Problem 18-7A (50 minutes)

Part 1 BREAK–EVEN ANALYSIS ASSUMING USE OF SAME MATERIALS

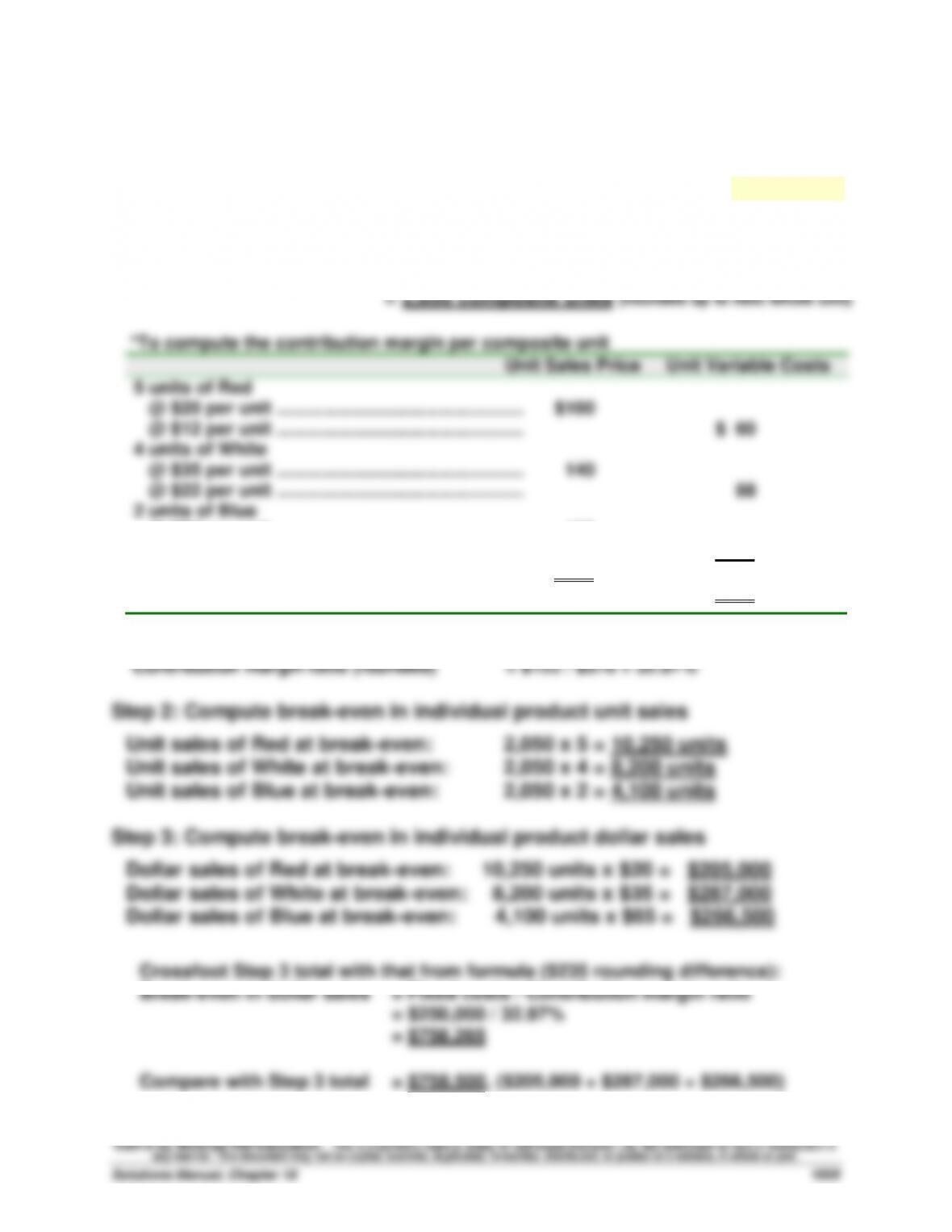

Step 1: Compute break-even in composite units—Use equation in Exhibit 18.29

Break-even in composite units = Fixed costs/Contribution margin per composite unit

= $250,000 / $122*

Problem 18–7A (Continued)

Part 2 BREAK–EVEN ANALYSIS ASSUMING USE OF NEW MATERIALS

Step 1: Compute break-even in composite units—Use equation in Exhibit 18.29

Break-even in composite units = Fixed costs/Contribution margin per composite unit

= ($250,000 + $50,000) / $220*

Problem 18-1B (25 minutes)

Parts 1 and 2

Gilmore Company

Contribution Margin Income Statement

For Year Ended December 31, 2015

(12,000 units) Per unit % of sales

Sales ($18 x 12,000) ………………….…….

$216,000

$18.000

100.00%

Variable costs

Plastic for CD sets ………………….…….

$ 1,500

$0.125

Assembly worker wages …………..…….

30,000

2.500

Labeling………………………………..…….

3,000

0.250

Sales commissions ………………..…….

6,000

40,500

0.500

3.375

18.75%

Contribution margin ……………………….

175,500

$14.625

81.25%

Fixed costs

Rent on factory ………………………..…

6,750

Factory cleaning service …………..…….

4,520

Factory mach. depreciation …………….

20,000

Office equipment lease …………….…….

1,050

System staff salaries ………………..…….

15,000

Admin. mgmt. salaries ……………..…….

120,000

167,320

Pretax income ………………………………….

8,180

Income tax (25%) ……………………….….

2,045

Net income ………………………………..…….

$ 6,135

The contribution margin per unit is $14.625, and the contribution margin ratio is

81.25%.

Part 3 Analysis Component

Contribution margin shows how much of total sales are available to cover

Problem 18-2B (45 minutes)

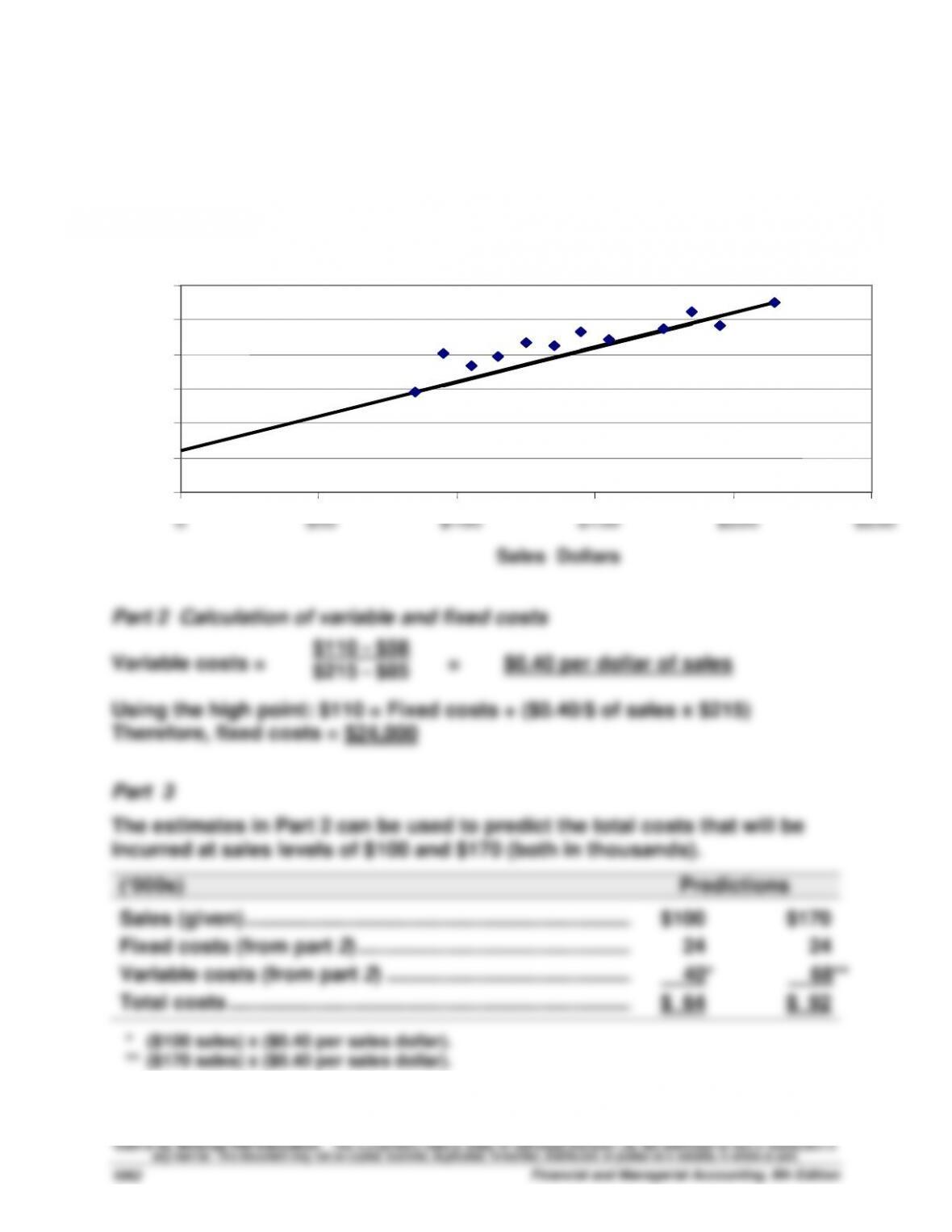

Parts 1 and 2

The scatter diagram and its estimated line of cost behavior appear below.

Sales and cost amounts are in thousands of dollars.

Sun Company

0

20

40

60

80

100

$120

0

$50

$100

$150

$200

$250

Sales Dollars

Total

Costs

Problem 18-3B (40 minutes)

Part 1

(a) Instructor note: Use the equation in Exhibit 18.11

Break-even in unit sales = Fixed costs / Contribution margin per unit

Problem 18-3B (Continued)

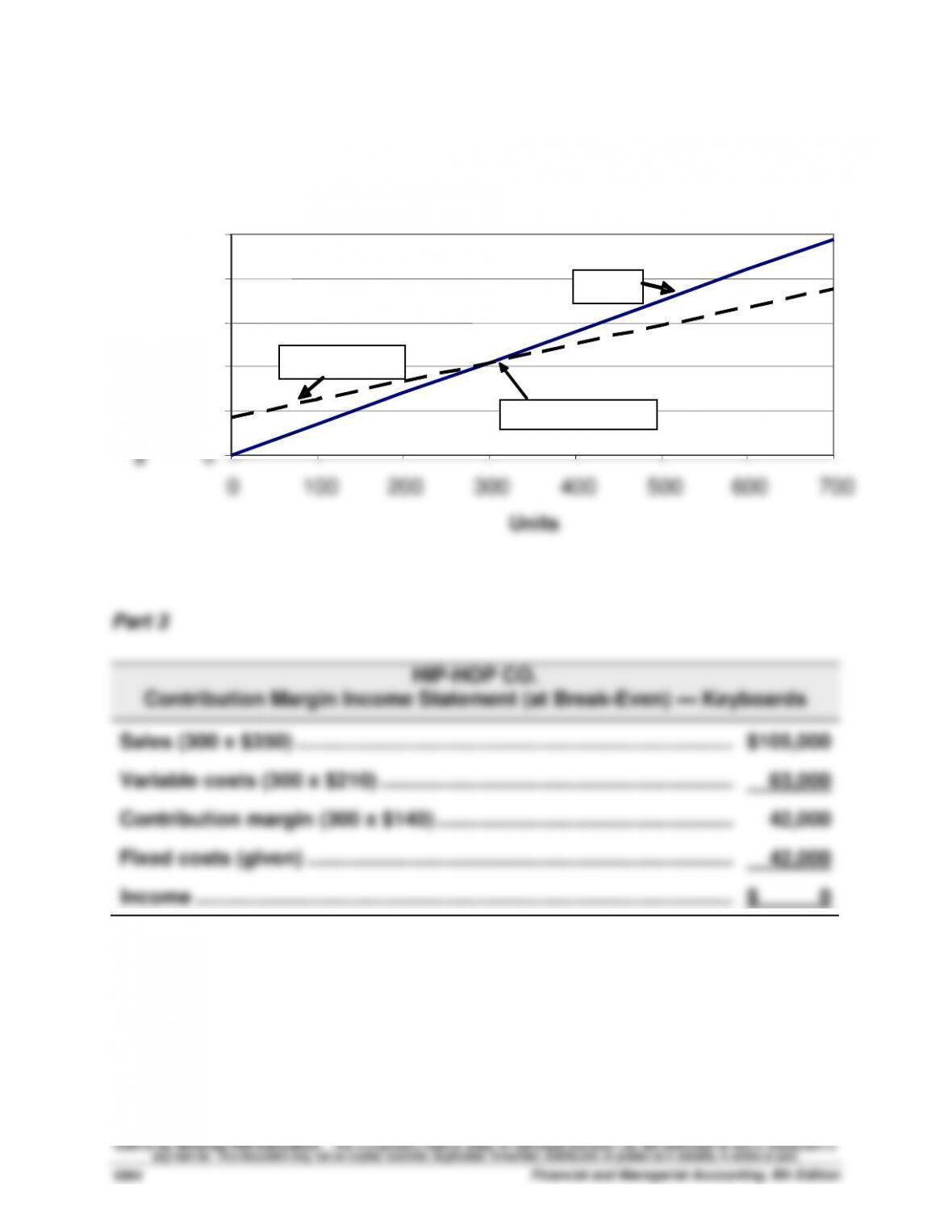

Part 2

Hip-Hop Company CVP chart

$ 0

$50,000

$100,000

$150,000

$200,000

$250,000

0

100

200

300

400

500

600

700

Units

Sales

Total Costs

Breakeven point

Problem 18-4B (75 minutes)

Part 1 Instructor note: Use the equation in Exhibit 18.12

2015 break-even in dollar sales = Fixed costs / Contribution margin ratio

= $200,000 / 20%*

= $1,000,000

Problem 18–4B (Continued)

Part 4 Instructor note: Use equations in Exhibit 18.22 and 18.23 with predicted

numbers

(Fixed costs + Pretax income)

Required sales in dollars = Contribution margin ratio

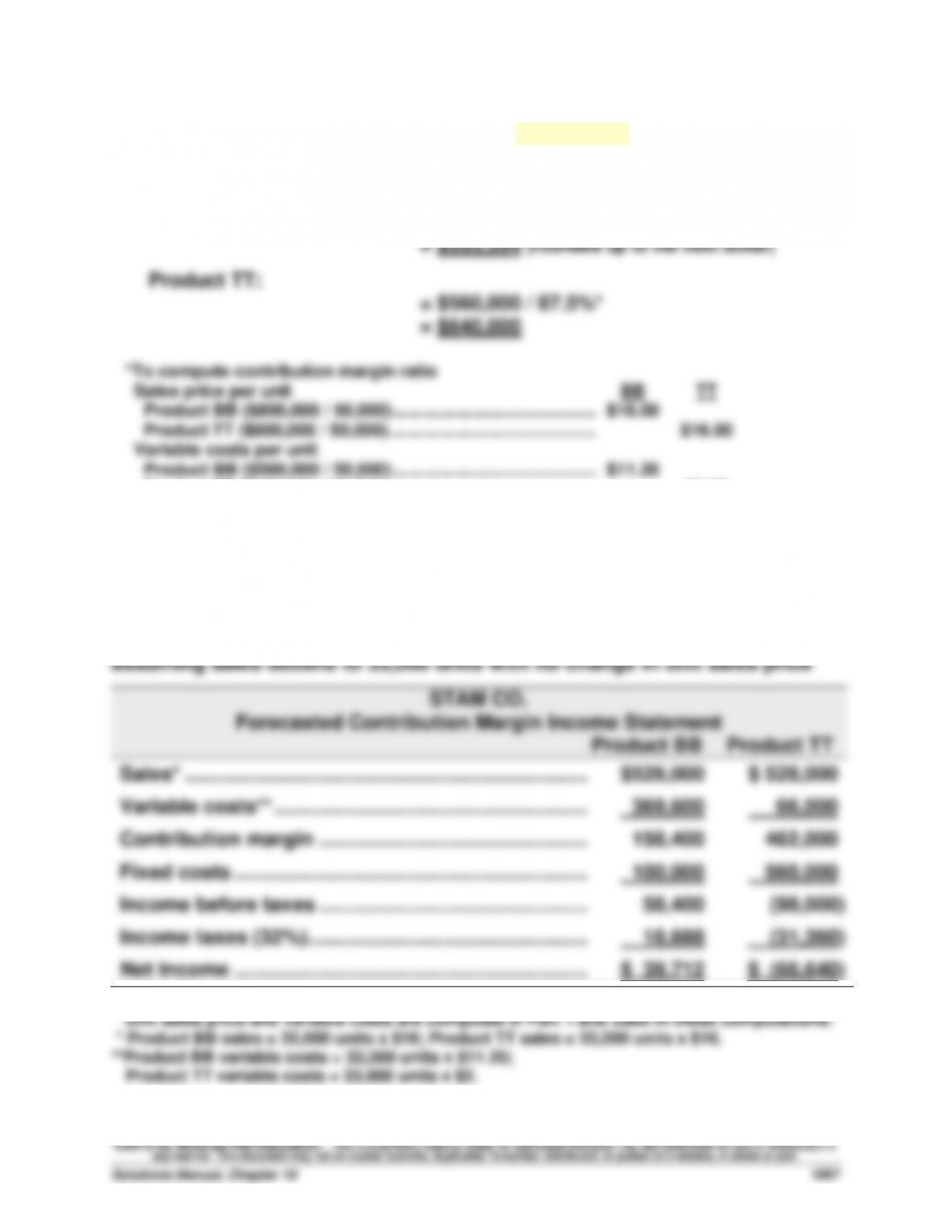

Problem 18-5B (65 minutes)

Part 1 Instructor note: Use the equation in Exhibit 18.12

Break-even in dollar sales = Fixed costs / Contribution margin ratio

Product BB:

= $100,000 / 30%*

Sales price per unit

Product BB ($800,000 / 50,000) …………………………..……….………………….

Product TT ($800,000 / 50,000)…………………………………….…………………

BB

$16.00

TT

$16.00

Variable costs per unit

Product BB ($560,000 / 50,000) …………………………..……….………………….

Product TT ($100,000 / 50,000)…………………………………….…………………

$11.20

$2.00

Contribution margin ratio

Product BB ($16.00 – $11.20) / $16.00) …………………………..

Product TT ($16 – $2) / $16) ……………………………………………………….

30.0%

87.5%

Part 2

Forecasted contribution margin income statements for each product

Problem 18–5B (Continued)

Forecasted contribution margin income statements for each product

assuming sales increase to 64,000 units with no change in unit sales price:

STAM CO.

Forecasted Contribution Margin Income Statement

Product BB

Product TT

Sales* ……………………………………………………….……..…

$1,024,000

$1,024,000

Variable costs** ………………………………………………..…

716,800

128,000

Contribution margin ……………………………………………

307,200

896,000

Fixed costs ……………………………………………………….

100,000

560,000

Income before taxes ……………………………………………

207,200

336,000

Income taxes (32%)…………………………………………..…

66,304

107,520

Net income ……………………………………………………….

$ 140,896

$ 228,480

Unit sales price and variable costs are computed in Part 1 and used in these computations:

* Product BB sales = 64,000 units x $16; Product TT sales = 64,000 units x $16.

**Product BB variable costs = 64,000 units x $11.20;

Product TT variable costs = 64,000 units x $2.

Part 4

If sales were to greatly increase, Product TT would experience the greater

increase in income because it would gain more contribution margin per

unit than Product BB ($14 for TT versus $4.80 for BB). Examining the

operating leverage of these two products would yield the same inference.