EXERCISES

Exercise 19-1 (15 minutes)

Part 1

Cost per unit of finished goods using absorption costing:

Direct materials ……………………………………………………………………….

$15 per unit

Direct labor ………………………………………………………………………….….

16 per unit

Variable overhead ($80,000/20,000 units) ………………………………….

4 per unit

Fixed overhead ($160,000/20,000 units) …………………………………….

8 per unit

Total cost per unit ………………………………………………………………..….

$43 per unit

Exercise 19-2 (15 minutes)

Part 1

Cost per unit of finished goods using variable costing:

Direct materials ……………………………………………………………………….

$15 per unit

Direct labor ………………………………………………………………………….….

16 per unit

Variable overhead ($80,000/20,000 units) ………………………………….

4 per unit

Total cost per unit ………………………………………………………………..….

$35 per unit

Exercise 19–2 (continued)

Part 2

Cost of ending finished goods inventory using variable costing:

Exercise 19-3 (25 minutes)

Part 1

SIMS COMPANY

Variable Costing Income Statement

Sales (70,000 units x $350/unit) …………………………..

$24,500,000

Variable expenses

Var. manuf. expense (70,000 units x 130/unit*) …..…….

$9,100,000

Var. selling and administrative expense ………………….

770,000

Total variable expenses ………………………………………….

9,870,000

Contribution margin …………………………..…………………….

14,630,000

Fixed expenses

Fixed manufacturing expenses …………………………..

7,000,000

Fixed selling and administrative expenses ………..…….

4,250,000

Total fixed expenses…………………………..…………….…….

11,250,000

Net income ……………………………………………………………….

$ 3,380,000

* Direct materials ………………….……….

$ 40 per unit

Direct labor ……………………….….

60 per unit

Variable overhead ………………..…………

30 per unit

Total variable manuf. cost …………………..

$130 per unit

Exercise 19–3 (continued)

Part 2

SIMS COMPANY

Absorption Costing Income Statement

Sales (70,000 units x $350 per unit) ……………………………………….…

$24,500,000

Cost of goods sold (70,000 units x $200 per unit*) ………………….…

14,000,000

Gross profit ………………………………………………………………………….…

10,500,000

Selling and administrative costs ($770,000 + $4,250,000) ……….…

5,020,000

Net income ………………………………………………………………………………

$ 5,480,000

*Direct materials ………………………………………………

$ 40 per unit

Direct labor …………………………………………………….

60 per unit

Variable overhead ($3,000,000/100,000 units) …….

30 per unit

Fixed overhead ($7,000,000/100,000 units) …………

70 per unit

Total absorption cost per unit …………………………..

$200 per unit

Part 3

Absorption costing and variable costing income will be identical if production

equals sales and there is no beginning finished goods inventory.

Exercise 19-4 (15 minutes)

Part 1

KENZI KAYAKING

Variable Costing Income Statement

Sales (800 x $1,050) ……………………………………………….

$840,000

Variable expenses

Variable production costs (800 x $400) ………………..

$320,000

Variable selling and administrative expenses ……...

75,000

Total variable expenses ……………………………………...

395,000

Contribution margin …………………………..………………….

445,000

Fixed expenses

Fixed manufacturing costs ………………………………….

105,000

Fixed selling and administrative expenses …………..

155,000

Total fixed expenses…………………………..……………….

260,000

Net income …………………………………………………………….

$185,000

Exercise 19–4 (continued)

Part 2

The absorption costing income is $25,000 higher than the variable costing

Exercise 19-5 (25 minutes)

a)

REY COMPANY

Absorption Costing Income Statement

Sales (20,000 units x $216 per unit) ……………………………………….…

$4,320,000

Cost of goods sold (20,000 units x $62 per unit*) ………………………

1,240,000

Gross margin ………………………………………………………………………..…

3,080,000

Selling and administrative costs [$200,000 + (20,000 x $18)] …..…

560,000

Net income ………………………………………………………………………………

$2,520,000

*Direct materials ………………………………………………

$ 20 per unit

Direct labor …………………………………………………….

28 per unit

Variable overhead ……………………………………………

6 per unit

Fixed overhead ($160,000/20,000 units) ……………..

8 per unit

Total absorption cost per unit …………………………..

$62 per unit

b)

REY COMPANY

Variable Costing Income Statement

Sales (20,000 units x $216/unit) …………………………..

$4,320,000

Variable expenses

Var. manuf. expense (20,000 units x $54/unit*) …..…….

$1,080,000

Var. selling and administrative expense ………………….

360,000

Total variable expenses ………………………………………….

1,440,000

Contribution margin …………………………..…………………….

2,880,000

Fixed expenses

Fixed overhead ……………………………………………………….

160,000

Fixed selling and administrative expenses ………..…….

200,000

Total fixed expenses…………………………..…………….…….

360,000

Net income ……………………………………………………………….

$2,520,000

* Direct materials ………………….……….

$ 20 per unit

Direct labor ……………………….….

28 per unit

Variable overhead ………………..…………

6 per unit

Total variable manuf. cost …………………..

$54 per unit

Exercise 19-6 (15 minutes)

Part 1

HAYEK BIKES

Absorption Costing Income Statement

Sales (225 units x $1,600 per unit) …………………………………………..………..

$360,000

Cost of goods sold (225 units x $775 per unit*) ………………………..…

174,375

Gross profit ……………………………………………………………………………………

185,625

Selling and administrative expense ($14,625 + $75,000) …………..………..

89,625

Net income ……………………………………………………………………………..…….

$ 96,000

* Production cost per unit:

Variable production costs …………………………..….….

$625

Fixed overhead ($56,250 / 375 units) ………………..….

150

Total production costs ……………………………………….

$775

Part 2

The absorption costing income is $22,500 ($96,000 – $73,500) higher than

the variable costing income. This difference is equal to 150 units in ending

inventory that each have $150 ($56,250 fixed overhead ÷ 375 units

produced) of fixed overhead attached to them; variable costing expenses

this cost.

Exercise 19-7 (25 minutes)

Part 1

OAK MART COMPANY

Variable Costing Income Statement

Sales (118,000 units x $320 per unit) ………………..…….

$37,760,000

Variable expenses

Variable production costs* …………………………….…….

$15,355,000

Variable selling and administrative expenses ……….

1,416,000

Total variable expenses ……………………………………….

16,771,000

Contribution margin …………………………..………………….

20,989,000

Fixed expenses

Fixed manufacturing costs …………………………….…….

7,400,000

Fixed selling and administrative expenses ……..…….

4,600,000

Total fixed expenses…………………………..………….…….

12,000,000

Net income ……………………………………………………….

$ 8,989,000

*Beginning variable finished goods ……………………….

$ 405,000

Variable cost of goods manufactured

Direct materials ($40 x 115,000) …………………..………

4,600,000

Direct labor ($62 x 115,000) …………………………..

7,130,000

Variable overhead ……………………………………………….

3,220,000

Total variable costs available …………………………..

15,355,000

Less ending finished goods ………………………..…

0

Variable production costs of goods sold ……..……….

$15,355,000

Exercise 19-7 (concluded)

Part 2

OAK MART COMPANY

Absorption Costing Income Statement

Sales (118,000 units x $320 per unit) ………………..…….

$37,760,000

Cost of goods sold

Beginning finished goods …………………………………….

$ 645,000

Cost of goods manufactured *………………………..…

22,350,000

Goods available for sale…………………………..…….…….

22,995,000

Less ending finished goods **………………………..…

0

Cost of goods sold …………………………..………………….

22,995,000

Gross margin …………………………………………………..…..

14,765,000

Selling and administrative expenses *** ………………….

6,016,000

Net income ……………………………………………………….

$ 8,749,000

* Direct materials ($40 x 115,000) ………

$ 4,600,000

Direct labor ($62 x 115,000)…………….

7,130,000

Variable overhead ………………………….

3,220,000

Fixed overhead ……………………………..

7,400,000

Total manufacturing costs ……………..

$22,350,000

**Beginning finished goods inventory .

3,000 units

Add units produced ……………………….

115,000 units

Less units sold ……………………………..

(118,000 units)

Ending finished goods inventory ……

0 units

***$1,416,000 + $4,600,000 = $6,016,000

Exercise 19-8 (20 minutes)

Part 1

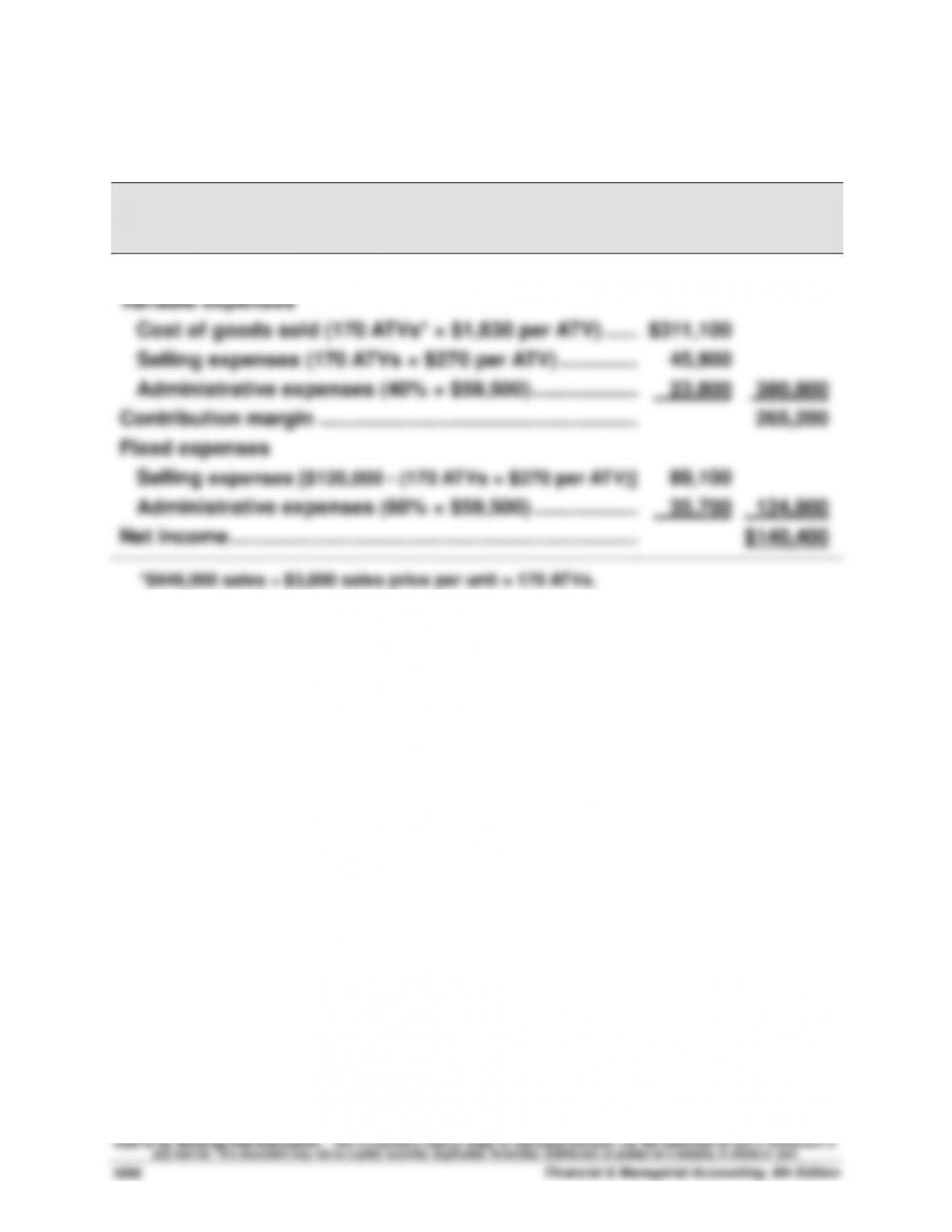

POLARIX

Income Statement—Consumer ATV Department

For Year Ended December 31, 2015

Sales ………………………………………………………………………………

$646,000

Variable expenses

Cost of goods sold (170 ATVs* × $1,830 per ATV) …….……

$311,100

Selling expenses (170 ATVs × $270 per ATV) …………………

45,900

Administrative expenses (40% × $59,500) ………………..……

23,800

380,800

Contribution margin …………………………..……………………..……

265,200

Fixed expenses

Selling expenses [$135,000 – (170 ATVs × $270 per ATV)]

89,100

Administrative expenses (60% × $59,500) ………………..……

35,700

124,800

Net income ………………………………………………………………..……

$140,400

*$646,000 sales ÷ $3,800 sales price per unit = 170 ATVs.

Exercise 19–8 (concluded)

Part 2

The company sold 170 ATVs and its contribution margin totals $265,200 for

the year. Consequently, the contribution of each ATV toward covering fixed

Exercise 19–9 (concluded)

b.

COOL SKY

Absorption Costing Income Statement

Sales (36,000 units x $140 per unit) ……………………………………….….

$5,040,000

Cost of goods sold (36,000 units x $102 per unit) ………………….….

3,672,000

Gross profit ………………………………………………………………………….….

1,368,000

Selling and administrative expenses* ……………………………………….

501,000

Net income …………………………………………………………………………..….

$ 867,000

*Variable ($11 x 36,000) …………………………..………..

$396,000

Fixed……………………………………………………………..

105,000

Total ……………………………………………………………..

$501,000

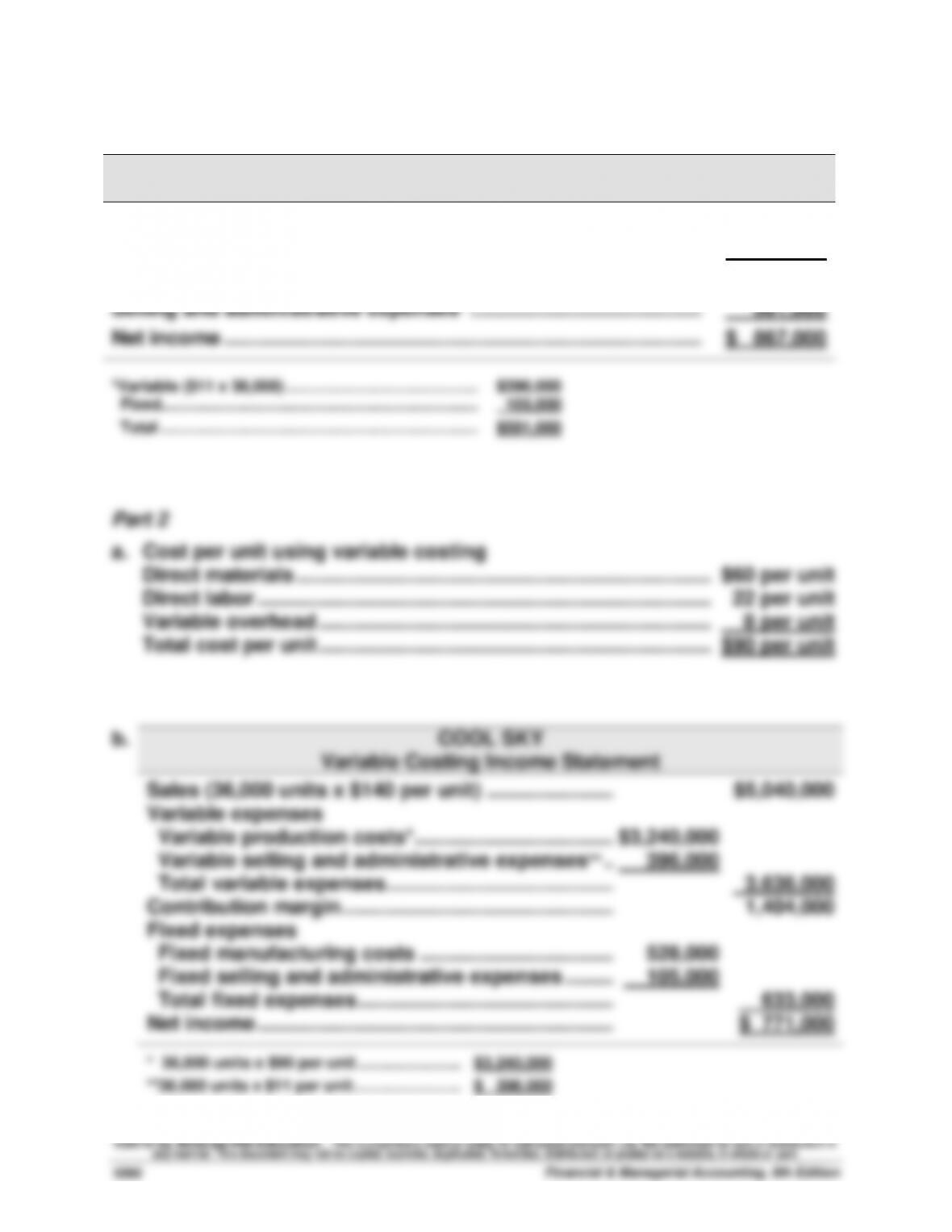

Part 2

a. Cost per unit using variable costing

Direct materials ………………………………………………………………..……..

$60 per unit

Direct labor ……………………………………………………………………………..

22 per unit

Variable overhead ……………………………………………………….…………..

8 per unit

Total cost per unit …………………………..………………………………..……..

$90 per unit

b.

COOL SKY

Variable Costing Income Statement

Sales (36,000 units x $140 per unit) …………………..……

$5,040,000

Variable expenses

Variable production costs*……………………………………

$3,240,000

Variable selling and administrative expenses** ..……

396,000

Total variable expenses…………………………………..……

3,636,000

Contribution margin ………………………………………….……

1,404,000

Fixed expenses

Fixed manufacturing costs ……………………………..……

528,000

Fixed selling and administrative expenses ……………

105,000

Total fixed expenses ……………………………………….……

633,000

Net income …………………………..…………………………..

$ 771,000

* 36,000 units x $90 per unit …………………..

$3,240,000

**36,000 units x $11 per unit ……………………

$ 396,000