Exercise 1-4 (10 minutes)

1.

A

4.

F

2.

G

5.

C

3.

D

Exercise 1-5 (20 minutes)

a. Auditing professionals with competing audit clients are likely to learn

valuable information about each client that the other clients would

benefit from knowing. In this situation the auditor must take care to

maintain the confidential nature of information about each client.

Exercise 1-6 (10 minutes)

a.

(C) Corporation

e.

(C) Corporation

b.

(P) Partnership

f.

(SP) Sole proprietorship

c.

(SP) Sole proprietorship

g.

(C) Corporation

d.

(SP) Sole proprietorship

Exercise 1-7 (10 minutes)

Code

Description

Principle/Assumption

H.

1.

A company reports details behind financial

statements that would impact users’ decisions.

Full disclosure

principle

G

2.

Financial statements reflect the assumption that

the business continues operating.

Going-concern

assumption

F

3.

A company records the expenses incurred to

generate the revenues reported.

Matching (expense

recognition) principle

A

4.

Derived from long-used and generally accepted

accounting practices.

General accounting

principle

C

5.

Every business is accounted for separately from

its owner or owners.

Business entity

assumption

D

6.

Revenue is recorded only when the earnings

process is complete.

Revenue recognition

principle

E

7.

Usually created by a pronouncement from an

authoritative body.

Specific accounting

principle

B

8.

Information is based on actual costs incurred in

transactions.

Cost principle

Exercise 1-8 (10 minutes)

Assets

=

Liabilities

+

Equity

(a) $ 65,000

=

$ 20,000

+

$45,000

$100,000

=

$ 34,000

+

(b) $66,000

$154,000

=

(c) $114,000

+

$40,000

Exercise 1-9 (20 minutes)

a. Using the accounting equation at the beginning of the year:

Assets

=

Liabilities

+

Equity

$300,000

=

?

+

$100,000

Thus, beginning liabilities = $200,000

Assets

=

Liabilities

+

Equity

$300,000 + $80,000

=

$200,000+ $50,000

+

?

$380,000

=

$250,000

+

?

Thus, ending equity = $130,000

Alternative approach to solving part (b):

Assets($80,000) = Liabilities($50,000) + Equity(?)

where “” refers to “change in.”

Thus: Ending Equity = $100,000 + $30,000 = $130,000

b. Using the accounting equation:

Assets

=

Liabilities

+

Equity

$123,000

=

$47,000

+

?

Thus, equity = $76,000

c. Using the accounting equation at the end of the year:

Assets

=

Liabilities

+

Equity

$190,000

=

$70,000 – $5,000

+

?

$190,000

=

$65,000

+

$125,000

Using the accounting equation at the beginning of the year:

Assets

=

Liabilities

+

Equity

$190,000 – $60,000

=

$70,000

+

?

$130,000

=

$70,000

+

?

Thus: Beginning Equity = $60,000

Exercise 1-10 (20 minutes)

a. Started the business with the owner investing $40,000 cash in the

Exercise 1-11 (20 minutes)

a. Purchased land for $4,000 cash.

Exercise 1-12 (15 minutes)

Examples of transactions that fit each case include:

a. Cash dividends (or some other asset) paid to the owner of the

business; OR, the business incurs an expense paid in cash.

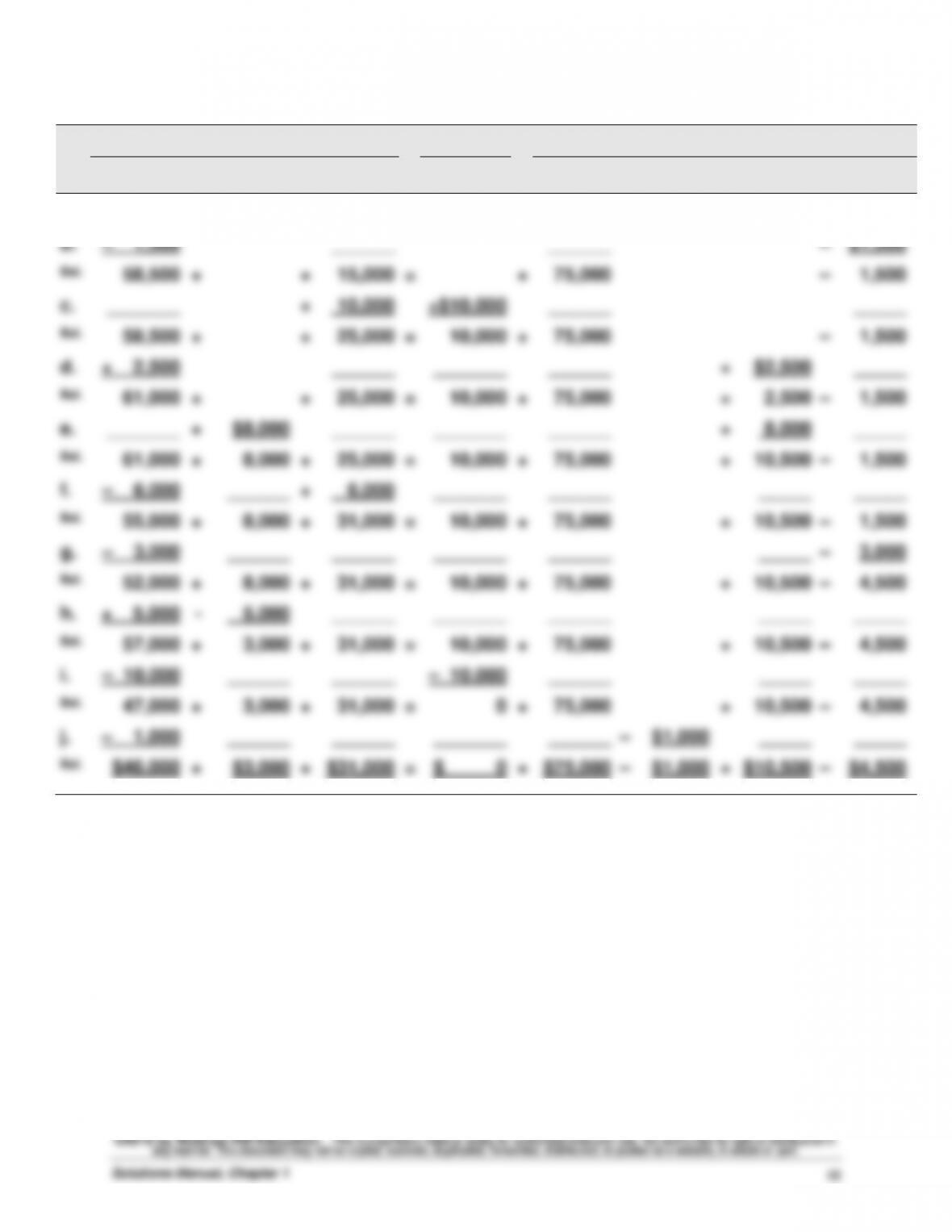

Exercise 1-13 (30 minutes)

Assets

=

Liabilities

+

Equity

Cash

+

Accounts

Receivable

+

Equip-

ment

=

Accounts

Payable

+

Common

Stock

–

Dividends

+

Revenues

–

Expenses

a.

+$60,000

+

$15,000

=

+

$75,000

b.

– 1,500

______

______

–

$1,500

Bal.

58,500

+

+

15,000

=

+

75,000

–

1,500

c.

_______

+

10,000

+$10,000

______

_____

Bal.

58,500

+

+

25,000

=

10,000

+

75,000

–

1,500

d.

+ 2,500

______

_______

______

+

$2,500

_____

Bal.

61,000

+

+

25,000

=

10,000

+

75,000

+

2,500

–

1,500

e.

_______

+

$8,000

______

_______

______

+

8,000

_____

Bal.

61,000

+

8,000

+

25,000

=

10,000

+

75,000

+

10,500

–

1,500

f.

– 6,000

______

+

6,000

_______

______

_____

_____

Bal.

55,000

+

8,000

+

31,000

=

10,000

+

75,000

+

10,500

–

1,500

g.

– 3,000

______

______

_______

______

_____

–

3,000

Bal.

52,000

+

8,000

+

31,000

=

10,000

+

75,000

+

10,500

–

4,500

h.

+ 5,000

–

5,000

______

_______

______

_____

_____

Bal.

57,000

+

3,000

+

31,000

=

10,000

+

75,000

+

10,500

–

4,500

i.

– 10,000

______

______

– 10,000

______

_____

_____

Bal.

47,000

+

3,000

+

31,000

=

0

+

75,000

+

10,500

–

4,500

j.

– 1,000

______

______

_______

______

–

$1,000

_____

_____

Bal.

$46,000

+

$3,000

+

$31,000

=

$ 0

+

$75,000

–

$1,000

+

$10,500

–

$4,500

Exercise 1-14 (10 minutes)

Return on assets

=

Net income / Average total assets

=

$40,000 / [($200,000 + $300,000)/2]

=

16%

Interpretation: Swiss Group’s return on assets of 16% is markedly above

the 10% return of its competitors. Accordingly, its performance is

assessed as superior to its competitors.

Exercise 1-15 (15 minutes)

ERNST CONSULTING

Income Statement

For Month Ended October 31

Revenues

Consulting fees earned …………………. $14,000

Expenses

Exercise 1-16 (15 minutes)

ERNST CONSULTING

Statement of Retained Earnings

For Month Ended October 31

Retained earnings, October 1 ……………………. $ 0

Exercise 1-17 (15 minutes)

ERNST CONSULTING

Balance Sheet

October 31

Assets Liabilities

Cash …………………………. $11,360 Accounts payable …………….. $ 8,500

* For the computation of this amount see Exercise 1-16.

Exercise 1-18 (15 minutes)

ERNST CONSULTING

Statement of Cash Flows

For Month Ended October 31

Cash flows from operating activities

Cash received from customers …………………………………….. $ 0

Cash paid to employees1 ……………………………………………… (1,750)

Cash paid for rent …………………………..……………………………. (3,550)

Cash paid for telephone expenses ……………………………….. (760)

1$7,000 Salaries Expense – $5,250 still owed = $1,750 paid to employees.

Exercise 1-19 (10 minutes)

I 1. Cash purchase of equipment O 5. Cash paid on an account payable

Exercise 1-20 (20 minutes)

BMW GROUP

Income Statement

For Year Ended December 31, 2013

Exercise 1-21B (10 minutes)

a. Financing*

b. Financing

PROBLEM SET A

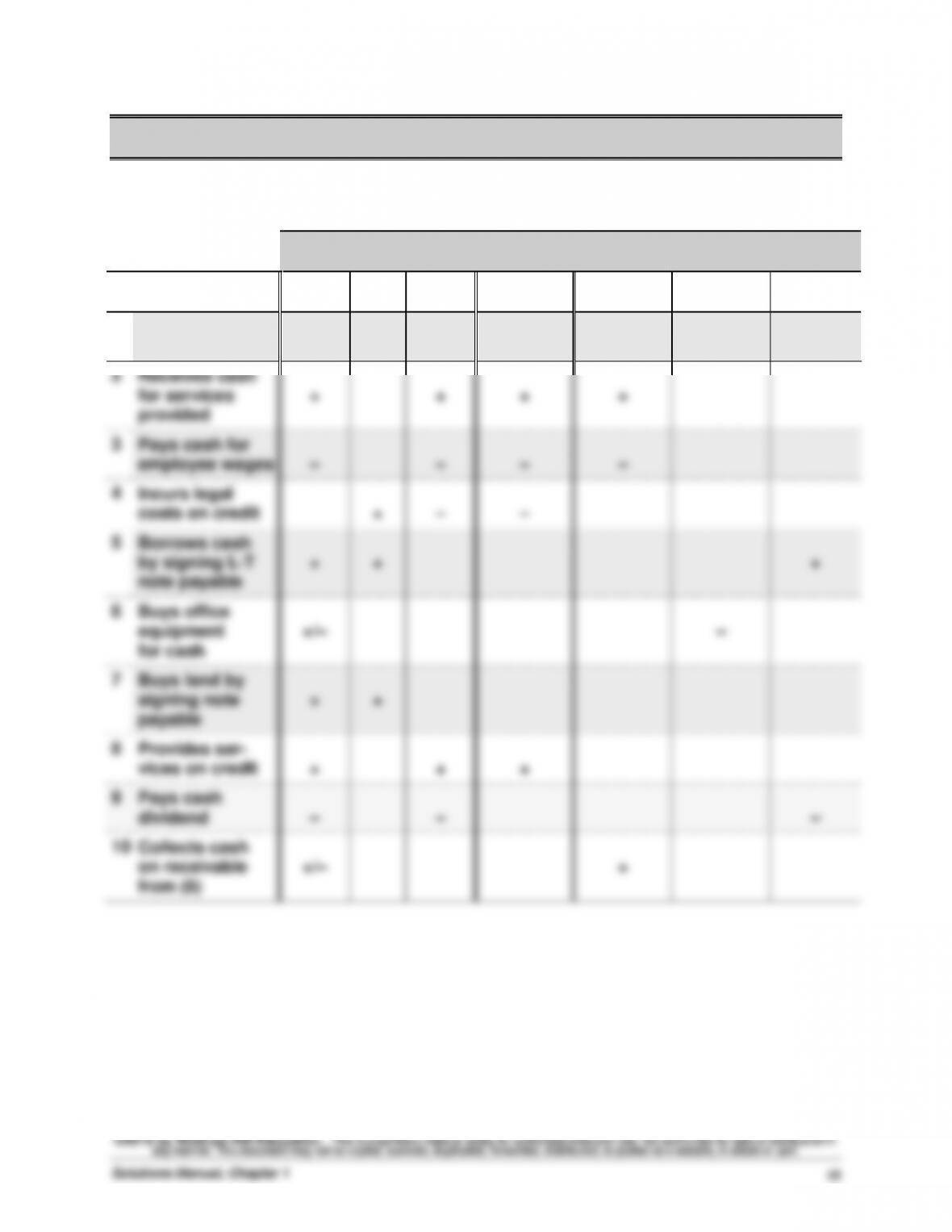

Problem 1-1A (25 minutes)

Balance Sheet

Income

Statement

Statement of

Cash Flows

Transaction

Total

Assets

Total

Liab.

Total

Equity

Net

Income

Operating

Activities

Investing

Activities

Financing

Activities

1

Owner invests

cash for its stock

+

+

+

2

Receives cash

for services

provided

+

+

+

+

3

Pays cash for

employee wages

–

–

–

–

4

Incurs legal

costs on credit

+

–

–

5

Borrows cash

by signing L-T

note payable

+

+

+

6

Buys office

equipment

for cash

+/–

–

7

Buys land by

signing note

payable

+

+

8

Provides ser-

vices on credit

+

+

+

9

Pays cash

dividend

–

–

–

10

Collects cash

on receivable

from (8)

+/–

+

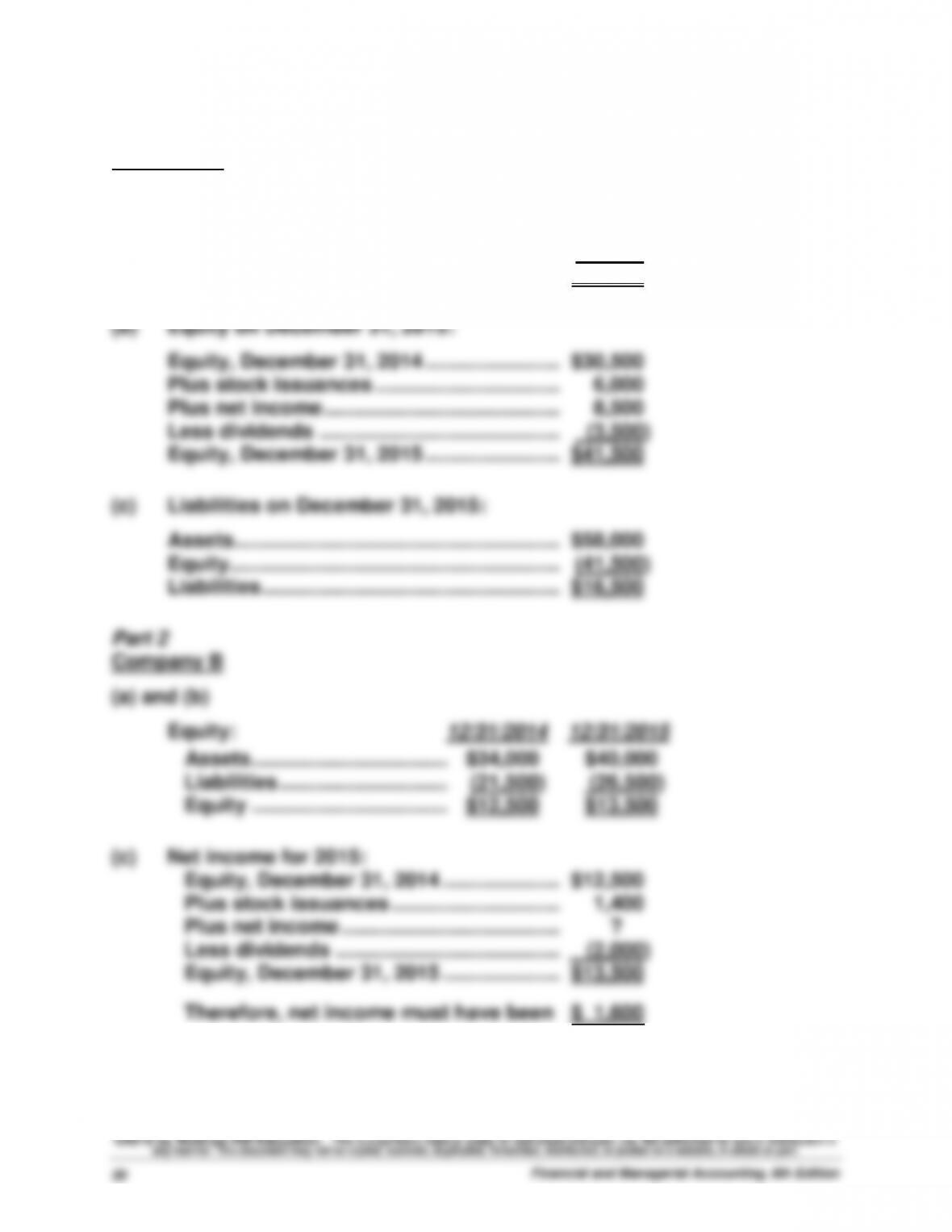

Problem 1-2A (40 minutes)

Part 1

Company A

(a) Equity on December 31, 2014:

Assets …………………………………………………. $55,000

Liabilities …………………………..………………… (24,500)

Equity………………………………………………….. $30,500