Problem 10–9AB (Concluded)

Part 3

2015

June 30

Bond Interest Expense …………………………..

7,660

Premium on Bonds Payable ………………….……….

465

Cash ……………………………………………….………

8,125

To record six months’ interest and

premium amortization.

Problem 10-10AB (60 minutes)

Part 1

2015

Jan. 1

Cash …………………………………………………….…

184,566

Premium on Bonds Payable …………….…………….

4,566

Bonds Payable ………………………………..……………….

180,000

Sold bonds on stated issue date.

Part 2

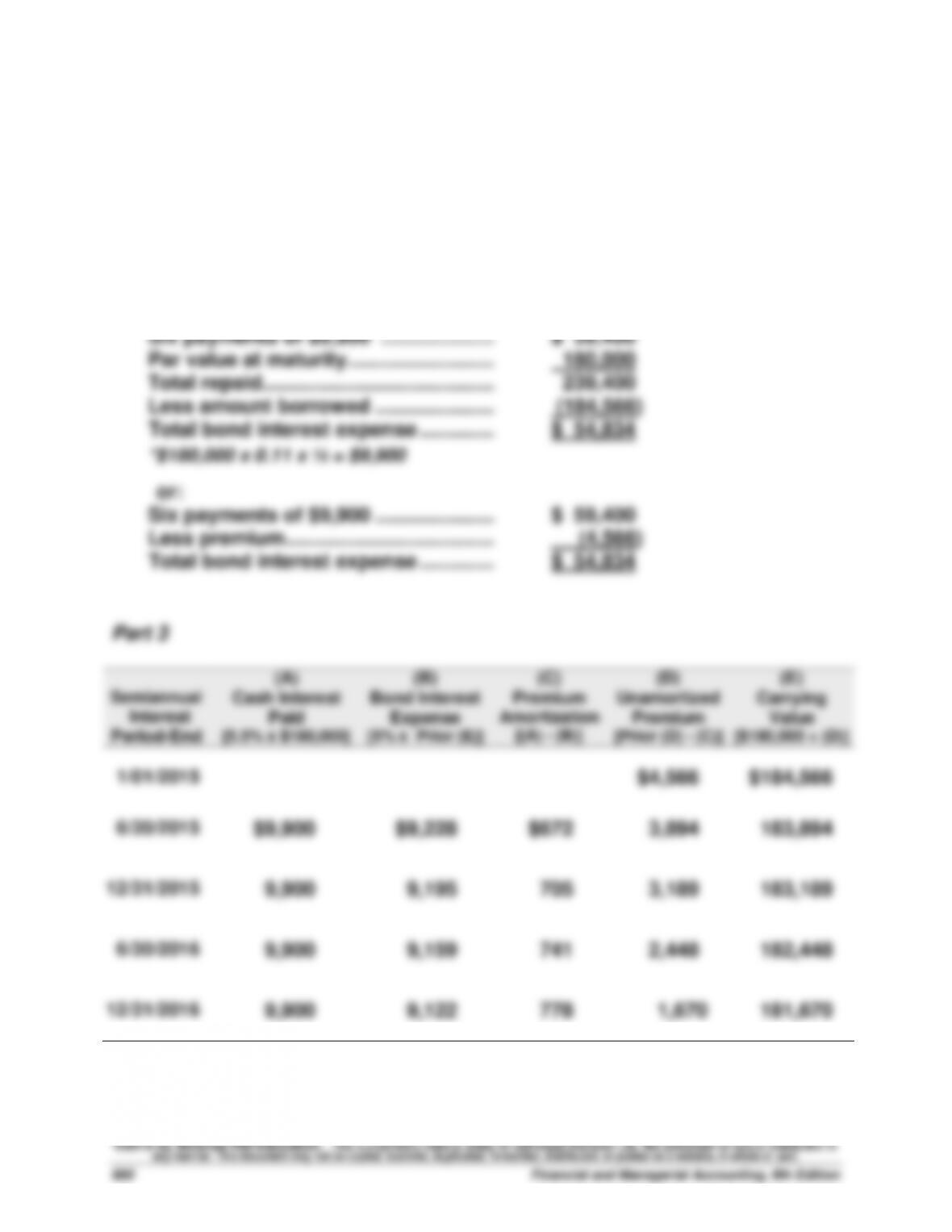

Six payments of $9,900 ……………………….

$ 59,400

Par value at maturity…………………………..

180,000

Total repaid ………………………………………….

239,400

Less amount borrowed ………………….…….

(184,566)

Total bond interest expense …………..…….

$ 54,834

*$180,000 x 0.11 x ½ = $9,900

or:

Six payments of $9,900 ………………….…….

$ 59,400

Less premium ………………………………..…….

(4,566)

Total bond interest expense …………..…….

$ 54,834

Part 3

Semiannual

Interest

Period-End

(A)

Cash Interest

Paid

[5.5% x $180,000]

(B)

Bond Interest

Expense

[5% x Prior (E)]

(C)

Premium

Amortization

[(A) – (B)]

(D)

Unamortized

Premium

[Prior (D) – (C)]

(E)

Carrying

Value

[$180,000 + (D)]

1/01/2015

$4,566

$184,566

6/30/2015

$9,900

$9,228

$672

3,894

183,894

12/31/2015

9,900

9,195

705

3,189

183,189

6/30/2016

9,900

9,159

741

2,448

182,448

12/31/2016

9,900

9,122

778

1,670

181,670

Problem 10-10AB (Concluded)

Part 4

2015

June 30

Bond Interest Expense …………………………..

9,228

Premium on Bonds Payable ………………….……….

672

Cash ……………………………………………….………

9,900

To record six months’ interest and

premium amortization.

2015

Dec. 31

Bond Interest Expense …………………………..

9,195

Premium on Bonds Payable ………………….……….

705

Cash ……………………………………………….………

9,900

To record six months’ interest and

premium amortization.

Jan. 1

Bonds Payable …………………………………….……………….

180,000

Premium on Bonds Payable ………………….……….

1,670

Cash*…………………………..………………….……….

176,400

Gain on Retirement of Bonds …………..………………

5,270

To record the retirement of bonds.

*($180,000 x 98%)

Part 6

If the market rate on the issue date had been 12% instead of 10%, the bonds

would have sold at a discount because the contract rate of 11% would have been

lower than the market rate.

Problem 10–11AD (35 minutes)

Part 1

Present Value of the Lease Payments

$10,000 x 3.9927 (from Table B.3) = $39,927

Part 2

Leased Asset—Office Equipment ……………………….….

39,927

Lease Liability ………………………………………………….

39,927

To record capital lease of office equipment.

Part 3

Capital Lease Liability Payment (Amortization) Schedule

Period

Ending

Date

Beginning

Balance of

Lease

Liability

Interest on

Lease

Liability

(8%)

Reduction

of Lease

Liability

Cash

Lease

Payment

Ending

Balance of

Lease

Liability

Year 1

$39,927

$ 3,194*

$ 6,806

$ 10,000

$33,121

Year 2

33,121

2,650

7,350

10,000

25,771

Year 3

25,771

2,062

7,938

10,000

17,833

Year 4

17,833

1,427

8,573

10,000

9,260

Year 5

9,260

740**

9,260

10,000

0

$10,073

$39,927

$ 50,000

* Rounded to nearest dollar.

** Difference due to rounding.

Part 4

Depreciation Expense—Leased Asset, Off. Equip ……………….

7,985

Accum. Depreciation—Leased Asset, Off. Equip ……..…….

7,985

To record depreciation ($39,927 / 5 years).

Problem 10-1B (50 minutes)

Part 1

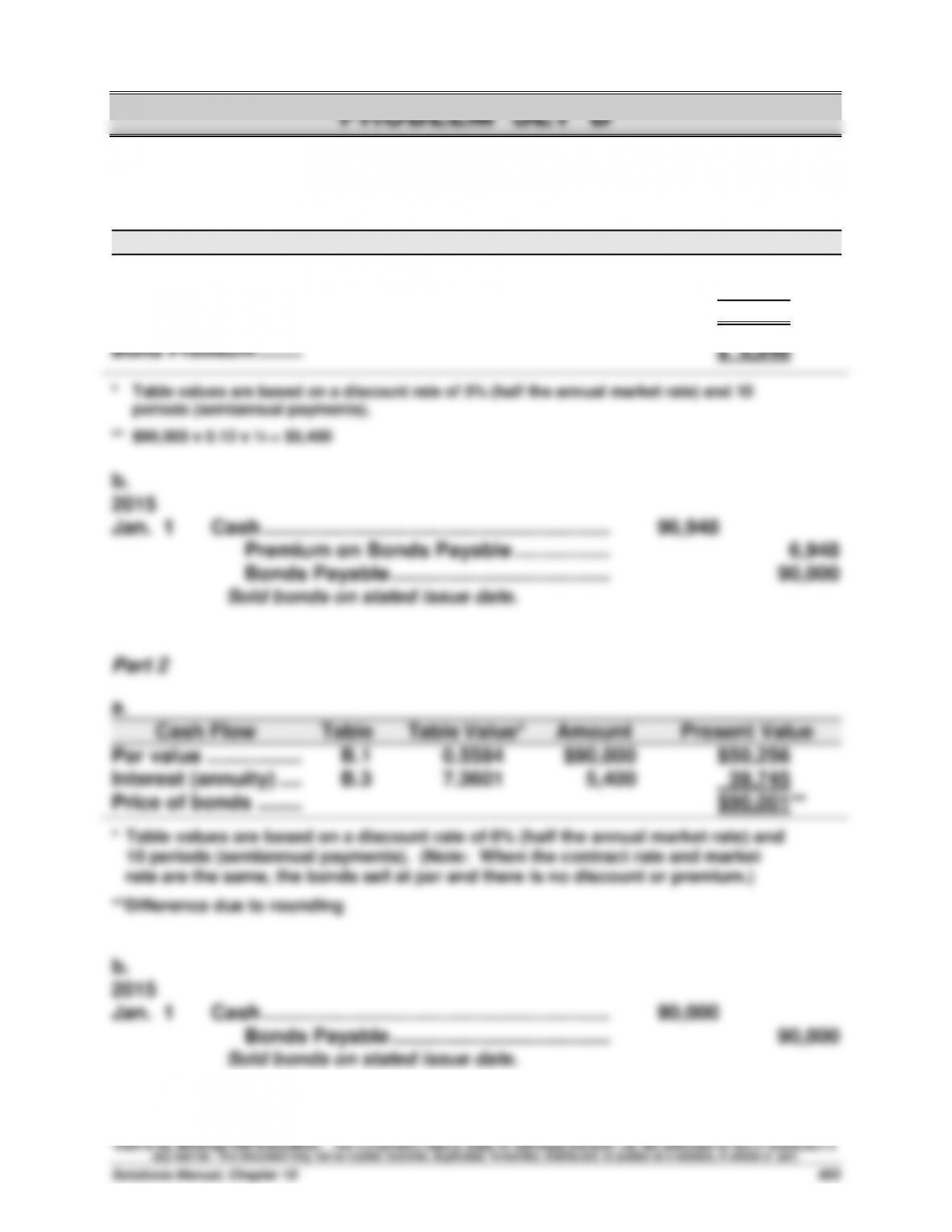

a.

Cash Flow

Table

Table Value*

Amount

Present Value

Par value ……………..

B.1

0.6139

$90,000

$55,251

Interest (annuity) ….

B.3

7.7217

5,400**

41,697

Price of bonds ……..

$96,948

Bond Premium ……..

$ 6,948

* Table values are based on a discount rate of 5% (half the annual market rate) and 10

periods (semiannual payments).

** $90,000 x 0.12 x ½ = $5,400

b.

2015

Jan. 1

Cash ……………………………………………………....

96,948

Premium on Bonds Payable ……………..……………

6,948

Bonds Payable …………………………………………………

90,000

Sold bonds on stated issue date.

Part 2

a.

Cash Flow

Table

Table Value*

Amount

Present Value

Par value ……………..

B.1

0.5584

$90,000

$50,256

Interest (annuity) ….

B.3

7.3601

5,400

39,745

Price of bonds ……..

$90,001**

* Table values are based on a discount rate of 6% (half the annual market rate) and

10 periods (semiannual payments). (Note: When the contract rate and market

rate are the same, the bonds sell at par and there is no discount or premium.)

**Difference due to rounding

b.

2015

Jan. 1

Cash ……………………………………………………....

90,000

Bonds Payable …………………………………………………

90,000

Sold bonds on stated issue date.

Problem 10-1B (Concluded)

Part 3

a.

Cash Flow

Table

Table Value*

Amount

Present Value

Par value ……………..

B.1

0.5083

$90,000

$45,747

Interest (annuity) ….

B.3

7.0236

5,400

37,927

Price of bonds ……..

$83,674

Bond discount ……..

$ 6,326

* Table values are based on a discount rate of 7% (half the annual market rate)

and 10 periods (semiannual payments).

b.

2015

Jan. 1

Cash ……………………………………………………....

83,674

Discount on Bonds Payable …………………..………

6,326

Bonds Payable …………………………………………………

90,000

Sold bonds on stated issue date.

Problem 10-2B (40 minutes)

Part 1

2015

Jan. 1

Cash ……………………………………………………....

3,010,000

Discount on Bonds Payable …………………..………

390,000

Bonds Payable …………………………………………………

3,400,000

Sold bonds on stated issue date.

Part 2

[Note: The semiannual amounts for (a), (b), and (c) below are the same throughout

the bonds’ life because the company uses straight-line amortization.]

(a) Cash Payment = $3,400,000 x 10% x 6/12 year = $170,000

(b) Discount = $3,400,000 – $3,010,000 = $390,000

Straight–line discount amortization = $390,000 / 20 semiannual periods

= $19,500

(c) Bond interest expense = $170,000 + $19,500 = $189,500

Problem 10-2B (Concluded)

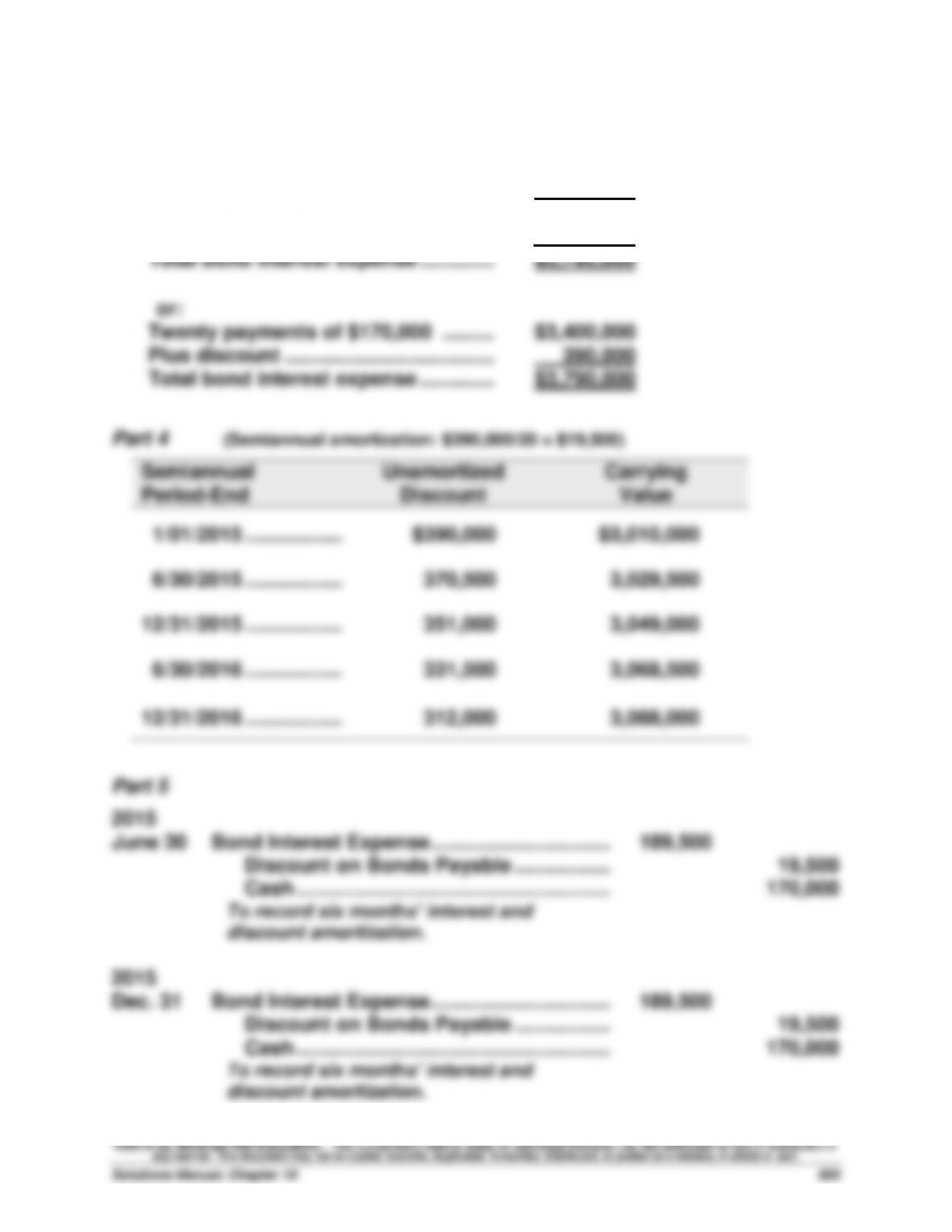

Part 3

Twenty payments of $170,000 ………..…….

$3,400,000

Par value at maturity…………………………..

3,400,000

Total repaid ………………………………………….

6,800,000

Less amount borrowed ………………….…….

(3,010,000)

Total bond interest expense …………..…….

$3,790,000

or:

Twenty payments of $170,000 ……….…….

$3,400,000

Plus discount ………………………………..…….

390,000

Total bond interest expense …………..…….

$3,790,000

Part 4 (Semiannual amortization: $390,000/20 = $19,500)

Semiannual

Period–End

Unamortized

Discount

Carrying

Value

1/01/2015 …………………

$390,000

$3,010,000

6/30/2015 …………………

370,500

3,029,500

12/31/2015 …………………

351,000

3,049,000

6/30/2016 …………………

331,500

3,068,500

12/31/2016 …………………

312,000

3,088,000

Part 5

2015

June 30

Bond Interest Expense …………………………..

189,500

Discount on Bonds Payable ……………..……………

19,500

Cash ………………………………………………..……..

170,000

To record six months’ interest and

discount amortization.

2015

Dec. 31

Bond Interest Expense …………………………..

189,500

Discount on Bonds Payable ……………..……………

19,500

Cash ………………………………………………..……..

170,000

To record six months’ interest and

discount amortization.

Problem 10-3B (40 minutes)

Part 1

2015

Jan. 1

Cash …………………………………………………….…

4,192,932

Premium on Bonds Payable …………….…………….

792,932

Bonds Payable ………………………………..……………….

3,400,000

Sold bonds on issue date at a premium.

Part 2

(a) Cash Payment = $3,400,000 x 10% x 6/12 year = $170,000

(b) Premium = $4,192,932 – $3,400,000 = $792,932

Straight–line premium amortization= $792,932/20 semiannual periods

= $ 39,647 rounded

(c) Bond interest expense = $170,000 – $39,647 = $130,353

Part 3

Twenty payments of $170,000 ………..…….

$3,400,000

Par value at maturity…………………………..

3,400,000

Total repaid ………………………………………….

6,800,000

Less amount borrowed ………………….…….

(4,192,932)

Total bond interest expense …………..…….

$2,607,068

or:

Twenty payments of $170,000 ………..…….

$3,400,000

Less premium ………………………………..…….

(792,932)

Total bond interest expense …………..…….

$2,607,068

Problem 10-3B (Concluded)

Part 4

Semiannual

Period–End

Unamortized

Premium

Carrying

Value

1/01/2015 ………….……..

$792,932

$4,192,932

6/30/2015 ………….……..

753,285

4,153,285

12/31/2015 ………….……..

713,638

4,113,638

6/30/2016 ………….……..

673,991

4,073,991

12/31/2016 ………….……..

634,344

4,034,344

Part 5

2015

June 30

Bond Interest Expense …………………………..

130,353

Premium on Bonds Payable ………………….……….

39,647

Cash ……………………………………………….………

170,000

To record six months’ interest and

premium amortization.

2015

Dec. 31

Bond Interest Expense …………………………..

130,353

Premium on Bonds Payable ………………….……….

39,647

Cash ……………………………………………….………

170,000

To record six months’ interest and

premium amortization.

Problem 10-4B (45 minutes)

Part 1

Ten payments of $14,400* …………………….

$ 144,000

Par value at maturity…………………………..

320,000

Total repaid ………………………………………….

464,000

Less amount borrowed ………………….…….

(332,988)

Total bond interest expense …………..…….

$ 131,012

*$320,000 x 0.09 x ½ = $14,400

or:

Ten payments of $14,400 ……………….…….

$ 144,000

Less premium ………………………………..…….

(12,988)

Total bond interest expense …………..…….

$ 131,012

Part 2

Straight-line amortization table ($12,988/10 = $1,299**)

Semiannual

Interest Period-End

Unamortized

Premium

Carrying

Value

1/01/2015

$12,988

$332,988

6/30/2015

11,689

331,689

12/31/2015

10,390

330,390

6/30/2016

9,091

329,091

12/31/2016

7,792

327,792

6/30/2017

6,493

326,493

12/31/2017

5,194

325,194

6/30/2018

3,895

323,895

12/31/2018

2,596

322,596

6/30/2019

1,299*

321,299

12/31/2019

0

320,000