EXERCISES

Exercise 14-1 (10 minutes)

Primary Information

Source

Financial

Managerial

Financial

Managerial

Managerial

Managerial

Financial

Managerial

5. Plan the budget for next quarter

6. Measure profitability of an individual store

7. Prepare financial reports according to GAAP

8. Determine location and size for a new plant

Business Decision

1. Determine whether to lend to a company

2. Evaluate a purchasing department’s performance

3. Report financial performance to board of directors

4. Estimate product cost for new line of shoes

Exercise 14-2 (20 minutes)

Product Cost

Variable

or Fixed

Direct

or Indirect

1. Leather cover for soccer balls Variable Direct

2. Annual flat fee paid for office security Fixed Indirect

3. Coolants for machinery Fixed Indirect

4. Wages of assembly workers Variable Direct

5. Lace to hold the leather together Variable Indirect

6. Taxes on factory Fixed Indirect

7. Machinery depreciation (straight-line) Fixed Indirect

Most fixed costs are indirect. Fixed costs normally are resources acquired to

support the production process rather than being traceable to individual

products or batches of product. However, not all indirect costs are fixed.

Exercise 14-3 (10 minutes)

1. Fixed, indirect

2. Fixed, indirect

3. Variable, direct

4. Fixed, indirect

5. Fixed, indirect

6. Variable, direct

Exercise 14-4 (20 minutes)

Cost

Variable

Fixed

Direct

Indirect

1. Advertising ………………………………….….

X

X

2. Beverages and snacks …………………….

X

X

3. Regional VP salary ………………………….

X

X

4. Depreciation on ground equip.……..….

X

X

5. Fuel and oil used in planes …………..….

X

X

6. Flight attendant salaries ………………….

X

X

7. Pilot salaries ………………………………..….

X

X

8. Maintenance worker wages ………….….

X

X

9. Customer service salaries ……………….

X

X

Exercise 14-5 (15 minutes)

1. Direct material

2. Factory overhead

3. Direct labor

4. General and administrative expense

5. Factory overhead

6. Factory overhead

7. Selling expense

8. Factory overhead

Exercise 14-6 (20 minutes)

1) Factory utilities Product Overhead Conversion

2) Advertising Period NA NA

3)

Amortization of patents on factory

machine

Product Overhead Conversion

4) State and federal income tax Period NA NA

5) Office supplies used Period NA NA

6) Insurance on factory bldg. Product Overhead Conversion

7) Wages to assembly workers Product Direct Labor

Prime and

Conversion

Exercise 14-7 (20 minutes)

Part 1

Company 1, Sunrise Foods, is a merchandising firm with only one

Exercise 14–7 (concluded)

Part 2

Company 1

Sunrise Foods

Balance Sheet—Current Asset Section

December 31, 2015

Cash ……………………………………………………………………………………..…………

$ 7,000

Accounts receivable …………………………………………………………………………

62,000

Merchandise inventory …………………………………………………………..…………

45,000

Prepaid expenses ………………………………………………………………….…………

1,500

Total current assets ……………………………………………………………….…………

$115,500

Company 2

Rayzer Skis Mfg.

Balance Sheet—Current Asset Section

December 31, 2015

Cash ……………………………………………………………………………………..…………

$ 5,000

Accounts receivable …………………………………………………………………………

75,000

Raw materials inventory…………………………..…………………………….…………

42,000

Work in process inventory ……………………………………………………....

30,000

Finished goods inventory ……………………………………………………….

50,000

Prepaid expenses ………………………………………………………………….…………

900

Total current assets ……………………………………………………………….…………

$202,900

Discussion: The current asset section of the balance sheet for these two

companies differs because one is a merchandiser and one is a

manufacturer. Sunrise Foods purchases items for resale, so it has only

one type of inventory. Rayzer Mfg., on the other hand, must report its

inventories at the various stages of completion: Raw materials are items

not yet put into the process; work in process are items started but not

complete; and finished goods are ready for sale.

Exercise 14-8 (30 minutes)

Garcon

Company

Pepper

Company

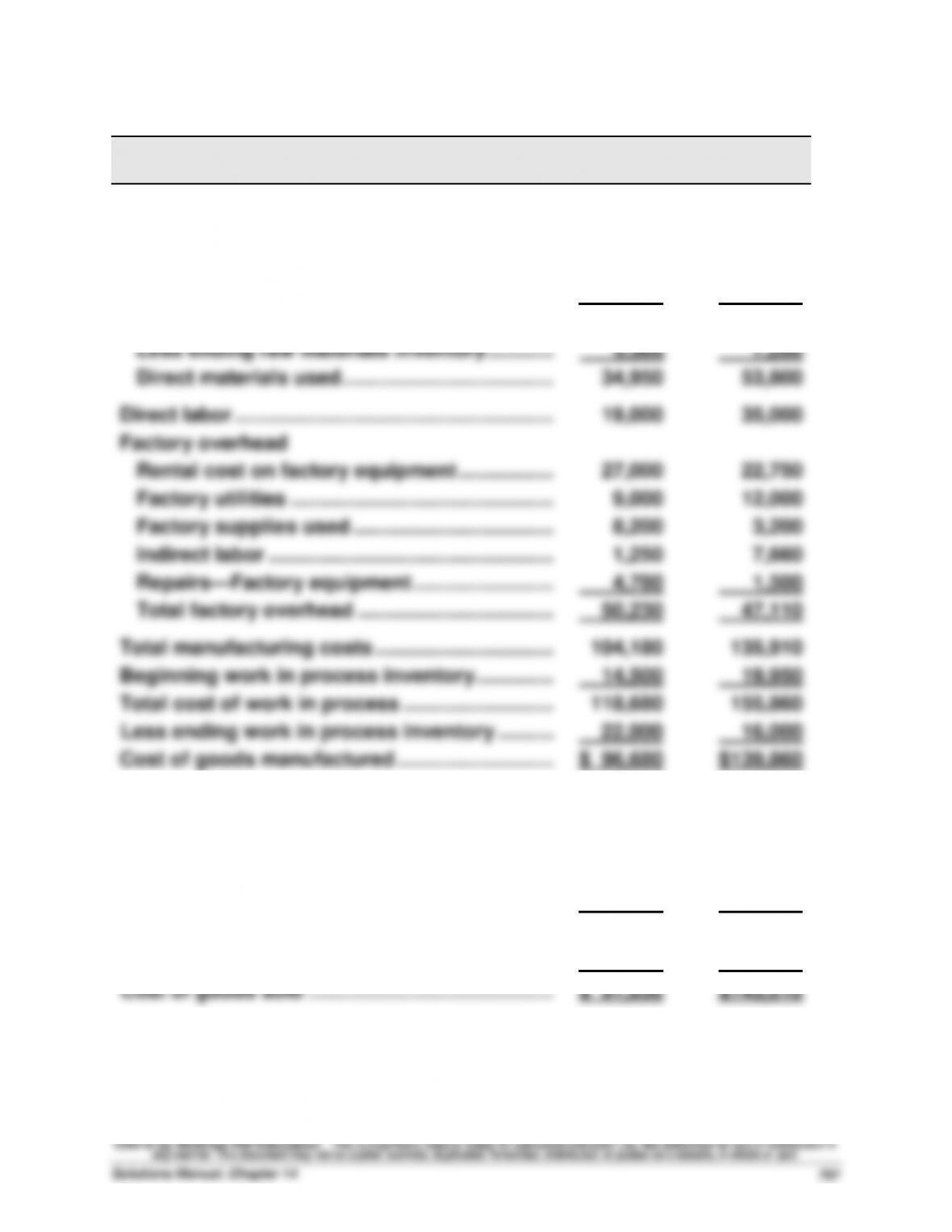

1. COST OF GOODS MANUFACTURED

Direct materials

Beginning raw materials inventory ……………..

$ 7,250

$ 9,000

Raw materials purchases …………………………..

33,000

52,000

Raw materials available for use ………………....

40,250

61,000

Less ending raw materials inventory …………..

5,300

7,200

Direct materials used…………………………..……..

34,950

53,800

Direct labor …………………………………………………..

19,000

35,000

Factory overhead

Rental cost on factory equipment ……………....

27,000

22,750

Factory utilities ………………………………………....

9,000

12,000

Factory supplies used ………………………………..

8,200

3,200

Indirect labor ……………………………………………..

1,250

7,660

Repairs—Factory equipment ……………………...

4,780

1,500

Total factory overhead ……………………………....

50,230

47,110

Total manufacturing costs …………………………..

104,180

135,910

Beginning work in process inventory …………....

14,500

19,950

Total cost of work in process ………………………..

118,680

155,860

Less ending work in process inventory ………...

22,000

16,000

Cost of goods manufactured ………………………...

$ 96,680

$139,860

2. COST OF GOODS SOLD

Beginning finished goods inventory ……………..

$ 12,000

$ 16,450

Cost of goods manufactured ………………………...

96,680

139,860

Cost of goods available for sale …………………....

108,680

156,310

Less ending finished goods inventory …………..

17,650

13,300

Cost of goods sold ……………………………………....

$ 91,030

$143,010

E EExercise 14–9 (30 minutes)

GARCON COMPANY

Income Statement

For Year Ended December 31, 2015

Sales …………………………………………………………………………….…..

$ 195,030

Cost of goods sold (from Ex. 14–8) ………………………………..…..

91,030

Gross profit ………………………………………………………………….…..

104,000

Operating expenses

Selling expenses ………………………………………………………….…..

General and administrative expenses …………………………..

50,000

21,000

Income before tax ……………………………………………………………..

$ 33,000

PEPPER COMPANY

Income Statement

For Year Ended December 31, 2015

Sales …………………………………………………………………………….…..

$ 290,010

Cost of goods sold (from Ex. 14–8) ………………………………..…..

143,010

Gross profit ………………………………………………………………….…..

147,000

Operating expenses

Selling expenses ………………………………………………………….…..

General and administrative expenses …………………………..

46,000

43,000

Income before tax ……………………………………………………………..

$ 58,000

Exercise 14–9 (continued)

GARCON COMPANY

Partial Balance Sheet

As of December 31, 2015

Cash ……………………………………………………………………….……..

$20,000

Accounts receivable, net………………………………………….……..

13,200

Inventories

Raw materials inventory…………………………..…………………..

$ 5,300

Work in process inventory …………………………………….……..

22,000

Finished goods inventory ……………………………………..……..

17,650

44,950

Total current assets ……………………………………………………….

$78,150

PEPPER COMPANY

Partial Balance Sheet

As of December 31, 2015

Cash ……………………………………………………………………….……..

$15,700

Accounts receivable, net…………………………..……………..……..

19,450

Inventories

Raw materials inventory…………………………..…………………..

$ 7,200

Work in process inventory …………………………………….……..

16,000

Finished goods inventory ……………………………………..……..

13,300

36,500

Total current assets ……………………………………………………….

$71,650

Exercise 14-10 (20 minutes)

Garcon

Company

Pepper

Company

1. PRIME COSTS

Direct materials

Beginning raw materials inventory ……………..

$ 7,250

$ 9,000

Raw materials purchases …………………………..

33,000

52,000

Raw materials available for use ………………....

40,250

61,000

Less ending raw materials inventory …………..

5,300

7,200

Direct materials used…………………………..……..

34,950

53,800

Direct labor …………………………………………………..

19,000

35,000

Total prime costs ………………………………………....

2. CONVERSION COSTS

Direct labor …………………………………………………..

Factory overhead

$53,950

$19,000

$88,800

$35,000

Rental cost on factory equipment ……………....

27,000

22,750

Factory utilities …………………………..……………..

9,000

12,000

Factory supplies used ………………………………..

8,200

3,200

Indirect labor ……………………………………………..

1,250

7,660

Repairs—Factory equipment ……………………...

4,780

1,500

Total factory overhead ……………………………....

50,230

47,110

Total conversion costs ………………………………....

$69,230

$82,110

Exercise 14–11 (20 minutes)

Merchandising Business

UNIMART

Partial Income Statement

For Year Ended December 31, 2015

Cost of goods sold

Merchandise inventory, December 31, 2014 …………………..…..

$ 275,000

Merchandise purchases ………………………………………………..…..

500,000

Goods available for sale…………………………..………………………..

775,000

Less merchandise inventory, December 31, 2015 …………..…..

115,000

Cost of goods sold …………………………..…………………………..

$ 660,000

Beginning Inventory 275,000

Purchases 500,000

Goods available for sale 775,000

660,000 Cost of Goods Sold

Ending Inventory 115,000

Merchandise Inventory

Exercise 14–11 (concluded)

Manufacturing Business

PRECISION MANUFACTURING

Partial Income Statement

For Year Ended December 31, 2015

Cost of goods sold

Finished goods inventory, December 31, 2014 ……………..…

$ 450,000

Cost of goods manufactured ……………………………………….…

900,000

Goods available for sale…………………………..………………….…

1,350,000

Less finished goods inventory, December 31, 2015 ……..…

375,000

Cost of goods sold …………………………..…………………………..

$ 975,000

Beginning Inventory 450,000

Cost of Goods Manufactured 900,000

Goods available for sale 1,350,000

975,000 Cost of Goods Sold

Ending Inventory 375,000

Finished Goods Inventory