Chapter Outline

1. Selling Expense Budget

a. Based on sales volume (either dollars or units depending

how rate is given)

b. Plan listing the type and amounts of selling expenses

expected during budget period.

c. Created to provide sufficient selling expenses to meet

sales goals reflected in sales budget.

2. General and Administrative Expense Budget

a. Plan showing predicted operating expenses not included in

selling expenses budget.

b. Consists of items variable or fixed in terms of sales

volume (expected units or sales dollars).

c. Interest expense and income tax expense cannot be

planned at this stage of budgeting process.

C. Capital Expenditures Budget

1. Shows estimated amounts to be received from plant asset

disposals, and estimated amounts to be spent on purchasing

additional plant assets; assumes proposed production program

is carried out.

2. Prepared after the operating budgets are prepared.

3. Shows expected investing activities in plant assets.

4. Affected by long-range plans for business instead of short–

term sales budgets.

5. Capital budgeting is process of evaluating and planning for

capital (plant and equipment) expenditures, which involve

long-run commitments of large amounts.

6. Major effect on predicted cash flows and company’s need for

debt or equity financing; often linked with company’s ability

to take on more debt.

D. Financial Budgets

1. Cash Budgetshows expected cash inflows and outflows

during budget period

Beginning cash balance

+ Budgeted cash receipts

Total available cash

– Budgeted cash disbursements

Preliminary Cash balance

+ or – Loan activity

Ending Cash Balance

a. May include planned receipts from short-term loans (if

expected preliminary cash balance is inadequate), or use

of cash to repay loans or acquire short-term investments

(if preliminary cash balance is in excess of requirements).

Notes

Chapter Outline

b. Budgeted cash receipts include:

i. Expected cash sales.

ii. Expected cash collections of accounts receivable.

iii. Other expected cash receipts such as interest revenue,

sale of assets, etc.

c. Budgeted cash disbursements include:

i. Budgeted cash disbursements from selling expense

budget and general and administrative expense

budget.

ii. Expected cash disbursements for interest expense and

income taxes.

iii. Expected cash purchases for a merchandiser.

iv. Expected direct materials, direct labor and overhead

payments (excluding depreciation) for a manufacturer.

v. Expected cash payments on accounts payable.

vi. Other expected cash payments such as owner’s

withdrawals or dividends, repayment of notes, etc.

2. Budgeted Income Statement

a. Managerial accounting report showing predicted amounts

of sales and expenses.

b. Summarizes the income effects of the budgeted activities

c. Information comes from already prepared budgets.

d. Income tax expense predicted at this level.

3. Budgeted Balance Sheet

a. Final step in preparing master budget.

b. Shows predicted amounts for assets, liabilities, and

stockholders’ equity as of end of budget period.

c. Prepared using information from other budgets (see notes

to budgeted balance sheet for sources of amounts).

E. Using the Master Budget

1. Planning: the master budget is clearly a plan for future

activities

2. Controlling: managers typically compare actual results to

budgeted results. The differences are called variances. They

examine theses variances, especially the large ones, to identify

areas for improvement and take corrective action.

Notes

Notes

Chapter Outline

III. Decision Analysis—Activity-Based Budgeting (ABB)-––budget

system based on expected activities.

A. Traditional budgets are based on figures from previous year,

adjusted for changes in operating conditions.

B. Activity-based budgeting requires management to list activities

and to understand the resources required to perform these

activities.

1. Helps management assess how much expenses will increase

with increases in activity levels.

2. Helps management reduce costs by eliminating non-value-

added activities.

Notes

IV. Appendix 20A – Merchandise Purchases Budget

A. MerchandisersSales budget used as basis for merchandise

purchases budget.

B. The merchandiser will express the purchases budge in both units

and dollars.

Expected unit sales

+ Budgeted ending inventory units

Required units of available merchandise

– Beginning inventory units

Total units to be purchased

x Budgeted cost per unit

Budgeted cost of merchandise purchases (dollars)

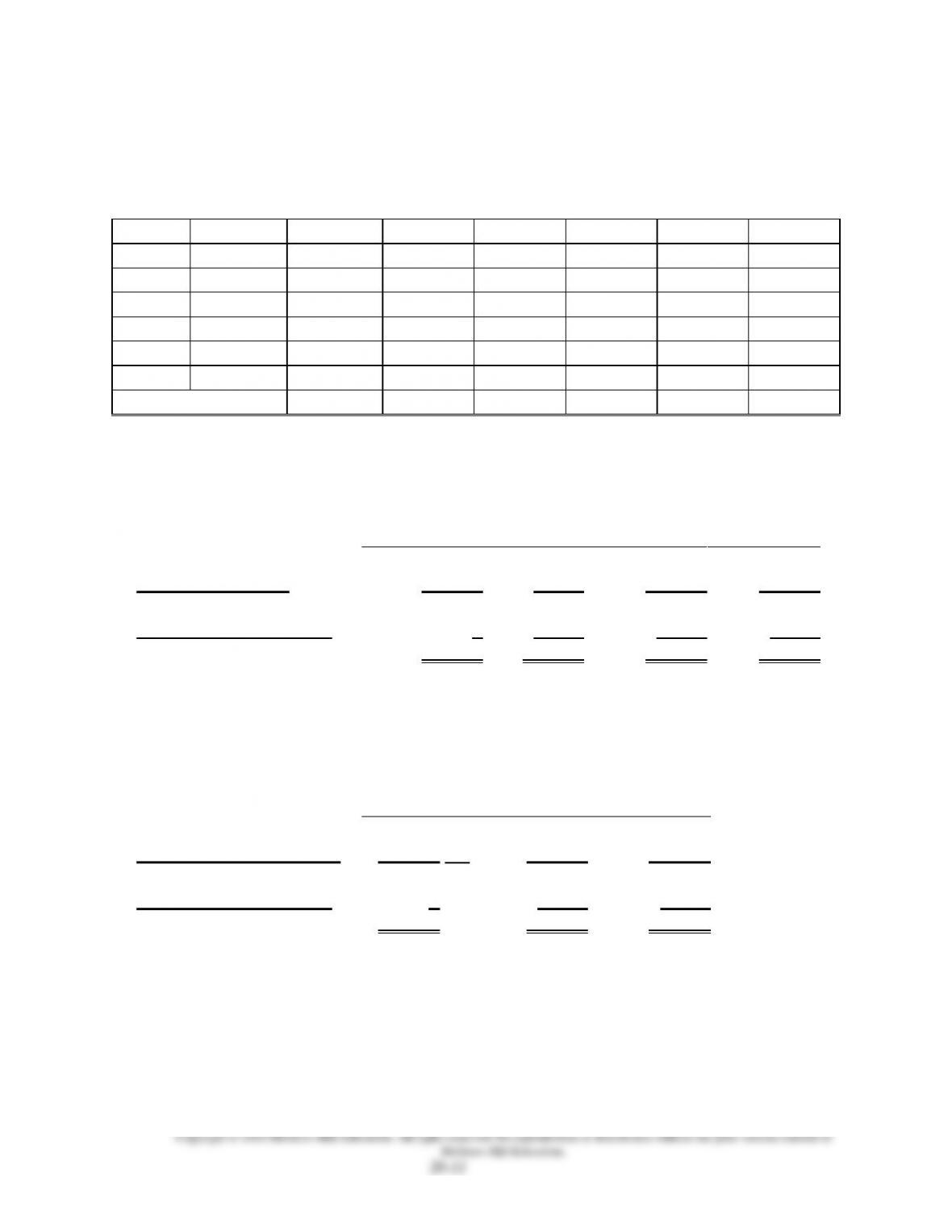

Alternate Demo Problem 20

ABC Company started business on January 1, 20xx. The company

estimated that sales for the first six months would be as follows:

Month

Units

Dollars

January

10,000

$ 50,000

February

8,000

40,000

March

15,000

75,000

April

17,000

85,000

May

22,000

110,000

June

30,000

150,000

The company sells all items on account and expects collections of

accounts receivable to be as follows: 60% in the month of the sale, and the

remaining 40% in the month after the sale.

Required:

(a) Compute the expected cash collections during the months of January,

February, March, April, May and June.

(b) The company has decided that finished goods inventory at the end of

each month should ideally be equal to 40% of next month’s sales. What

should budgeted production be for each of the first four months?

(c) It takes two pounds of raw material to make one unit of finished

product. The company wants to keep an ending inventory of raw

material equal to 30% of next month’s production needs. How many

pounds of raw material should be purchased in each of the first three

months?

(d) The raw material costs $2 per pound. The company pays for 70% of its

purchases during the month of purchase and the remainder in the

following month. How much cash will be disbursed during the month of

March for the purchase of raw material?

(e) The projected cash balance on March 1 is $13,500. What is the

estimated cash balance at the end of the month? (Prepare a formal

cash budget for the month of March.)

Solution: Alternate Demo Problem 20

(a)

Collections

Month

Sales

Jan.

Feb.

March

April

May

June

Jan.

$ 50,000

$30,000

$20,000

Feb.

40,000

24,000

$16,000

March

75,000

45,000

$30,000

April

85,000

51,000

$ 34,000

May

110,000

66,000

$ 44,000

June

150,000

90,000

Total collected

$30,000

$44,000

$61,000

$81,000

$100,000

$134,000

Note: 60% of sales collected in month of sale; 40% in the following month.

(b)

Jan.

Feb.

March

April

Ending inventory

3,200

6,000

6,800

8,800

+

Estimated sales

10,000

8,000

15,000

17,000

=

Total requirements

13,200

14,000

21,800

25,800

–

Beginning inventory

0

3,200

6,000

6,800

=

Budgeted Production

13,200

10,800

15,800

19,000

Note: Ending inventory is equal to 40% of next month’s sales (in units), and

beginning inventory is equal to last month’s ending inventory.

(c)

Jan.

Feb.

March

Ending inventory

6,480

(1)

9,480

11,400

+

Budgeted production

26,400

(2)

21,600

31,600

=

Total requirements

32,880

31,080

43,000

–

Beginning inventory

0

6,480

9,480

=

Raw material needed

32,880

24,600

33,520

Note: It takes two pounds of raw material to make one unit of product and

ending inventory should equal 30% of next month’s production.

(1) 6,480 = 10,800 units x 2 pounds x 30%

(2) 26,400 = 13,200 units x 2 pounds

(d)

Jan.

Feb.

March

Purchases (in units)

$32,880

24,600

33,520

X

Price per pound

2.00

2.00

2.00

=

Purchase cost

$65,760

$49,200

$67,040

March cash disbursement equals 70% of March purchases plus 30% of

February purchases.

Therefore, March cash disbursements equal:

Purchases from:

February

30% x $49,200

$14,760

March

70% x $67,040

+

46,928

Total cash paid for materials

$61,688

(e)

ABC COMPANY

Cash Budget

For the Month of March 20xx

Beginning cash balance

$13,500

Cash receipts from customers

61,000

Total cash available

74,500

Cash disbursements

61,688

Ending cash balance

$12,812