Exercise 20-22 (30 minutes)

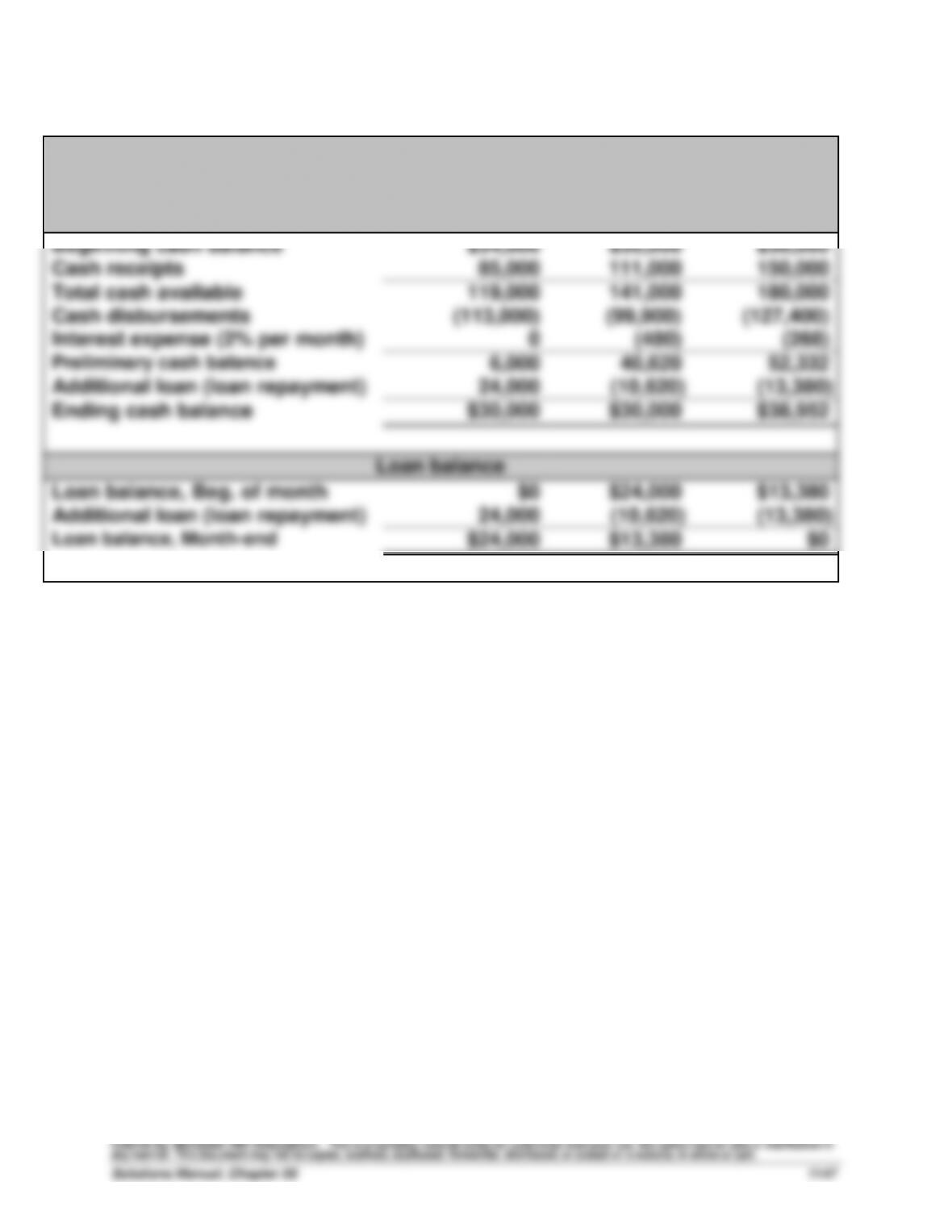

Mike’s Motors Corp.

Cash Budget

For July, August, and September

July

August

September

Beginning cash balance

$34,000

$30,000

$30,000

Cash receipts

85,000

111,000

150,000

Total cash available

119,000

141,000

180,000

Cash disbursements

(113,000)

(99,900)

(127,400)

Interest expense (2% per month)

0

(480)

(268)

Preliminary cash balance

6,000

40,620

52,332

Additional loan (loan repayment)

24,000

(10,620)

(13,380)

Ending cash balance

$30,000

$30,000

$38,952

Loan balance

Loan balance, Beg. of month

$0

$24,000

$13,380

Additional loan (loan repayment)

24,000

(10,620)

(13,380)

Loan balance, Month-end

$24,000

$13,380

$0

Exercise 20-23 (30 minutes)

1. Merchandise Purchases Budget

Note: Shaded numbers represent known information provided in the exercise.

Walker Company

Merchandise Purchases Budget

For July, August, and September

July

August

September

Next month’s budgeted sales …………..

315,000

270,000

200,000

(10)

Ratio of inventory to next month sales .

x 15%

(9)

x 15%

(9)

x 15%

(9)

Budgeted ending inventory ……………..

47,250

(6)

40,500

(3)

30,000

Add budgeted sales for month …………

180,000

315,000

270,000

Required units available inventory …..

227,250

(7)

355,500

(4)

300,000

(1)

Less beginning inventory ………………..

27,000

(8)

47,250

(5)

40,500

(2)

Budgeted merchandise purchases …..

200,250

308,250

259,500

Exercise 20-23 (concluded)

Notes: concluded

(5) August beginning inventory

Total required (4 above)

355,500

Less budgeted purchases

(308,250)

August beginning inventory

47,250

(6) August Beginning Inventory = July Ending Inventory

(7) July required units

Ending inventory

47,250

Add budgeted sales

180,000

Total required in July

227,250

(8) July Beginning Inventory

Total required (7 above)

227,250

Less budgeted purchases

(200,250)

July beginning inventory

27,000

(9) Percent of Sales to be held as Ending Inventory

Ending inventory for August

September Sales

= 40,500 = 15%

270,000

This percentage is constant for the three months.

(10) October expected sales

September Ending Inventory

Required %

= 30,000 = 200,000

15%

2. Monthly ending inventory is 15% of next month’s sales (see note #9).

3. October budgeted sales = 200,000 (see note #10 above).

Exercise 20–24 (25 minutes)

ACCO COMPANY

Cash Budget

For Month Ended July 31

Beginning cash balance ……………………………………..….

$ 50,000

Cash receipts from sales (note 1) …………………………..

1,364,000

Total cash available ……………………………………………….

$1,414,000

Cash disbursements

Payments for merchandise (note 2) …………………….….

730,000

Salaries ……………………………………………………………….

275,000

Other expenses ………………………………………………..….

200,000

Accrued taxes ………………………………………………….….

80,000

Interest on bank loan ……………………………………….….

6,600

Total cash disbursements…………………………..………….

1,291,600

Ending cash balance ………………………………………….….

$ 122,400

Supporting calculations

(1) Cash receipts in July from sales

From May sales ($1,720,000 x 20%) …………..

$ 344,000

From June sales ($1,200,000 x 50%) ………….

600,000

From July sales ($1,400,000 x 30%) …………..

420,000

Total …………………………..…………………………...

$1,364,000

(2) Cash disbursements in July for merchandise

For June purchases ($700,000 x 40%) ……….

$ 280,000

For July purchases ($750,000 x 60%) ………..

450,000

Total …………………………..…………………………...

$ 730,000

Exercise 20–25 (45 minutes)

ACCO COMPANY

Budgeted Income Statement

For Month Ended July 31

Sales (from Exercise 20–24) ………………………………………....

$1,400,000

Cost of goods sold (note 1) ……………………………………...

770,000

Gross profit …………………………………………………………...

630,000

Operating expenses

Salaries expense (note 2) ……………………………………....

$285,000

Depreciation expense (from Exercise 20–24) ……………....

36,000

Other cash expenses (from Exercise 20–24) ………………..

200,000

Bank loan interest expense …………………………………..

6,600

Total expenses ……………………………………………………....

527,600

Income before taxes ……………………………………………....

102,400

Income tax expense (note 3) ……………………………………..

30,720

Net income ……………………………………………………………..

$ 71,680

Supporting calculations

(1) Cost of goods sold

Sales ……………………………………………………....

$1,400,000

Cost percent …………………………………………....

55%

Cost of goods sold …………………………………..

$ 770,000

(2) Salaries expense

Cash paid ………………………………………………...

$ 275,000

Less beginning payable …………………………..

(50,000)

Plus ending payable ………………………………...

60,000

Salaries expense ……………………………………...

$ 285,000

(3) Income tax expense

Pre-tax income ………………………………………...

$ 102,400

Tax rate …………………………………………………...

30%

Income tax expense ………………………………....

$ 30,720

Exercise 20–25 (Continued)

ACCO COMPANY

Budgeted Balance Sheet

As of July 31

ASSETS

Cash (from Exercise 20–24) ……………………………………..….

$ 122,400

Accounts receivable (note 1) ………………………………..….

1,220,000

Inventory (given) ………………………………………………….….

60,000

Total current assets ……………………………………………….

1,402,400

Equipment …………………………..…………………………….….

$1,600,000

Less accumulated depreciation (note 2) ……………….….

316,000

1,284,000

Total assets …………………………..…………………………..

$2,686,400

LIABILITIES AND EQUITY

Liabilities

Accounts payable (note 3) ………………………………….….

$ 300,000

Salaries payable ………………………………………………….

60,000

Income taxes payable ………………………………………….

30,720

Total current liabilities ……………………………………..….

390,720

Bank loan payable ……………………………………………….

660,000

1,050,720

Stockholders’ equity

Common stock …………………………..…………………….….

600,000

Retained earnings (note 4) …………………………………….

1,035,680

1,635,680

Total liabilities and equity …………………………………..….

$2,686,400

Supporting calculations

(1) Accounts receivable

June sales (20% x $1,200,000) ……….………………….

$ 240,000

July sales (70% x $1,400,000) …………………………..

980,000

Total ……………………………………………………….

$ 1,220,000

(2) Accumulated depreciation

Beginning ……………………………………………………….

$ 280,000

Expense ……………………………………………………….

36,000

Ending……………………………………………………….

$ 316,000

(3) Accounts payable

Purchases ……………………………………………………….

$ 750,000

Percent unpaid …………………………....……………………

40%

Payable ……………………………………….………………

$ 300,000

(4) Retained earnings

Beginning ……………………………………………………….

$ 964,000

Net income…………………………………..…………………..

71,680

Ending……………………………………………………….

$1,035,680

Exercise 20–26 (30 minutes)

Preliminary calculations (sales, cost of sales, beginning and ending inventory)

August

September

October

November

Sales……………………………………………………

$325,000

$ 320,000

$250,000

$310,000

Cost to sales percent …………………………..

x 60%

x 60%

x 60%

x 60%

Cost of goods sold …………………………….…

195,000

192,000

150,000

186,000

Beginning inventory percent …………………

x 20%

x 20%

x 20%

x 20%

Beginning inventory …………………………..

$ 39,000

$ 38,400

$ 30,000

$ 37,200

Ending inventory (from next month) ………

$ 38,400

$ 30,000

$ 37,200

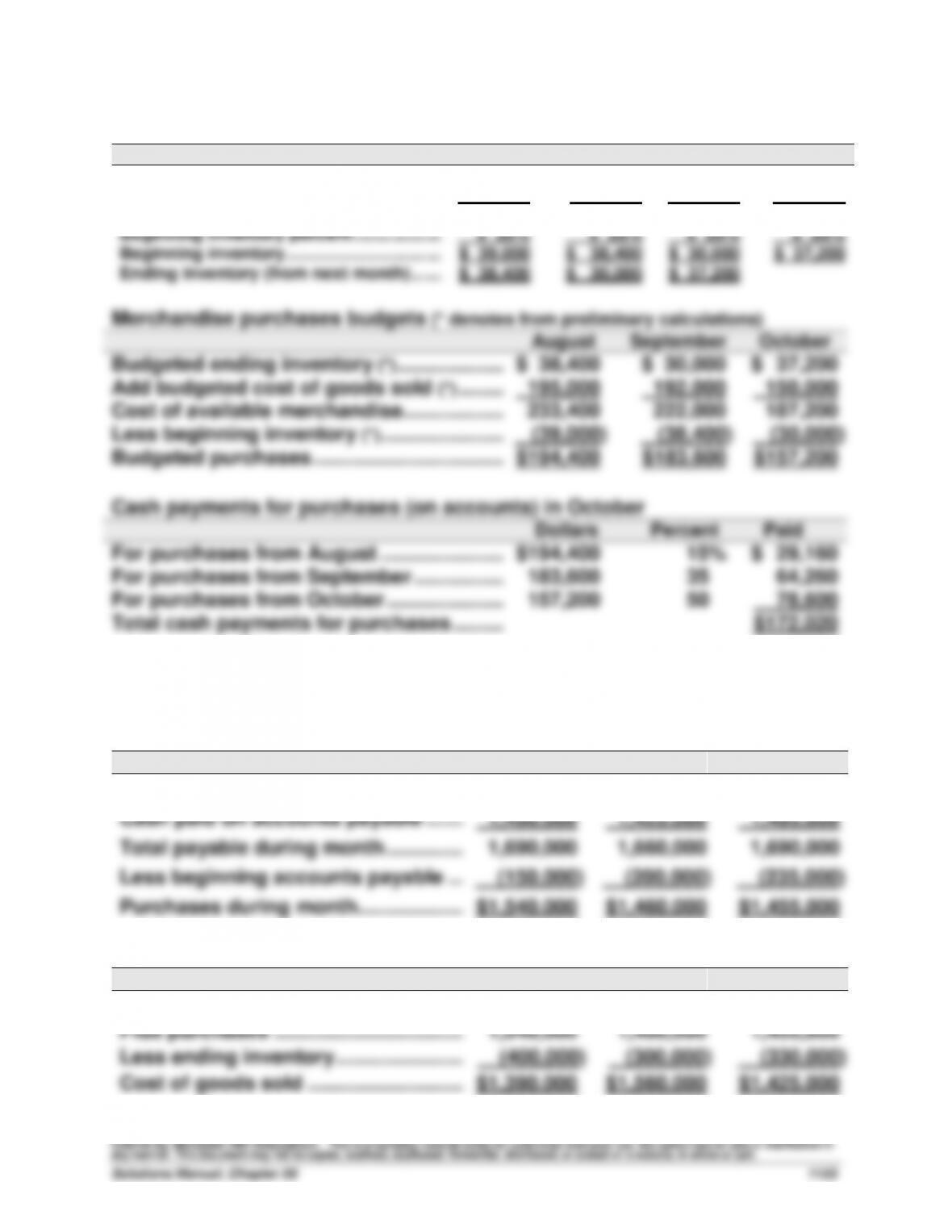

Merchandise purchases budgets (* denotes from preliminary calculations)

August

September

October

Budgeted ending inventory (*) ……………….…..

$ 38,400

$ 30,000

$ 37,200

Add budgeted cost of goods sold (*) ……..…..

195,000

192,000

150,000

Cost of available merchandise…………………..

233,400

222,000

187,200

Less beginning inventory (*) ………………….…..

(39,000)

(38,400)

(30,000)

Budgeted purchases …………………………….…..

$194,400

$183,600

$157,200

Cash payments for purchases (on accounts) in October

Dollars

Percent

Paid

For purchases from August ………………….…..

$194,400

15%

$ 29,160

For purchases from September …………….…..

183,600

35

64,260

For purchases from October ……………………..

157,200

50

78,600

Total cash payments for purchases …………..

$172,020

Exercise 20–27 (25 minutes)

1. Budgeted merchandise purchases

June

July

August

Ending accounts payable……………………..

$ 200,000

$ 235,000

$ 195,000

Cash paid on accounts payable …….……..

1,490,000

1,425,000

1,495,000

Total payable during month …………..……..

1,690,000

1,660,000

1,690,000

Less beginning accounts payable ………..

(150,000)

(200,000)

(235,000)

Purchases during month……………….……..

$1,540,000

$1,460,000

$1,455,000

2. Budgeted cost of goods sold

June

July

August

Beginning inventory ……………………..……

$ 250,000

$ 400,000

$ 300,000

Plus purchases …………………………….……..

1,540,000

1,460,000

1,455,000

Less ending inventory …………………..……..

(400,000)

(300,000)

(330,000)

Cost of goods sold ……………………….….

$1,390,000

$1,560,000

$1,425,000

Exercise 20–28 (40 minutes)

1.

Preliminary calculations (sales, cost of sales, beginning inventory)

July

August

September

October

November

Budgeted sales ………………………….

$350,000

$290,000

$320,000

$275,000

$265,000

Cost to sales percent ……………..….

x 70%

x 70%

x 70%

x 70%

x 70%

Budgeted cost of goods sold ….….

245,000

203,000

224,000

192,500

185,500

Budgeted inventory percent ……….

x 20%

x 20%

x 20%

x 20%

x 20%

Budgeted beginning inventory …..….

$ 49,000

$ 40,600

$ 44,800

$ 38,500

$ 37,100

Budgeted merchandise purchases

July

August

September

October

Budgeted ending inventory ………..……

$ 40,600

$ 44,800

$ 38,500

$ 37,100

Budgeted cost of goods sold ……..……

245,000

203,000

224,000

192,500

Cost of available merchandise …………

285,600

247,800

262,500

229,600

Less beginning inventory …………..……

(49,000)

(40,600)

(44,800)

(38,500)

Budgeted purchases ………………….……

$236,600

$207,200

$217,700

$191,100

2.

Budgeted payments on accounts payable in September

Purchases

Percent Paid

Dollars Paid

For purchases from September………..

$217,700

25%

$ 54,425

For purchases from August ……………..

207,200

60

124,320

For purchases from July ………………….

236,600

15

35,490

Total payments ……………………………….

$214,235

Budgeted payments on accounts payable in October

Purchases

Percent Paid

Dollars Paid

For purchases from October ……………

$191,100

25%

$ 47,775

For purchases from September………..

217,700

60

130,620

For purchases from August ……………..

207,200

15

31,080

Total payments ……………………………….

$209,475

3.

Budgeted balance of accounts payable at the end of September

Purchases

Percent Unpaid

Dollars Unpaid

From purchases in September ………...

$217,700

75%

$163,275

From purchases in August ……………...

207,200

15

31,080

Total …………………………..…………………..

$194,355

Budgeted balance of accounts payable at the end of October

Purchases

Percent Unpaid

Dollars Unpaid

From purchases in October ……………..

$191,100

75%

$143,325

From purchases in September ………...

217,700

15

32,655

Total …………………………..…………………..

$175,980

Exercise 20–29 (10 minutes)

HECTOR COMPANY

Budgeted Cash Disbursements

For August and September

August

Sept.

Payments for merchandise*……………………………………….……

$14,400

$19,200

Selling expenses (10% of sales) ………………………………………

7,200

6,600

Administrative expenses (8% of sales) …………………………..

5,760

5,280

Rent expense ……………………………………………………….…………

7,400

7,400

Total cash disbursements…………………………..……………..……

$34,760

$38,480

**Equals prior month’s purchases. Note that depreciation expense is excluded since it is

a non-cash expense.

Exercise 20–30 (25 minutes)

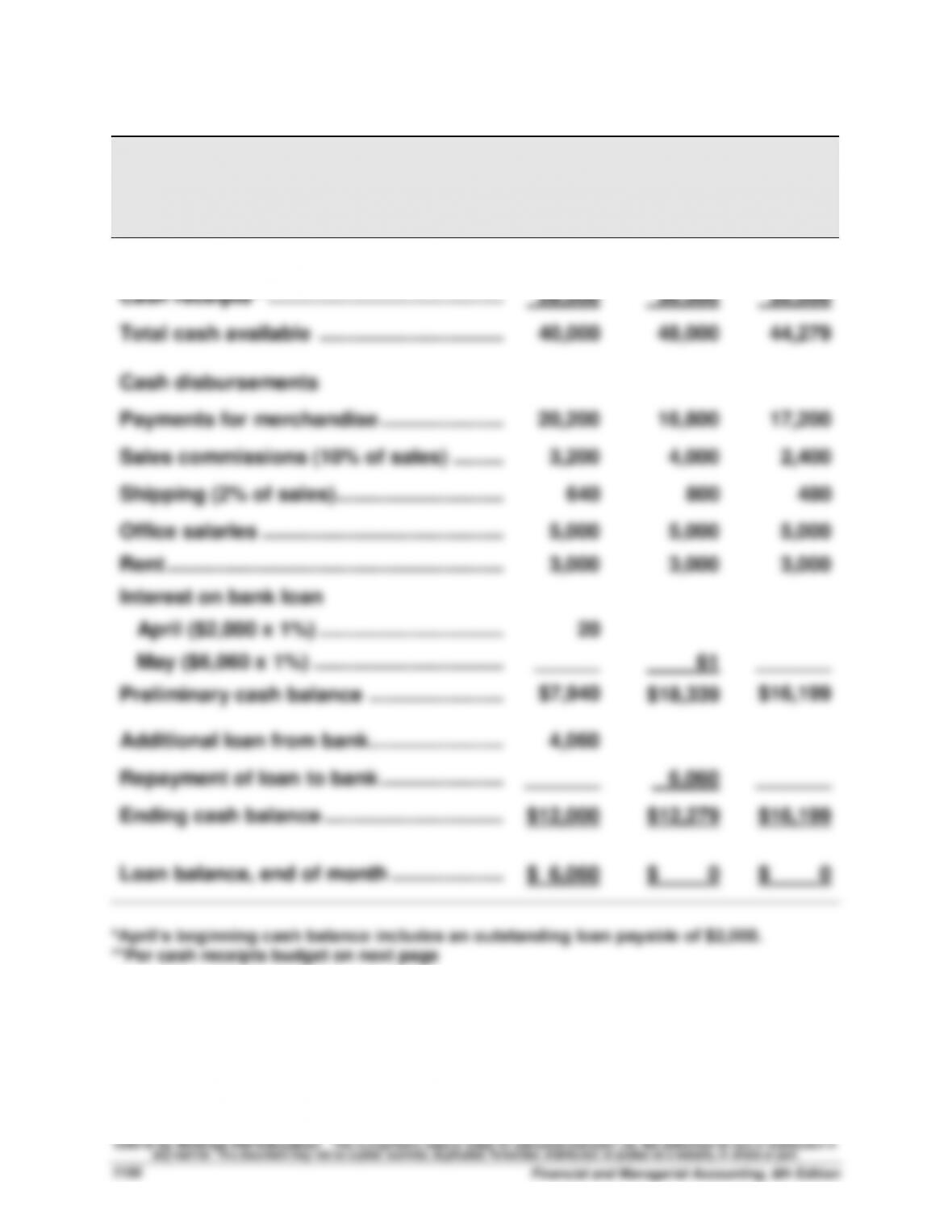

CASTOR, INC.

Cash Budget

For April, May, and June

April

May

June

Beginning cash balance* …………………….…

$12,000

$12,000

$12,279

Cash receipts** ………………………………………

28,000

36,000

32,000

Total cash available ………………………………

40,000

48,000

44,279

Cash disbursements

Payments for merchandise ………………….…

20,200

16,800

17,200

Sales commissions (10% of sales) …………

3,200

4,000

2,400

Shipping (2% of sales)…………………………..

640

800

480

Office salaries …………………………..………..…

Rent ………………………………………………………

Interest on bank loan

April ($2,000 x 1%) …………………………...…

May ($6,060 x 1%) …………………………….…

Preliminary cash balance ………………………

5,000

3,000

20

______

$7,940

5,000

3,000

61

$18,339

5,000

3,000

_______

$16,199

Additional loan from bank………………………

4,060

Repayment of loan to bank ………………….…

_______

6,060

_______

Ending cash balance …………………………..

$12,000

$12,279

$16,199

Loan balance, end of month ………………..…

$ 6,060

$ 0

$ 0

*April’s beginning cash balance includes an outstanding loan payable of $2,000.

**Per cash receipts budget on next page