Problem 10–10BB (Concluded)

Part 4

2015

June 30

Bond Interest Expense …………………………..

24,680

Premium on Bonds Payable ………………….……….

4,570

Cash ……………………………………………….………

29,250

To record six months’ interest and

premium amortization.

2015

Dec. 31

Bond Interest Expense …………………………..

24,452

Premium on Bonds Payable ………………….……….

4,798

Cash ……………………………………………….………

29,250

To record six months’ interest and

premium amortization.

Jan. 1

Bonds Payable …………………………………….……………….

450,000

Premium on Bonds Payable ………………….……….

23,912

Loss on Retirement of Bonds ……………….………….

3,088

Cash*…………………………..………………….……….

477,000

To record the retirement of bonds.

*($450,000 x 106%)

Part 6

If the market rate on the issue date had been 14% instead of 10%, the bonds

would have sold at a discount because the contract rate of 13% would have been

lower than the market rate.

Problem 10–11BD (35 minutes)

Part 1

Present Value of the Lease Payments

$20,000 x 3.7908 (from Table B.3) = $75,816

Part 2

Leased Asset—Office Equipment ……………………….….

75,816

Lease Liability ………………………………………………….

75,816

To record capital lease of office equipment.

Part 3

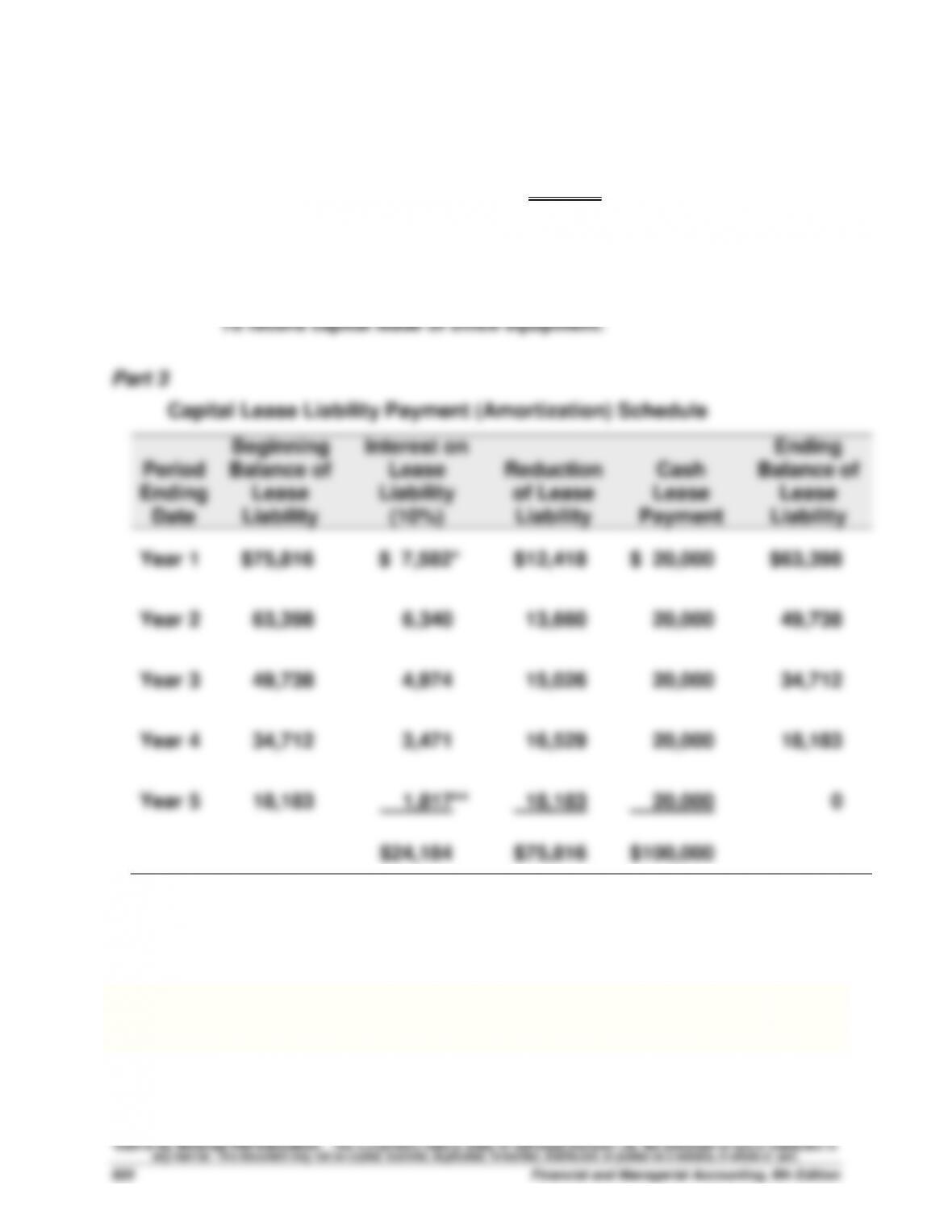

Capital Lease Liability Payment (Amortization) Schedule

Period

Ending

Date

Beginning

Balance of

Lease

Liability

Interest on

Lease

Liability

(10%)

Reduction

of Lease

Liability

Cash

Lease

Payment

Ending

Balance of

Lease

Liability

Year 1

$75,816

$ 7,582*

$12,418

$ 20,000

$63,398

Year 2

63,398

6,340

13,660

20,000

49,738

Year 3

49,738

4,974

15,026

20,000

34,712

Year 4

34,712

3,471

16,529

20,000

18,183

Year 5

18,183

1,817**

18,183

20,000

0

$24,184

$75,816

$100,000

* Rounded to nearest dollar.

** Adjusted for prior period rounding errors.

Part 4

Depreciation Expense—Leased Asset, Off. Equip ………..……..

15,163

Accum. Depreciation—Leased Asset, Off. Equip …….……..

15,163

To record depreciation ($75,816 / 5 years).

b. Equity

$119,393 / ($120,268 + $94,639) = 55.6%

Part 3

Santana Rey should understand the risks she is taking by borrowing funds

from the bank. She currently has no interest–bearing debt (per prior chapter

serial problems), but the loan will require her to pay interest. The interest

is a fixed cost that must be paid, no matter what her profits are. She must

due.

1. Apple reported long-term debt of $16,960 million as of September 28,

2013.

2. The interest that Apple must pay on $100 million of 4.25% convertible

3. Assuming that Apple had $100 million carrying value of convertible

bonds that convert into 20,000 shares of stock, the following entry

4. Answer depends on the financial statement information obtained.

1. Apple’s current year debt–to-equity ratio = $83,451 / $123,549 = 0.68

2. For both years, Apple’s debt–to-equity ratio is above that of the industry

average of 0.44. This implies that its debt levels are more risky than that

1. The ethics of the Traverse County officials are questionable. The

financial impact of the leasing arrangement is the same as bond

financing in that the county has a debt obligation requiring the

repayment of principal and interest over time. Taxes may need to be

2. Because the lease requires payments of a non–binding nature, investors

who purchased the tax-exempt securities from the bank are holding an

investment that is more risky than the conventional municipal bonds of

Traverse County.

Communicating in Practice — BTN 10-4