PROBLEM SET A

Problem 15-1A (80 minutes)

Part 1 Total manufacturing costs and the costs assigned to each job

306

307

308

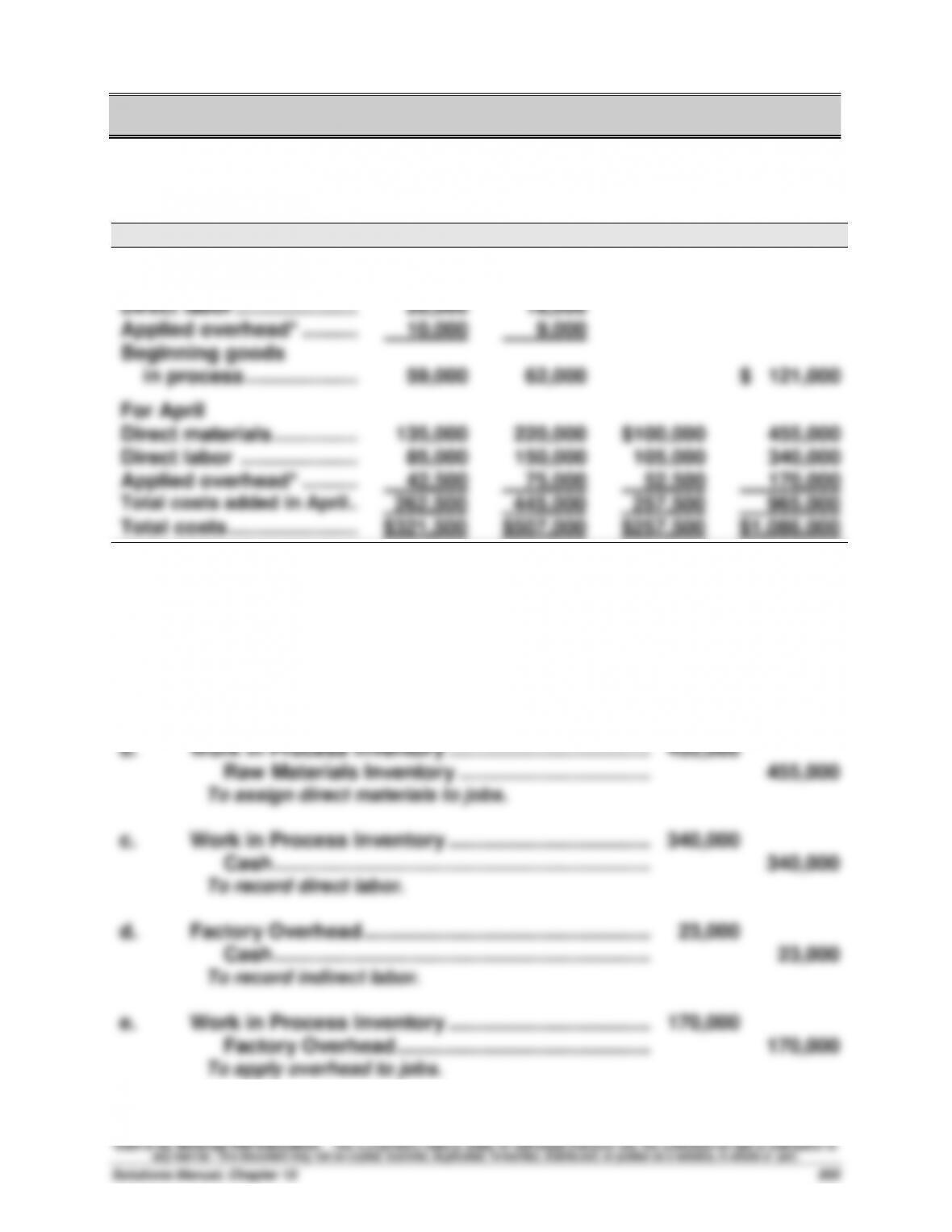

April Total

From March

Direct materials ………………….

$ 29,000

$ 35,000

Direct labor ………………….…….

20,000

18,000

Applied overhead* ……….…….

10,000

9,000

Beginning goods

in process ………………..…….

59,000

62,000

$ 121,000

For April

Direct materials ………………….

135,000

220,000

$100,000

455,000

Direct labor ……………………….

85,000

150,000

105,000

340,000

Applied overhead* ……….…….

42,500

75,000

52,500

170,000

Total costs added in April ..…….

262,500

445,000

257,500

965,000

Total costs …………………..…….

$321,500

$507,000

$257,500

$1,086,000

*Equals 50% of direct labor cost.

Part 2 Journal entries for April

a.

Raw Materials Inventory …………………………………..…….

500,000

Accounts Payable …………………………………………….

500,000

To record materials purchases.

b.

Work in Process Inventory …………………………..…..…….

455,000

Raw Materials Inventory ……………………………..…….

455,000

To assign direct materials to jobs.

c.

Work in Process Inventory ……………………………….…….

340,000

Cash …………………………………………………………..…….

340,000

To record direct labor.

d.

Factory Overhead …………………………………………….…….

23,000

Cash …………………………………………………………..…….

23,000

To record indirect labor.

e.

Work in Process Inventory …………………………..…..…….

170,000

Factory Overhead ……………………………………….…….

170,000

To apply overhead to jobs.

Problem 15-1A (continued)

f.

[continued from prior page]

Factory Overhead …………………………………………….…….

50,000

Raw Materials Inventory ……………………………..…….

50,000

To record indirect materials.

Factory Overhead …………………………………………….…….

19,000

Cash …………………………………………………………..…….

19,000

To record factory utilities.

Factory Overhead …………………………………………….…….

51,000

Accumulated Depreciation—Factory Equip ……….

51,000

To record other factory overhead.

Factory Overhead …………………………………………….…….

32,000

Cash …………………………………………………………..…….

32,000

To record factory rent.

g.

Finished Goods Inventory (306 & 307) ……………….…….

828,500

Work in Process Inventory …………………………..

828,500

To record jobs completed ($321,500 + $507,000).

h.

Cost of Goods Sold (306) ………………………………….…….

321,500

Finished Goods Inventory …………………………..

321,500

To record cost of sale of job.

i.

Cash ………………………………………………………………..…….

635,000

Sales ………………………………………………………….…….

635,000

To record sale of job.

j.

Cost of Goods Sold ………………………………………….…….

5,000

Factory Overhead* ……………………………………..…….

5,000

To assign underapplied overhead.

*Overhead applied to jobs …..

$170,000

Overhead incurred

Indirect materials………………..….

$50,000

Indirect labor ……………………..….

23,000

Factory rent ……………………….….

32,000

Factory utilities …………………..….

19,000

Factory equip. depreciation. .….

51,000

175,000

Underapplied overhead ………….

$ 5,000

Problem 15–1A (Continued)

Part 3

MARCELINO COMPANY

Schedule of Cost of Goods Manufactured

For Month Ended April 30

Direct materials used ……………………………………………………….

$ 455,000

Direct labor used ………………………………………………………….……..

340,000

Factory overhead applied …………………………………………….……..

170,000

Total manufacturing costs …………………………………………………..

965,000

Add work in process March 31 (Jobs 306 & 307) ………….……..

121,000

Total cost of work in process ……………………………………….……..

1,086,000

Deduct work in process, April 30 (Job 308)…………………..……..

(257,500)

Cost of goods manufactured ………………………………………..……..

$ 828,500

Part 4

Gross profit on the income statement for the month ended April 30

Sales …………………………………………………………………………………………….….

$ 635,000

Cost of goods sold ($321,500 + $5,000) …………………………………………….

(326,500)

Gross profit …………………………..……………………………………………………….

$ 308,500

Presentation of inventories on the April 30 balance sheet

Inventories

Raw materials …………………………………………………………………………………

$ 75,000*

Work in process (Job 308) …………………………………………………………….…

257,500

Finished goods (Job 307) ……………………………………………………………..…

507,000

Total inventories ………………………………………………………………………….…

$ 839,500

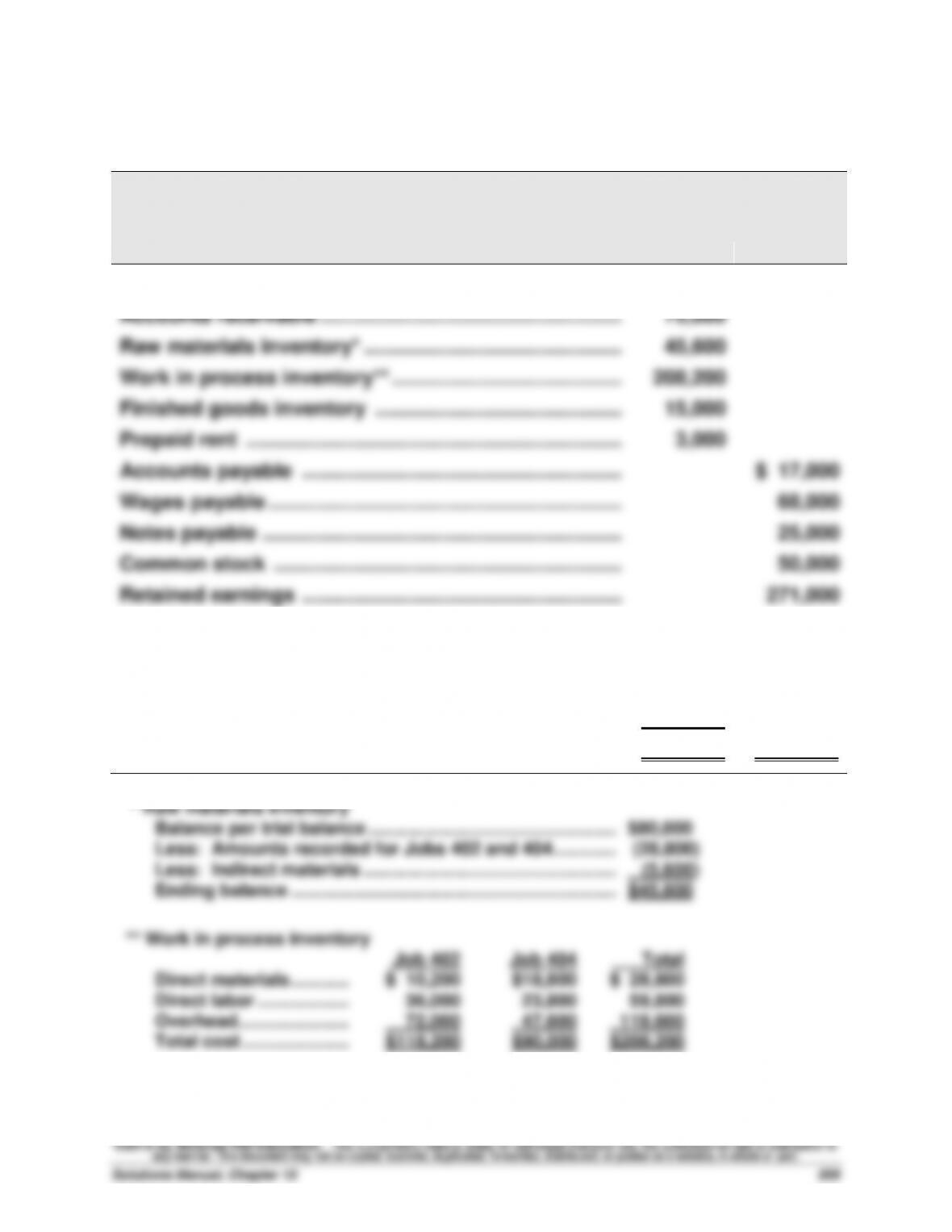

* Beginning raw materials inventory ……………….………….

$ 80,000

Purchases ………………………………………………….……

500,000

Direct materials used ………………………………….……………………

(455,000)

Indirect materials used………………………………..……………………..

(50,000)

Ending raw materials inventory …………………………..

$ 75,000

Part 5

Overhead is underapplied by $5,000, meaning that individual jobs or batches of

jobs are under-costed. Thus, profits at the job (and batch) level are overstated.

Problem 15-2A (75 minutes)

Part 1

a.

Dec. 31

Work in Process Inventory ……………………………………..

28,800

Raw Materials Inventory …………………………..

28,800

To record direct materials costs for

Jobs 402 and 404 ($10,200 + 18,600).

b.

Dec. 31

Work in Process Inventory ……………………………………..

59,800

Wages Payable …………………………..…………..………..

59,800

To record direct labor costs for

Jobs 402 and 404 ($36,000 + $23,800).

c.

Dec. 31

Work in Process Inventory ……………………………………..

119,600

Factory Overhead…………………………..……….………..

119,600

To allocate overhead to Jobs 402 and 404

at 200% of direct labor cost assigned.

d.

Dec. 31

Factory Overhead…………………………..…………….………..

5,600

Raw Materials Inventory …………………………..

5,600

To add cost of indirect materials

to actual factory overhead.

e.

Dec. 31

Factory Overhead…………………………..…………….………..

8,200

Wages Payable …………………………..…………..………..

8,200

To accrue indirect labor and assign it to

actual factory overhead.

Dec. 31

Cost of Goods Sold ………………………………………………..

9,200

Factory Overhead…………………………..……….………..

9,200

To close underapplied overhead.

Problem 15-2A (continued)

Part 3

BERGAMO BAY COMPANY

Trial Balance

December 31, 2015

Debit

Credit

Cash ……………………………………………………………………..…

$170,000

Accounts receivable …………………………..…………………..…

75,000

Raw materials inventory* ………………………………………..…

45,600

Work in process inventory** ………………………………………

208,200

Finished goods inventory …………………………………………

15,000

Prepaid rent …………………………………………………………..…

3,000

Accounts payable ………………………………………………….…

$ 17,000

Wages payable ……………………………………………………….

Notes payable ………………………………………………………..…

68,000

25,000

Common stock ……………………………………………………….

50,000

Retained earnings ………………………………………………….…

271,000

Sales ……………………………………………………………………..…

373,000

Cost of goods sold ($218,000 + $9,200) ………………………..…

227,200

Factory overhead …………………………..……………………….…

0

Operating expenses………………………………………………..…

60,000

_______

Totals …………………………………………………………………….…

$804,000

$804,000

Problem 15-2A (continued)

Part 4

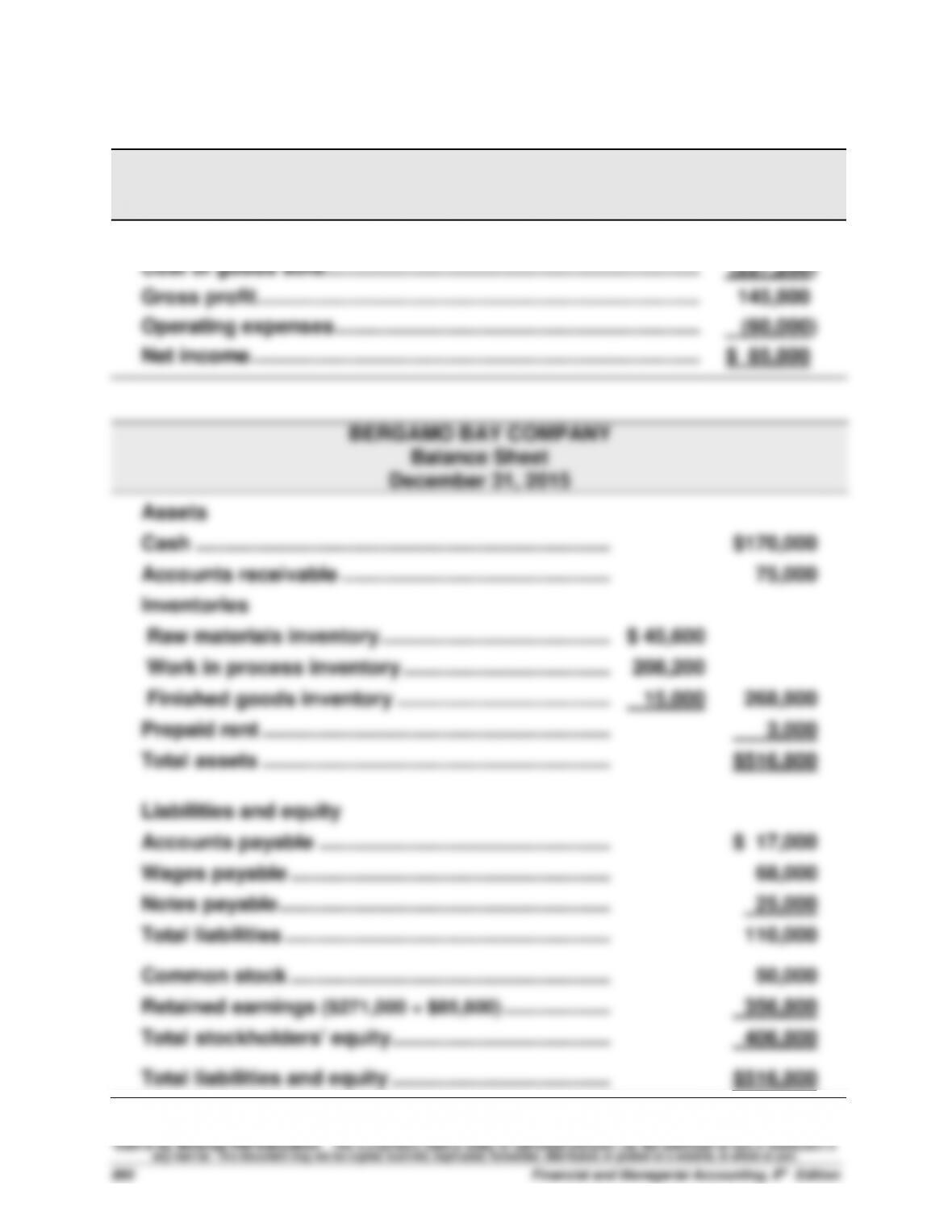

BERGAMO BAY COMPANY

Income Statement

For Year Ended December 31, 2015

Sales …………………………..………………………………………………….……

$373,000

Cost of goods sold ………………………………………………………….……

(227,200)

Gross profit …………………………………………………………………….……

145,800

Operating expenses ………………………………………………………..……

(60,000)

Net income ……………………………………………………….…………….……

$ 85,800

BERGAMO BAY COMPANY

Balance Sheet

December 31, 2015

Assets

Cash ………………………………………………………………..…………

$170,000

Accounts receivable ……………………………………………………

75,000

Inventories

Raw materials inventory …………………………..…………………

$ 45,600

Work in process inventory ……………………………….…………

208,200

Finished goods inventory ………………………………..…………

15,000

268,800

Prepaid rent …………………………..…………………………..

3,000

Total assets ……………………………………………………....

$516,800

Liabilities and equity

Accounts payable …………………………………………….…………

$ 17,000

Wages payable ……………………………………………………….

Notes payable …………………………………………………..…..

68,000

25,000

Total liabilities ………………………………………………….……

110,000

Common stock ……………………………………………………….

50,000

Retained earnings ($271,000 + $85,800) ……………….…………

356,800

Total stockholders’ equity ……………………………………………

406,800

Total liabilities and equity ……………………………………………

$516,800

Problem 15-2A (concluded)

Part 5

This $5,600 error would cause the costs for Job 404 to be understated.

Since Job 404 is in process at the end of the period, work in process

Problem 15-3A (70 minutes)

Part 1

JOB COST SHEETS

Job No. 136

Job No. 138

Materials …………..

$ 48,000

Materials …………..

$ 19,200

Labor …………..…..

12,000

Labor………………..

37,500

Overhead ……..…..

24,000

Overhead ……..…..

75,000

Total cost …….…..

$ 84,000

Total cost …….…..

$131,700

Job No. 137

Job No. 139

Materials …………..

$ 32,000

Materials …………..

$ 22,400

Labor …………..…..

10,500

Labor………………..

39,000

Overhead ……..…..

21,000

Overhead ……..…..

78,000

Total cost …….…..

$ 63,500

Total cost …….…..

$139,400

Job No. 140

Materials …………..

$ 6,400

Labor………………..

3,000

Overhead ……..…..

6,000

Total cost …….…..

$ 15,400

Part 2

a.

Raw Materials Inventory …………………………………..…….

200,000

Accounts Payable …………………………………………….

200,000

To record materials purchases.

b.

Work in Process Inventory …………………………..…..…….

128,000

Factory Overhead …………………………………………….…….

19,500

Raw Materials Inventory ……………………………..…….

147,500

To record direct & indirect materials.

c.

Factory Overhead …………………………………………….…….

15,000

Cash …………………………………………………………..…….

15,000

To record other factory overhead.

Problem 15-3A (Continued)

[continued from prior page]

d.

Work in Process Inventory …………………………..…..…….

102,000

Factory Overhead …………………………………………….…….

24,000

Cash …………………………………………………………..…….

126,000

To record direct & indirect labor.

e.

Work in Process Inventory …………………………..…..…….

177,000

Factory Overhead ……………………………………….…….

177,000

To apply overhead to jobs

[($12,000 + $37,500 + $39,000) x 200%].

f.

Finished Goods Inventory ………………………………..…….

355,100

Work in Process Inventory …………………………..

355,100

To record completion of jobs

($84,000 + $131,700 + $139,400).

g.

Accounts Receivable ……………………………………….…….

525,000

Sales ………………………………………………………….…….

525,000

To record sales on account.

Cost of Goods Sold ………………………………………….…….

215,700

Finished Goods Inventory …………………………..

215,700

To record cost of sales ($84,000 + $131,700).

h.

Factory Overhead …………………………………………….…….

149,500

Accum. Depreciation—Factory Building…………….

68,000

Accum. Depreciation—Factory Equipment ….…….

36,500

Prepaid Insurance …………………………..………….…….

10,000

Property Taxes Payable …………………………………….

35,000

To record other factory overhead.

i.

Work in Process Inventory …………………………..…..…….

27,000

Factory Overhead ……………………………………….…….

27,000

To apply overhead to jobs

[($10,500 + $3,000) x 200%].

Problem 15–3A (Continued)

Part 3

GENERAL LEDGER ACCOUNTS

Raw Materials Inventory

(a)

200,000

(b)

147,500

Bal.

52,500

Work in Process Inventory

Factory Overhead

(b)

128,000

(f)

355,100

(b)

19,500

(e)

177,000

(d)

102,000

(c)

15,000

(i)

27,000

(e)

177,000

(d)

24,000

(i)

27,000

(h)

149,500

Bal.

78,900

Bal.

4,000

Finished Goods Inventory

Cost of Goods Sold

(f)

355,100

(g)

215,700

(g)

215,700

Bal.

139,400

Bal.

215,700

Part 4

Reports of Job Costs*

Work in Process Inventory

Job 137 …………………………….……

$ 63,500

Job 140 …………………………….……

15,400

Balance …………………………....……

$ 78,900

Finished Goods Inventory

Job 139 …………………………….……

$139,400

Balance …………………………....……

$139,400

Cost of Goods Sold

Job 136 …………………………….……

$ 84,000

Job 138 …………………………….……

131,700

Balance …………………………....……

$215,700

*Individual totals reconcile with account balances in part 3.