Exercise 10-2 (30 minutes)

1. Discount = Par value – Issue price = $180,000 – $170,862 = $9,138

2. Total bond interest expense over the life of the bonds

Amount repaid

Six payments of $7,200* ……………..

$ 43,200

Par value at maturity…………………..

180,000

Total repaid ………………………………..

223,200

Less amount borrowed …………………

(170,862)

Total bond interest expense ………….

$ 52,338

*180,000 x 0.08 x ½ = $7,200

or:

Six payments of $7,200 ………………….…….

$ 43,200

Plus discount ………………………………..…….

9,138

Total bond interest expense …………..…….

$ 52,338

3. Straight-line amortization table ($9,138/6 = $1,523)

Semiannual

Period–End

Unamortized

Discount

Carrying

Value

(0)

1/01/2015 ……………..……..

$9,138

$170,862

(1)

6/30/2015 ……………..……..

7,615

172,385

(2)

12/31/2015 ……………..……..

6,092

173,908

(3)

6/30/2016 ……………..……..

4,569

175,431

(4)

12/31/2016 ……………..……..

3,046

176,954

(5)

6/30/2017 ……………..……..

1,523

178,477

(6)

12/31/2017 ……………..……..

0

180,000

Exercise 10-3 (25 minutes)

1. Semiannual cash interest payment = $800,000 x 6% x ½ year = $24,000

2. Number of payments = 10 years x 2 per year = 20 semiannual payments

3. The 6% contract rate is less than the 8% market rate; therefore, the

4. Estimation of the market price at the issue date

Cash Flow

Table

Table Value*

Amount

Present Value

Par (maturity) value ……..

B.1

0.4564

$800,000

$365,120

Interest (annuity) ……..…..

B.3

13.5903

24,000

326,167

Price of bonds ……………..

$691,287

* Table values are based on a discount rate of 4% (half the annual market rate) and

20 periods (semiannual payments).

5.

Cash ………………………………………………………………..……

691,287

Discount on Bonds Payable……………………………………

108,713

Bonds Payable …………………………………………………

800,000

Sold bonds at a discount on the stated issue date.

Exercise 10-4 (20 minutes)

2015

(a)

Dec. 31

Cash ………………………………………………………..……………

186,534

Discount on Bonds Payable ……………………..……

13,466

Bonds Payable …………………………………………………

200,000

Sold bonds at discount.

2016

(b)

June 30

Bond Interest Expense ……………………………..……………

7,684

Discount on Bonds Payable** ……………..……………

1,684

Cash*…………………………..……………………..……

6,000

Paid semiannual interest and record amor-

tization. *$200,000 x6% x1/2 **13,466 – $11,782

(c)

Dec. 31

Bond Interest Expense ……………………………..……………

7,684

Discount on Bonds Payable** ……………..……………

1,684

Cash*…………………………..……………………..……

6,000

Paid semiannual interest and record amor-

tization. *$200,000 x6% x1/2 **$11,782 – $10,098

Exercise 10-5 (35 minutes)

2015

(a)

Dec. 31

Cash ……………………………………………………....

188,000

Discount on Bonds Payable …………………..………

12,000

Bonds Payable …………………………………………………

200,000

Sold bonds at discount.

(b)

2016

June 30

Bond Interest Expense …………………………..

8,000

Discount on Bonds Payable* …………….…………….

3,000

Cash** ……………………………………………..………..

5,000

Paid semiannual interest and record amor-

tization. *$12,000-$9,000 **$200,000x 5% x ½

Dec. 31

Bond Interest Expense …………………………..

8,000

Discount on Bonds Payable* …………….…………….

3,000

Cash** ……………………………………………..………..

5,000

Paid semiannual interest and record amor-

tization. *$9,000– $6,000 **$200,000x 5% x ½

2017

June 30

Bond Interest Expense …………………………..

8,000

Discount on Bonds Payable* …………….…………….

3,000

Cash** ……………………………………………..………..

5,000

Paid semiannual interest and record amor-

tization. *$6,000-$3,000 **$200,000 x 5% x ½

Dec. 31

Bond Interest Expense …………………………..

8,000

Discount on Bonds Payable* …………….…………….

3,000

Cash** ……………………………………………..………..

5,000

Paid semiannual interest and record amor-

tization. *$3,000 – $0 **$200,000 x 5% x ½

(c)

Dec. 31

Bonds Payable ………………………………………………………

200,000

Cash ………………………………………………..……..

200,000

Record maturity and payment of bonds.

Exercise 10-6 (20 minutes)

2014

(a)

Dec. 31

Cash ………………………………………………………..……………

216,222

Premium on Bonds Payable ………………..…………

16,222

Bonds Payable …………………………………………………

200,000

Sold bonds at premium.

2015

(b)

June 30

Bond Interest Expense ……………………………..……………

8,378

Premium on Bonds Payable* …………………….…….

1,622

Cash** ………………………………………………..……..

10,000

Paid semiannual interest and record amor-

tization. *$16,222- $14,600 **$200,000x 10% x ½

(c)

Dec. 31

Bond Interest Expense ………………………………….…………….

8,378

Premium on Bonds Payable* …………………………..

1,622

Cash** …………………………..…………………………..

10,000

Paid semiannual interest and record amor-

tization. *$14,600-$12,978 **$200,000x 10% x ½

Exercise 10-7 (30 minutes)

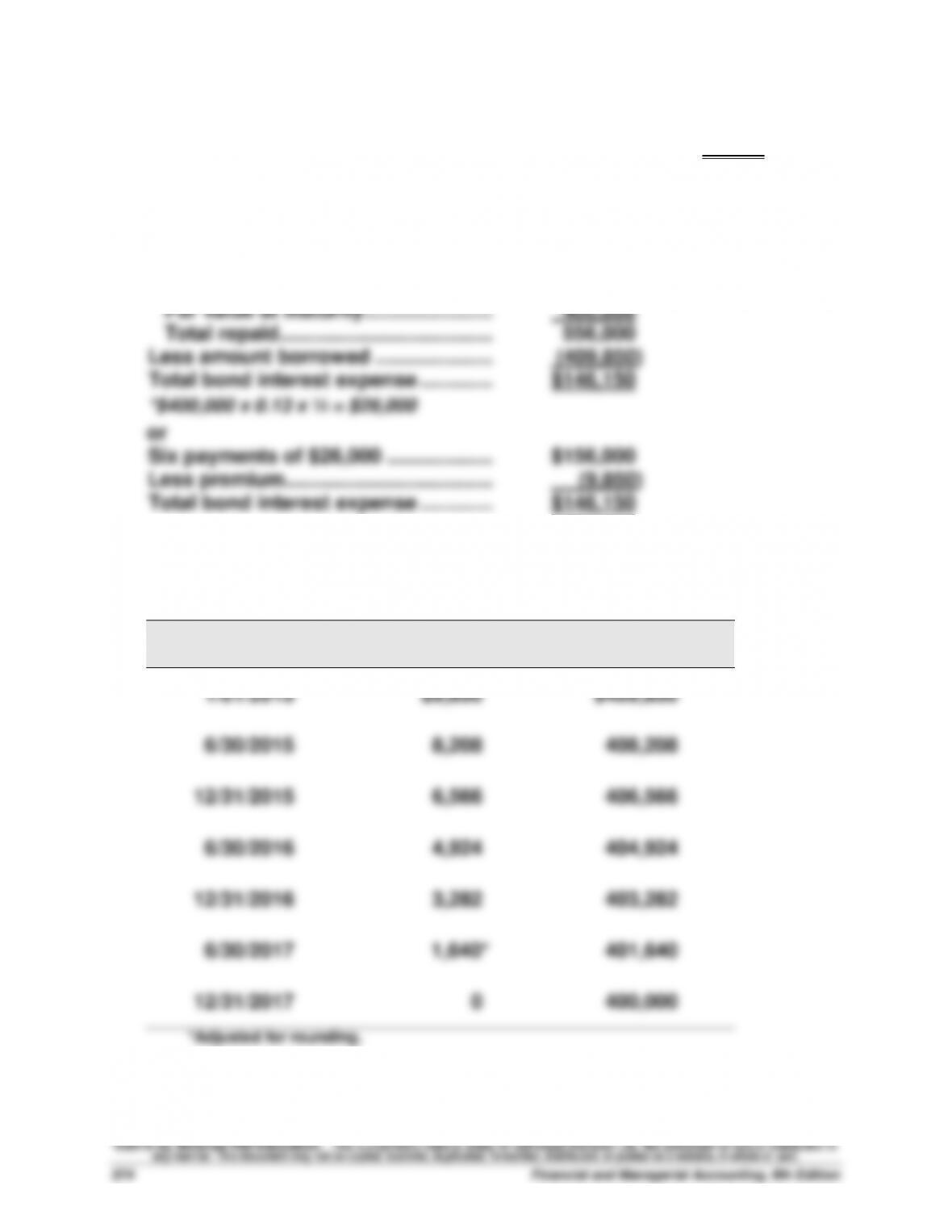

1. Premium = Issue price – Par value = $409,850 – $400,000 = $9,850

2. Total bond interest expense over the life of the bonds

Amount repaid

Six payments of $26,000* ……………

$156,000

Par value at maturity…………………..

400,000

Total repaid ………………………………..

556,000

Less amount borrowed …………………

(409,850)

Total bond interest expense ………….

$146,150

*$400,000 x 0.13 x ½ = $26,000

or

Six payments of $26,000 ……………….

$156,000

Less premium ……………………………….

(9,850)

Total bond interest expense ………….

$146,150

3. Straight-line amortization table ($9,850/6 = $1,642)

Semiannual

Interest Period-End

Unamortized

Premium

Carrying

Value

1/01/2015

$9,850

$409,850

6/30/2015

8,208

408,208

12/31/2015

6,566

406,566

6/30/2016

4,924

404,924

12/31/2016

3,282

403,282

6/30/2017

1,640*

401,640

12/31/2017

0

400,000

*Adjusted for rounding.

Exercise 10-8 (25 minutes)

1. Semiannual cash interest payment = $150,000 x 10% x ½ year = $7,500

2. Number of payments = 5 years x 2 per year = 10 semiannual payments

3. The 10% contract rate is greater than the 8% market rate; therefore, the

4. Estimation of the market price at the issue date

Cash Flow

Table

Table Value*

Amount

Present Value

Par (maturity) value …..…

B.1

0.6756

$150,000

$101,340

Interest (annuity) ……….…

B.3

8.1109

7,500

60,832

Price of bonds …………..…

$162,172

* Table values are based on a discount rate of 4% (half the annual market rate) and

10 periods (semiannual payments).

5.

Cash ………………………………………………………………..……

162,172

Premium on Bonds Payable ………………………..…

12,172

Bonds Payable …………………………………………………

150,000

Sold bonds at a premium on the stated issue date.

Exercise 10-9 (20 minutes)

1. Cash proceeds from sale of bonds at issuance

2. Discount at issuance

Par value ………………………………………...

$700,000

Cash issue price (from part 1) ………....

(684,250)

Discount at issuance ……………………....

$ 15,750

3. Total amortization for first 6 years

The first six years (from 1/1/15 to 12/31/20) equals 40% of the bonds’ 15–

4. Carrying value of the bonds at 12/31/2020

Discount at issuance (from part 2) …...

$ 15,750

Less amortization (from part 3) ………..

(6,300)

Remaining discount ………………………..

$ 9,450

Entire Group

Retired 20%

Par value ……………………………………….…

$700,000

$140,000

Remaining discount …………………………

(9,450)

(1,890)

Carrying value ……………………………….…

$690,550

$138,110

5. Cash purchase price

6. Loss on retirement

Cash paid (from part 5)…………………..

$ 146,300

Carrying value (from part 4) ……………

(138,110)

Loss on retirement ………………………...

$ 8,190

7. Journal entry at retirement for 20% of bonds

2021

Jan. 1

Bonds Payable ………………………………………………………

140,000

Loss on Retirement of Bonds Payable ……………………

8,190

Discount on Bonds Payable ……………..……………

1,890

Cash ………………………………………………..……..

146,300

To record the retirement of bonds.

Exercise 10-10 (20 minutes)

1. Amount of each payment = Initial note balance / Table B.3 value

2. Amortization table for the loan

Payments

Period

Ending

Date

(A)

Beginning

Balance

[Prior (E)]

(B)

Debit

Interest

Expense

[7% x (A)]

+

(C)

Debit

Notes

Payable

[(D) – (B)]

=

(D)

Credit

Cash

[computed]

(E)

Ending

Balance

[(A) – (C)]

2015 …….

$100,000

$ 7,000

$ 22,523

$ 29,523

$77,477

2016 …….

77,477

5,423

24,100

29,523

53,377

2017 …….

53,377

3,736

25,787

29,523

27,590

2018 …….

27,590

1,933*

27,590

29,523

0

$18,092

$100,000

$118,092

*Adjusted for rounding.

Exercise 10-11 (20 minutes)

2015

Jan. 1

Cash ……………………………………………………………………..

100,000

Notes Payable …………………………………………..……..

100,000

Borrowed $100,000 by signing a 7%

installment note.

2015

Dec. 31

Interest Expense …………………………………………….……..

7,000

Notes Payable ………………………………………………..……..

22,523

Cash ………………………………………………………………..

29,523

To record first installment payment.

2016

Dec. 31

Interest Expense …………………………………………….……..

5,423

Notes Payable ………………………………………………..……..

24,100

Cash ………………………………………………………………..

29,523

To record second installment payment.

2017

Dec. 31

Interest Expense …………………………………………….……..

3,736

Notes Payable ………………………………………………..……..

25,787

Cash ………………………………………………………………..

29,523

To record third installment payment.

2018

Dec. 31

Interest Expense …………………………………………….……..

1,933

Notes Payable ………………………………………………..……..

27,590

Cash ………………………………………………………………..

29,523

To record fourth installment payment.

Exercise 10-12 (15 minutes)

1a. Current debt–to-equity ratio = $220,000 / $400,000* = 0.55

2. Montclair’s risk will increase because it will have more debt. That debt

(plus interest) must be repaid even if the project does not work out as