Problem 10-3A (Concluded)

Part 4

Semiannual

Period–End

Unamortized

Premium

Carrying

Value

1/01/2015 …………………

$895,980

$4,895,980

6/30/2015 …………………

866,114

4,866,114

12/31/2015 …………………

836,248

4,836,248

6/30/2016 …………………

806,382

4,806,382

12/31/2016 …………………

776,516

4,776,516

Part 5

2015

June 30

Bond Interest Expense …………………………..

90,134

Premium on Bonds Payable ………………….……….

29,866

Cash ……………………………………………….………

120,000

To record six months’ interest and

premium amortization.

2015

Dec. 31

Bond Interest Expense …………………………..

90,134

Premium on Bonds Payable ………………….……….

29,866

Cash ……………………………………………….………

120,000

To record six months’ interest and

premium amortization.

Problem 10-4A (45 minutes)

Part 1

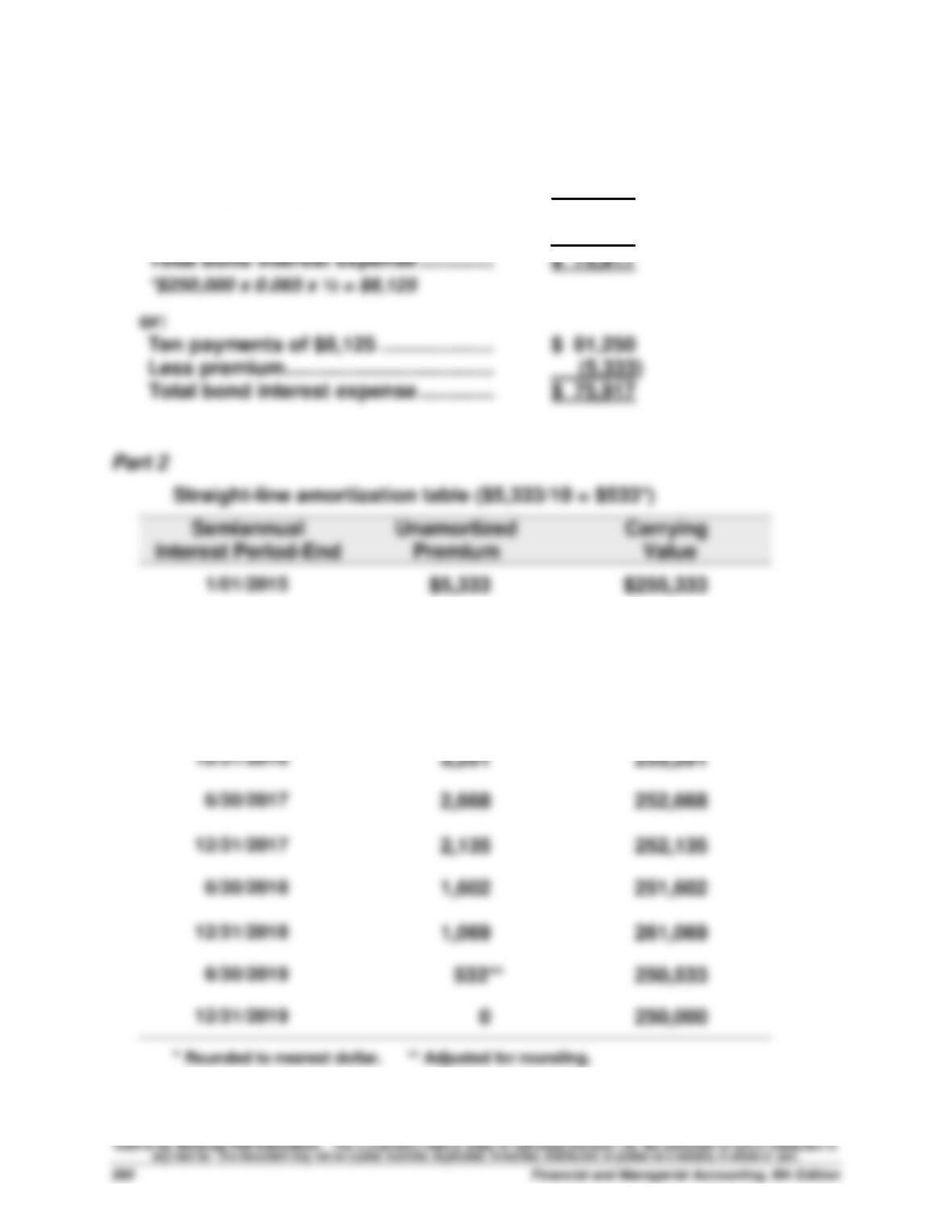

Ten payments of $8,125* ……………….…….

$ 81,250

Par value at maturity…………………………..

250,000

Total repaid ………………………………………….

331,250

Less amount borrowed ………………….…….

(255,333)

Total bond interest expense …………..…….

$ 75,917

*$250,000 x 0.065 x ½ = $8,125

or:

Ten payments of $8,125 ……………………….

$ 81,250

Less premium ………………………………..…….

(5,333)

Total bond interest expense …………..…….

$ 75,917

Part 2

Straight-line amortization table ($5,333/10 = $533*)

Semiannual

Interest Period-End

Unamortized

Premium

Carrying

Value

1/01/2015

$5,333

$255,333

6/30/2015

4,800

254,800

12/31/2015

4,267

254,267

6/30/2016

3,734

253,734

12/31/2016

3,201

253,201

6/30/2017

2,668

252,668

12/31/2017

2,135

252,135

6/30/2018

1,602

251,602

12/31/2018

1,069

261,069

6/30/2019

533**

250,533

12/31/2019

0

250,000

* Rounded to nearest dollar. ** Adjusted for rounding.

Problem 10-4A (Concluded)

Part 3

2015

June 30

Bond Interest Expense …………………………..

7,592

Premium on Bonds Payable ………………….……….

533

Cash ……………………………………………….………

8,125

To record six months’ interest and

premium amortization.

2015

Dec. 31

Bond Interest Expense …………………………..

7,592

Premium on Bonds Payable ………………….……….

533

Cash ……………………………………………….………

8,125

To record six months’ interest and

premium amortization.

Problem 10-5A (60 minutes)

Part 1

2015

Jan. 1

Cash …………………………………………………….…

292,181

Discount on Bonds Payable ………………….……….

32,819

Bonds Payable ………………………………..……………….

325,000

Sold bonds on stated issue date.

Part 2

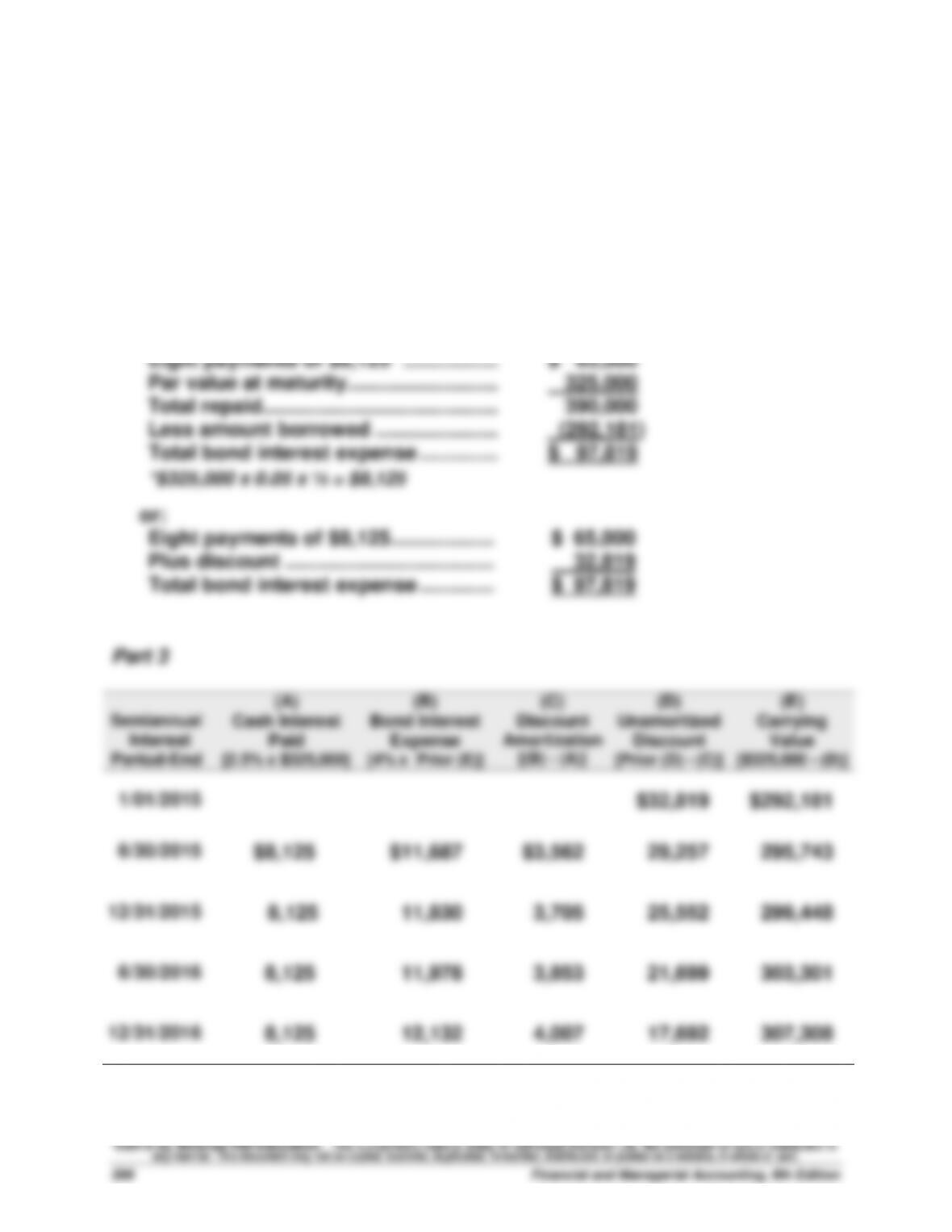

Eight payments of $8,125* ……………....

$ 65,000

Par value at maturity………………………..

325,000

Total repaid ……………………………………..

390,000

Less amount borrowed …………………...

(292,181)

Total bond interest expense …………....

$ 97,819

*$325,000 x 0.05 x ½ = $8,125

or:

Eight payments of $8,125 ………………...

$ 65,000

Plus discount ………………………………....

32,819

Total bond interest expense …………....

$ 97,819

Part 3 Straight-line amortization table ($32,819/8 =$4,102*)

Semiannual

Interest Period-End

Unamortized

Discount

Carrying

Value

1/01/2015

$32,819

$292,181

6/30/2015

28,717

296,283

12/31/2015

24,615

300,385

6/30/2016

20,513

304,487

12/31/2016

16,411

308,589

*(rounded to nearest dollar)

Problem 10–5A (Concluded)

Part 4

2015

June 30

Bond Interest Expense …………………………..

12,227

Discount on Bonds Payable …………….…………….

4,102

Cash ……………………………………………….………

8,125

To record six months’ interest and

discount amortization.

2015

Dec. 31

Bond Interest Expense …………………………..

12,227

Discount on Bonds Payable …………….…………….

4,102

Cash ……………………………………………….………

8,125

To record six months’ interest and

discount amortization.

Problem 10–6A (45 minutes)

Part 1 Amount of Payment

Note balance ………………………………………..……………..

$200,000

Number of periods ………………………………..……………….

5

Interest rate ………………………………………….……………

8%

Value from Table B.3 …………………………….……………….

3.9927

Payment ($200,000 / 3.9927) ………………….……….

$ 50,091

rounded to nearest dollar

Part 2

Payments

Period

Ending

Date

(A)

Beginning

Balance

[Prior (E)]

(B)

Debit

Interest

Expense

[8% x (A)]

+

(C)

Debit

Notes

Payable

[(D) – (B)]

=

(D)

Credit

Cash

[computed]

(E)

Ending

Balance

[(A) – (C)]

10/31/2016 …..…….

$200,000

$ 16,000

$ 34,091

$ 50,091

$165,909

10/31/2017 …..…….

165,909

13,273

36,818

50,091

129,091

10/31/2018 …..…….

129,091

10,327

39,764

50,091

89,327

10/31/2019 …..…….

89,327

7,146

42,945

50,091

46,382

10/31/2020 …..…….

46,382

3,709*

46,382

50,091

0

$ 50,455

$200,000

$250,455

* Adjusted for rounding

Part 3

2015

Dec. 31

Interest Expense …………………………………………….……..

2,667

Interest Payable …………………………..…………………..

2,667

Accrued interest on the installment

note payable ($16,000 x 2/12) (rounded).

2016

Oct. 31

Interest Expense …………………………………………….……..

13,333

Interest Payable ……………………………………………..……..

2,667

Notes Payable …………………………..…………………………..

34,091

Cash ………………………………………………………………..

50,091

Record first payment on installment note

(interest expense = $16,000 – $2,667).

Problem 10–7A (20 minutes)

Part 1

Pulaski Company debt–to-equity = $360,000 / $500,000 = 0.72

Problem 10–8AB (60 minutes)

Part 1

2015

Jan. 1

Cash …………………………………………………….…

292,181

Discount on Bonds Payable ………………….……….

32,819

Bonds Payable ………………………………..……………….

325,000

Sold bonds on stated issue date.

Part 2

Eight payments of $8,125* ……………....

$ 65,000

Par value at maturity………………………..

325,000

Total repaid ……………………………………..

390,000

Less amount borrowed …………………...

(292,181)

Total bond interest expense …………....

$ 97,819

*$325,000 x 0.05 x ½ = $8,125

or:

Eight payments of $8,125 ………………...

$ 65,000

Plus discount ………………………………....

32,819

Total bond interest expense …………....

$ 97,819

Part 3

Semiannual

Interest

Period-End

(A)

Cash Interest

Paid

[2.5% x $325,000]

(B)

Bond Interest

Expense

[4% x Prior (E)]

(C)

Discount

Amortization

[(B) – (A)]

(D)

Unamortized

Discount

[Prior (D) – (C)]

(E)

Carrying

Value

[$325,000 – (D)]

1/01/2015

$32,819

$292,181

6/30/2015

$8,125

$11,687

$3,562

29,257

295,743

12/31/2015

8,125

11,830

3,705

25,552

299,448

6/30/2016

8,125

11,978

3,853

21,699

303,301

12/31/2016

8,125

12,132

4,007

17,692

307,308

Problem 10–8AB (Concluded)

Part 4

2015

June 30

Bond Interest Expense …………………………..

11,687

Discount on Bonds Payable …………….…………….

3,562

Cash ……………………………………………….………

8,125

To record six months’ interest and

discount amortization.

2015

Dec. 31

Bond Interest Expense …………………………..

11,830

Discount on Bonds Payable …………….…………….

3,705

Cash ……………………………………………….………

8,125

To record six months’ interest and

discount amortization.

Problem 10–9AB (45 minutes)

Part 1

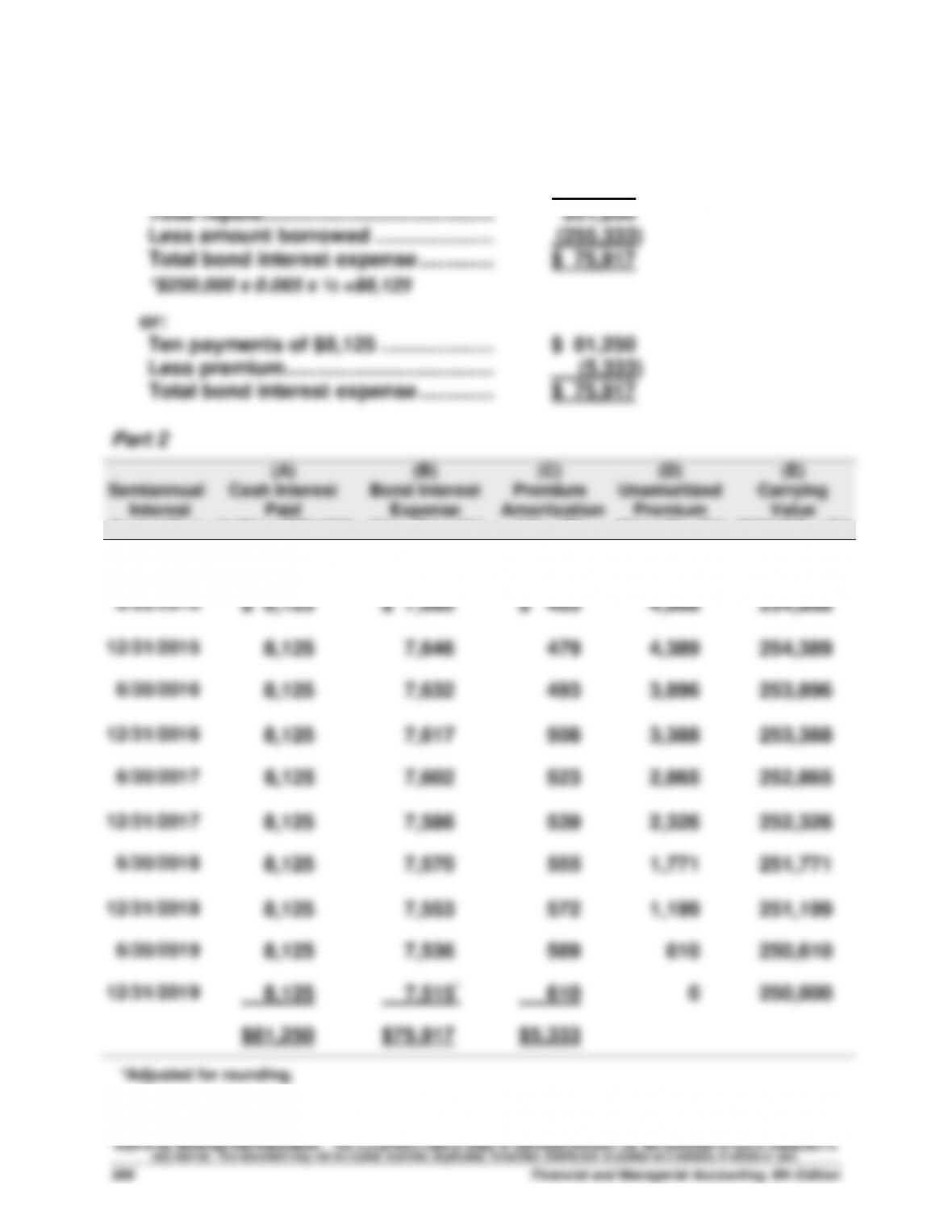

Ten payments of $8,125* ……………….……..

$ 81,250

Par value at maturity…………………………..

250,000

Total repaid …………………………………………..

331,250

Less amount borrowed ………………….……..

(255,333)

Total bond interest expense …………..……..

$ 75,917

*$250,000 x 0.065 x ½ =$8,125

or:

Ten payments of $8,125 ……………………….

$ 81,250

Less premium ………………………………..…….

(5,333)

Total bond interest expense …………..…….

$ 75,917

Part 2

Semiannual

Interest

Period-End

(A)

Cash Interest

Paid

[3.25% x $250,000]

(B)

Bond Interest

Expense

[3% x Prior (E)]

(C)

Premium

Amortization

[(A) – (B)]

(D)

Unamortized

Premium

[Prior (D) – (C)]

(E)

Carrying

Value

[$250,000 + (D)]

1/01/2015

$5,333

$255,333

6/30/2015

$ 8,125

$ 7,660

$ 465

4,868

254,868

12/31/2015

8,125

7,646

479

4,389

254,389

6/30/2016

8,125

7,632

493

3,896

253,896

12/31/2016

8,125

7,617

508

3,388

253,388

6/30/2017

8,125

7,602

523

2,865

252,865

12/31/2017

8,125

7,586

539

2,326

252,326

6/30/2018

8,125

7,570

555

1,771

251,771

12/31/2018

8,125

7,553

572

1,199

251,199

6/30/2019

8,125

7,536

589

610

250,610

12/31/2019

8,125

7,515*

610

0

250,000

$81,250

$75,917

$5,333

*Adjusted for rounding.