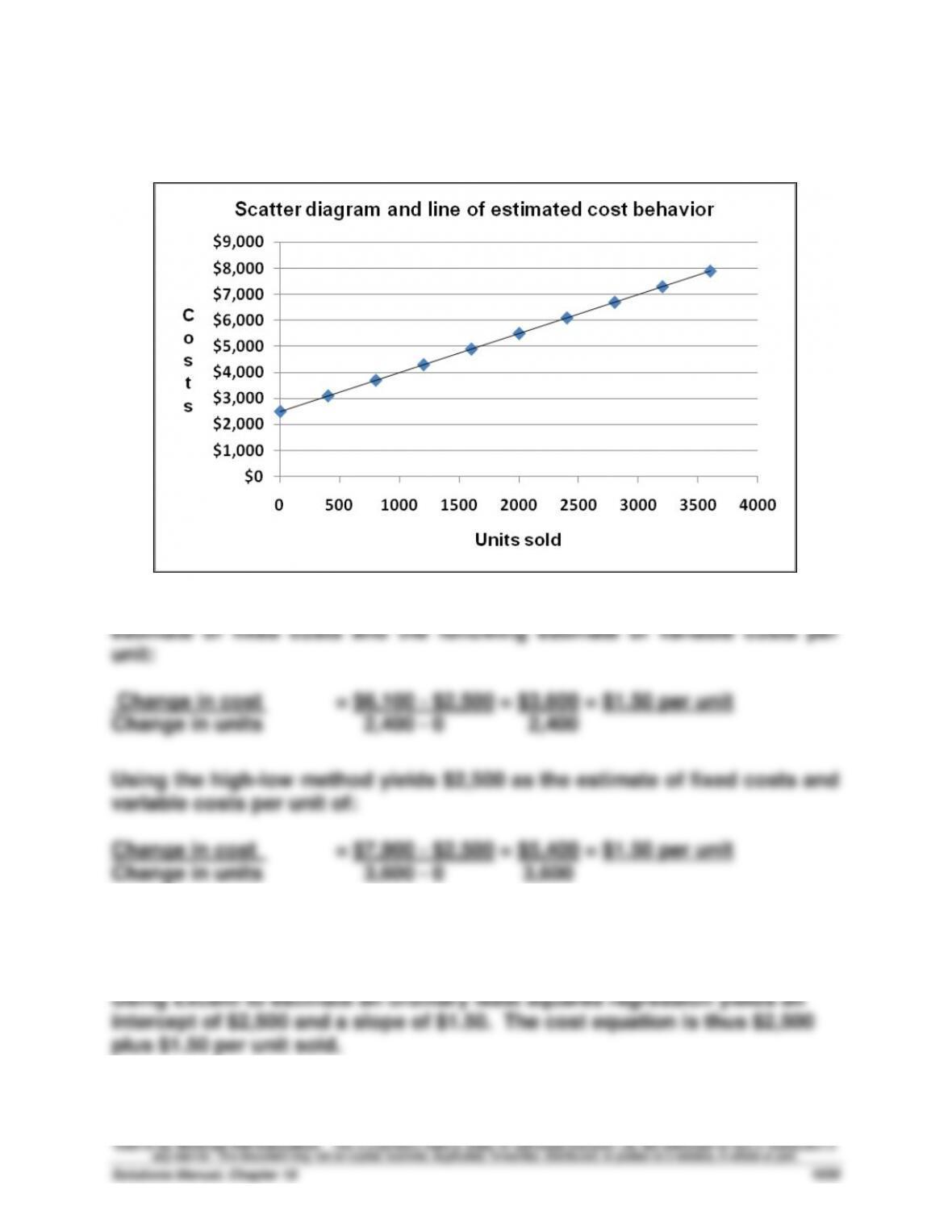

Exercise 18-6 (20 minutes)

The scatter diagram and line of estimated cost behavior appear below.

Selecting 0 and 2,400 units sold as the activity levels yields $2,500 as the

Exercise 18-7A (20 minutes)

Exercise 18-8 (10 minutes)

(1) Contribution margin = Selling price – Variable costs

(2) Contribution margin ratio = Contribution margin = $41 = 20%

(3) The contribution margin of 20% implies that for each $1 in sales, the

Exercise 18-9 (30 minutes)

(a) Contribution margin per unit = $180 – $135 = $45 per unit

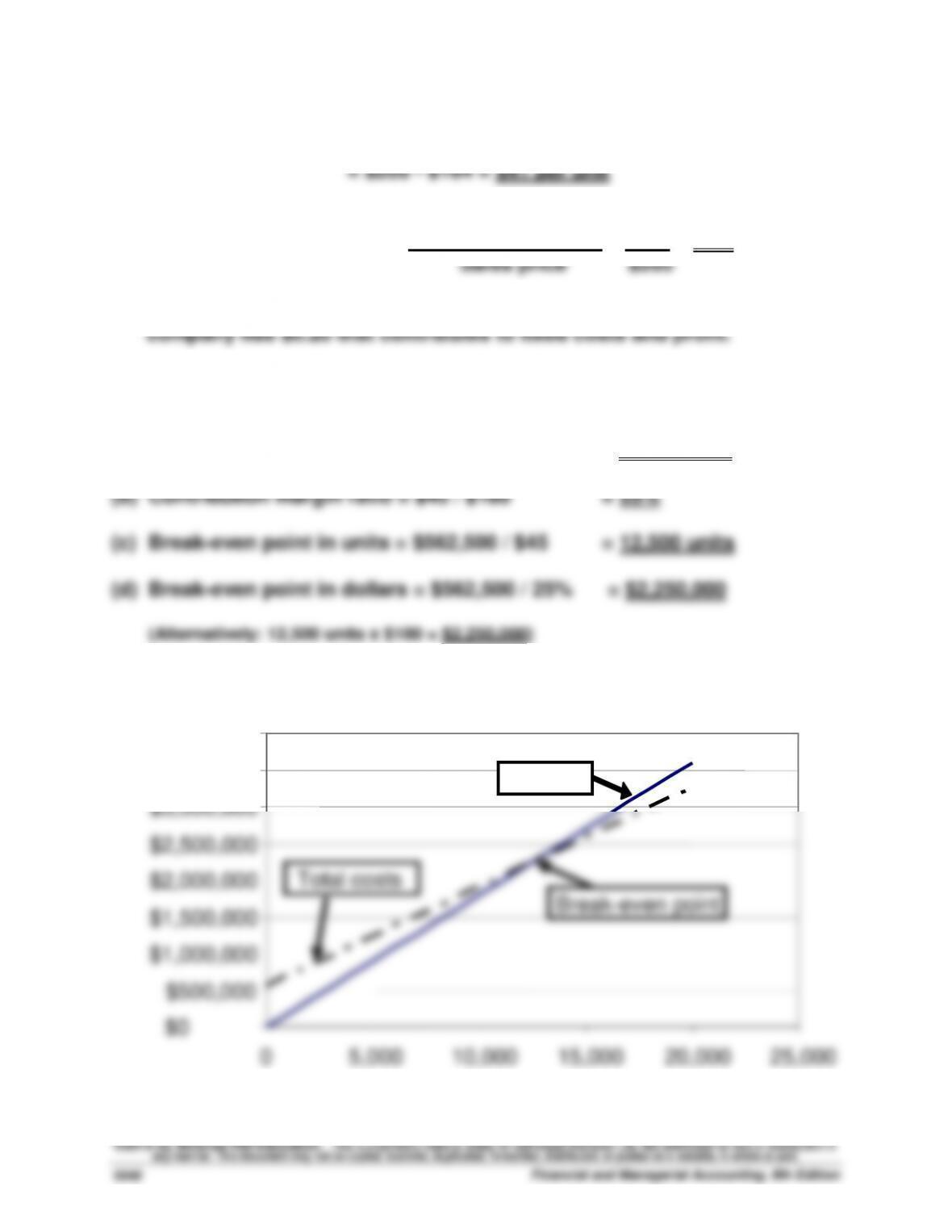

Exercise 18–10 (15 minutes)

$0

$500,000

$1,000,000

$1,500,000

$2,000,000

$2,500,000

$3,000,000

$3,500,000

$4,000,000

0

5,000

10,000

15,000

20,000

25,000

Units

Sales

Total costs

Break-even point

Exercise 18-11 (20 minutes)

1.

BLANCHARD COMPANY

Contribution Margin Income Statement (at Break-Even)

Sales (12,500 x $180) ………………………………………………………..………

$2,250,000

Variable costs (12,500 x $135) …………………………………………..………

1,687,500

Contribution margin (12,500 x $45) ……………………………………………

562,500

Fixed costs ……………………………………………………………………..………

562,500

Net income ………………………………………………………………………………

$ 0

2. Sales (in dollars) to break even with increased fixed costs

Break-even = (Original fixed costs + Additional fixed costs)

Exercise 18-12 (25 minutes)

1. Unit sales at target income =

2. Dollar sales at target income = costs income

Contribution margin ratio

Exercise 18-13 (20 minutes)

BLANCHARD COMPANY

Forecasted Contribution Margin Income Statement

Sales (40,000 x $200) …………………………………………………………….….

$8,000,000

Variable costs (40,000 x $140) ……………………………………………….….

5,600,000

Contribution margin (40,000 x $60) ………………………………………..….

2,400,000

Fixed costs ………………………………………………………………………….….

562,500

Income before taxes …………………………..………………………………..….

1,837,500

Income taxes (20% x $1,837,500) ……………………………………………….

367,500

Net income …………………………………………………………………………..….

$1,470,000

Fixed Target

costs income

Contribution margin/unit

+

Exercise 18–14 (10 minutes)

1. Fixed costs + Target pretax income

Dollar sales = Contribution margin ratio

2.

Sales …………………………..…………..……

$1,296,000

Fixed costs ……………………………………

(160,000)

Pretax income …………………………..

(164,000)

Variable costs …………………………..

$ 972,000

(Alternatively: $1,296,000 in sales x [1 – 0.25 CM ratio] = $972,000)

Exercise 18-15 (30 minutes)

(a) Total expected variable costs

= Variable costs per unit x units produced and sold

= $60* x 200,000 units

Exercise 18-16 (10 minutes)

1. Break-even in units = Fixed costs / Contribution margin per unit

2. Break-even point in dollars = Fixed costs / Contribution margin ratio

Exercise 18-17 (15 minutes)

1. Dollar sales for target income = Fixed costs + Target income

2. Margin of safety (%) = Expected sales – breakeven sales

Exercise 18-18 (15 minutes)

HUDSON CO.

Forecasted Contribution Margin Income Statement

For Year Ended December 31, 2016

Sales (9,600 x $225) ……………………………………………………………..….

$2,160,000

Variable costs (9,600 x $171*) ……………………………………………….….

1,641,600

Contribution margin …………………………………………………………….….

518,400

Fixed costs ($324,000 + $40,500) …………………………………………..….

364,500

Income (pretax) ……………………………………………………………………….

$ 153,900

*Revised variable costs = $180 – $9 = $171 per unit

Exercise 18-19 (10 minutes)

1. Revised contribution margin per unit = $240 – $180 = $60

2. Revised contribution margin ratio = $60/$240 = 25%

3. Break-even in units = Fixed costs / Contribution margin per unit

4. Break-even point in dollars = Fixed costs / Contribution margin ratio

Exercise 18–20 (15 minutes)

HUDSON CO.

Forecasted Contribution Margin Income Statement

For Year Ended December 31, 2016

Sales (11,000 x $225) ……………………………………………………….…..….

$2,475,000

Variable costs (11,000 x $180) ………………………………………………….

1,980,000

Contribution margin …………………………………………………………….….

495,000

Fixed costs ($324,000 + $81,000) …………………………………………..….

405,000

Income (pretax) ……………………………………………………………………….

$ 90,000

Exercise 18-21 (20 minutes)

1. Pretax income = Sales – Variable costs – Fixed costs

2. Instructor note: Use equation in Exhibit 18.23;

Unit sales = Fixed costs + Target pretax income

Exercise 18-22 (25 minutes)

1. Selling price per composite unit

8 windows @ $200 per unit ……………………………………………………...

$1,600

2 doors @ $500 per unit …………………………………………………………..

1,000

Selling price per composite unit ……………………………………………...

$2,600

2. Variable costs per composite unit

8 windows @ $125 per unit ……………………………………………………...

$1,000

2 doors @ $350 per unit …………………………………………………………..

700

Variable costs per composite unit …………………………………………...

$1,700

3. Break-even point in composite units

Fixed costs .

4. Unit sales of windows and doors at break-even point

Windows: 8 x 1,000 units (from 3) ………..…….

8,000 units

Doors: 2 x 1,000 units (from 3) ………..…….

2,000 units

Exercise 18-23 (25 minutes)

1. Selling price per composite unit

5 Easy returns @ $50 each …………………………………………………….

$ 250

3 Moderate returns @ $125 each…………………………………………….

375

2 Business returns @ $275 each…………………………………………….

Selling price per composite unit …………………………………………….

550

$1,175

2. Variable costs per composite unit

5 Easy returns @ $30 each …………………………………………………….

$ 150

3 Moderate returns @ $75 each………………………………………………

225

2 Business returns @ $100 each…………………………………………….

Variable costs per composite unit ………………………………………….

200

$ 575

3. Break-even point in composite units

Fixed costs .

4. Unit sales of Easy, Moderate, and Business returns at break-even point

Easy: 5 x 30 units (from 3) …………….…….

150 units

Moderate: 3 x 30 units (from 3) …………….…….

90 units

Business: 2 x 30 units (from 3) …………….…….

60 units

Exercise 18-24 (30 minutes)

1. Prepare a contribution margin income statement for Co. A to compute its DOL;

2. Prepare a contribution margin income statement for Co. B to compute its DOL;

3. Analyze and interpret which company benefits more from a 20% sales increase.

Step 1.

Company A

Contribution Margin Income Statement

Sales (given)…………………………………………………………………..

$6,000,000

Variable costs [$6,000,000 x (100% – 60%)] ………………………

2,400,000

Contribution margin ($6,000,000 x 60%) ………………………….

3,600,000

Fixed costs (given) ………………………………………………………...

2,600,000

Pretax income …………………………..……………………………………

$1,000,000

Company A’s DOL

=

Contribution margin in dollars / Pretax income

=

$3,600,000 / $1,000,000

=

3.6

Step 2.

Company B

Contribution Margin Income Statement

Sales (given)…………………………………………………………………..

$4,500,000

Variable costs [$4,500,000 x (100% – 25%)] ………………………

3,375,000

Contribution margin ($4,500,000 x 25%) ………………………….

1,125,000

Fixed costs (given) ………………………………………………………...

375,000

Pretax income …………………………..……………………………………

$ 750,000

Company B’s DOL

=

Contribution margin in dollars / Pretax income

=

$1,125,000 / $750,000

=

1.5

Step 3.

Interpretation: Company A benefits more from a 20% increase in sales.

1.5 x 20%). Note that although Company A’s fixed costs are higher, its