Exercise 16–11 (continued)

2.

Cost assignment and reconciliation – FIFO

Cost of 60,000 units from beginning inventory

Beginning inventory

$ 167,066

Materials to complete (24,000 EUP x $2.58 per EUP)

61,920

Conversion to complete (36,000 EUP x $2.16 per EUP)

77,760

139,680

Total cost of 60,000 units from beginning inventory

$ 306,746

Costs of units started and completed

Direct materials (240,000 EUP x $2.58 per EUP)

$619,200

Conversion costs (240,000 EUP x $2.16 per EUP)

518,400

Total cost of 240,000 units started and completed

1,137,600

Total cost of 300,000 units transferred out

$1,444,346

Costs of units in ending inventory

Direct materials (65,600 EUP x $2.58 per EUP)

$169,248

Conversion costs (24,600 EUP x $2.16 per EUP)

53,136

Total cost of 82,000 units in ending inventory

222,384

Total costs assigned

$1,666,730

Costs to be assigned:

Beginning inventory

$167,066

Direct materials – current period

850,368

Conversion costs – current period

649,296

Total costs to be assigned

$1,666,730

Dept. 1 – WIP

Beg. Inv

167,066

DM

850,368

Conv

649,296

1,666,730

1,444,346

Transferred out

End. Inv.

222,384

Exercise 16-12 (30 minutes)

ASHAD COMPANY

Process Cost Summary – Weighted Average Method

For Month Ended July 31

Costs Charged to Production

Costs of beginning work in process ($18,550 + $2,280) ……………………...

$ 20,830

Costs incurred this period ($357,500 + $188,670) ……………………………....

546,170

Total costs to account for ………………………………………………………………...

$567,000

Unit Information

Units to Account For

Units Accounted For

Beginning work in process …….…………

2,000

Completed & transferred out …………………………..

32,000

Units started this period ……………………

32,500

Ending work in process …………….…………….

2,500

Total units to account for ……….…………

34,500

Total units accounted for ………….……………….

34,500

Equivalent Units of Production (EUP)

Direct

Materials

Conversion

Units completed and transferred out ……..

32,000 EUP

32,000 EUP

Units of ending work in process …………….

2,500 EUP

1,500 EUP

Equivalent units of production ……………...

34,500 EUP

33,500 EUP

Cost per EUP

Direct

Materials

Conversion

Costs of beginning work in process ……...

$ 18,550

$ 2,280

Costs incurred this period ……………………..

357,500

188,670

Total costs …………………………………………...

$376,050

$190,950

÷ Equivalent units of production …………...

34,500

33,500

Cost per equivalent unit of production …....

$10.90 per

EUP

$5.70 per

EUP

Cost Assignment and Reconciliation

Costs transferred out

Direct materials (32,000 x $10.90) …………………….…….

$348,800

Conversion (32,000 x $5.70) …………………………….………….

182,400

Total transferred out

$531,200

Cost of ending work in process

Direct materials (2,500 x $10.90) …………………………..

27,250

Conversion (1,500 x $5.70) ………………………………………….

8,550

Total ending work in process …………………………..

35,800

Total costs accounted for …………………………………….………….

$567,000

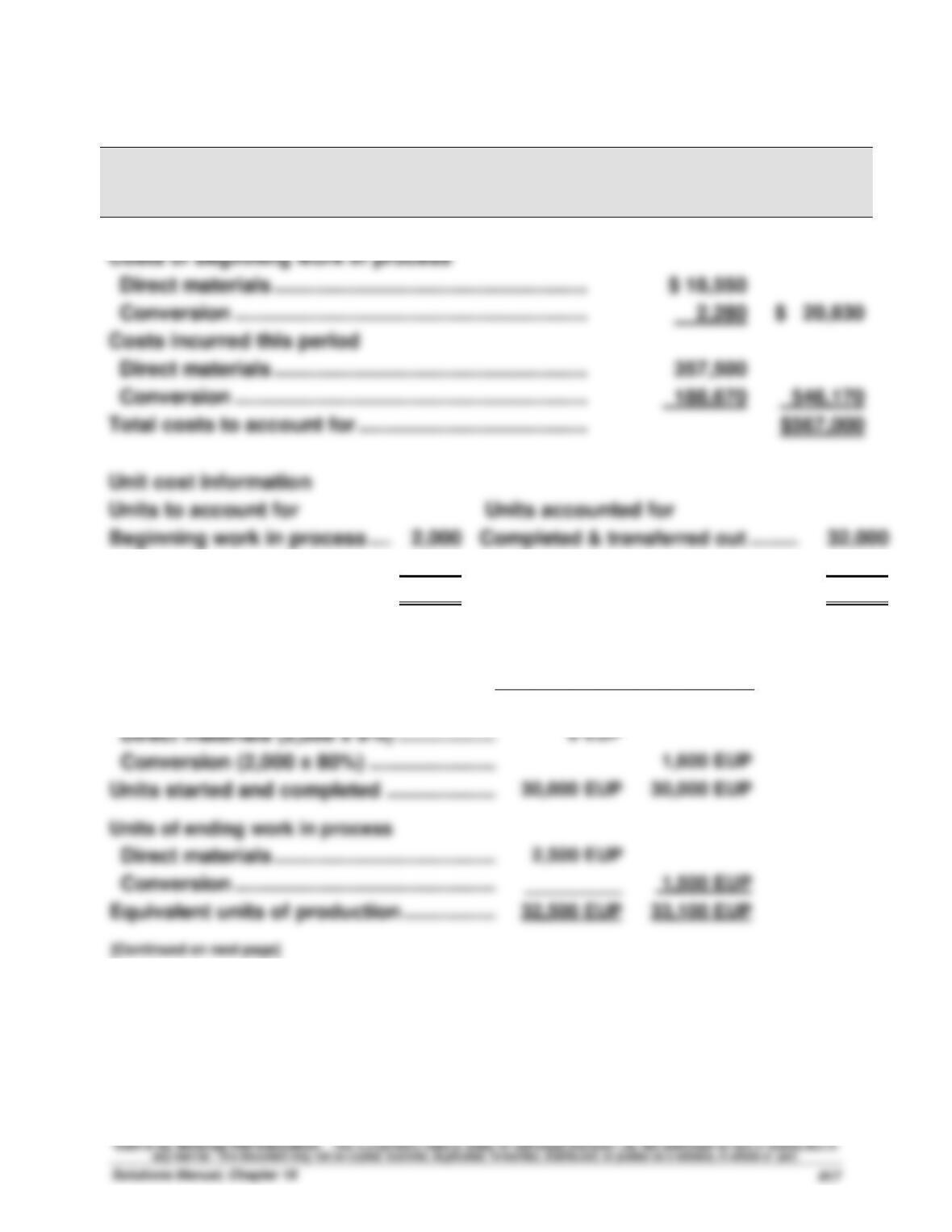

Exercise 16–13 (40 minutes)

ASHAD COMPANY

Process Cost Summary – FIFO Method

For Month Ended July 31

Costs Charged to Production

Costs of beginning work in process

Direct materials ………………………………………………..……..

$ 18,550

Conversion ……………………………………………………….

2,280

$ 20,830

Costs incurred this period

Direct materials ………………………………………………..……..

357,500

Conversion ……………………………………………………….

188,670

546,170

Total costs to account for …………………………………..………

$567,000

Unit cost information

Units to account for

Units accounted for

Beginning work in process ….……………………….

2,000

Completed & transferred out ………..

32,000

Units started this period…………………………..

32,500

Ending work in process ……………...

2,500

Total units to account for …….…………………….

34,500

Total units accounted for …………....

34,500

Equivalent units of production

Direct

Materials

Conversion

Units to complete beginning WIP

Direct materials (2,000 x 0%) ……………………….

0 EUP

Conversion (2,000 x 80%) …………………..………

1,600 EUP

Units started and completed ………………..……….

30,000 EUP

30,000 EUP

Units of ending work in process

Direct materials ………………………………….……….

2,500 EUP

Conversion ………………………………………..……….

_________

1,500 EUP

Equivalent units of production ……………..……….

32,500 EUP

33,100 EUP

[Continued on next page]

Exercise 16–13 (Concluded)

Cost per EUP

Direct

Materials

Conversion

Costs incurred this period ………………

$ 357,500

$ 188,670

EUP (from prior page) …………………….

÷ 32,500

÷ 33,100

Cost per EUP …………………………………

$11.00 per

EUP

$5.70 per

EUP

Cost assignment and reconciliation

Costs transferred out

Cost of beginning work in process ………………………

$20,830

Cost to complete beginning work in process

Direct materials (0 EUP x $11.00 per EUP)…………..

$ 0

Conversion (1,600 EUP x $5.70 per EUP) …………….

9,120

9,120

Costs of units started and completed this period

Direct materials (30,000 EUP x $11.00 per EUP) ….

330,000

Conversion (30,000 EUP x $5.70 per EUP) …………..

171,000

501,000

Total cost of work finished this period ………………..

530,950

Costs of ending work in process

Direct materials (2,500 EUP x $11.00 per EUP) ……

27,500

Conversion (1,500 EUP x $5.70 per EUP) …………….

8,550

36,050

Total costs accounted for …………………………………….

$567,000

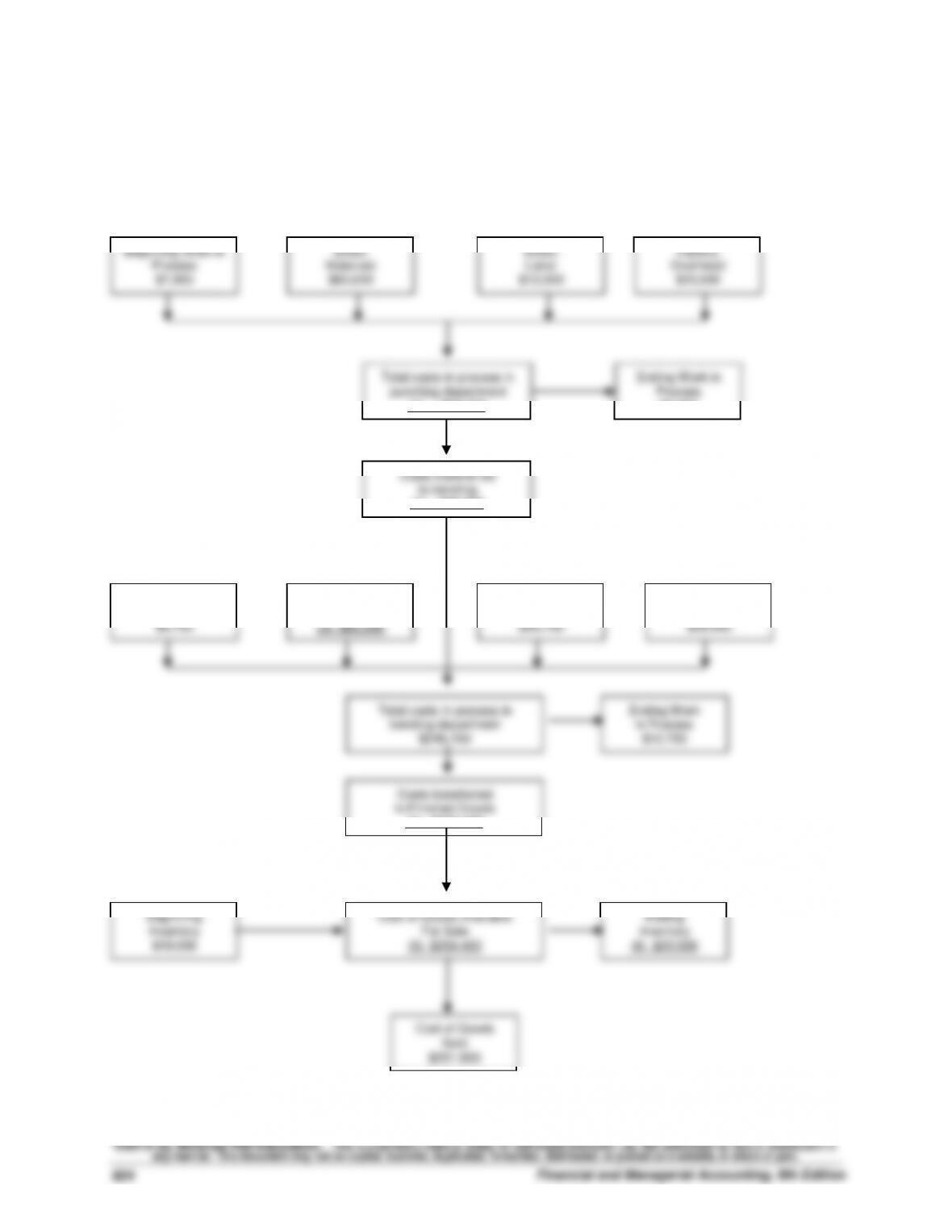

Exercise 16-14 (30 minutes)

Part 1: Cost of goods transferred and cost of goods sold

Weaving

Sewing

Finished

Department

Department

Goods

Beginning inventory …………………………….

$ 300,000

$ 570,000

$1,266,000

Direct materials …………………………………...

240,000

75,000

Direct labor ………………………………………….

1,200,000

360,000

Overhead applied (80% & 150% of labor) …...

960,000

540,000

Total costs—Weaving………………………...

2,700,000

Less ending inventory—Weaving ……….

(330,000)

TRANSFERRED TO SEWING (a) …………………..

$2,370,000

2,370,000

Total costs—Sewing ………………………………...

3,915,000

Less ending inventory—Sewing ………..

(700,000)

TRANSFERRED TO FINISHED GOODS (b) ……..

$3,215,000

3,215,000

Less ending inventory—Finished goods ….

(1,206,000)

COST OF GOODS SOLD (c) ……………………….

$3,275,000

Part 2: Summary journal entries.

June 30

Work in Process Inventory—Sewing ………….………….

2,370,000

Work in Process Inventory—Weaving ……………….

2,370,000

Transferred products from weaving to sewing.

June 30

Finished Goods Inventory…………………………..

3,215,000

Work in Process Inventory—Sewing ……..………….

3,215,000

Transferred completed products from

sewing to finished goods inventory.

June 30

Accounts Receivable …………………………………………….

4,000,000

Sales …………………………..……………………….….

4,000,000

Sold finished goods.

June 30

Cost of Goods Sold …………………………………..………….

3,275,000

Finished Goods Inventory …………………….…….

3,275,000

To record cost of goods sold for the month.

Exercise 16-15 (25 minutes)

Summary journal entries (all dated June 30)

a.

Raw Materials Inventory …………………………....………….

500,000

Accounts Payable ………………………………..………….

500,000

Purchased raw materials.

b.

Work in Process Inventory—Weaving …………………….

240,000

Work in Process Inventory—Sewing …………..………….

75,000

Raw Materials Inventory ………………………..…

315,000

Used direct materials.

c.

Factory Overhead ……………………………………..………….

120,000

Raw Materials Inventory ……………………….….

120,000

Used indirect materials.

d.

Work in Process Inventory—Weaving ………..………….

1,200,000

Work in Process Inventory—Sewing ………….………….

360,000

Factory Payroll Payable ……………………….….

1,560,000

Used direct labor.

e.

Factory Overhead ……………………………………..………….

1,500,000

Factory Payroll Payable ………………………..…

1,500,000

Used indirect labor.

f.

Factory Overhead ……………………………………..………….

156,000

Other Accounts ……………………………………………….

156,000

Incurred other overhead costs.

g.

Work in Process Inventory—Weaving ………..………….

960,000

Work in Process Inventory—Sewing ………….………….

540,000

Factory Overhead …………………………………………….

1,500,000

Applied overhead using predetermined rates.

h.

Factory Payroll Payable …………………………….………….

3,060,000

Cash …………………………..………………………..…

3,060,000

Paid total payroll.

Exercise 16–16 (25 minutes)

ELLIOTT COMPANY

Process Cost Summary – Weighted Average Method

For Month Ended March 31

Costs Charged to Production

Costs of beginning work in process

Direct materials ………………………………………………………..

$ 2,500

Conversion ……………………………………………………………….

6,360

$ 8,860

Costs incurred this period

Direct materials ………………………………………………………..

168,000

Conversion ……………………………………………………………….

479,640

647,640

Total costs to account for …………………………………………..

$656,500

Unit information

Units to account for

Units accounted for

Beginning work in process ……..……………………

2,000

Completed & transferred out ………….

17,000

Units started this period ………….……………….

20,000

Ending work in process ……..……….

5,000

Total units to account for ………..…………………

22,000

Total units accounted for …………….

22,000

Equivalent units of production

Direct

Materials

Conversion

Units completed & transferred out ….

17,000 EUP

17,000 EUP

Units of ending work in process

Direct materials (5,000 x 100%) ……..

5,000 EUP

Conversion (5,000 x 35%) ……………..

__________

1,750 EUP

Equivalent units of production ……….

22,000 EUP

18,750 EUP

Cost per EUP

Direct

Materials

Conversion

Cost of beginning work in process …

$ 2,500

$ 6,360

Costs incurred this period ………………

168,000

479,640

Total costs …………………………………….

$170,500

$486,000

÷ EUP …………………………………………….

22,000 EUP

18,750 EUP

Cost per EUP …………………………………

$7.75 per

EUP

$25.92 per

EUP

[Continued on next page]

Exercise 16-16 (continued)

Cost assignment and reconciliation

Costs transferred out

Direct materials (17,000 EUP x $7.75 per EUP) ……

$131,750

Conversion (17,000 x $25.92 per EUP) ………………..

440,640

$572,390

Costs of ending work in process

Direct materials (5,000 EUP x $7.75 per EUP) ……..

38,750

Conversion (1,750 EUP x $25.92 per EUP) …………..

45,360

84,110

Total costs accounted for …………………………………….

$656,500

Exercise 16-17 (40 minutes)

OSLO COMPANY

Process Cost Summary – Weighted Average Method

For Month Ended May 31

Costs Charged to Production

Costs of beginning work in process

Direct materials ………………………………………………………..

$ 2,880

Conversion ……………………………………………………………….

5,358

$ 8,238

Costs incurred this period

Direct materials ………………………………………………………..

197,120

Conversion ……………………………………………………………….

234,992

432,112

Total costs to account for …………………………………………..

$440,350

Unit information

Units to account for

Units accounted for

Beginning work in process ………….

4,000

Completed & transferred out …………………………..

13,000

Units started this period ………..…….

12,000

Ending work in process ……….………………….

3,000

Total units to account for …………….

16,000

Total units accounted for …….…………………….

16,000

[Continued on next page]

Exercise 16–17 (Concluded)

Equivalent units of production

Direct

Materials

Conversion

Units completed & transferred out ………..

13,000 EUP

13,000 EUP

Units of ending work in process

Direct materials (3,000 x 100%) ……….…..

3,000 EUP

Conversion (3,000 x 25%) ……………….…..

__________

750 EUP

Equivalent units of production ……………..

16,000 EUP

13,750 EUP

Cost per EUP

Direct

Materials

Conversion

Cost of beginning work in process …..…..

$ 2,880

$ 5,358

Costs incurred this period ………………..…..

197,120

234,992

Total costs …………………………………………..

$200,000

$240,350

÷ EUP …………………………………………………..

16,000 EUP

13,750 EUP

Cost per EUP …………………………………..…..

$12.50 per

EUP

$17.48 per

EUP

Cost assignment and reconciliation

Costs transferred out

Direct materials (13,000 EUP x $12.50 per EUP) ….

$162,500

Conversion (13,000 x $17.48 per EUP) ………………..

227,240

$389,740

Costs of ending work in process

Direct materials (3,000 EUP x $12.50 per EUP) ……

37,500

Conversion (750 EUP x $17.48 per EUP) ……………..

13,110

50,610

Total costs accounted for …………………………………….

$440,350

Exercise 16-18 (10 minutes)

Equivalent units of production—FIFO

Units of

Percent

Equivalent

EUP (for materials and conversion)

Product

Added

Units

Beginning work in process ………....

30,000

70%

21,000 EUP

Goods started and completed ……..

120,000

100

120,000 EUP

Ending work in process ……………...

20,000

80

16,000 EUP

Total units …………………………..……...

170,000

157,000 EUP

Exercise 16–19 (20 minutes)

[Note: Solution key is on the following page.]

Punching

Bending

Warehouse

punching department

(1) $94,500

Process

$6,000

Costs transferred

(2) $88,500

Beginning Work in

Process

Direct

Materials

Direct

Labor

Factory

Overhead

to Finished Goods

(4) $236,400

Beginning

Cost of Goods Available

Ending