Problem 15-4A (35 minutes)

Part 1

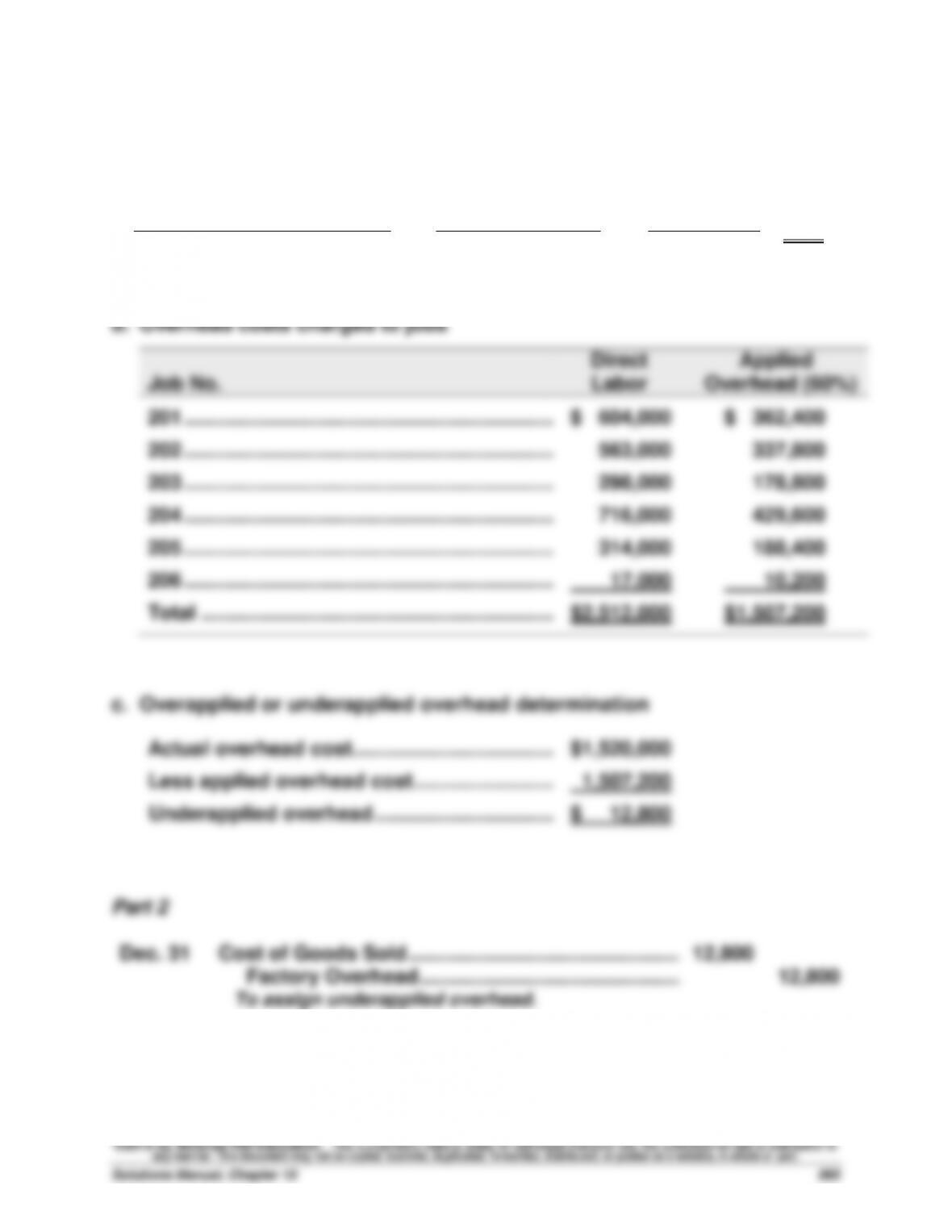

a. Predetermined overhead rate

= = = 60%

Estimated overhead costs

Estimated direct labor cost

$1,500,000

$2,500,000

$1,500,000

[50 x 2,000 x $25]

Problem 15-5A (80 minutes)

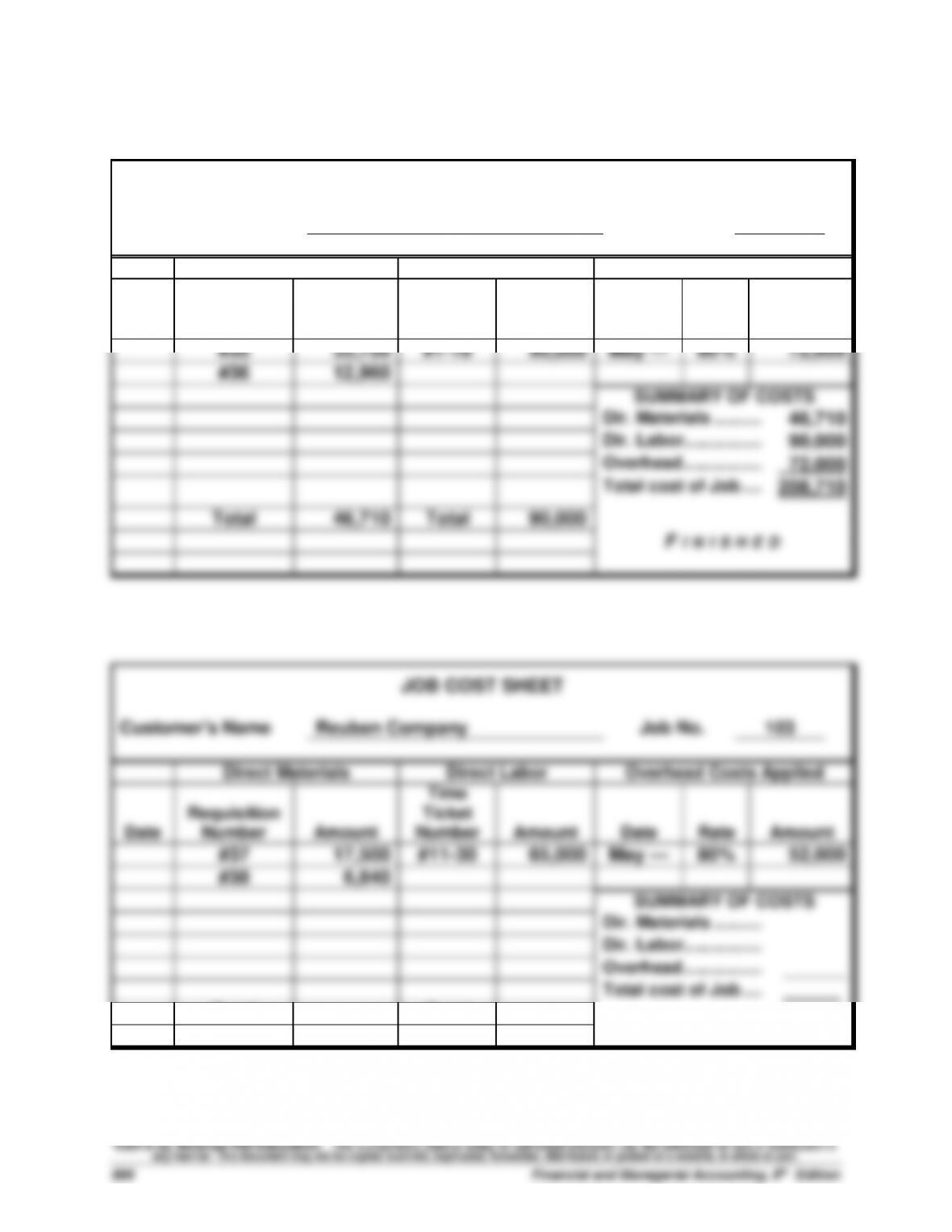

JOB COST SHEET

Customer’s Name

Worldwide Company

Job No.

102

Direct Materials

Direct Labor

Overhead Costs Applied

Date

Requisition

Number

Amount

Time

Ticket

Number

Amount

Date

Rate

Amount

#35

33,750

#1–10

90,000

May —

80%

72,000

#36

12,960

SUMMARY OF COSTS

Dir. Materials ………..…………………

46,710

Dir. Labor ……………..……………

90,000

Overhead ……………..……………

72,000

Total cost of Job …..………………………

208,710

Total

46,710

Total

90,000

FI N I S H E D

JOB COST SHEET

Customer’s Name

Reuben Company

Job No.

103

Direct Materials

Direct Labor

Overhead Costs Applied

Date

Requisition

Number

Amount

Time

Ticket

Number

Amount

Date

Rate

Amount

#37

17,500

#11–30

65,000

May —

80%

52,000

#38

6,840

SUMMARY OF COSTS

Dir. Materials ………..…………………

Dir. Labor ……………..……………

Overhead ……………..……………

______

Total cost of Job …..………………………

.

Total

Total

Problem 15-5A (Continued)

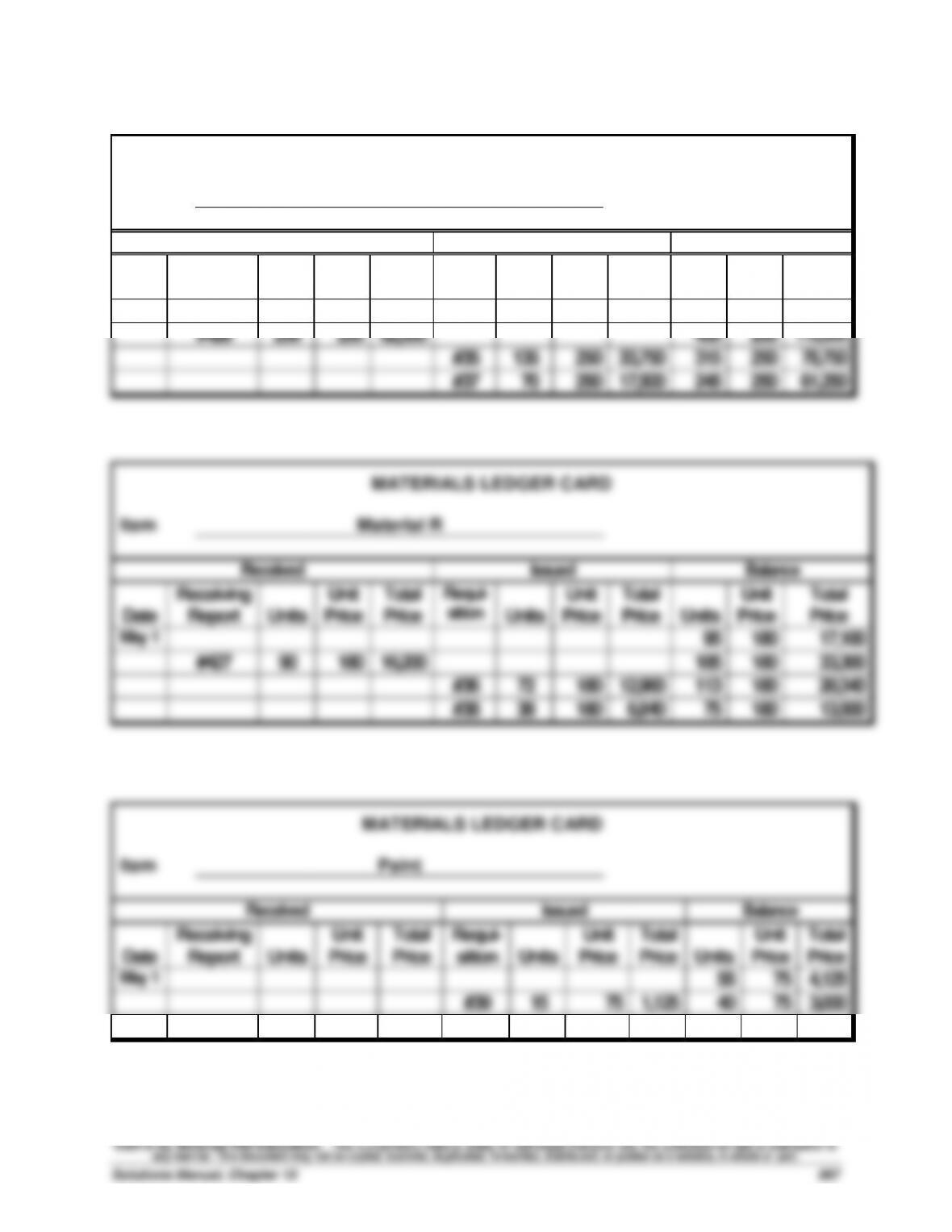

MATERIALS LEDGER CARD

Item

Material M

Received

Issued

Balance

Date

Receiving

Report

Units

Unit

Price

Total

Price

Requi–

sition

Units

Unit

Price

Total

Price

Units

Unit

Price

Total

Price

May 1

200

250

50,000

#426

250

250

62,500

450

250

112,500

#35

135

250

33,750

315

250

78,750

#37

70

250

17,500

245

250

61,250

Received

Issued

May 1

180

90

180

16,200

185

180

#36

72

180

113

180

MATERIALS LEDGER CARD

Item

May 1

15

Problem 15–5A (Continued)

GENERAL JOURNAL

a.

Raw Materials Inventory ………………………………………..

78,700

Accounts Payable ………………………………………..…..

78,700

To record materials purchases ($62,500+$16,200).

d.

Work in Process Inventory* ……………………………….…..

155,000

Factory Overhead …………………………..……………………..

19,250

Cash ………………………………………………………………..

174,250

To record direct & indirect labor.

*($90,000 + 65,000)

Factory Overhead …………………………..……………………..

102,000

Cash ………………………………………………………………..

102,000

To record other factory overhead.

e.

Finished Goods Inventory ……………………………………..

208,710

Work in Process ………………………………………….…..

208,710

To record completion of jobs.

f.

Accounts Receivable ………………………………………..…..

400,000

Sales …………………………………………………………..…..

400,000

To record sales on account.

Cost of Goods Sold …………………………..…………………..

208,710

Finished Goods Inventory ………………………………..

208,710

To record cost of sales.

h.

Work in Process Inventory* ……………………………….…..

71,050

Factory Overhead …………………………..……………………..

1,125

Raw Materials Inventory …………………………………..

72,175

To record direct & indirect materials.

*($33,750 + $12,960 + $17,500 + $6,840)

i.

Work in Process Inventory …………………………..………..

124,000

Factory Overhead …………………………..………………..

124,000

To apply overhead ($72,000 + 52,000).

Problem 15–5A (Continued)

j. The ending balance in the Factory Overhead account is computed as:

Actual Factory Overhead

Miscellaneous overhead …………………….

$102,000

Indirect materials ……………………………….

1,125

Indirect labor …………………………..……..….

19,250

Total actual factory overhead ………….….

122,375

Factory overhead applied ………………….….

124,000

Overapplied overhead ……………………….….

$ (1,625)

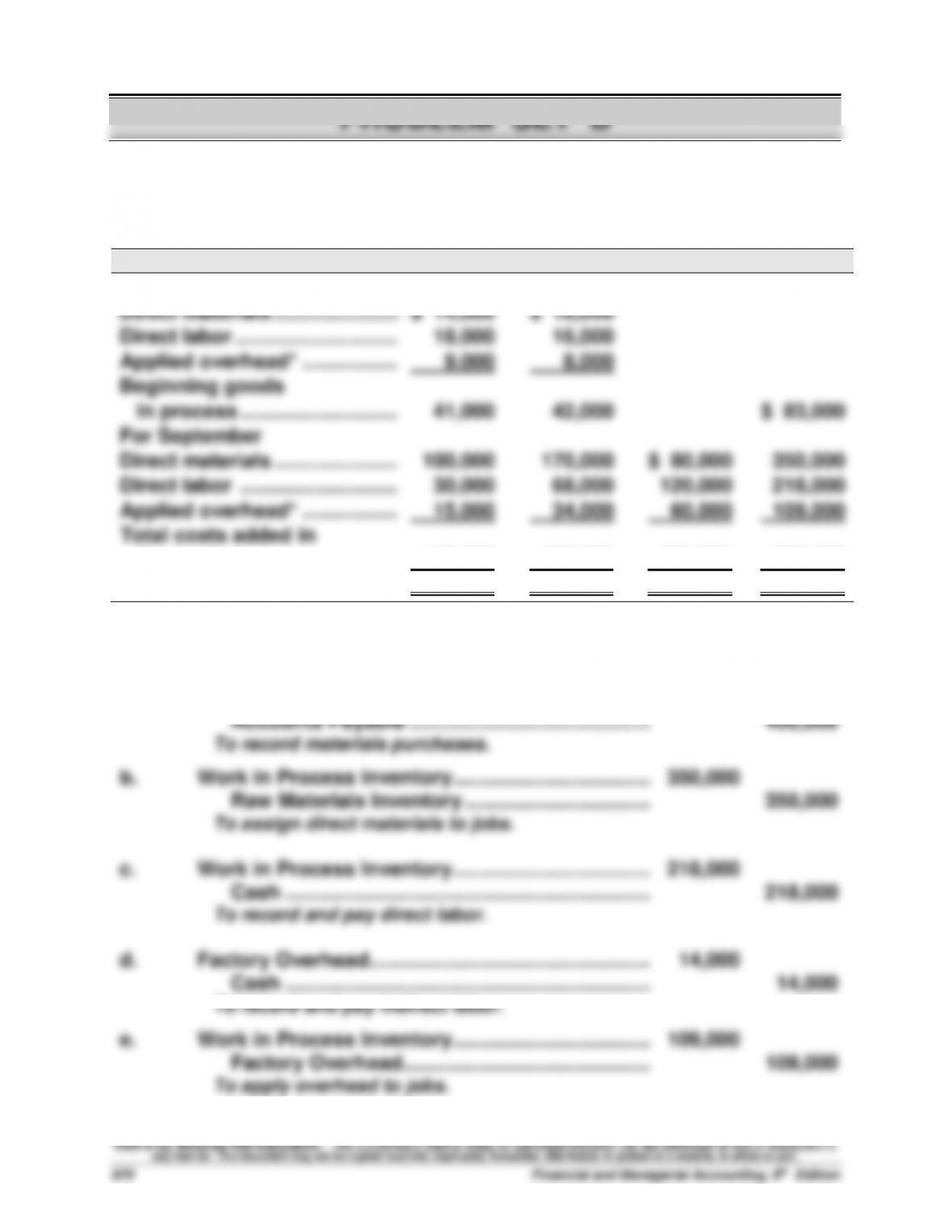

Problem 15-1B (80 minutes)

Part 1

Total manufacturing costs and the costs assigned to each job

114

115

116

Sept. Total

From August

Direct materials …………………..………

$ 14,000

$ 18,000

Direct labor …………………………..

18,000

16,000

Applied overhead* ………………………

9,000

8,000

Beginning goods

In process ………………………..…

41,000

42,000

$ 83,000

For September

Direct materials …………………..………

100,000

170,000

$ 80,000

350,000

Direct labor ………………………..…

30,000

68,000

120,000

218,000

Applied overhead* ………………………

15,000

34,000

60,000

109,000

Total costs added in

September ……………………….….

145,000

272,000

260,000

677,000

Total costs …………………………..

$186,000

$314,000

$260,000

$760,000

*Equals 50% of direct labor cost.

Part 2 Journal entries for September

a.

Raw Materials Inventory ………………………………….……..

400,000

Accounts Payable ……………………………………..……..

400,000

To record materials purchases.

b.

Work in Process Inventory ……………………………………..

350,000

Raw Materials Inventory …………………………….……..

350,000

To assign direct materials to jobs.

c.

Work in Process Inventory ……………………………………..

218,000

Cash ………………………………………………………………..

218,000

To record and pay direct labor.

d.

Factory Overhead…………………………..……………….……..

14,000

Cash ………………………………………………………………..

14,000

To record and pay indirect labor.

e.

Work in Process Inventory ……………………………………..

109,000

Factory Overhead…………………………..………….……..

109,000

To apply overhead to jobs.

Problem 15–1B (Continued)

f. [continued from prior page]

Factory Overhead…………………………..……………….……..

20,000

Cash ………………………………………………………………..

20,000

To record other factory overhead (rent).

Factory Overhead…………………………..……………….……..

12,000

Cash ………………………………………………………………..

12,000

To record other factory overhead (utilities).

Factory Overhead…………………………..……………….……..

30,000

Accum. Depreciation—Factory Equip ………………..

30,000

To record other factory overhead (depreciation).

Factory Overhead…………………………..……………….……..

30,000

Raw Materials Inventory …………………………….……..

30,000

To record indirect materials.

g.

Finished Goods Inventory ……………………………….……..

500,000

Work in Process Inventory …………………………..

500,000

To record jobs completed ($186,000 + $314,000).

h.

Cost of Goods Sold ………………………………………………..

186,000

Finished Goods Inventory …………………………..

186,000

To record cost of sale of job.

i.

Cash ……………………………………………………………………..

380,000

Sales ………………………………………………………………..

380,000

To record sale of job.

j.

Factory Overhead* ………………………………………….……..

3,000

Cost of Goods Sold…………………………………….……..

3,000

To assign overapplied overhead.

Problem 15–1B (Continued)

Part 3

PEREZ MFG.

Schedule of Cost of Goods Manufactured

For Month Ended September 30

Direct materials used…………………………..……………………..

$350,000

Direct labor used ……………………………………………………….

218,000

Factory overhead applied …………………………………………..

109,000

Total manufacturing costs ………………………………………....

677,000

Add work in process August 31 (Jobs 114 & 115) ………....

83,000

Total cost of work in process ……………………………………..

760,000

Deduct work in process, September 30 (Job 116) ………...

(260,000)

Cost of goods manufactured ……………………………………...

$500,000

Part 4

Gross profit on the income statement for the month ended September 30

Sales …………………………………………………………………………………………

$380,000

Cost of goods sold ($186,000 – $3,000) …………………………………….…

(183,000)

Gross profit …………………………………………………………………………….…

$197,000

Presentation of inventories on the September 30 balance sheet

Inventories

Raw materials ……………………………………………………………………….…

$170,000*

Work in process (Job 116) ……………………………………………………….

260,000

Finished goods (Job 115) ……………………………………………………….

314,000

Total inventories ………………………………………………………………………

$744,000

* Beginning raw materials inventory …………………………..

$150,000

Purchases ……………………………………………………….

400,000

Direct materials used ……………………………………………………….

(350,000)

Indirect materials used…………………………….…………………………

(30,000)

Ending raw materials inventory ………………..…………

$170,000

Problem 15–1B (Concluded)

Part 5

Problem 15-2B (75 minutes)

Part 1

a.

Dec. 31

Work in Process Inventory …………………………..

12,200

Raw Materials Inventory ………………………..…

12,200

To record direct materials costs for

Jobs 603 and 604 ($4,600 + $7,600).

b.

Dec. 31

Work in Process Inventory …………………………..

13,000

Wages Payable ……………………………………..………….

13,000

To record direct labor costs for

Jobs 603 and 604 ($5,000 + $8,000).

c.

Dec. 31

Work in Process Inventory …………………………..

26,000

Factory Overhead…………………………..……..………….

26,000

To allocate overhead to Jobs 603 and 604 at

200% of direct labor cost assigned to them.

d.

Dec. 31

Factory Overhead…………………………..…………..………….

2,100

Raw Materials Inventory ………………………..…

2,100

To add cost of indirect materials

to actual factory overhead.

e.

Dec. 31

Factory Overhead…………………………..…………..………….

3,000

Wages Payable ……………………………………..………….

3,000

To accrue cost of indirect labor.

Problem 15–2B (Continued)

Part 2

Revised Factory Overhead account

Ending balance from trial balance …………………………..…..….

$27,000

Debit

Applied to Jobs 603 and 604…………………………..……………….

(26,000)

Credit

Additional indirect materials…………………………..……………….

2,100

Debit

Additional indirect labor………………………………………………….

3,000

Debit

Underapplied overhead ……………………………………………….….

$ 6,100

Debit

Cash …………………………..………………………………………..

Accounts receivable ……………………………………………...

Raw materials inventory* …………………………..…………..

Accounts payable …………………………..…………………....

Common stock ……………………………………………………..

Retained earnings ………………………………………………...

Factory overhead …………………………………………………..