Quick Study 16-23 (10 minutes)

1.

Raw Materials Inventory ………………………………………..

62,000

Cash ………………………………………………………………..

62,000

Purchase of raw materials inventory.

2.

Work in Process Inventory ………………………………..…..

50,000

Raw Materials Inventory …………………………………..

50,000

Direct materials used in production.

Quick Study 16-24 (10 minutes)

1.

Work in Process Inventory ………………………………..…..

125,000

Factory Payroll Payable ……………………………….…..

125,000

To record direct labor used in production.

2.

Factory Overhead ……………………………………………..…..

10,000

Factory Payroll Payable ……………………………….…..

10,000

To record indirect labor used in production.

3.

Factory Payroll Payable …………………………………….…..

135,000

Cash ………………………………………………………………..

135,000

To record payment of factory payroll.

Quick Study 16-25 (15 minutes)

1.

Factory Overhead ……………………………………………..…..

9,000

Raw Materials Inventory …………………………………..

9,000

To record indirect materials used in production.

2.

Factory Overhead ……………………………………………..…..

156,000

Other accounts …………………………………………..…..

156,000

To record other overhead costs.

3.

Work in Process Inventory …………………………..………..

175,000

Factory Overhead ……………………………………….…..

175,000

To record overhead applied ($125,000 x 140%).

Quick Study 16-26 (10 minutes)

Finished Goods Inventory ……………………………………..

275,000

Work in Process Inventory …………………………..

275,000

Transfer of finished goods from production.

Quick Study 16-27 (5 minutes)

If the company is successful in reducing water usage, its raw materials

EXERCISES

Exercise 16-1 (10 minutes)

1. Process operation 7. Job order operation

2. Process operation 8. Process operation

3. Process operation 9. Job order operation

4. Process operation 10. Job order operation

5. Job order operation 11. Job order operation

6. Process operation 12. Process operation

Exercise 16-2 (10 minutes)

a. Job order operation. e. Job order operation.

Exercise 16-3 (10 minutes)

1. F 5. G

2. A 6. B

3. D 7. E

4. C

Exercise 16-4 (30 minutes)

1. Beginning inventory is 100% complete with respect to materials.

Ending inventory is 100% complete with respect to materials.

EUP for Materials

Units of

Product

Goods completed (80,000 EUP x 100%) ………………………………

80,000

Ending work in process (16,000 EUP x 100%) ……………………..

16,000

Total EUP …………………………………………………………………………..

96,000

2. Beginning inventory is 40% complete with respect to materials.

Ending inventory is 75% complete with respect to materials.

Units of

EUP for Materials

Product

Goods completed (80,000 EUP x 100%) ………………………………

80,000

Ending work in process (16,000 EUP x 75%) ……………………….

12,000

Total EUP …………………………………………………………………………..

92,000

3. Beginning inventory is 60% complete with respect to materials.

Ending inventory is 30% complete with respect to materials.

Units of

EUP for Materials

Product

Goods completed (80,000 EUP x 100%) ………………………………

80,000

Ending work in process (16,000 EUP x 30%) ……………………….

4,800

Total EUP …………………………………………………………………………..

84,800

Exercise 16-5 (30 minutes)

1. Beginning inventory is 100% complete with respect to materials.

Ending inventory is 100% complete with respect to materials.

EUP for Materials

Units of

Product

To complete beginning work in process (24,000 EUP x 0%) …..….

0

Units started and completed (56,000 EUP x 100%) ………………..….

56,000

Ending work in process (16,000 EUP x 100%) ……………………….….

16,000

Total EUP …………………………………………………………………………….….

72,000

2. Beginning inventory is 40% complete with respect to materials.

Ending inventory is 75% complete with respect to materials.

Units of

EUP for Materials

Product

To complete beginning work in process (24,000 EUP x 60%) …….

14,400

Units started and completed (56,000 EUP x 100%) ………………..….

56,000

Ending work in process (16,000 EUP x 75%) …………………………..

12,000

Total EUP …………………………………………………………………………….….

82,400

3. Beginning inventory is 60% complete with respect to materials.

Ending inventory is 30% complete with respect to materials.

Units of

EUP for Materials

Product

To complete beginning work in process (24,000 EUP x 40%) …….

9,600

Units started and completed (56,000 EUP x 100%) ………………..….

56,000

Ending work in process (16,000 EUP x 30%) …………………………..

4,800

Total EUP …………………………………………………………………………….….

70,400

Exercise 16-6 (30 minutes)

1.

Equivalent units of production—Weighted average

Direct

Materials

Conversion

Units completed & transferred out (295,000 x 100%) .……….

295,000

295,000

Units of ending work in process

Direct materials, 30,000 x 80% ……………………………..……….

24,000

Conversion, 30,000 x 30% …………………………………………….

______

9,000

Equivalent units of production ……………………………….……….

319,000

304,000

2.

Cost per equivalent unit—Weighted average

Direct

Materials

Conversion

Costs of beginning work in process ………………………..

$ 44,800

$ 15,300

Costs incurred this period ……………………………………....

1,231,200

896,700

Total costs ……………………………………………………………..

$1,276,000

$912,000

÷ Equivalent units of production (from part 1) ………....

319,000

304,000

Cost per equivalent unit of production …………………....

$4.00 per

EUP

$3.00 per

EUP

3.

Cost assignment—Weighted average

Costs of units transferred out

Direct materials (295,000 EUP x $4.00 per EUP) ……

$1,180,000

Conversion (295,000 EUP x $3.00 per EUP) …………..

885,000

Total costs transferred out ……………………………………..

$2,065,000

Costs of ending work in process

Direct materials (24,000 EUP x $4.00 per EUP) ……..

96,000

Conversion (9,000 EUP x $3.00 per EUP) ………………

27,000

Total costs of ending work in process …………………….

123,000

Total costs assigned* …………………………………………….

$2,188,000

*Equals costs to account for of $2,188,000, computed as $60,100 + $1,231,200 + $896,700

Exercise 16-7 (30 minutes)

1.

Equivalent units of production—FIFO

Direct

Materials

Conversion

Units to complete beginning work in process

Direct materials (25,000 x 40%) ……………………………………..

Conversion (25,000 x 60%) ………………………………….………..

Units started and completed (270,000 x 100%) ……….………..

10,000

270,000

15,000

270,000

Units of ending work in process

Direct materials, 30,000 x 80% …………………………….………..

24,000

Conversion, 30,000 x 30% …………………………………..………..

______

9,000

Equivalent units of production ………………………………………..

304,000

294,000

2.

Cost per equivalent unit—FIFO

Direct

Materials

Conversion

Costs incurred this period ……………………………………….

$1,231,200

$896,700

÷ Equivalent units of production (from part 1) ………….

304,000

294,000

Cost per equivalent unit of production …………………….

$4.05 per

EUP

$3.05 per

EUP

Exercise 16-8 (20 minutes)

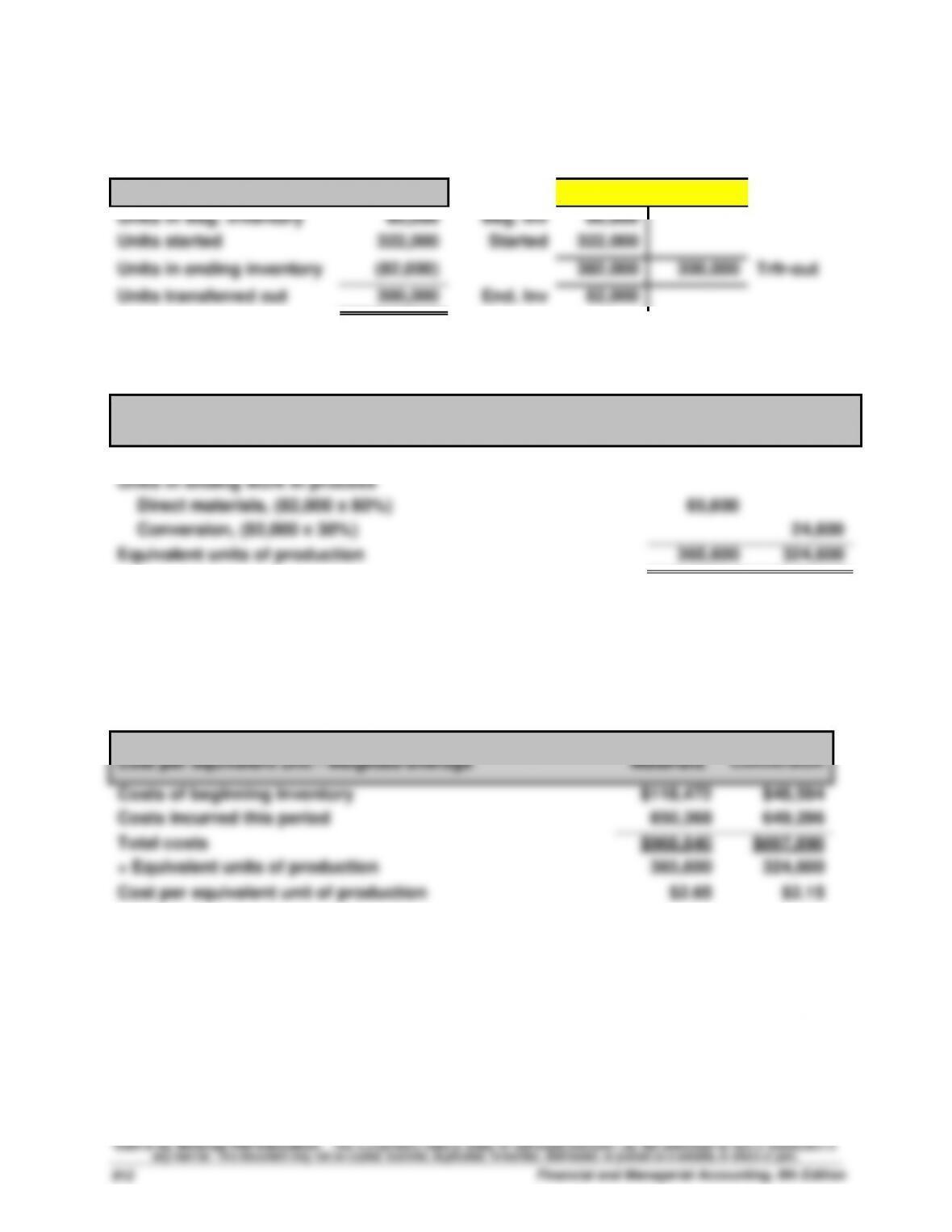

1. Units transferred out

Units

Dept. 1 – units

Units in Beg. inventory

60,000

Beg. Inv

60,000

Units started

322,000

Started

322,000

Units in ending inventory

(82,000)

382,000

300,000

Trfr-out

Units transferred out

300,000

End. Inv

82,000

2. EUP

Equivalent units of production – weighted-average

Direct

Materials

Conversion

Units completed & transferred out (300,000 x 100%)………

300,000

300,000

Units in ending work in process

Direct materials, (82,000 x 80%)

65,600

Conversion, (82,000 x 30%)

24,600

Equivalent units of production

365,600

324,600

Exercise 16-9 (20 minutes)

1. Cost per EUP

Cost per equivalent unit – weighted-average

Direct

Materials

Conversion

Costs of beginning inventory

$118,472

$48,594

Costs incurred this period

850,368

649,296

Total costs

$968,840

$697,890

÷ Equivalent units of production

365,600

324,600

Cost per equivalent unit of production

$2.65

$2.15

Exercise 16-9 (continued)

2.

Cost assignment and reconciliation – weighted-average

Costs of units transferred out

Direct materials (300,000 EUP x $2.65 per EUP)

$795,000

Conversion costs (300,000 EUP x $2.15 per EUP)

645,000

Total cost of 300,000 units transferred out

$1,440,000

Costs of units in ending inventory

Direct materials (65,600 EUP x $2.65 per EUP)

$173,840

Conversion costs (24,600 EUP x $2.15 per EUP)

52,890

Total cost of 82,000 units in ending inventory

226,730

Total costs assigned

$1,666,730

Costs to be assigned:

Beginning inventory

$167,066

Direct materials – current period

850,368

Conversion costs – current period

649,296

Total costs to be assigned

$1,666,730

Dept. 1 – WIP

Beg. Inv

167,066

DM

850,368

Conv

649,296

1,666,730

1,440,000

Transferred out

End. Inv.

226,730

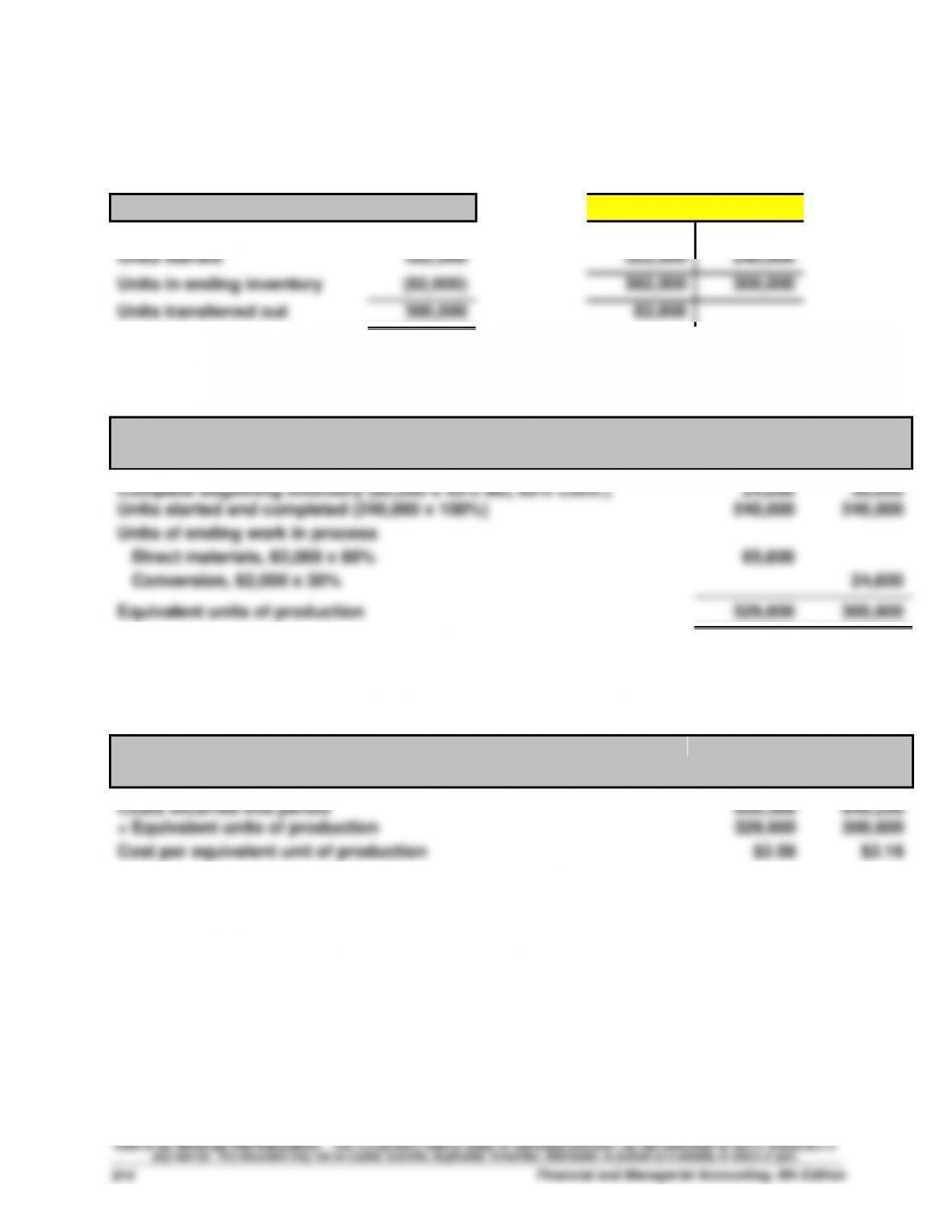

Exercise 16-10 (20 minutes)

1.

Units

Units

Units in beginning inventory

60,000

60,000

60,000

Units started

322,000

322,000

240,000

Units in ending inventory

(82,000)

382,000

300,000

Units transferred out

300,000

82,000

2.

Equivalent units of production – FIFO

Direct

Materials

Conversion

Complete beginning inventory (60,000 x 40% Mtl, 60% Conv.)

24,000

36,000

Units started and completed (240,000 x 100%)

240,000

240,000

Units of ending work in process

Direct materials, 82,000 x 80%

65,600

Conversion, 82,000 x 30%

24,600

Equivalent units of production

329,600

300,600

Exercise 16–11 (20 minutes)

1.

Cost per equivalent unit – FIFO

Direct

Materials

Conversion

Costs incurred this period

850,368

649,296

÷ Equivalent units of production

329,600

300,600

Cost per equivalent unit of production

$2.58

$2.16