Exercise 20–30 (continued)

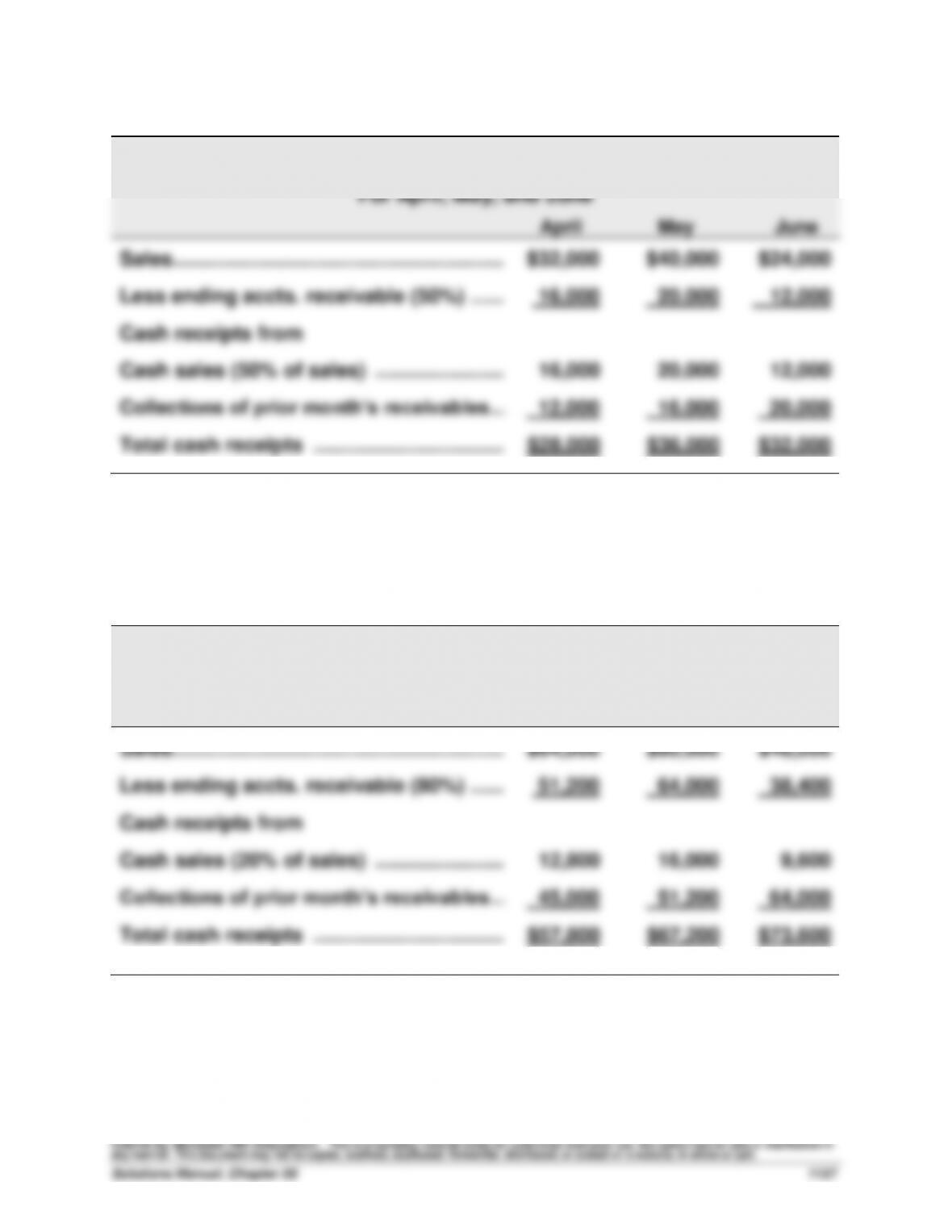

CASTOR, INC.

Cash Receipts Budget

For April, May, and June

April

May

June

Sales …………………………………………………..…

$32,000

$40,000

$24,000

Less ending accts. receivable (50%) ………

16,000

20,000

12,000

Cash receipts from

Cash sales (50% of sales) …………………..…

16,000

20,000

12,000

Collections of prior month’s receivables ……

12,000

16,000

20,000

Total cash receipts …………………………….…

$28,000

$36,000

$32,000

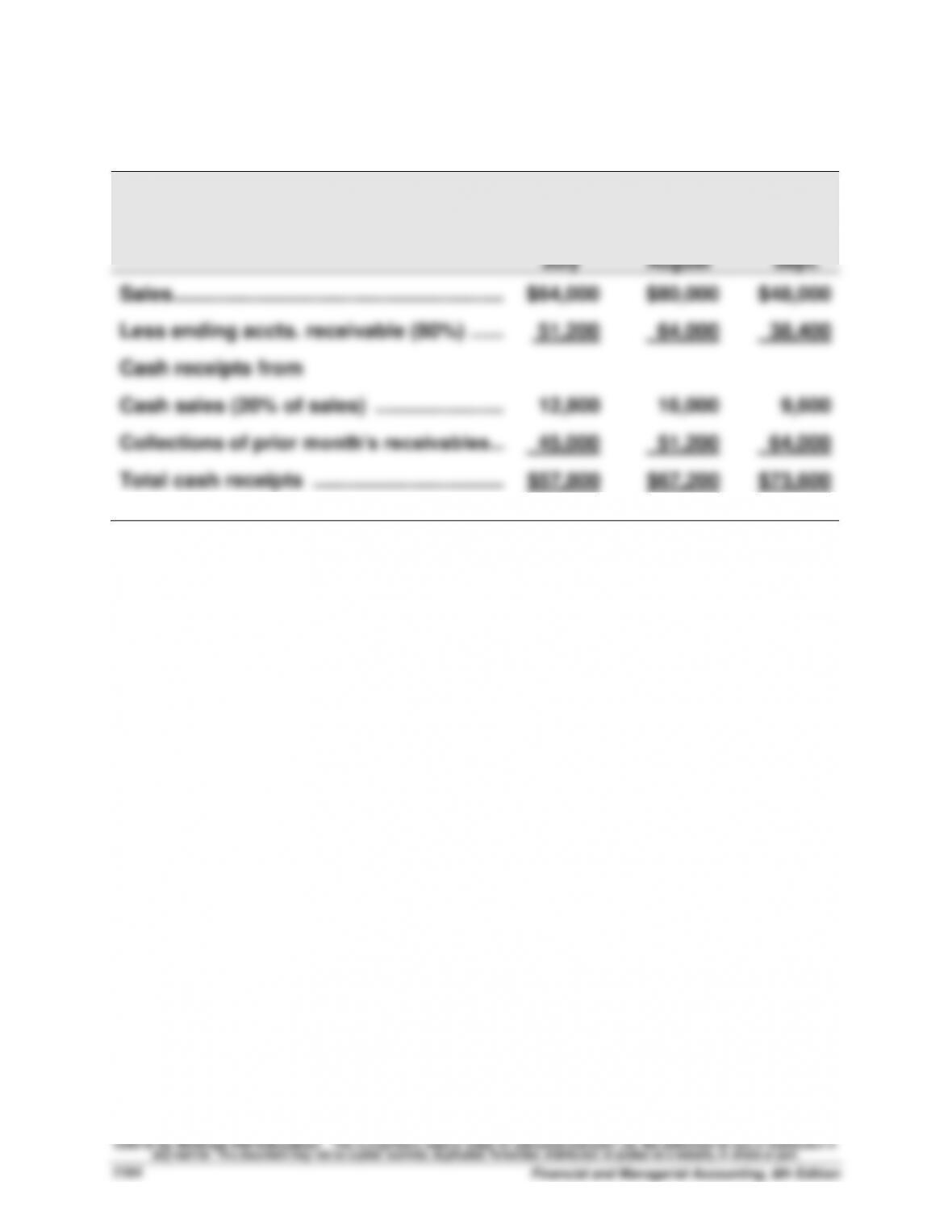

Exercise 20–31 (30 minutes)

(1)

KELSEY

Cash Receipts Budget

For July, August, and September

July

August

Sept.

Sales …………………………………………………..…

$64,000

$80,000

$48,000

Less ending accts. receivable (80%) ………

51,200

64,000

38,400

Cash receipts from

Cash sales (20% of sales) …………………..…

12,800

16,000

9,600

Collections of prior month’s receivables ……

45,000

51,200

64,000

Total cash receipts …………………………….…

$57,800

$67,200

$73,600

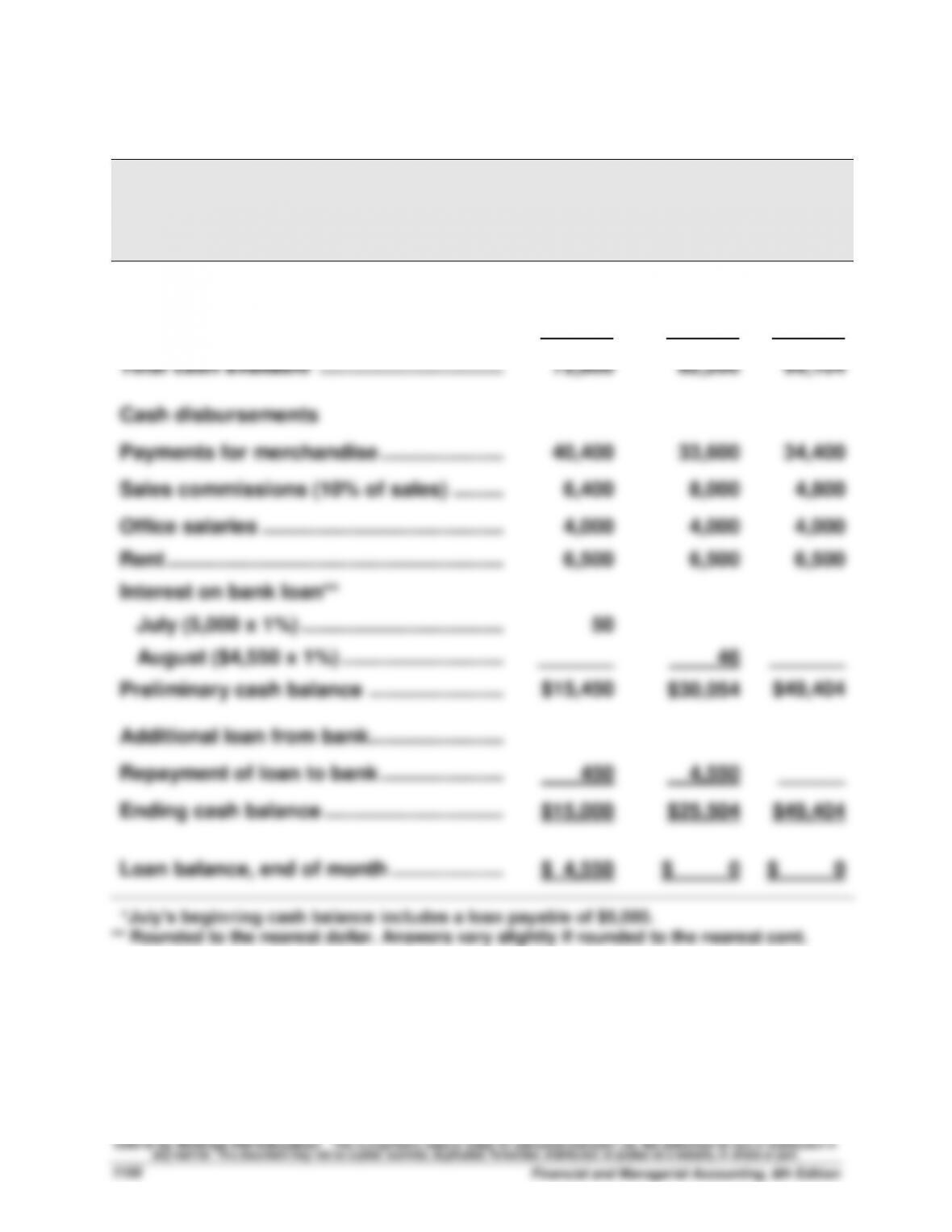

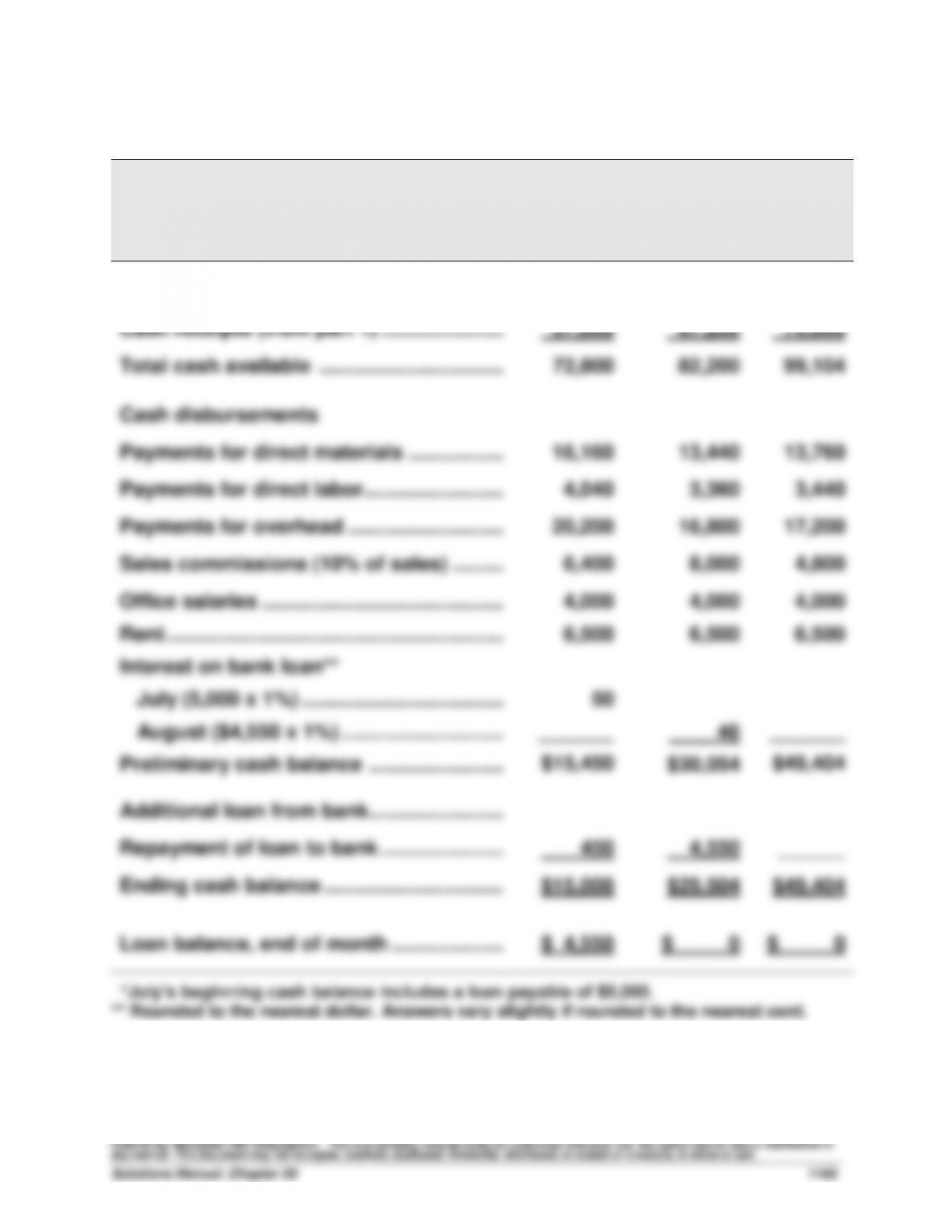

Exercise 20–31 (continued)

(2)

KELSEY

Cash Budget

For July, August, and September

July

August

Sept.

Beginning cash balance* …………………….…

$15,000

$15,000

$25,504

Cash receipts (from part 1) ………………….…

57,800

67,200

73,600

Total cash available ………………………………

72,800

82,200

99,104

Cash disbursements

Payments for merchandise ………………….…

40,400

33,600

34,400

Sales commissions (10% of sales) …………

6,400

8,000

4,800

Office salaries …………………………………….…

Rent ………………………………………………………

Interest on bank loan**

July (5,000 x 1%) …………………………………

August ($4,550 x 1%) ………………………..…

Preliminary cash balance ………………………

4,000

6,500

50

_______

$15,450

4,000

6,500

46

$30,054

4,000

6,500

_______

$49,404

Additional loan from bank………………………

Repayment of loan to bank ………………….…

450

4,550

______

Ending cash balance …………………………..

$15,000

$25,504

$49,404

Loan balance, end of month ………………..…

$ 4,550

$ 0

$ 0

*July’s beginning cash balance includes a loan payable of $5,000.

** Rounded to the nearest dollar. Answers vary slightly if rounded to the nearest cent.

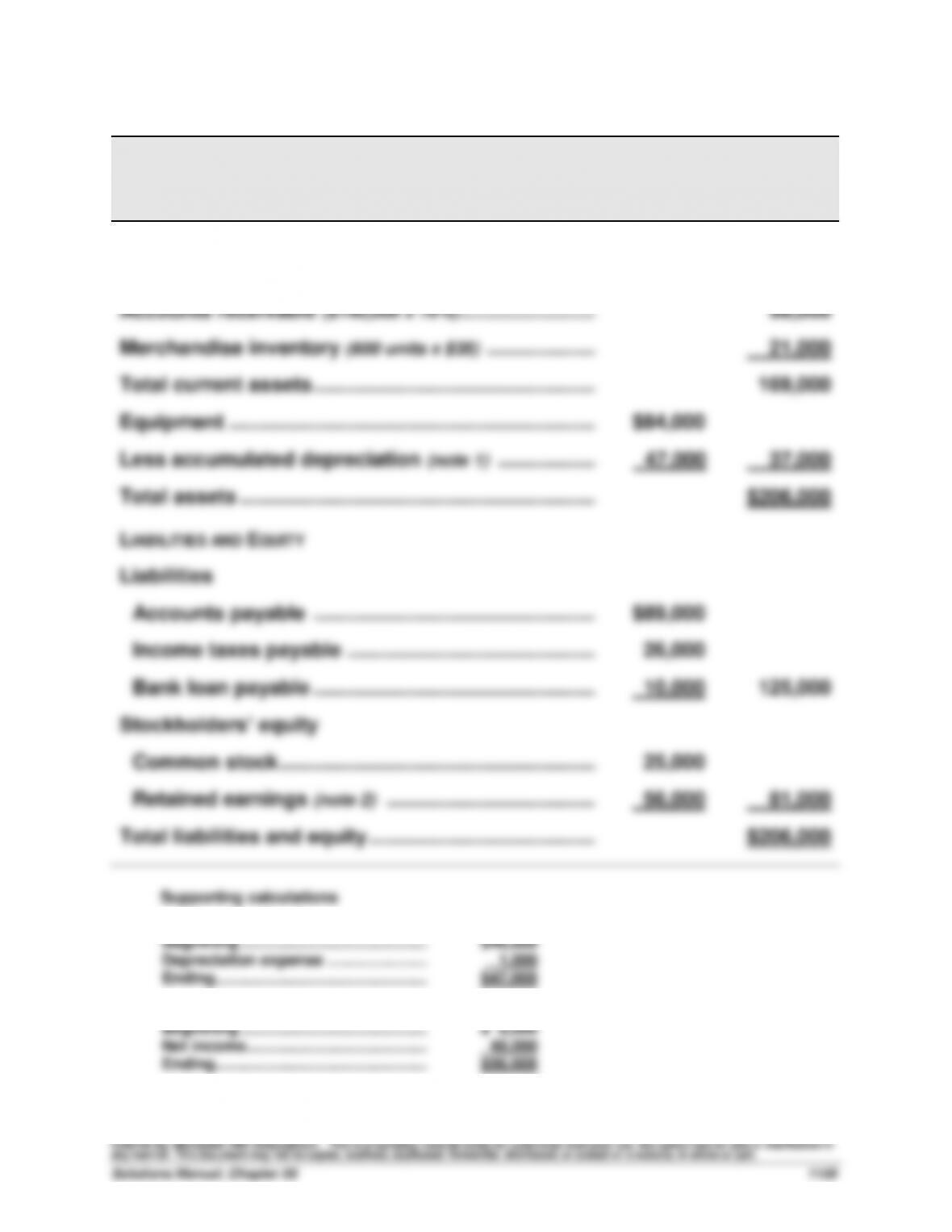

Exercise 20–32 (15 minutes)

ZETROV COMPANY

Budgeted Balance Sheet

As of March 31

ASSETS

Cash ………………………………………………………………….….

$ 50,000

Accounts receivable ($140,000 x 70%) …………………….….

98,000

Merchandise inventory (600 units x $35) ………………..….

21,000

Total current assets ……………………………………………….

169,000

Equipment …………………………………………………………….

$84,000

Less accumulated depreciation (note 1) ………………….

47,000

37,000

Total assets ……………………………………………………….

$206,000

LIABILITIES AND EQUITY

Liabilities

Accounts payable ……………………………………………….

$89,000

Income taxes payable ………………………………………….

26,000

Bank loan payable ……………………………………………….

10,000

125,000

Stockholders’ equity

Common stock …………………………………………………….

25,000

Retained earnings (note 2) …………………………..……….

56,000

81,000

Total liabilities and equity …………………………………..….

$206,000

Supporting calculations

(1) Accumulated depreciation

Beginning ……………………………………………………….

$46,000

Depreciation expense …………………..………

1,000

Ending…………………………..…………….…………….

$47,000

(2) Retained earnings

Beginning ……………………………………………………….

$ 8,000

Net income…………………………………..…………………..

48,000

Ending…………………………..…………….…………….

$56,000

Exercise 20–33 (15 minutes)

FORTUNE, INC.

Budgeted Income Statement

For Quarter Ended March 31

Sales (note 1) …………………………………………………………...

$3,750,000

Cost of goods sold (note 2) ……………………………………...

2,100,000

Gross profit …………………………………………………………...

1,650,000

Operating expenses

Commissions expense (8% of sales) ………………………..

$300,000

Rent expense ($14,000 x 3) ……………………………………...

42,000

Advertising expense (15% of sales) ………………………....

562,500

Office salaries expense ($75,000 x 3) ……………………....

225,000

Depreciation expense ($40,000 x 3) ………………………....

120,000

Interest expense ($250,000 x 15% x 3/12) …………………....

Total operating expenses ……………………………………..

9,375

1,258,875

Income before income taxes…………………………………...

391,125

Income tax expense (note 3) ……………………………………..

117,338

Net income …………………………..………………………………...

$ 273,787

Supporting calculations

(1) Sales

Unit sales (45,000 + 55,000 + 50,000) ………....

150,000

Unit price ………………………………………………...

$25

Sales dollars …………………………………………....

$3,750,000

(2) Cost of goods sold

Unit sales (45,000 + 55,000 + 50,000) ………....

150,000

Unit cost…………………………………………………..

$14

Cost of goods sold dollars ………………………..

$2,100,000

(3) Income tax expense

Pre-tax income ………………………………………...

$ 391,125

Tax rate …………………………………………………...

30%

Income tax expense ………………………………....

$ 117,338*

* Rounded to the nearest dollar.

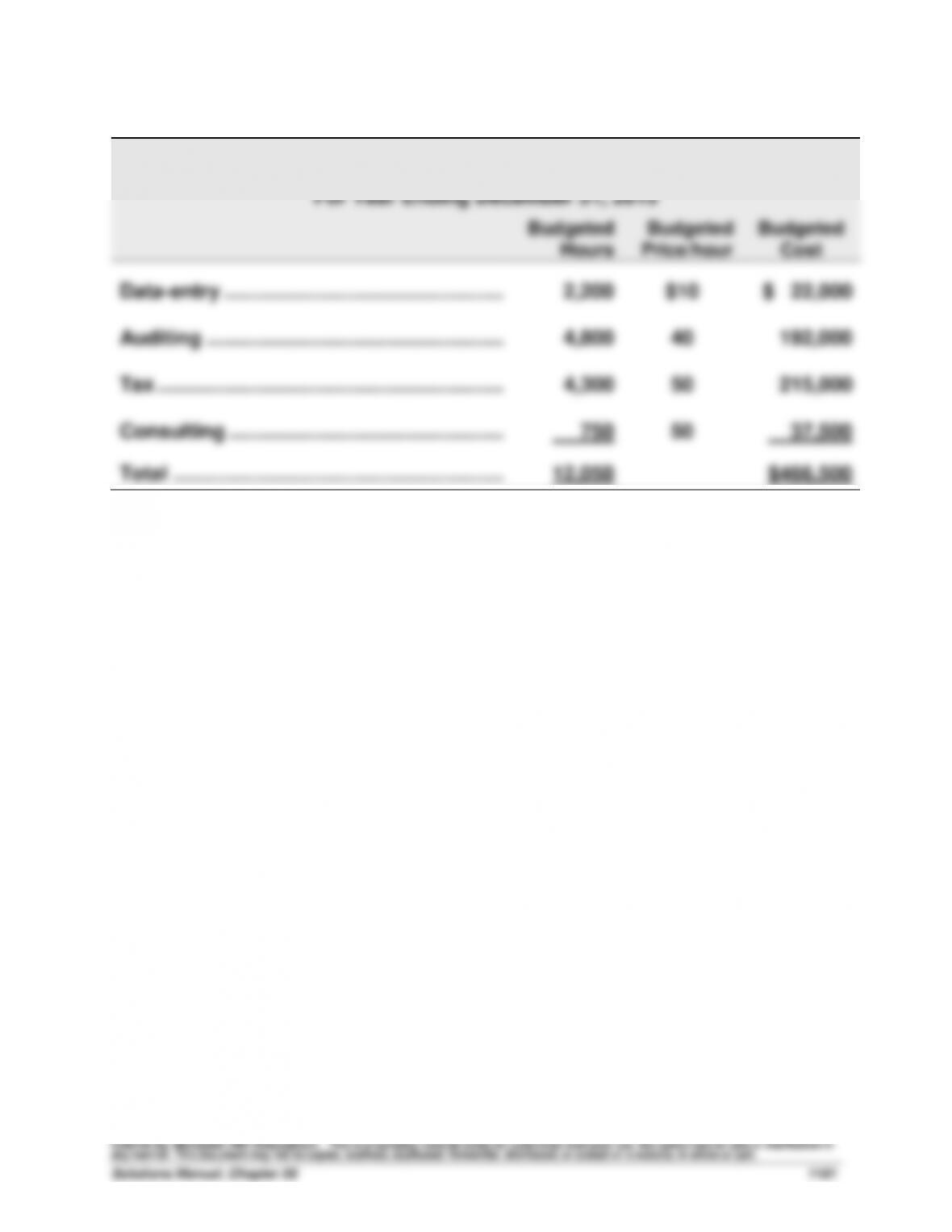

Exercise 20-34 (15 minutes)

RENDER CO. CPA

Activity-Based Budget

For Year Ending December 31, 2015

Budgeted

Hours

Budgeted

Price/hour

Budgeted

Cost

Data-entry …………………………………………..…

2,200

$10

$ 22,000

Auditing ……………………………………………..…

4,800

40

192,000

Tax ……………………………………………………....

4,300

50

215,000

Consulting ………………………………………….…

Total …………………………………………………..…

750

12,050

50

37,500

$466,500

Problem 20-1A (40 minutes)

Part 1

BLACK DIAMOND COMPANY

Production Budget (in units)

Third Quarter

Budgeted ending inventory (skis) …………………………………………………

3,500

Add budgeted sales ………………………………………………………………..……

150,000

Required units of available production …………………………………………

153,500

Deduct beginning inventory (skis) …………………………………………..……

(5,000)

Units to be manufactured………………………………………………………..……

148,500

Part 2

BLACK DIAMOND COMPANY

Direct Materials Budget (in lbs, except where noted)

Third Quarter

Materials (carbon fiber) needed for production (148,500 x 2) ……..

297,000

Add budgeted ending inventory (carbon fiber) ………………………....

4,000

Total materials (carbon fiber) requirements ……………………………...

301,000

Deduct beginning inventory (carbon fiber) ………………………………..

(6,000)

Units of materials (carbon fiber) to be purchased ……………………...

295,000

Materials cost per pound ………………………………………………………....

$15

Total cost of materials purchases (295,000 x $15) ……………………..

$4,425,000

Problem 20-1A (concluded)

Part 3

BLACK DIAMOND COMPANY

Direct Labor Budget

Third Quarter

Units to be produced ………………………………………………………

148,500

Labor requirements per unit (hours) …………………………..

x 0.50

Total labor hours needed …………………………………………..……

74,250

Labor rate (per hour) ………………………………………………………

x $20

Labor dollars …………………………………………………………….……

$1,485,000

Part 4

BLACK DIAMOND COMPANY

Factory Overhead Budget

Third Quarter

Total labor hours needed …………………………………………..……

74,250

Variable overhead rate per DL hour …………………………………

x $8

Budgeted variable overhead ……………………………………………

$ 594,000

Budgeted fixed overhead …………………………………………..……

1,782,000

Budgeted total overhead …………………………………………………

$2,376,000

Problem 20-2A (30 minutes)

(1)

BUILT-TIGHT

Cash Receipts Budget

For July, August, and September

July

August

Sept.

Sales …………………………………………………..…

$64,000

$80,000

$48,000

Less ending accts. receivable (80%) ………

51,200

64,000

38,400

Cash receipts from

Cash sales (20% of sales) …………………..…

12,800

16,000

9,600

Collections of prior month’s receivables ……

45,000

51,200

64,000

Total cash receipts …………………………….…

$57,800

$67,200

$73,600

Problem 20-2A (continued)

(2)

BUILT-TIGHT

Cash Budget

For July, August, and September

July

August

Sept.

Beginning cash balance* …………………….…

$15,000

$15,000

$25,504

Cash receipts (from part 1) ………………….…

57,800

67,200

73,600

Total cash available ………………………………

72,800

82,200

99,104

Cash disbursements

Payments for direct materials ……………..…

16,160

13,440

13,760

Payments for direct labor…………………….…

4,040

3,360

3,440

Payments for overhead ……………………….…

20,200

16,800

17,200

Sales commissions (10% of sales) …………

6,400

8,000

4,800

Office salaries …………………………………….…

Rent ………………………………………………………

Interest on bank loan**

July (5,000 x 1%) …………………………………

August ($4,550 x 1%) ………………………..…

Preliminary cash balance ………………………

4,000

6,500

50

_______

$15,450

4,000

6,500

46

$30,054

4,000

6,500

_______

$49,404

Additional loan from bank………………………

Repayment of loan to bank ………………….…

450

4,550

______

Ending cash balance …………………………..

$15,000

$25,504

$49,404

Loan balance, end of month ………………..…

$ 4,550

$ 0

$ 0

*July’s beginning cash balance includes a loan payable of $5,000.

** Rounded to the nearest dollar. Answers vary slightly if rounded to the nearest cent.

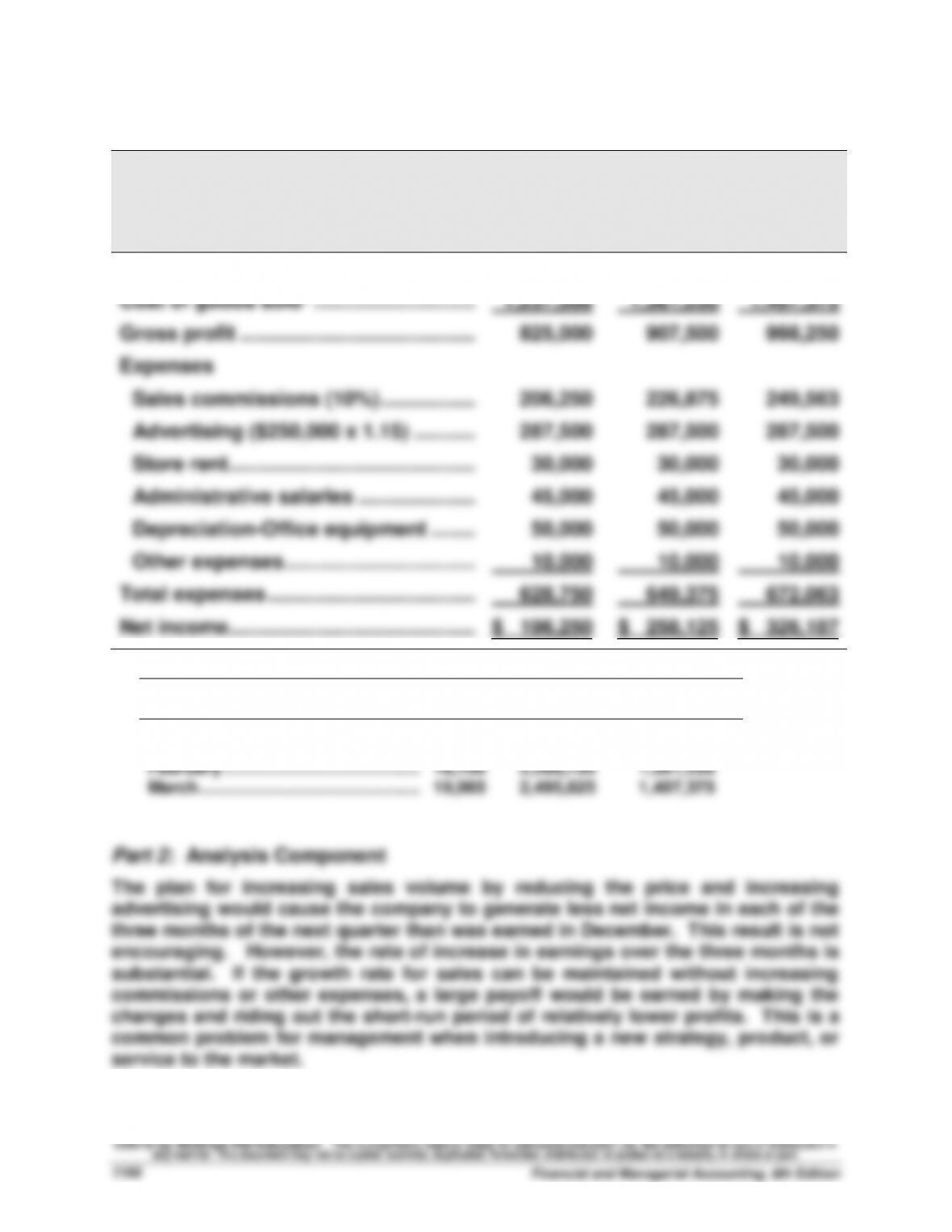

Problem 20-3A (50 minutes)

Part 1

MERLINE MANUFACTURING

Budgeted Income Statement

For Months of January, February, and March, 2016

January

February

March

Sales* …………………………………………….…

$2,062,500

$2,268,750

$2,495,625

Cost of goods sold* ………………………..…

1,237,500

1,361,250

1,497,375

Gross profit ………………………………………

825,000

907,500

998,250

Expenses

Sales commissions (10%) ……………..…

206,250

226,875

249,563

Advertising ($250,000 x 1.15) ………..…

287,500

287,500

287,500

Store rent ……………………………………..…

30,000

30,000

30,000

Administrative salaries ……………………

45,000

45,000

45,000

Depreciation-Office equipment ……..…

50,000

50,000

50,000

Other expenses …………………………….…

10,000

10,000

10,000

Total expenses ……………………………….…

628,750

649,375

672,063

Net income …………………………..……………

$ 196,250

$ 258,125

$ 326,187

* Volume for the next three months increases by 10% per month

Sales

Cost of Goods

Units

(@ $125)

Sold (@ $75)

December ($2,250,000/$150) …………………

15,000

January ………………………………………………

16,500

$2,062,500

$1,237,500

February …………………………..…………………

18,150

2,268,750

1,361,250

March ……………………………………….…………

19,965

2,495,625

1,497,375

Part 2: Analysis Component

The plan for increasing sales volume by reducing the price and increasing

advertising would cause the company to generate less net income in each of the

three months of the next quarter than was earned in December. This result is not

encouraging. However, the rate of increase in earnings over the three months is

substantial. If the growth rate for sales can be maintained without increasing

commissions or other expenses, a large payoff would be earned by making the

changes and riding out the short-run period of relatively lower profits. This is a

common problem for management when introducing a new strategy, product, or

service to the market.