Problem 10-4B (Concluded)

Part 3

2015

June 30

Bond Interest Expense …………………………..

13,101

Premium on Bonds Payable ………………….……….

1,299

Cash ……………………………………………….………

14,400

To record six months’ interest and

premium amortization.

2015

Dec. 31

Bond Interest Expense …………………………..

13,101

Premium on Bonds Payable ………………….……….

1,299

Cash ……………………………………………….………

14,400

To record six months’ interest and

premium amortization.

Problem 10-5B (60 minutes)

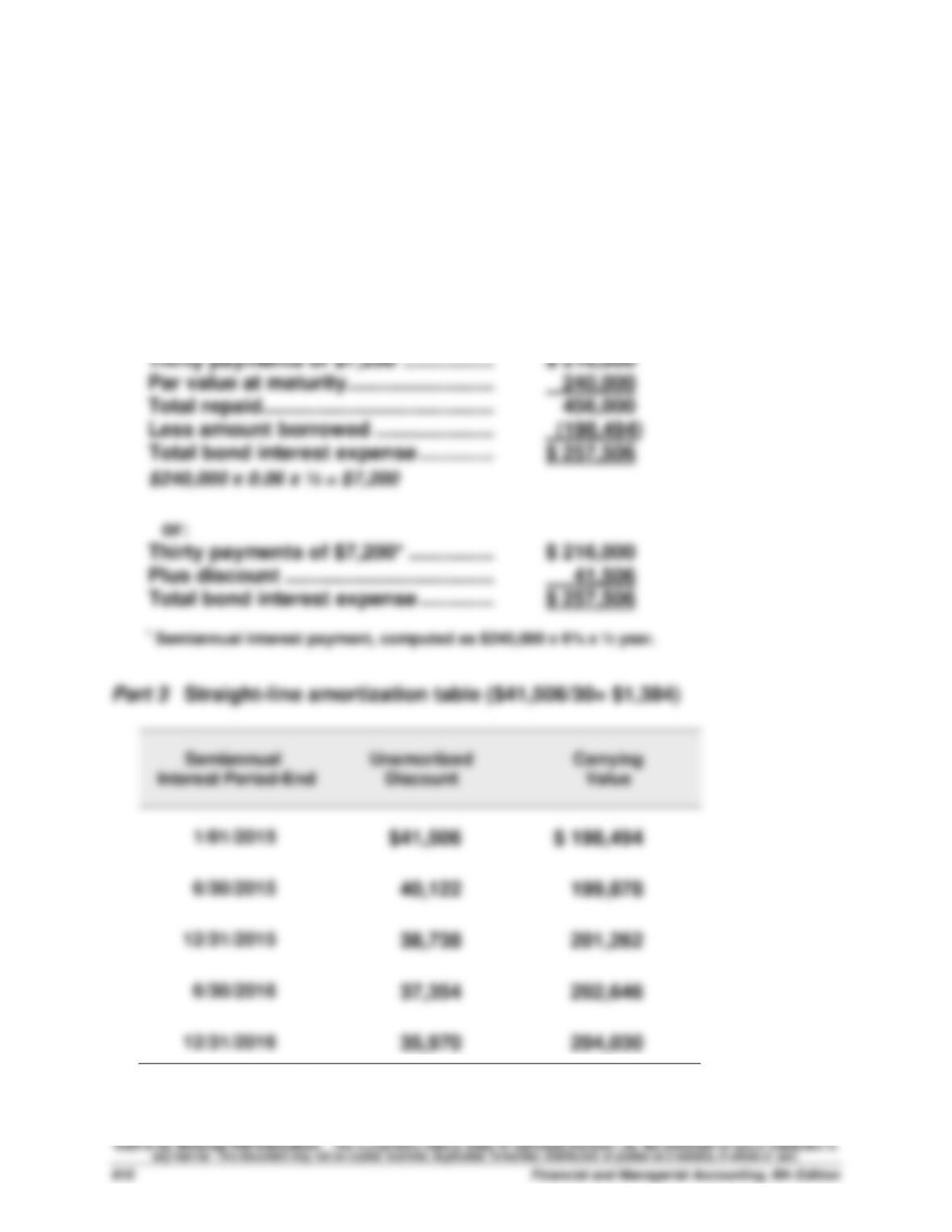

Part 1

2015

Jan. 1

Cash …………………………………………………….…

198,494

Discount on Bonds Payable ………………….……….

41,506

Bonds Payable ………………………………..……………….

240,000

Sold bonds on stated issue date.

Part 2

Thirty payments of $7,200* ……………..…….

$ 216,000

Par value at maturity…………………………..

240,000

Total repaid ………………………………………….

456,000

Less amount borrowed ………………….…….

(198,494)

Total bond interest expense …………..…….

$ 257,506

$240,000 x 0.06 x ½ = $7,200

or:

Thirty payments of $7,200* …………….…….

$ 216,000

Plus discount ………………………………..…….

41,506

Total bond interest expense …………..…….

$ 257,506

* Semiannual interest payment, computed as $240,000 x 6% x ½ year.

Part 3 Straight-line amortization table ($41,506/30= $1,384)

Semiannual

Interest Period-End

Unamortized

Discount

Carrying

Value

1/01/2015

$41,506

$ 198,494

6/30/2015

40,122

199,878

12/31/2015

38,738

201,262

6/30/2016

37,354

202,646

12/31/2016

35,970

204,030

Problem 10-5B (Concluded)

Part 4

2015

June 30

Bond Interest Expense …………………………..

8,584

Discount on Bonds Payable …………….…………….

1,384

Cash ……………………………………………….………

7,200

To record six months’ interest and

discount amortization.

2015

Dec. 31

Bond Interest Expense …………………………..

8,584

Discount on Bonds Payable …………….…………….

1,384

Cash ……………………………………………….………

7,200

To record six months’ interest and

discount amortization.

Problem 10-6B (45 minutes)

Part 1 Amount of Payment

Note balance ………………………………………..……………..

$150,000

Number of periods ………………………………..……………….

3

Interest rate ………………………………………….……………

10%

Value from Table B.3 …………………………….……………….

2.4869

Payment ($150,000 / 2.4869) ………………….……….

$ 60,316

Part 2

Payments

Period

Ending

Date

(A)

Beginning

Balance

[Prior (E)]

(B)

Debit

Interest

Expense

[10% x (A)]

+

(C)

Debit

Notes

Payable

[(D) – (B)]

=

(D)

Credit

Cash

[computed]

(E)

Ending

Balance

[(A) – (C)]

9/30/2016 ………….

$150,000

$15,000

$ 45,316

$ 60,316

$104,684

9/30/2017 ………….

104,684

10,468

49,848

60,316

54,836

9/30/2018 ………….

54,836

5,480*

54,836

60,316

0

$30,948

$150,000

$180,948

*Adjusted for rounding.

Part 3

2015

Dec. 31

Interest Expense …………………………..………………..……..

3,750

Interest Payable …………………………..…………………..

3,750

Accrued interest on the installment

note payable ($15,000 x 3/12).

2016

Sept. 30

Interest Expense …………………………..………………..……..

11,250

Interest Payable ……………………………………………..……..

3,750

Notes Payable …………………………..…………………………..

45,316

Cash ………………………………………………………………..

60,316

Record first payment on installment note

(interest expense = $15,000 – $3,750).

Problem 10-7B (30 minutes)

Part 1

Atlas Company

Debt–to-equity ratio = $80,000 / $100,000 = 0.80

Problem 10-8BB (60 minutes)

Part 1

2015

Jan. 1

Cash …………………………………………………….…

198,494

Discount on Bonds Payable ………………….……….

41,506

Bonds Payable ………………………………..……………….

240,000

Sold bonds on stated issue date.

Part 2

Thirty payments of $7,200* ……………..…….

$ 216,000

Par value at maturity…………………………..

240,000

Total repaid ………………………………………….

456,000

Less amount borrowed ………………….…….

(198,494)

Total bond interest expense …………..…….

$ 257,506

*$240,000 x 0.06 x ½ = $7,200

or:

Thirty payments of $7,200 …………………….

$ 216,000

Plus discount ………………………………..…….

41,506

Total bond interest expense …………..…….

$ 257,506

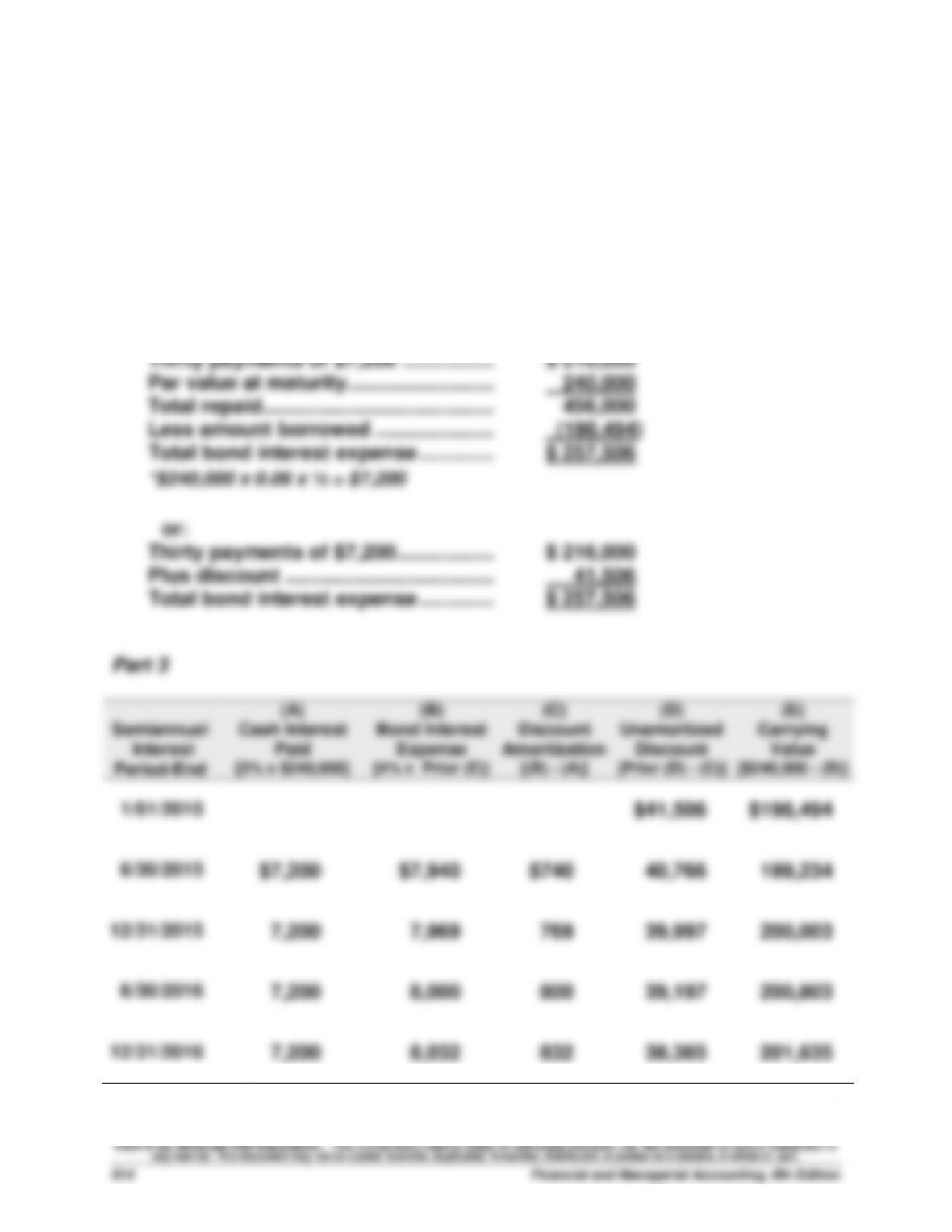

Part 3

Semiannual

Interest

Period-End

(A)

Cash Interest

Paid

[3% x $240,000]

(B)

Bond Interest

Expense

[4% x Prior (E)]

(C)

Discount

Amortization

[(B) – (A)]

(D)

Unamortized

Discount

[Prior (D) – (C)]

(E)

Carrying

Value

[$240,000 – (D)]

1/01/2015

$41,506

$198,494

6/30/2015

$7,200

$7,940

$740

40,766

199,234

12/31/2015

7,200

7,969

769

39,997

200,003

6/30/2016

7,200

8,000

800

39,197

200,803

12/31/2016

7,200

8,032

832

38,365

201,635

Problem 10-8BB (Concluded)

Part 4

2015

June 30

Bond Interest Expense …………………………..

7,940

Discount on Bonds Payable …………….…………….

740

Cash ……………………………………………….………

7,200

To record six months’ interest and

discount amortization.

2015

Dec. 31

Bond Interest Expense …………………………..

7,969

Discount on Bonds Payable …………….…………….

769

Cash ……………………………………………….………

7,200

To record six months’ interest and

discount amortization.

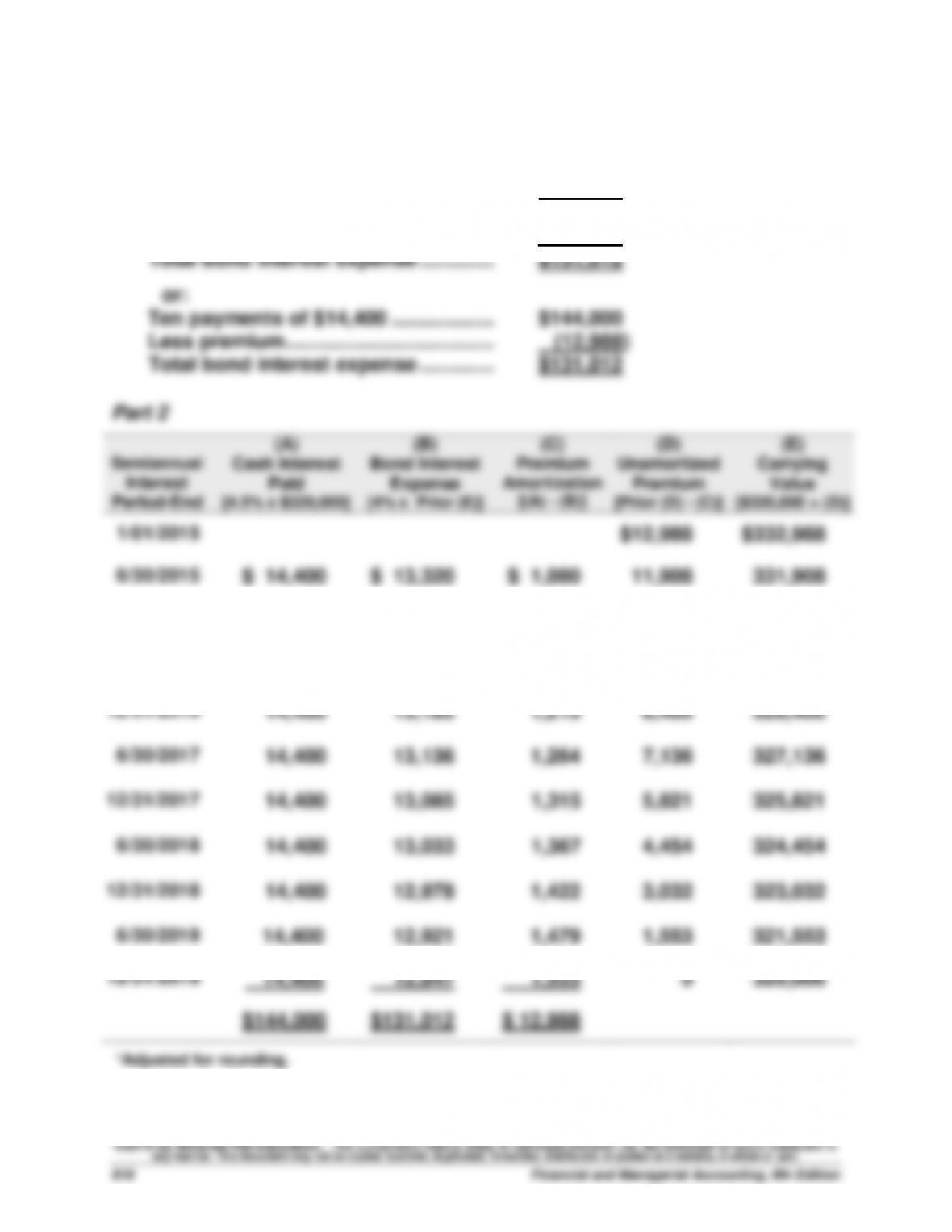

Problem 10-9BB (45 minutes)

Part 1

Ten payments of $14,400 ……………….…….

$144,000

Par value at maturity…………………………..

320,000

Total repaid ………………………………………….

464,000

Less amount borrowed ………………….…….

(332,988)

Total bond interest expense …………..…….

$131,012

or:

Ten payments of $14,400 ……………….…….

$144,000

Less premium ………………………………..…….

(12,988)

Total bond interest expense …………..…….

$131,012

Part 2

Semiannual

Interest

Period-End

(A)

Cash Interest

Paid

[4.5% x $320,000]

(B)

Bond Interest

Expense

[4% x Prior (E)]

(C)

Premium

Amortization

[(A) – (B)]

(D)

Unamortized

Premium

[Prior (D) – (C)]

(E)

Carrying

Value

[$320,000 + (D)]

1/01/2015

$12,988

$332,988

6/30/2015

$ 14,400

$ 13,320

$ 1,080

11,908

331,908

12/31/2015

14,400

13,276

1,124

10,784

330,784

6/30/2016

14,400

13,231

1,169

9,615

329,615

12/31/2016

14,400

13,185

1,215

8,400

328,400

6/30/2017

14,400

13,136

1,264

7,136

327,136

12/31/2017

14,400

13,085

1,315

5,821

325,821

6/30/2018

14,400

13,033

1,367

4,454

324,454

12/31/2018

14,400

12,978

1,422

3,032

323,032

6/30/2019

14,400

12,921

1,479

1,553

321,553

12/31/2019

14,400

12,847*

1,553

0

320,000

$144,000

$131,012

$ 12,988

*Adjusted for rounding.

Problem 10-9BB (Concluded)

Part 3

2015

June 30

Bond Interest Expense …………………………..

13,320

Premium on Bonds Payable ………………….……….

1,080

Cash ……………………………………………….………

14,400

To record six months’ interest and

premium amortization.

1,124

To record six months’ interest and

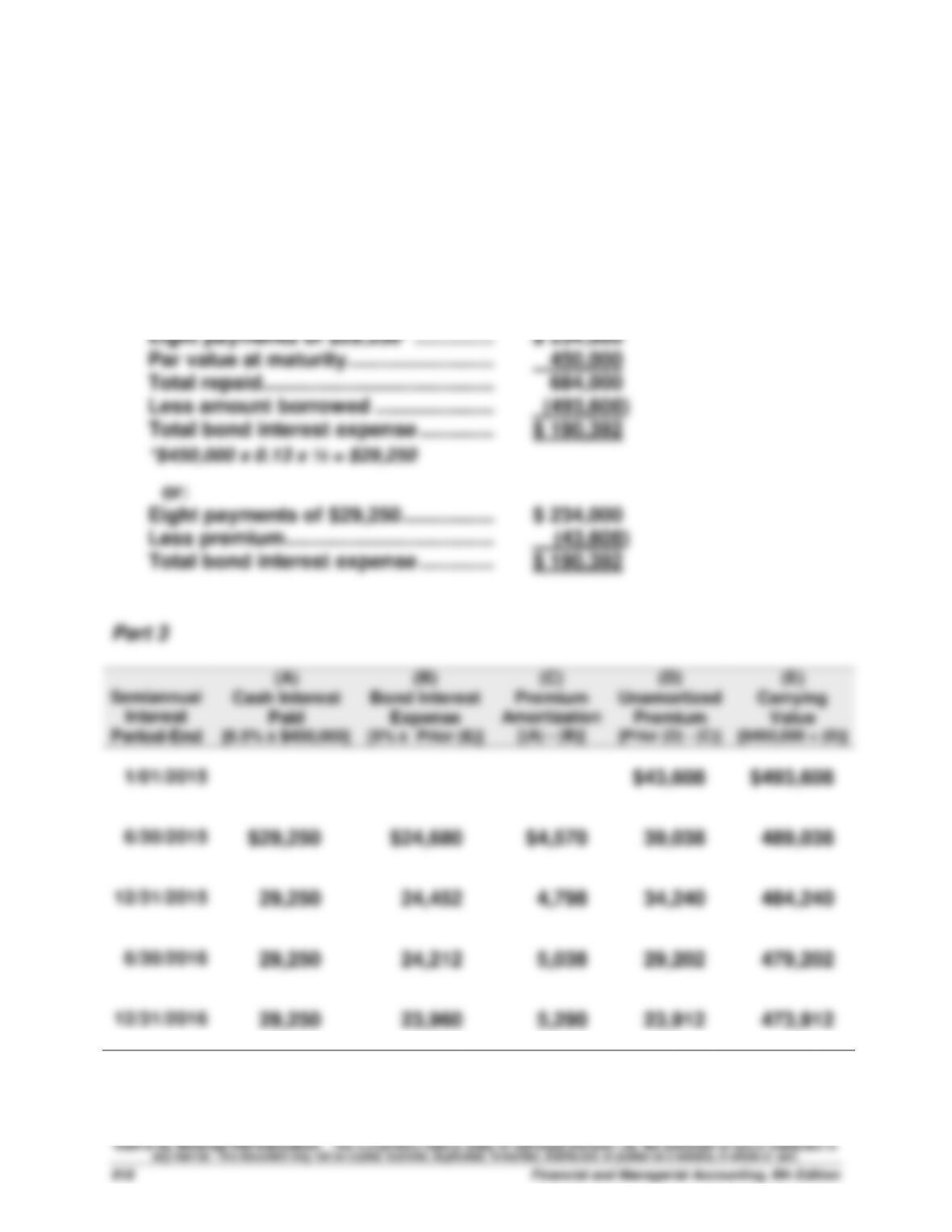

Problem 10–10BB (70 minutes)

Part 1

2015

Jan. 1

Cash …………………………………………………….…

493,608

Premium on Bonds Payable …………….…………….

43,608

Bonds Payable ………………………………..……………….

450,000

Sold bonds on stated issue date.

Part 2

Eight payments of $29,250* ………………….

$ 234,000

Par value at maturity…………………………..

450,000

Total repaid ………………………………………….

684,000

Less amount borrowed ………………….…….

(493,608)

Total bond interest expense …………..…….

$ 190,392

*$450,000 x 0.13 x ½ = $29,250

or:

Eight payments of $29,250 ……………..…….

$ 234,000

Less premium ………………………………..…….

(43,608)

Total bond interest expense …………..…….

$ 190,392

Part 3

Semiannual

Interest

Period-End

(A)

Cash Interest

Paid

[6.5% x $450,000]

(B)

Bond Interest

Expense

[5% x Prior (E)]

(C)

Premium

Amortization

[(A) – (B)]

(D)

Unamortized

Premium

[Prior (D) – (C)]

(E)

Carrying

Value

[$450,000 + (D)]

1/01/2015

$43,608

$493,608

6/30/2015

$29,250

$24,680

$4,570

39,038

489,038

12/31/2015

29,250

24,452

4,798

34,240

484,240

6/30/2016

29,250

24,212

5,038

29,202

479,202

12/31/2016

29,250

23,960

5,290

23,912

473,912