Exercise 2-8 (30 minutes)

Cash

Photography Equipment

Aug. 1

6,500

Aug. 2

2,100

Aug. 1

33,500

20

3,331

5

880

31

675

Common Stock

Balance

6,176

Aug. 1

40,000

Office Supplies

Photography Fees Earned

Aug. 5

880

Aug. 20

3,331

Prepaid Insurance

Utilities Expense

Aug. 2

2,100

Aug. 31

675

POSE–FOR–PICS

Trial Balance

August 31

Debit

Credit

Cash ………………………………………..…

$ 6,176

Office supplies …………………………..

880

Prepaid insurance …………………….…

2,100

Photography equipment………………

33,500

Common stock …………………………..

$40,000

Photography fees earned ………….…

3,331

Utilities expense ……………………….…

675

______

Totals …………………………………………

$43,331

$43,331

Exercise 2-9 (30 minutes)

a. Cash ………………………………………………………………… 100,750

Common Stock ………………………………………….. 100,750

Owner invested in the business for stock.

b. Office Supplies …………………………………………………. 1,250

Exercise 2-9 (concluded)

Cash

Accounts Payable

(a)

100,750

(b)

1,250

(e)

10,050

(c)

10,050

(d)

15,500

(e)

10,050

Balance

0

(h)

1,125

(g)

1,225

(i)

10,000

Balance

94,850

Common Stock

(a)

100,750

Balance

100,750

Accounts Receivable

Dividends

(f)

2,700

(h)

1,125

(i)

10,000

Balance

1,575

Balance

10,000

Office Supplies

Fees Earned

(b)

1,250

(d)

15,500

Balance

1,250

(f)

2,700

Balance

18,200

Office Equipment

Rent Expense

(c)

10,050

(g)

1,225

Balance

10,050

Balance

1,225

Exercise 2-10 (15 minutes)

SPADE COMPANY

Trial Balance

May 31, 2015

Debit

Credit

Cash ………………………………………

$ 94,850

Accounts receivable ……………….

1,575

Office supplies………………………..

1,250

Office equipment …………………….

10,050

Accounts payable……………………

$ 0

Common stock ……………………….

100,750

Dividends ……………………………….………………..

10,000

Fees earned …………………………...

18,200

Rent expense …………………………..

1,225

_______

Totals ……………………………………...

$118,950

$118,950

Exercise 2-11 (20 minutes)

Transactions that created expenses:

b. Salaries Expense………………………………….. 1,233

Cash …………………………..………………….. 1,233

Paid salary of receptionist.

Exercise 2-12 (20 minutes)

Transactions that created revenues:

b. Accounts Receivable …………………………..………. 2,300

Services Revenue …………………………..……… 2,300

Provided services on credit.

Exercise 2-13 (25 minutes)

a. Belle created a new business and invested $6,000 cash, $7,600 of

equipment, and $12,000 in automobiles in exchange for stock.

Exercise 2-14 (30 minutes)

a. Cash …………………………..……………………………………. 6,000

Equipment ……………………………………………………….. 7,600

Automobiles …………………………………………………….. 12,000

Common Stock ………………………………………….. 25,600

Exercise 2-15 (20 minutes)

Calculation of change in equity for part a through part d

Assets

–

Liabilities

=

Equity

Beginning of the year ……….

$ 60,000

–

$20,000

=

$40,000

End of the year ………………...

105,000

–

36,000

=

69,000

Net increase in equity ……….

$29,000

a. Net income …………………………..……………………..

$ ?

Plus owner investments ………………………………

0

Less dividends …………………………………………..

(0)

Change in equity …………………………………………

$29,000

Net Income = $29,000

Since there were no additional investments or dividends, the net

income for the year equals the net increase in equity.

b. Net income …………………………..……………………..

$ ?

Plus owner investments ………………………………

0

Less dividends ($1,250/mo. x 12 mo.) …………..

(15,000)

Change in equity …………………………………………

$29,000

Net Income = $44,000

The dividends were added back because they reduced equity

without reducing net income.

c. Net income …………………………..……………………..

$ ?

Plus owner investment ………………………………..

55,000

Less dividends ……………………………………………

(0)

Change in equity …………………………………………

$29,000

Net Loss = $26,000

The investment was deducted because it increased equity without

creating net income.

d. Net income …………………………..……………………..

$ ?

Plus owner investment ………………………………..

35,000

Less dividends ($1,250/mo. X 12 mo.) …………..

(15,000)

Change in equity …………………………………………

$29,000

Net Income = $9,000

The dividends were added back because they reduced equity

without reducing net income and the investments were deducted

because they increased equity without creating net income.

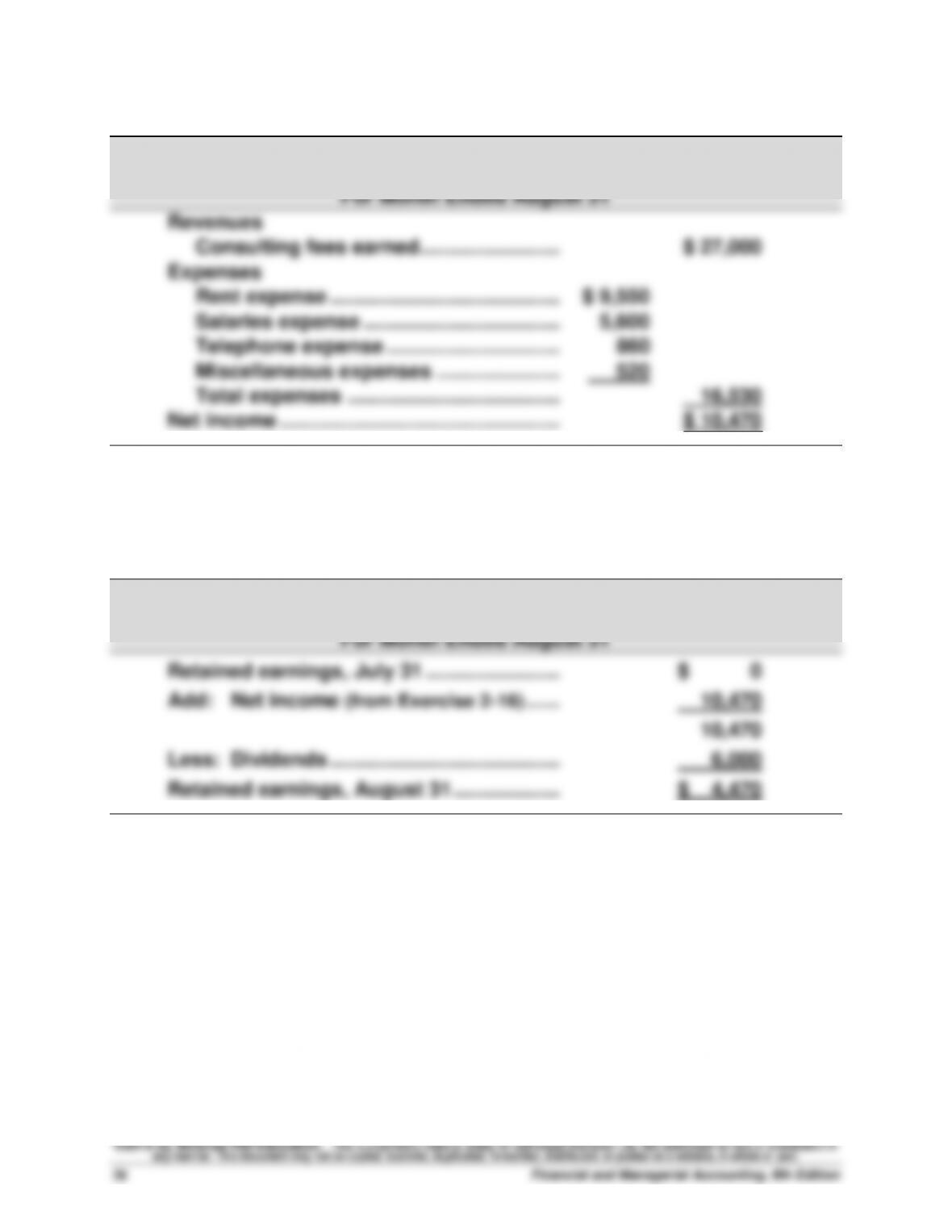

Exercise 2-16 (15 minutes)

HELP TODAY

Income Statement

Exercise 2-17 (15 minutes)

HELP TODAY

Statement of Retained Earnings

Exercise 2-18 (15 minutes)

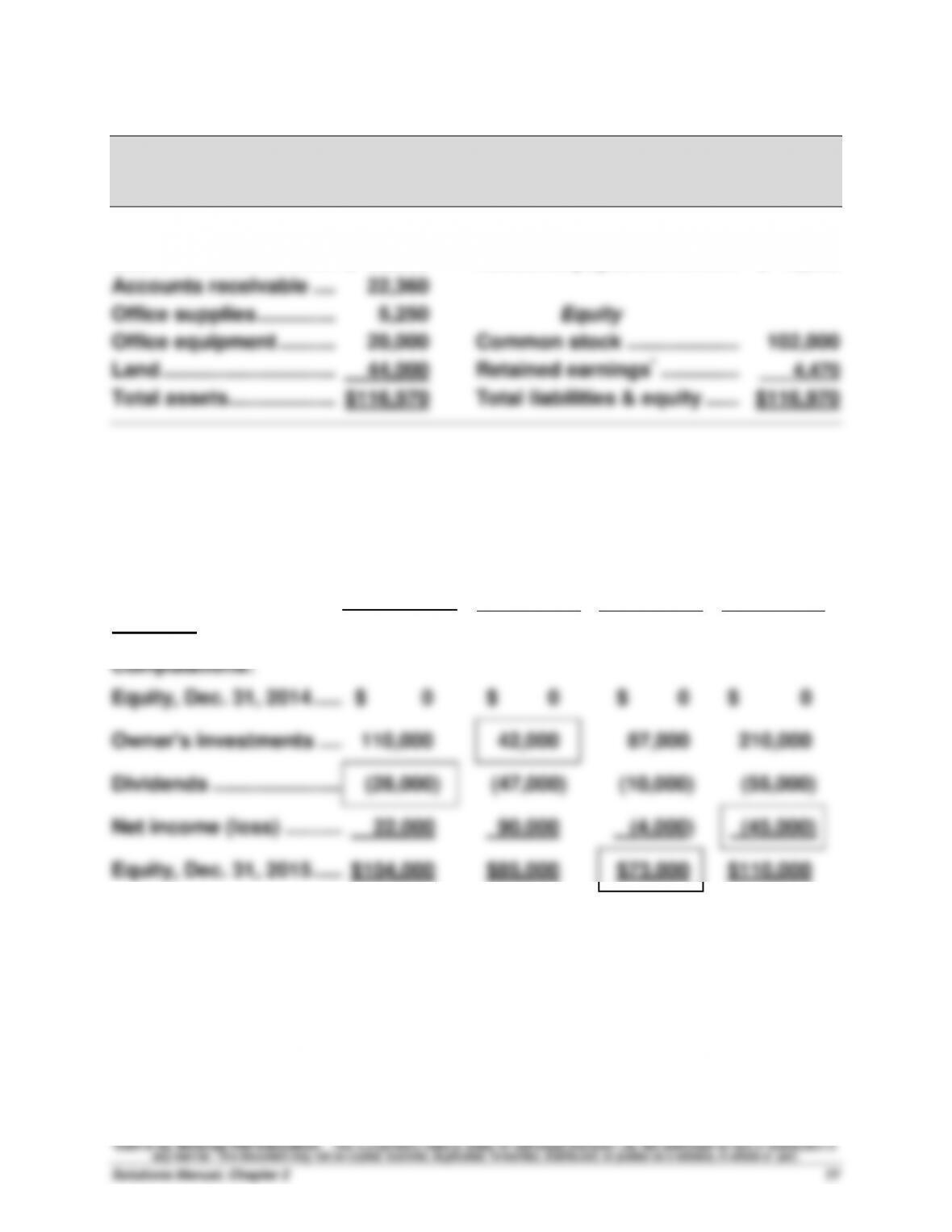

HELP TODAY

Balance Sheet

August 31

Assets Liabilities

Cash …………………………. $ 25,360 Accounts payable ……………. $ 10,500

* Amount from Exercise 2-17.

Exercise 2-19 (15 minutes)

(a)

(b)

(c)

(d)

Answers

$(28,000)

$42,000

$73,000

$(45,000)

Computations:

Equity, Dec. 31, 2014 …………..

$ 0

$ 0

$ 0

$ 0

Owner’s investments …..……..

110,000

42,000

87,000

210,000

Dividends …………………………..

(28,000)

(47,000)

(10,000)

(55,000)

Net income (loss) ………..……..

22,000

90,000

(4,000)

(45,000)

Equity, Dec. 31, 2015 …………..

$104,000

$85,000

$73,000

$110,000

Exercise 2-20 (20 minutes)

Description

(1)

Difference

between

Debit and

Credit

Columns

(2)

Column

with the

Larger

Total

(3)

Identify

account(s)

incorrectly

stated

(4)

Amount that account(s)

is overstated or

understated

a.

$3,600 debit to Rent

Expense is posted as

a $1,340 debit.

$2,260

Credit

Rent Expense

Rent Expense is

understated by $2,260

b.

$6,500 credit to Cash

is posted twice as two

credits to Cash.

$6,500

Credit

Cash

Cash is understated by

$6,500

c.

$10,900 debit to the

Dividends account is

debited to Common

Stock

$0

––

Common

Stock

Dividends

Common Stock is

understated by $10,900

Dividends is

understated by $10,900

d.

$2,050 debit to

Prepaid Insurance is

posted as a debit to

Insurance Expense.

$0

––

Prepaid

Insurance

Insurance

Expense

Prepaid Insurance is

understated by $2,050

Insurance Expense is

overstated by $2,050

e.

$38,000 debit to

Machinery is posted

as a debit to Accounts

Payable.

$0

––

Machinery

Accounts

Payable

Machinery is

understated by $38,000

Accounts Payable is

understated by $38,000

f.

$5,850 credit to

Services Revenue is

posted as a $585

credit.

$5,265

Debit

Services

Revenue

Services Revenue is

understated by $5,265

g.

$1,390 debit to Store

Supplies is not

posted.

$1,390

Credit

Store

Supplies

Store Supplies is

understated by $1,390