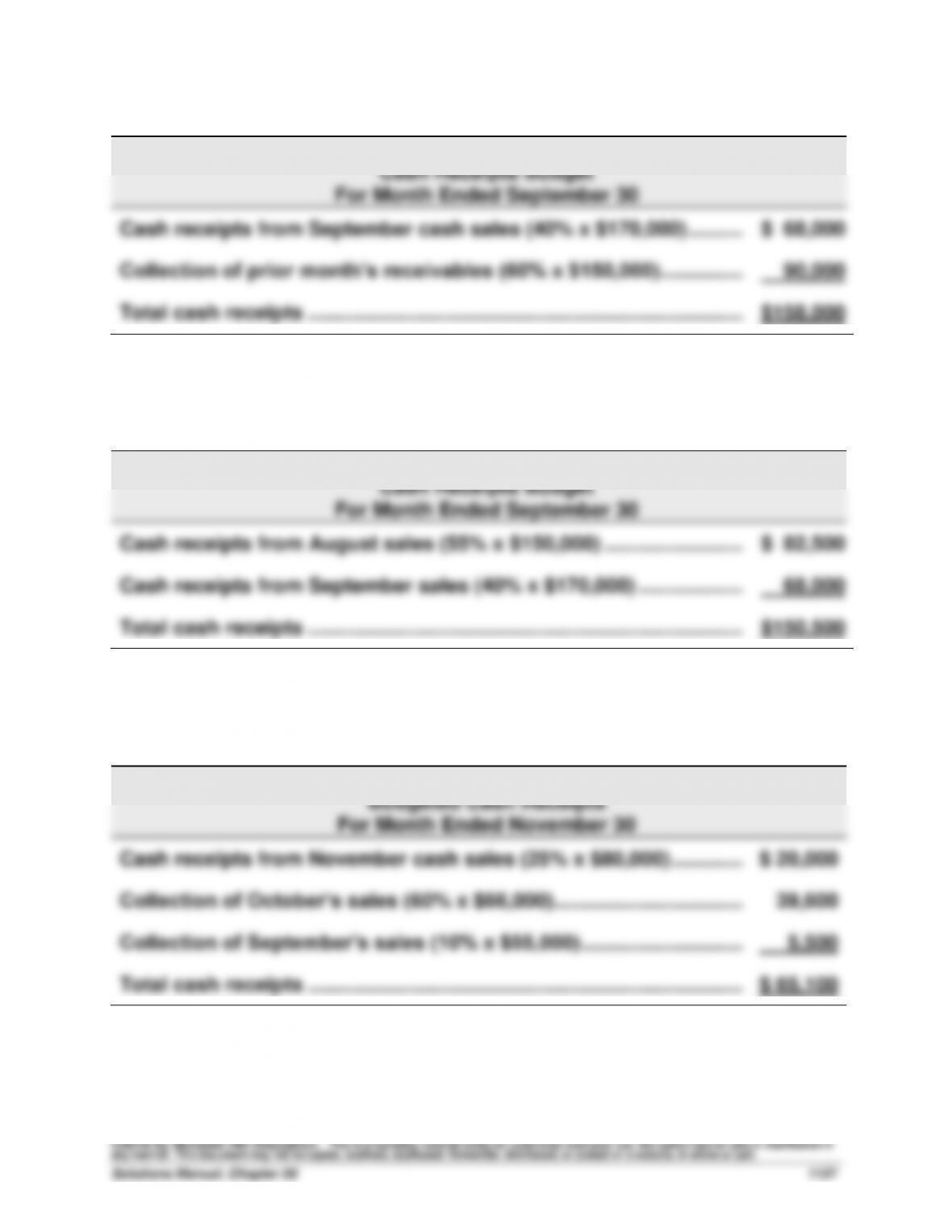

Quick Study 20-19 (10 minutes)

GUITAR SHOPPE

Cash Receipts Budget

For Month Ended September 30

Cash receipts from September cash sales (40% x $170,000) ………...

$ 68,000

Collection of prior month’s receivables (60% x $150,000)……………..

90,000

Total cash receipts ……………………………………………………………………..

$158,000

Quick Study 20–20 (10 minutes)

MUSIC WORLD

Cash Receipts Budget

For Month Ended September 30

Cash receipts from August sales (55% x $150,000) ……………………...

$ 82,500

Cash receipts from September sales (40% x $170,000) ………………...

68,000

Total cash receipts ……………………………………………………………………..

$150,500

Quick Study 20–21 (10 minutes)

WELLS COMPANY

Budgeted Cash Receipts

For Month Ended November 30

Cash receipts from November cash sales (25% x $80,000) …………...

$ 20,000

Collection of October’s sales (60% x $66,000) ……………………………...

39,600

Collection of September’s sales (10% x $55,000) ………………………....

5,500

Total cash receipts ……………………………………………………………………..

$ 65,100

Quick Study 20–22 (15 minutes)

Computation of budgeted Accounts Receivable balance as of July 31

Sales month

Total Sales

Credit

Sales*

Percent Still

Uncollected*

Amount

Uncollected

June ……………..….

$420,000

$168,000

10%

$ 16,800

July ………………….

398,000

159,200

80%

127,360

Total …………….….

$144,160

* Credit sales are 40% of total sales—of these credit sales, 20% are collected in the sale month,

70% are collected in the month after sale, and 10% are collected in the second month after sale.

Quick Study 20–23 (5 minutes)

MESSERS COMPANY

Cash Budget

For Month Ended February 28

Beginning cash balance ……………………………………………………………...

$ 20,000

Cash receipts ……………………………………………………………………………..

75,000

Total cash available …………………………………………………………………....

95,000

Cash disbursements……………………………………………………….…………..

(100,250)

Preliminary cash balance …………………………………………………………....

$ (5,250)

Additional loan from bank…………………………………………………………...

10,250

Ending cash balance …………………………………………………………………..

$ 5,000

Based on the cash budget above, the company must borrow $10,250 during

February to maintain a $5,000 cash balance.

Quick Study 20–24 (15 minutes)

GADO COMPANY

Cash Budget

For Month Ended March 31

Beginning cash balance ………………………………………………….

$ 72,000

Cash receipts from sales ………………………………………….…….

300,000

Total cash available ………………………………………………….……

$372,000

Cash disbursements

Payments for purchases ………………………………………….…….

140,000

Salaries …………………………..…………………………………………….

80,000

Other expenses ……………………………………………………….

45,000

Repayment of bank loan ………………………………………….…….

20,000

Total cash disbursements…………………………..………………….

285,000

Ending cash balance ………………………………………………..…….

$ 87,000

Quick Study 20-25 (10 minutes)

Sales …………………………………………………………………………………………. BIS

Office salaries paid ……………………………………………………………………. BIS

Quick Study 20-26 (10 minutes)

GORDANDS

Cash Disbursements for Merchandise (Budgeted)

For Month Ended September 30

Cash disbursements for September purchases (25% x $720,000) ....

$180,000

Cash disbursements for August purchases (75% x $600,000) ………..

450,000

Total cash disbursements…………………………..……………………………....

$630,000

Quick Study 20-27 (10 minutes)

MEYER CO.

Cash Disbursements for Merchandise (Budgeted)

For January, February, and March

January

February

March

Purchases …………………………………………..…

$15,800

$18,600

$20,200

Cash disbursements for

Current month’s purchases (40%) ………

$ 6,320

$ 7,440

$ 8,080

Prior month’s purchases (60%) ……………

22,000*

9,480

11,160

Total cash disbursements for purchases ..…

$28,320

$16,920

$19,240

* Accounts payable balance at December 31

Quick Study 20-28 (5 minutes)

RAIDER-X COMPANY

Purchases Budget (in units)

For Month Ended April 30

Budgeted ending inventory (130% x 3,000) …………………………………..

3,900

Budgeted sales for April (units) …………………………………………………..

18,000

Required units of available inventory …………………………………………..

Less beginning inventory (units) …………………………..…………………....

21,900

(3,000)

Units to be purchased ………………………………………………………………...

18,900

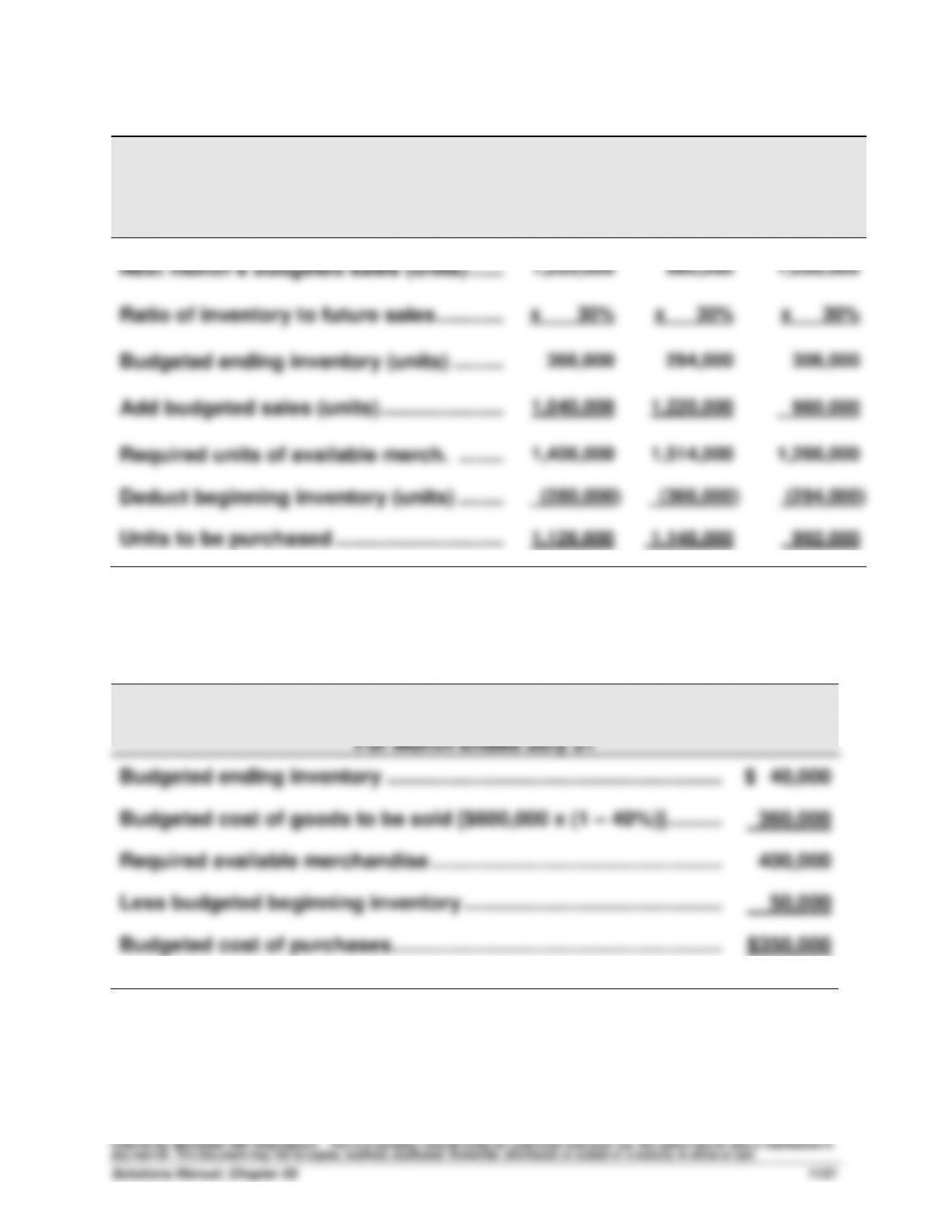

Quick Study 20-29 (15 minutes)

LEXI COMPANY

Merchandise Purchases Budget

For April, May, and June

April

May

June

Next month’s budgeted sales (units) ………

1,220,000

980,000

1,020,000

Ratio of inventory to future sales ……………

x 30%

x 30%

x 30%

Budgeted ending inventory (units) …………

366,000

294,000

306,000

Add budgeted sales (units) ………………….…

1,040,000

1,220,000

980,000

Required units of available merch. ……..…

1,406,000

1,514,000

1,286,000

Deduct beginning inventory (units) ……..…

(280,000)

(366,000)

(294,000)

Units to be purchased …………………………..

1,126,000

1,148,000

992,000

Quick Study 20-30 (15 minutes)

MONTEL COMPANY

Computation of Budgeted Cost of Purchases

For Month Ended July 31

Budgeted ending inventory ……………………………………………………….

$ 40,000

Budgeted cost of goods to be sold [$600,000 x (1 – 40%)]……….…………

360,000

Required available merchandise …………………………………………….…………

400,000

Less budgeted beginning inventory ……………………………………….…………

50,000

Budgeted cost of purchases…………………………………………………..…..

$350,000

Quick Study 20–31 (10 minutes)

1. Activity-based budgeting requires managers to focus on the activities of

2. Traditional budgeting consists of listing the amount of resources

Quick Study 20–32 (10 minutes)

1.

Sales (current year) ………………………………………………………..

(in € millions)

€25,400

Sales growth (€25,400 x 3%) ……………………………………………

762

Budgeted sales (next year) ……………………………………………..

€26,162

2.

Note: Assume budgeted sales of €26,000 for this question.

Budgeted selling expenses (€26,000 x 20%) …………………….

€5,200

Budgeted general and admin. expenses (€26,000 x 4%) …..

1,040

EXERCISES

Exercise 20-1 (5 minutes)

1. No 4. No

2. No 5. Yes

3. Yes 6. Yes

Exercise 20-2 (10 minutes)

(1) h (2) d (3) g (4) e (5) i (6) b (7) a (8) f (9) c

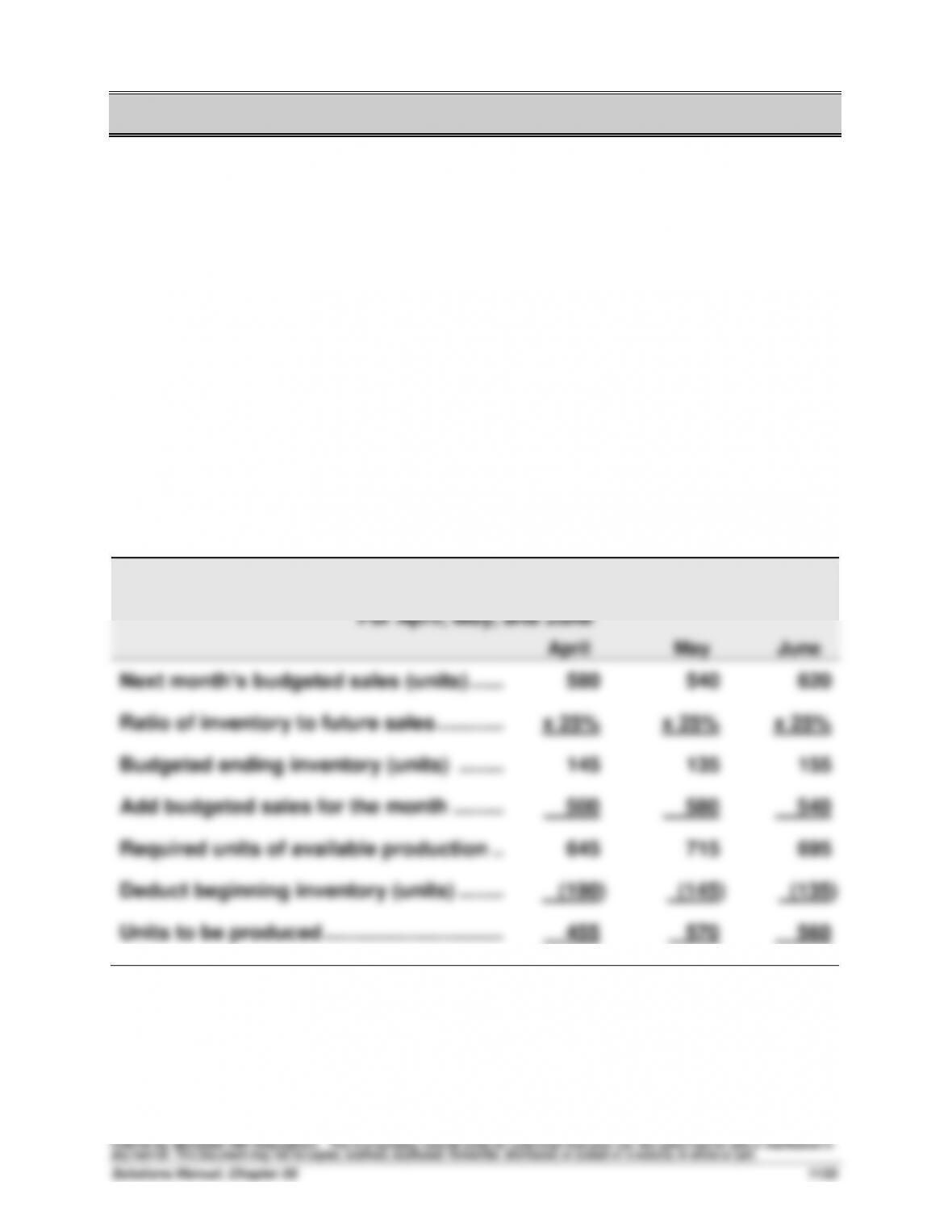

Exercise 20-3 (15 minutes)

HOSPITABLE CO.

Production Budget

For April, May, and June

April

May

June

Next month’s budgeted sales (units) ………

580

540

620

Ratio of inventory to future sales ……………

x 25%

x 25%

x 25%

Budgeted ending inventory (units) ……..…

145

135

155

Add budgeted sales for the month …………

500

580

540

Required units of available production ..…

645

715

695

Deduct beginning inventory (units) ……..…

(190)

(145)

(135)

Units to be produced …………………………..

455

570

560

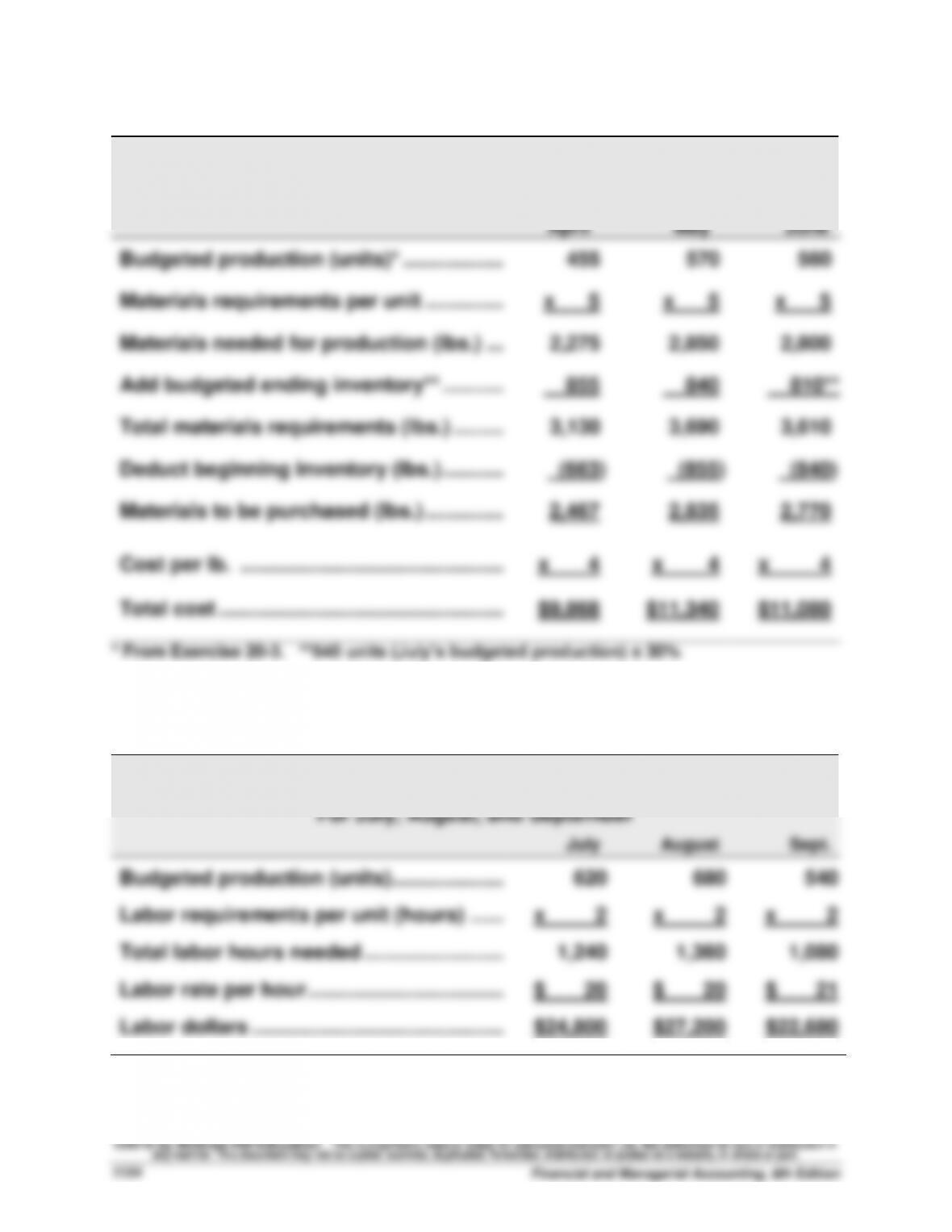

Exercise 20-4 (15 minutes)

HOSPITABLE CO.

Direct Materials Budget

For April, May, and June

April

May

June

Budgeted production (units)* …………………

455

570

560

Materials requirements per unit …………..…

x 5

x 5

x 5

Materials needed for production (lbs.) ……

2,275

2,850

2,800

Add budgeted ending inventory** ………..…

855

840

810**

Total materials requirements (lbs.) …………

3,130

3,690

3,610

Deduct beginning inventory (lbs.) ………..…

(663)

(855)

(840)

Materials to be purchased (lbs.) …………..…

2,467

2,835

2,770

Cost per lb. ………………………………………..…

Total cost ………………………………………………

x 4

$9,868

x 4

$11,340

x 4

$11,080

* From Exercise 20–3. **540 units (July’s budgeted production) x 30%

Exercise 20-5 (10 minutes)

MANNER COMPANY

Direct Labor Budget

For July, August, and September

July

August

Sept.

Budgeted production (units)………………..…

620

680

540

Labor requirements per unit (hours) ………

x 2

x 2

x 2

Total labor hours needed …………………….…

1,240

1,360

1,080

Labor rate per hour ……………………………..…

$ 20

$ 20

$ 21

Labor dollars …………………………………………

$24,800

$27,200

$22,680

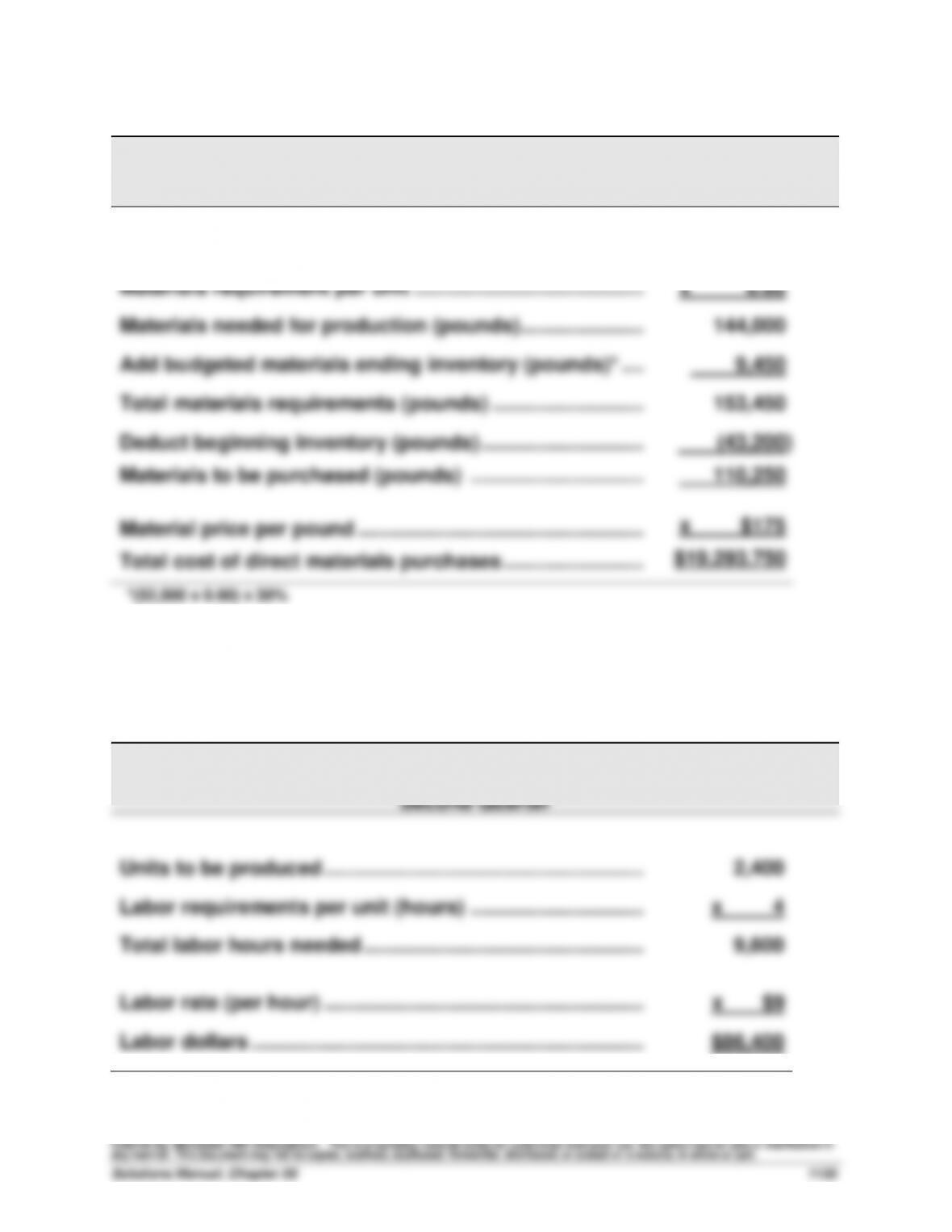

Exercise 20-6 (15 minutes)

RIDA INC.

Direct Materials Budget

Second Quarter

Units to be produced ………………………………………………………

240,000

Materials requirement per unit …………………………..……………

x 0.60

Materials needed for production (pounds) ………………….……

144,000

Add budgeted materials ending inventory (pounds)* ….……

9,450

Total materials requirements (pounds) …………………………..

153,450

Deduct beginning inventory (pounds) ………………………..…

Materials to be purchased (pounds) …………………………..

Material price per pound …………………………………………………

Total cost of direct materials purchases …………………….……

(43,200)

110,250

x $175

$19,293,750

*(52,500 x 0.60) x 30%

Exercise 20-7 (15 minutes)

1.

ADDISON CO.

Direct Labor Budget

Second Quarter

Units to be produced ………………………………………………………

2,400

Labor requirements per unit (hours) …………………………..

x 4

Total labor hours needed …………………………………………..……

9,600

Labor rate (per hour) ………………………………………………………

x $9

Labor dollars …………………………………………………………….……

$86,400

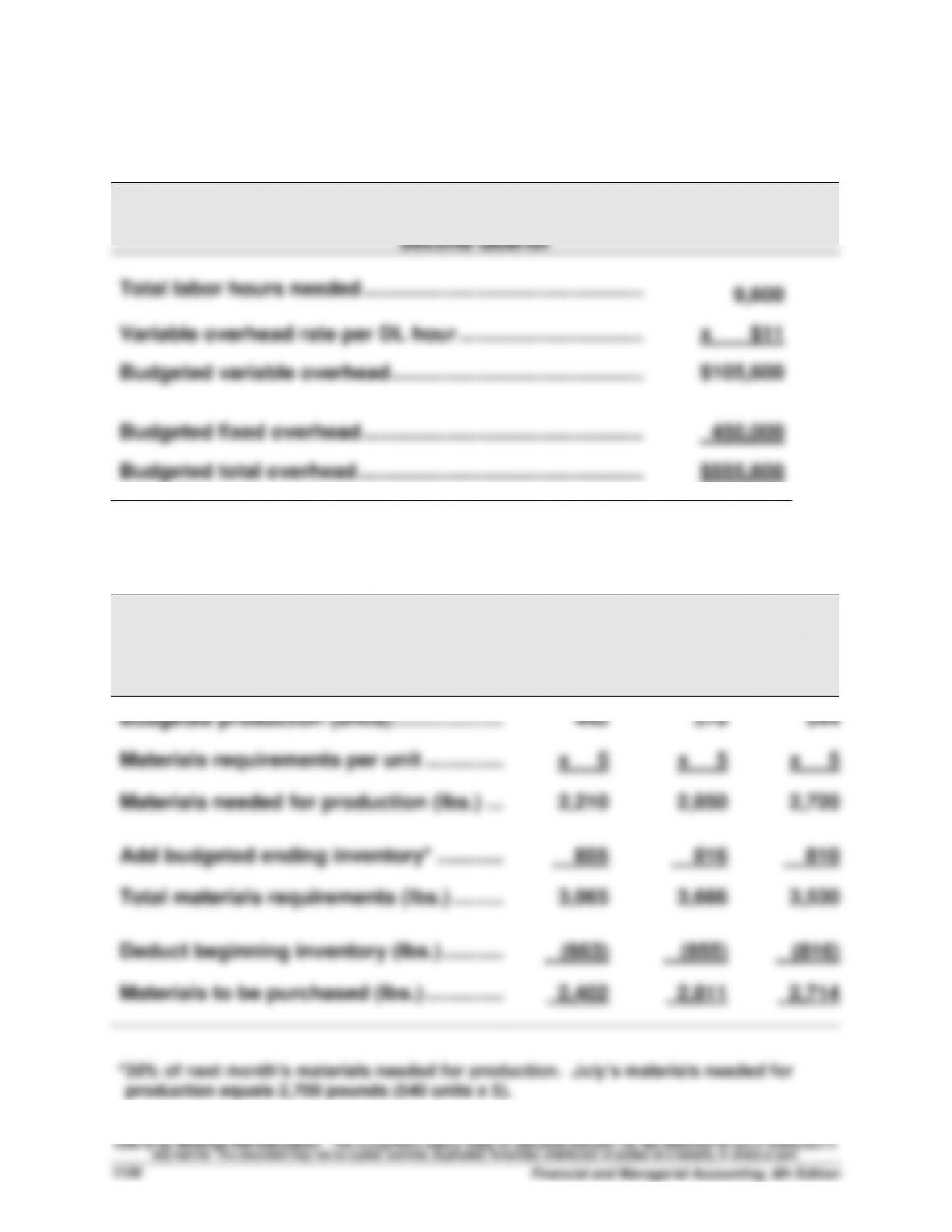

Exercise 20–7 (continued)

2.

ADDISON CO.

Factory Overhead Budget

Second Quarter

Total labor hours needed …………………………………………..……

9,600

Variable overhead rate per DL hour …………………………...……

x $11

Budgeted variable overhead …………………………..………….……

$105,600

Budgeted fixed overhead …………………………………………..……

450,000

Budgeted total overhead …………………………………………………

$555,600

Exercise 20-8 (20 minutes)

RAD CO.

Direct Materials Budget

For April, May, and June

April

May

June

Budgeted production (units)………………..…

442

570

544

Materials requirements per unit …………..…

x 5

x 5

x 5

Materials needed for production (lbs.) ……

2,210

2,850

2,720

Add budgeted ending inventory* ……………

855

816

810

Total materials requirements (lbs.) …………

3,065

3,666

3,530

Deduct beginning inventory (lbs.) ………..…

(663)

(855)

(816)

Materials to be purchased (lbs.) …………..…

2,402

2,811

2,714

*30% of next month’s materials needed for production. July’s materials needed for

production equals 2,700 pounds (540 units x 5).