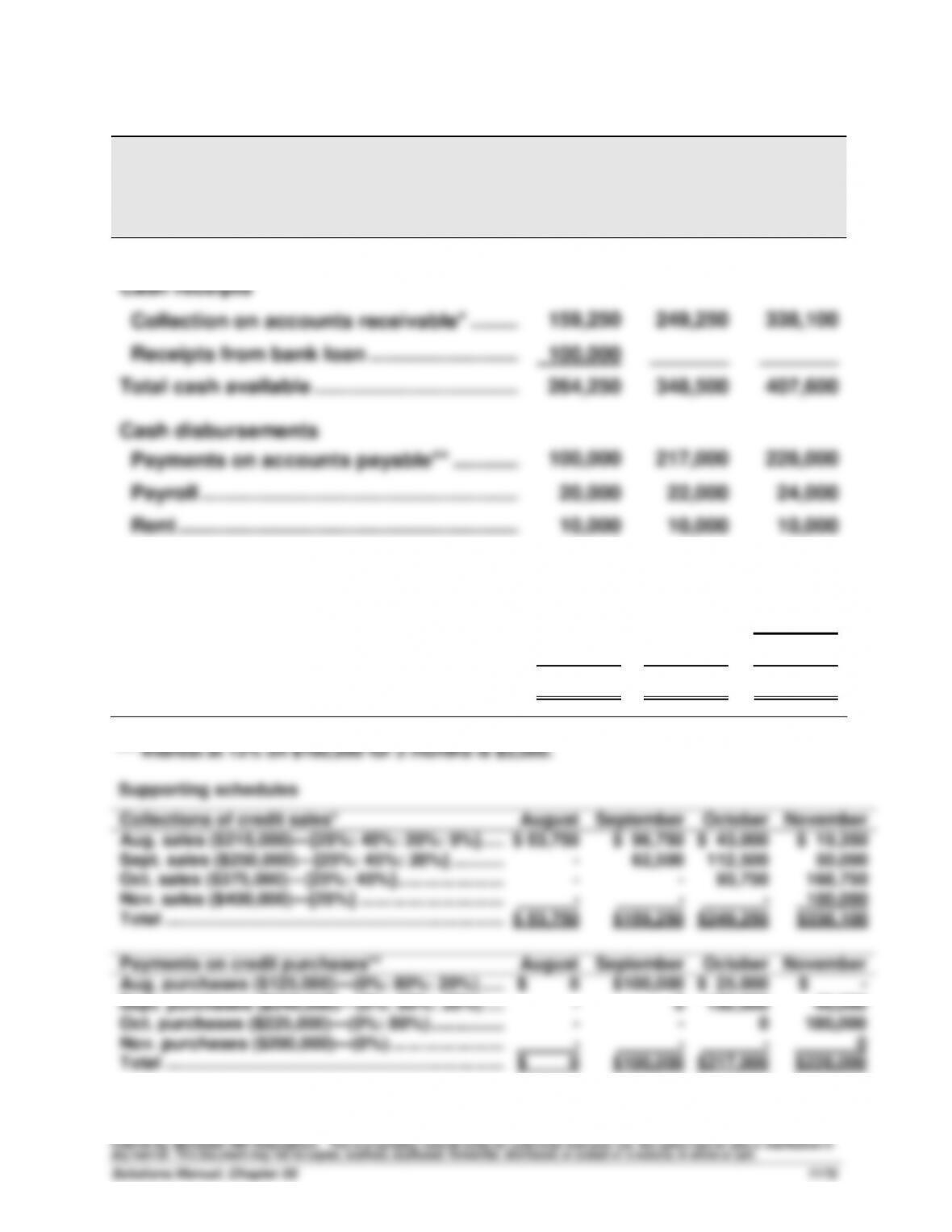

ONEIDA COMPANY

Cash Budget

For September, October, and November

September

October

November

Beginning balance ……………………………………

$ 5,000

$ 99,250

$ 69,500

Cash receipts

Collection on accounts receivable* …………

159,250

249,250

338,100

Receipts from bank loan …………………………

100,000

_______

_______

Total cash available ……………………………….…

264,250

348,500

407,600

Cash disbursements

Payments on accounts payable** ……………

100,000

217,000

228,000

Payroll ……………………………………………………

20,000

22,000

24,000

Rent …………………………………………………….…

10,000

10,000

10,000

Other expenses ………………………………………

35,000

30,000

20,000

Repayment on bank loan ……………………..…

100,000

Interest on bank loan***………………………..…

________

________

3,000

Total cash disbursements…………………….…

165,000

279,000

385,000

Ending cash balance ……………………………..…

$ 99,250

$ 69,500

$ 22,600

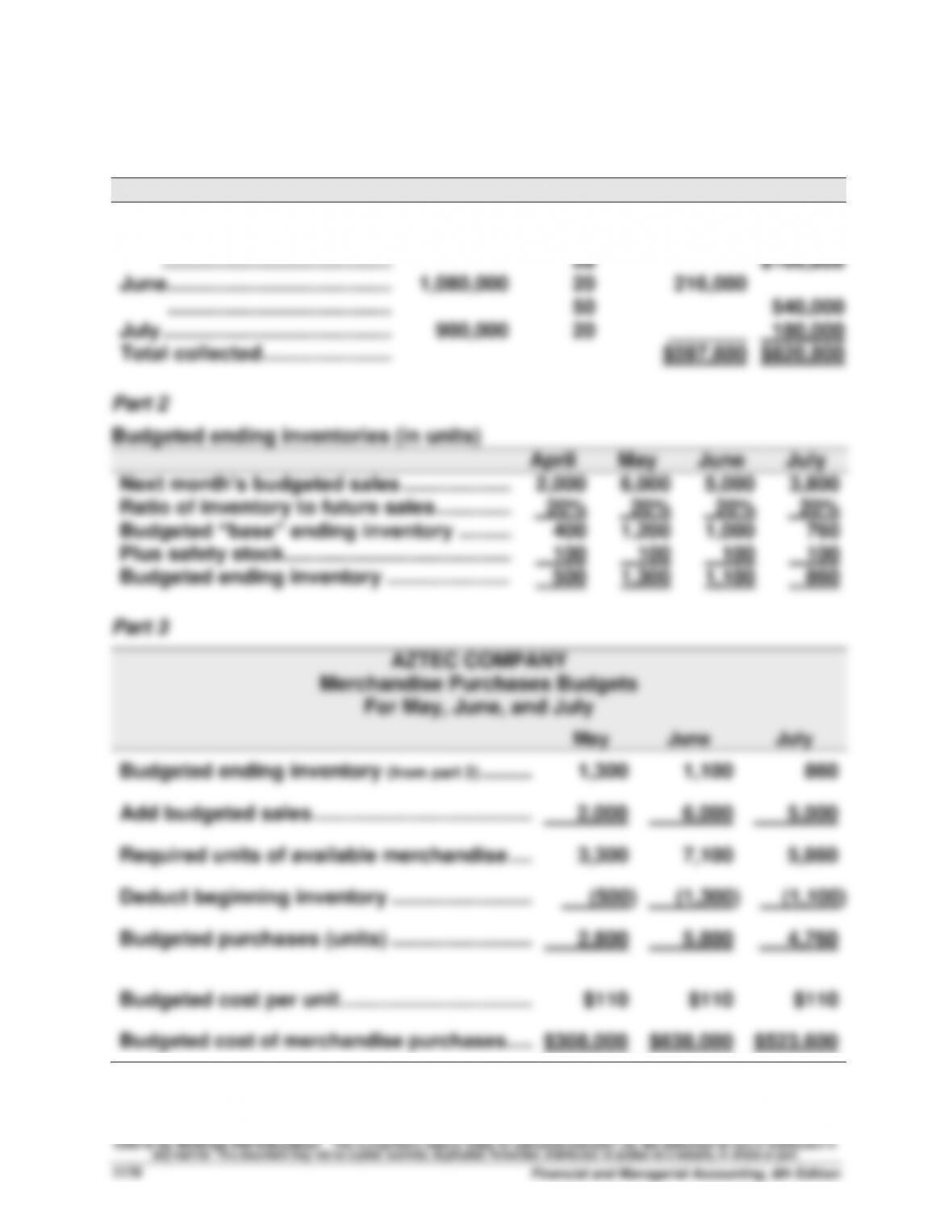

Problem 20-7A (70 minutes)

Part 1

Cash collections of credit sales (accounts receivable)

From sales in

Total

% Collected

June

July

April ………………………………….……

$ 720,000

28%

$201,600

May …………………………………..……

360,000

50

180,000

…………………………………..……

28

$100,800

June ………………………………….……

1,080,000

20

216,000

………………………………….……

50

540,000

July …………………………………..……

900,000

20

_______

180,000

Total collected …………………..……

$597,600

$820,800

Part 2

Budgeted ending inventories (in units)

April

May

June

July

Next month’s budgeted sales ………………...

2,000

6,000

5,000

3,800

Ratio of inventory to future sales …………...

20%

20%

20%

20%

Budgeted “base” ending inventory ………..

400

1,200

1,000

760

Plus safety stock …………………………………...

100

100

100

100

Budgeted ending inventory …………………...

500

1,300

1,100

860

Part 3

AZTEC COMPANY

Merchandise Purchases Budgets

For May, June, and July

May

June

July

Budgeted ending inventory (from part 2) …………

1,300

1,100

860

Add budgeted sales ……………………………………

2,000

6,000

5,000

Required units of available merchandise ….…

3,300

7,100

5,860

Deduct beginning inventory …………………….…

(500)

(1,300)

(1,100)

Budgeted purchases (units) …………………….…

2,800

5,800

4,760

Budgeted cost per unit …………………………….…

$110

$110

$110

Budgeted cost of merchandise purchases…..…

$308,000

$638,000

$523,600