Problem 16-7A (Concluded)

Part 3

If equivalent units of production for a production department’s ending

inventory for October are understated, then total equivalent units of

production is also understated. This means the cost per equivalent unit for

Problem 16-1B (45 minutes)

Part 1: Cost of goods transferred and cost of goods sold

Beginning work in process inventory ……………………………………....

$156,000

Direct materials used in production ………………………………………...

120,000

Direct labor used in production………………………………………………..

350,000

Overhead applied (75% of direct labor cost) ……………………………..

262,500

Total production costs …………………………………………………………....

888,500

Less ending work in process inventory …………………………………...

(250,000)

Transferred to finished goods inventory (a) ……………………………..

$638,500

Beginning finished goods inventory ……………………………………....

$160,000

Plus goods transferred from production ………………………………....

638,500

Goods available for sale …………………………..……………………………..

798,500

Less ending finished goods inventory ……………………………………..

(198,000)

Cost of goods sold (b) …………………………………………………………....

$600,500

Part 2: Summary journal entries

a.

June 30

Raw Materials Inventory …………………………….………….

200,000

Accounts Payable ………………………………..………….

200,000

Purchased raw materials.

b.

June 30

Work in Process Inventory…………………………..

120,000

Raw Materials Inventory ………………………..…

120,000

Used direct materials.

c.

June 30

Factory Overhead ……………………………………..………….

42,000

Raw Materials Inventory ……………………….….

42,000

Used indirect materials.

Problem 16–1B (Continued)

d.

June 30

Work in Process Inventory…………………………..

350,000

Factory Payroll Payable ……………………….….

350,000

Used direct labor.

e.

June 30

Factory Overhead ………………………………………………….

50,000

Factory Payroll Payable ……………………….….

50,000

Used indirect labor.

f.

June 30

Factory Payroll Payable …………………………….………….

400,000

Cash ……………………………………………………….

400,000

Paid payroll cost.

g.

June 30

Factory Overhead ……………………………………..………….

170,500

Other Accounts ……………………………………………….

170,500

Incurred other overhead costs.

h.

June 30

Work in Process Inventory…………………………..

262,500

Factory Overhead …………………………………………….

262,500

Applied overhead at 75% of direct labor cost.

i.

June 30

Finished Goods Inventory…………………………..

638,500

Work in Process Inventory…………………….…….

638,500

Transferred completed products from

production to finished goods inventory.

j.

June 30

Accounts Receivable …………………………………………….

1,000,000

Sales ……………………………………………………….

1,000,000

Sold finished goods.

June 30

Cost of Goods Sold …………………………………..………….

600,500

Finished Goods Inventory …………………….…….

600,500

To record cost of goods sold for June.

Problem 16-2B (50 minutes)

Part 1

(a) and (b) Equivalent units with respect to direct materials and conversion

Direct

Equivalent units of production

Materials

Conversion

Units completed & transferred out …………………..

80,000

80,000

Units of ending work in process ……………………..

Direct materials (8,000 x 100%) ………………….

8,000

Conversion (8,000 x 25%)…………………………..

______

2,000

Equivalent units of production ………………………..

88,000

82,000

Part 2

Cost per equivalent unit of production

Direct

Materials

Conversion

Costs of beginning work in process ……………...

$ 58,000

$ 86,400

Costs incurred this period …………………………..

712,000

1,980,000

Total costs …………………………………………………...

$770,000

$2,066,400

÷ Equivalent units of production …………………...

88,000 EUP

82,000 EUP

Cost per equivalent unit of production …………..

$8.75 per EUP

$25.20 per EUP

Part 3: Assigning product costs to units

Costs transferred out

Direct materials (80,000 EUP x $8.75 per EUP) ………

$ 700,000

Conversion (80,000 EUP x $25.20 per EUP) ……..……

2,016,000

Total costs transferred out ……………………………..……

$2,716,000

Cost of ending work in process

Direct materials (8,000 EUP x $8.75 per EUP) …..……

70,000

Conversion (2,000 EUP x $25.20 per EUP) ……….……

50,400

Total costs of ending work in process …………….……

120,400

Total costs accounted for* ………………………………..……

$2,836,400

*This equals the sum of the total direct materials cost and the total conversion costs ($770,000 +

$2,066,400 = $2,836,400).

Problem 16–2B (Concluded)

Part 4

MEMORANDUM

TO:

FROM:

DATE:

RE: Percentage of Completion Error Analysis

If the units in ending inventory are 75% complete instead of 25% with respect

Problem 16-3B (75 minutes)

Part 1

BRAUN COMPANY

Process Cost Summary – Weighted Average Method

For Month Ended November 30

Costs Charged to Production

Costs of beginning work in process

Direct materials ………………………………………………………..

$ 6,800

Conversion ………………………………………………………………

14,500

Costs incurred this period

$ 21,300

Direct materials ………………………………………………………..

116,400

Conversion ………………………………………………………………

1,067,000

1,183,400

Total costs to account for …………………………………………..

$1,204,700

Unit cost information

Units to account for

Units accounted for

Beginning work in process …..……..

7,500

Completed & transferred out ……….………………….

100,000

Units started this period ……….……..

104,500

Ending work in process …………….…………….

12,000

Total units to account for ……..……..

112,000

Total units accounted for …………..………………

112,000

Equivalent units of production

Direct

Materials

Conversion

Units completed & transferred out …….….

100,000 EUP

100,000 EUP

Units of ending work in process

Direct materials (12,000 x 100%) ……..….

12,000 EUP

Conversion (12,000 x 25%) ………………….

__________

3,000 EUP

Equivalent units of production ………….….

112,000 EUP

103,000 EUP

Cost per EUP

Direct

Materials

Conversion

Cost of beginning work in process ……….

$ 6,800

$ 14,500

Costs incurred this period ………………..….

116,400

1,067,000

Total costs ……………………………………….….

$123,200

$1,081,500

÷ EUP ……………………………………………….….

112,000 EUP

103,000 EUP

Cost per EUP …………………………..……….….

$1.10 per EUP

$10.50 per EUP

[Continued on next page]

Problem 16-3B (Concluded)

Cost assignment and reconciliation

Costs transferred out

Direct materials (100,000 EUP x $1.10 per EUP) ….

$110,000

Conversion (100,000 x $10.50 per EUP) ………………

1,050,000

$1,160,000

Costs of ending work in process

Direct materials (12,000 EUP x $1.10 per EUP) ……

13,200

Conversion (3,000 EUP x $10.50 per EUP) …………..

31,500

44,700

Total costs accounted for …………………………………….

$1,204,700

Part 2

Nov. 30

Finished Goods Inventory……………………….….

1,160,000

Work in Process Inventory…………………………..

1,160,000

Transfer of goods to finished goods

inventory.

Problem 16-4B (80 minutes)

Part 1

SWITCH CO.

Process Cost Summary – Weighted Average Method

For Month Ended January 31

Costs Charged to Production

Costs of beginning work in process

Direct materials ……………………………………………………….

$ 7,500

Conversion ………………………………………………………….…..

49,840

Costs incurred this period

$ 57,340

Direct materials ……………………………………………………….

112,500

Conversion ………………………………………………………….…..

616,000

728,500

Total costs to account for …………………………………………..

$785,840

Unit cost information

Units to account for

Units accounted for

Beginning work in process …….……

10,000

Completed & transferred out .….

220,000

Units started this period ………..……

250,000

Ending work in process ………

40,000

Total units to account for ……….……

260,000

Total units accounted for….…

260,000

Equivalent units of production

Direct

Materials

Conversion

Units completed & transferred out ……………………..

220,000 EUP

220,000 EUP

Units of ending work in process

Direct materials (40,000 x 50%) ………………………..

20,000 EUP

Conversion (40,000 x 30%) …………………….…….

___________

12,000 EUP

Equivalent units of production

240,000 EUP

232,000 EUP

Cost per EUP

Direct Materials

Conversion

Cost of beginning work in process …………………..

$ 7,500

$ 49,840

Costs incurred this period ……………………….….

112,500

616,000

Total costs …………………………..………………….……….

$120,000

$665,840

÷ EUP ……………………………………………………....

240,000 EUP

232,000 EUP

Cost per EUP …………………………..………………………..

$0.50 per EUP

$2.87 per EUP

[Continued on next page]

Problem 16-4B (Concluded)

Cost assignment and reconciliation

Costs transferred out

Direct materials (220,000 EUP x $0.50 per EUP) ……….…….

$110,000

Conversion (220,000 x $2.87 per EUP) ……………………..……

631,400

$741,400

Costs of ending work in process

Direct materials (20,000 EUP x $0.50 per EUP) ……………….

10,000

Conversion (12,000 EUP x $2.87 per EUP) ………………..…….

34,440

44,440

Total costs accounted for ………………………………………….…….

$785,840

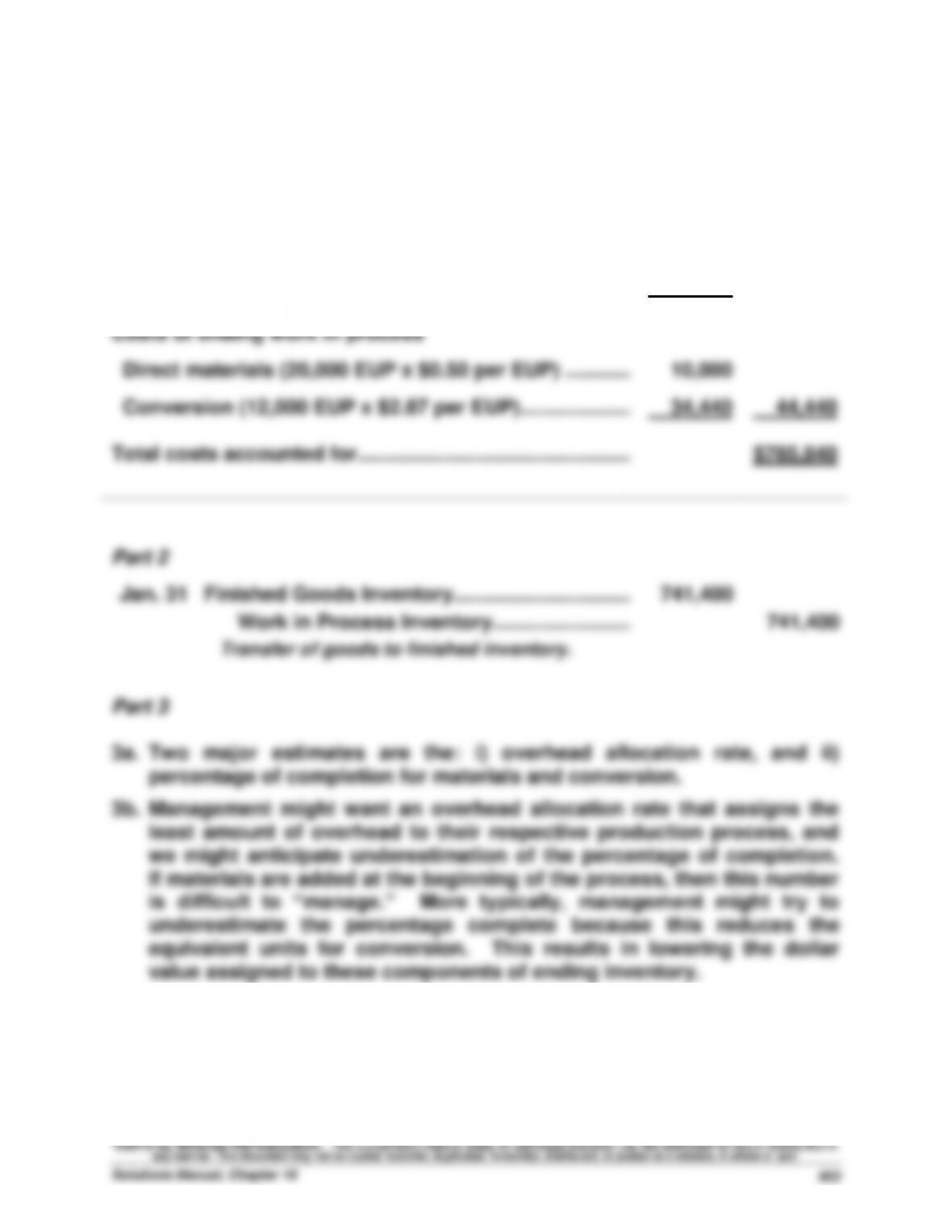

Part 2

Jan. 31

Finished Goods Inventory…………………………..

741,400

Work in Process Inventory…………………….…….

741,400

Transfer of goods to finished inventory.

Part 3

3a. Two major estimates are the: i) overhead allocation rate, and ii)

percentage of completion for materials and conversion.

3b. Management might want an overhead allocation rate that assigns the

least amount of overhead to their respective production process, and

we might anticipate underestimation of the percentage of completion.

If materials are added at the beginning of the process, then this number

is difficult to “manage.” More typically, management might try to

underestimate the percentage complete because this reduces the

equivalent units for conversion. This results in lowering the dollar

value assigned to these components of ending inventory.

Problem 16-5B (80 minutes)

Part 1

SWITCH COMPANY

Process Cost Summary – FIFO Method

For Month Ended January 31

Costs Charged to Production

Costs of beginning work in process

Direct materials ……………………………………………….………

$ 7,500

Conversion ……………………………………………………....

49,840

$ 57,340

Costs incurred this period

Direct materials ……………………………………………….………

112,500

Conversion ……………………………………………………....

616,000

728,500

Total costs to account for ………………………………….……….

$785,840

Unit cost information

Units to account for

Units accounted for

Beginning work in process ….………..

10,000

Completed & transferred out…..…

220,000

Units started this period ……..……….

250,000

Ending work in process ……..…

40,000

Total units to account for …………….

260,000

Total units accounted for ………

260,000

Equivalent units of production

Direct

Materials

Conversion

Units to complete beginning WIP

Direct materials (10,000 x 25%) ……..

2,500 EUP

Conversion (10,000 x 40%) …………....

4,000 EUP

Units started and completed …………...

210,000 EUP

210,000 EUP

Units of ending work in process

Direct materials (40,000 x 50%) ……..

20,000 EUP

Conversion (40,000 x 30%) …………....

__________

12,000 EUP

Equivalent units of production ………..

232,500 EUP

226,000 EUP

[Continued on next page]