Exercise D-6 (25 minutes)

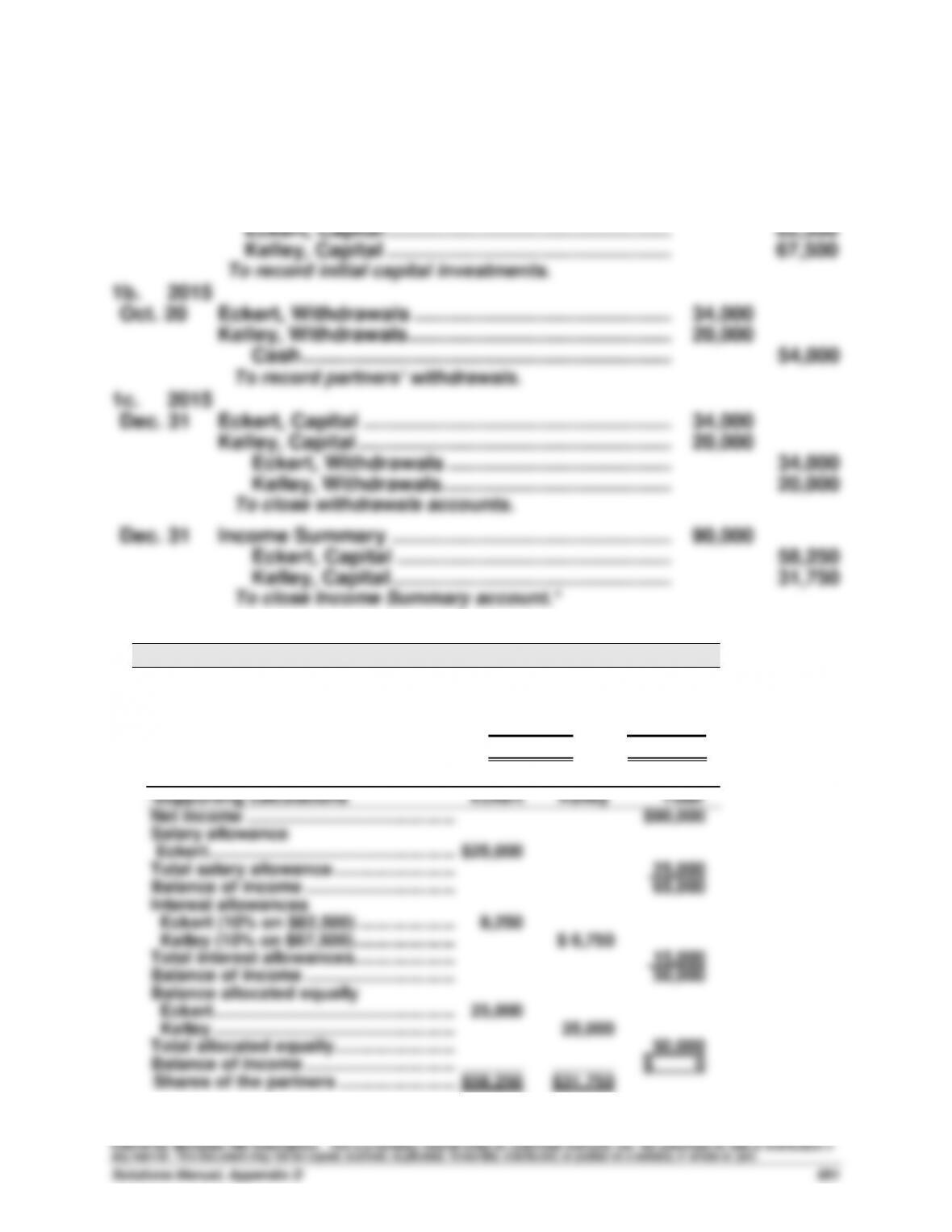

1a. 2015

Mar. 1

Cash ………………………………………………………………..

82,500

Land ………………………………………………………………..

60,000

Building …………………………………………………………..

100,000

Long–Term Note Payable …………………………....

92,500

Eckert, Capital …………………………………………….

82,500

Kelley, Capital …………………………………………….

67,500

To record initial capital investments.

1b. 2015

Oct. 20

Eckert, Withdrawals ……………………………………….…

34,000

Kelley, Withdrawals ………………………………………..…

20,000

Cash ………………………………………………………...…

54,000

To record partners’ withdrawals.

1c. 2015

Dec. 31

Eckert, Capital ……………………………………………….…

34,000

Kelley, Capital ………………………………………………..…

20,000

Eckert, Withdrawals ………………………………….…

34,000

Kelley, Withdrawals …………………………………..…

20,000

To close withdrawals accounts.

Dec. 31

Income Summary …………………………………………..…

90,000

Eckert, Capital ………………………………………….…

58,250

Kelley, Capital …………………………………………..…

31,750

To close Income Summary account.*

2.

Capital account balances

Eckert

Kelley

Initial investment …………………………..

$ 82,500

$ 67,500

Withdrawals …………………………..……..

(34,000)

(20,000)

Share of income* …………………………..

58,250

31,750

Ending balances ……………………….….

$106,750

$ 79,250

*Supporting calculations

Eckert

Kelley

Total

Net income …………………………………….…………………

$90,000

Salary allowance

Eckert ……………………………………………………….

$25,000

Total salary allowance …………………….…….

25,000

Balance of income …………………………..

65,000

Interest allowances

Eckert (10% on $82,500) ………………..…………

8,250

Kelley (10% on $67,500) …………………………..

$ 6,750

Total interest allowances…………………………..

15,000

Balance of income …………………………..

50,000

Balance allocated equally

Eckert …………………………………………..…………..

25,000

Kelley …………………………………………..…………..

25,000

Total allocated equally …………………….…….

50,000

Balance of income …………………………..

_______

_______

$ 0

Shares of the partners …………………………..

$58,250

$31,750

Exercise D-7 (10 minutes)

Sept. 30

Mandy, Capital …………………………..………………..……

100,000

Brittney, Capital …………………………..………………

100,000

To record admission of Brittney.

Exercise D-8 (25 minutes)

1.

Nov. 1

Cash ……………………………………………………….…….….

90,000

Madison, Capital ………………………………………….

90,000

To record admission of Madison

[($510,000 + $90,000) x 15%].

2.

Nov. 1

Cash ………………………………………………………………..

120,000

Madison, Capital……………………………………..…..

94,500

Main, Capital …………………………………………..…..

20,400

Frist, Capital …………………………..…………………..

5,100

To record admission of Madison.

Supporting computations

$510,000 + $120,000 = $630,000

$630,000 x 15% = $94,500

$120,000 – $94,500 = $25,500

$25,500 x 80% = $20,400

$25,500 x 20% = $5,100

3.

Nov. 1

Cash ………………………………………………………………..

80,000

Main, Capital ………………………………………………..…..

6,800

Frist, Capital …………………………..………………………..

1,700

Madison, Capital……………………………………..…..

88,500

To record admission of Madison.

Supporting computations

$510,000 + $80,000 = $590,000

$590,000 x 15% = $88,500

$80,000 – $88,500 = $(8,500)

$(8,500) x 80% = $(6,800)

$(8,500) x 20% = $(1,700)

Exercise D-9 (15 minutes)

1.

Jan. 31

Tulip, Capital ………………………………………………..…..

60,000

Cash ……………………………………………………….

60,000

To record retirement of Tulip.

2.

Jan. 31

Tulip, Capital ………………………………………………..…..

60,000

Hunter, Capital* …………………………..……………….…..

12,500

Folgers, Capital** ……………………………………………..

7,500

Cash ……………………………………………………….

80,000

To record retirement of Tulip.

* (5/8 x $20,000)

**(3/8 x $20,000)

3.

Jan. 31

Tulip, Capital ………………………………………………..…..

60,000

Hunter, Capital* …………………………..………….…..

18,750

Folgers, Capital** …………………………..……….…..

11,250

Cash ……………………………………………………….

30,000

To record retirement of Tulip.

* (5/8 x $30,000)

**(3/8 x $30,000)

Exercise D-10 (30 minutes)

a. Loss from selling assets

Total book value of assets …………………………..…….……

$126,000

Total liabilities (before liquidation) …………………….……

$78,000

Total liabilities remaining after paying

proceeds of asset sales to creditors ………………..……

(28,000)

Cash proceeds from sale of assets …………………….……

(50,000)

Loss on sale of assets* ……………………………………..……

$ 76,000

* Alternative computation

1) $28,000 = $78,000 – Cash from asset sale

(This implies $50,000 cash from asset sale)

2) Loss on sale of assets = Book value of assets – Cash received

= $126,000 – $50,000 = $76,000

b. Loss allocation

Turner

Roth

Lowe

Total

Capital balances before

loss liquidation

$ 2,500

$ 14,000

$ 31,500

$ 48,000

Allocation of loss

$76,000 x 1/10 …………………..

(7,600)

$76,000 x 4/10 …………………..

(30,400)

$76,000 x 5/10 …………………..

______

_______

(38,000)

(76,000)

Capital balances after loss …..

$(5,100)

$(16,400)

$ (6,500)

$(28,000)

c. Deficiency, if any, to be covered

Exercise D-11 (30 minutes)

a. Loss from selling assets

Total book value of assets …………………………..………….

$126,000

Total liabilities before liquidation …………………………..

$78,000

Total liabilities remaining after paying proceeds

of asset sales to creditors ………………………………….….

(28,000)

Cash proceeds from sale of assets ………………………….

(50,000)

Loss on sale of assets …………………………………………….

$ 76,000

b. Loss and deficit allocation

Turner

Roth

Lowe

Total

Capital balances before loss

$ 2,500

$ 14,000

$ 31,500

$ 48,000

Allocation of loss

$76,000 x 1/10 …………………..

(7,600)

$76,000 x 4/10 …………………..

(30,400)

$76,000 x 5/10 …………………..

______

_______

(38,000)

(76,000)

Capital balances after loss …..

(5,100)

(16,400)

(6,500)

$(28,000)

Allocation of Lowe’s deficit

to Turner and Roth

$6,500 x 1/5 ……………………...

(1,300)

$6,500 x 4/5 ……………………...

______

(5,200)

6,500

_________

Cash paid by each partner

$(6,400)

$(21,600)

$ 0

$(28,000)

c. Deficiency, if any, to be covered

As a limited partner, Lowe has no personal liability for the $28,000

liability. Therefore, Turner and Roth must share the loss reflected in

Lowe’s capital account deficit as shown above.

Exercise D-12 (20 minutes)

Rugged Sports Enterprises LP:

PROBLEM SET A

Problem D-1A (45 minutes)

Preliminary calculations

Plan (a) & Plan (c)

Percentages based on initial investments

Watts = $42,000/$105,000 = 40%

Lyon = $63,000/$105,000 = 60%

Plan (b)

Percentages based on time

Watts = 0.5/1.5 = 33 1/3%

Lyon = 1.0/1.5 = 66 2/3%

Plan (c) & Plan (d)

Salary allowance

Lyon= 12 x $6,000 = $72,000

Plan (d)

Interest allowances

Watts = 10% x $42,000 = $ 4,200

Lyon= 10% x $63,000 = $ 6,300

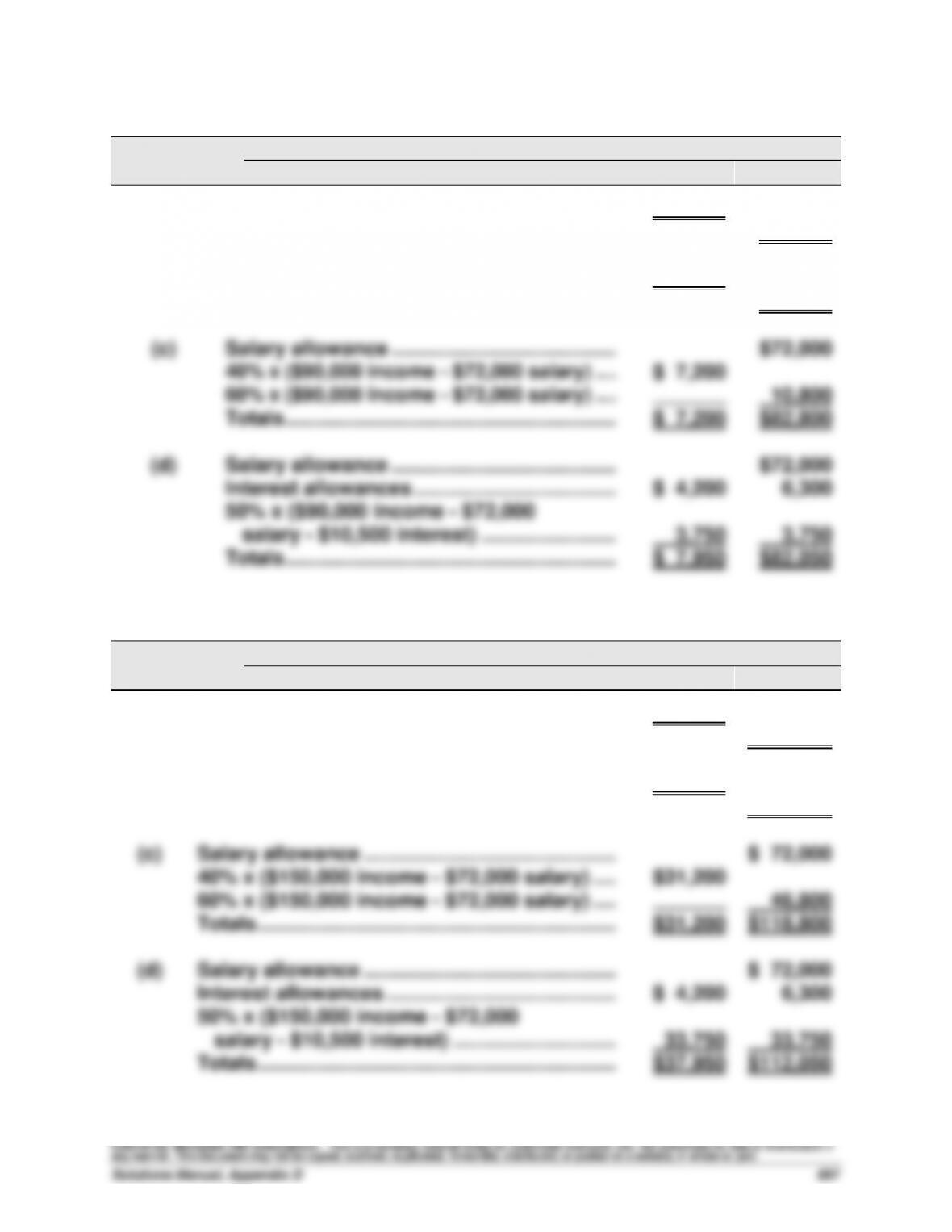

Problem D-1A (Concluded)

Income (Loss)

Year 2

Sharing Plan

Calculations

Watts

Lyon

(a)

40% x $90,000 income …………………………..

$36,000

60% x $90,000 income …………………………..

$54,000

(b)

33 1/3% x $90,000 income …………………….…….

$30,000

66 2/3% x $90,000 income …………………….…….

$60,000

(c)

Salary allowance …………………………..……..…………..

$72,000

40% x ($90,000 income – $72,000 salary) ….……………

$ 7,200

60% x ($90,000 income – $72,000 salary) ….……………

_______

10,800

Totals …………………………..…………………………..

$ 7,200

$82,800

(d)

Salary allowance …………………………..……..…………..

$72,000

Interest allowances …………………………………………..

$ 4,200

6,300

50% x ($90,000 income – $72,000

salary – $10,500 interest) …………………………..

3,750

3,750

Totals …………………………..…………………………..

$ 7,950

$82,050

Income (Loss)

Year 3

Sharing Plan

Calculations

Watts

Lyon

(a)

40% x $150,000 income …………………………….………

$60,000

60% x $150,000 income …………………………….………

$ 90,000

(b)

33 1/3% x $150,000 income ……………………….….

$50,000

66 2/3% x $150,000 income ……………………….….

$100,000

(c)

Salary allowance …………………………..………….………

$ 72,000

40% x ($150,000 income – $72,000 salary) ….………

$31,200

60% x ($150,000 income – $72,000 salary) ….………

_______

46,800

Totals …………………………..…………………………..

$31,200

$118,800

(d)

Salary allowance …………………………..………….………

$ 72,000

Interest allowances …………………………………..………

$ 4,200

6,300

50% x ($150,000 income – $72,000

salary – $10,500 interest) ………………………..…

33,750

33,750

Totals …………………………..…………………………..

$37,950

$112,050

Problem D-2A (50 minutes)

1.

Dec. 31

Income Summary …………………………..…………………

249,000

Kara Ries, Capital …………………………………….…

83,000

Tammy Bax, Capital ……………………………………

83,000

Joe Thomas, Capital ……………………………………

83,000

To close Income Summary.

2.

Dec. 31

Income Summary …………………………..…………………

249,000

Kara Ries, Capital …………………………………….…

62,250

Tammy Bax, Capital ……………………………………

87,150

Joe Thomas, Capital ……………………………………

99,600

To close Income Summary*.

*Supporting computations

($80,000/$320,000) x $249,000 = $62,250

($112,000/$320,000) x $249,000 = $87,150

($128,000/$320,000) x $249,000 = $99,600

3.

Dec. 31

Income Summary …………………………..…………………

249,000

Kara Ries, Capital …………………………………….…

79,000

Tammy Bax, Capital ……………………………………

72,200

Joe Thomas, Capital ……………………………………

97,800

To close Income Summary*.

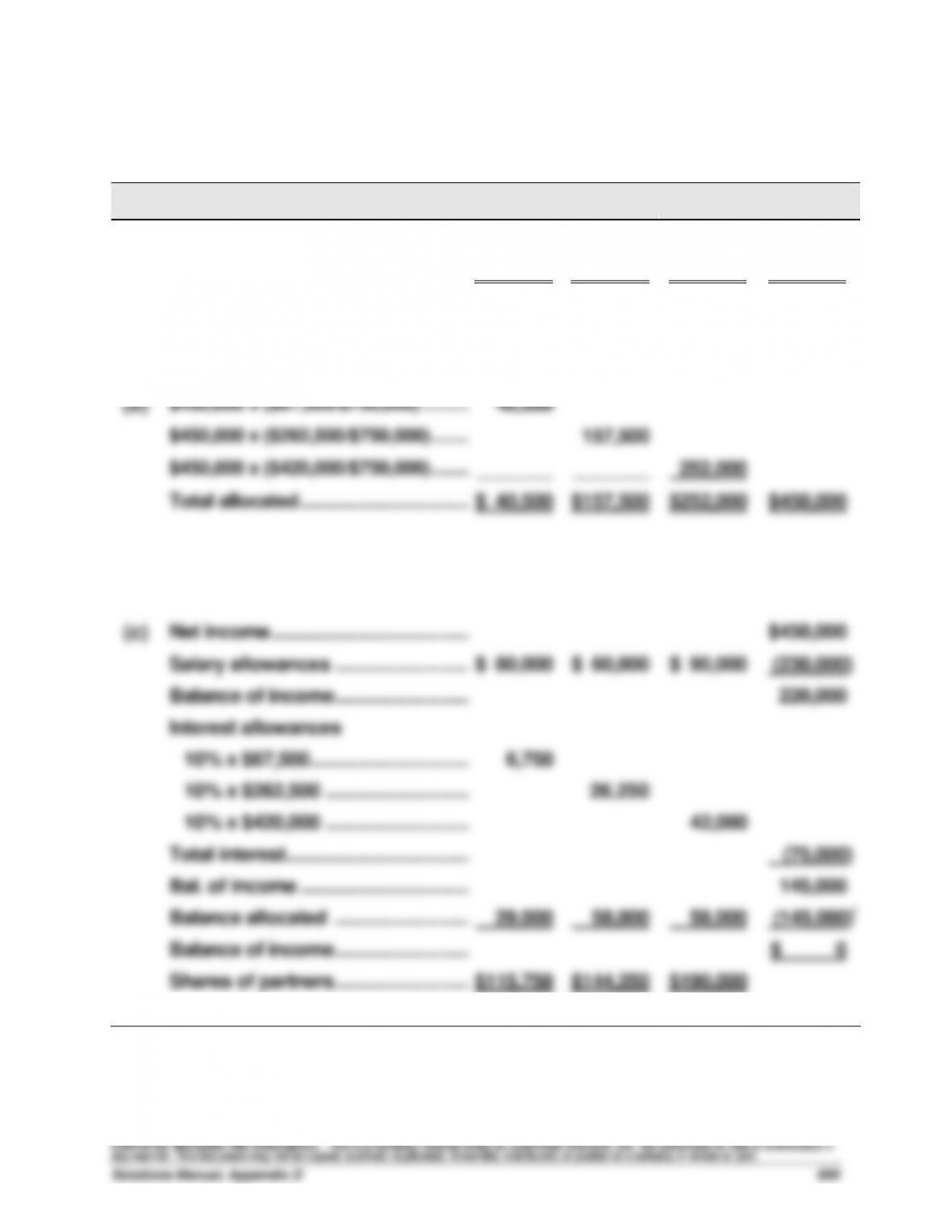

*Supporting calculations

Ries

Bax

Thomas

Total

Net income ……………………………….………..

$249,000

Salary allowances

Ries……………………………………….………..

$66,000

Bax………………………………………..………..

$56,000

Thomas …………………………………………..

$80,000

Total salaries ……………………………………..

202,000

Balance after salary allowances …………..

47,000

Interest allowances

Ries (10% on $80,000) …………….………..

8,000

Bax (10% on $112,000) ……………………..

11,200

Thomas (10% on $128,000) ……..………..

12,800

Total interest …………………………….………..

32,000

Bal. after interest and salaries ……………..

15,000

Balance allocated equally ………….………..

5,000

5,000

5,000

Total allocated equally ………………………..

15,000

Balance of income …………………….…….

______

______

______

$ 0

Shares of the partners……………….………..

$79,000

$72,200

$97,800

Problem D-3A (40 minutes)

Part 1

Income (Loss)

Sharing Plan

Calculations

Bill

Bruce

Barb

Total

(a)

$450,000/3 ……………………………………………………….

$150,000

$150,000

$150,000

$450,000

(b)

$450,000 x ($67,500/$750,000) ……….………………….

40,500

$450,000 x ($262,500/$750,000) ……..……………………

157,500

$450,000 x ($420,000/$750,000) ……..……………………

_______

_______

252,000

Total allocated ……………………………..………………………..

$ 40,500

$157,500

$252,000

$450,000

(c)

Net income …………………………..…………………………..

$450,000

Salary allowances ……………………….….

$ 80,000

$ 60,000

$ 90,000

(230,000)

Balance of income ……………………….….

220,000

Interest allowances

10% x $67,500 ……………………………………………………….

6,750

10% x $262,500 …………………………..

26,250

10% x $420,000 …………………………..

42,000

Total interest ………………………………..……………………..

(75,000)

Bal. of income …………………………..…………………………..

145,000

Balance allocated ……………………….….

29,000

58,000

58,000

(145,000)*

Balance of income ……………………….….

$ 0

Shares of partners ……………………….….

$115,750

$144,250

$190,000

Problem D-3A (Concluded)

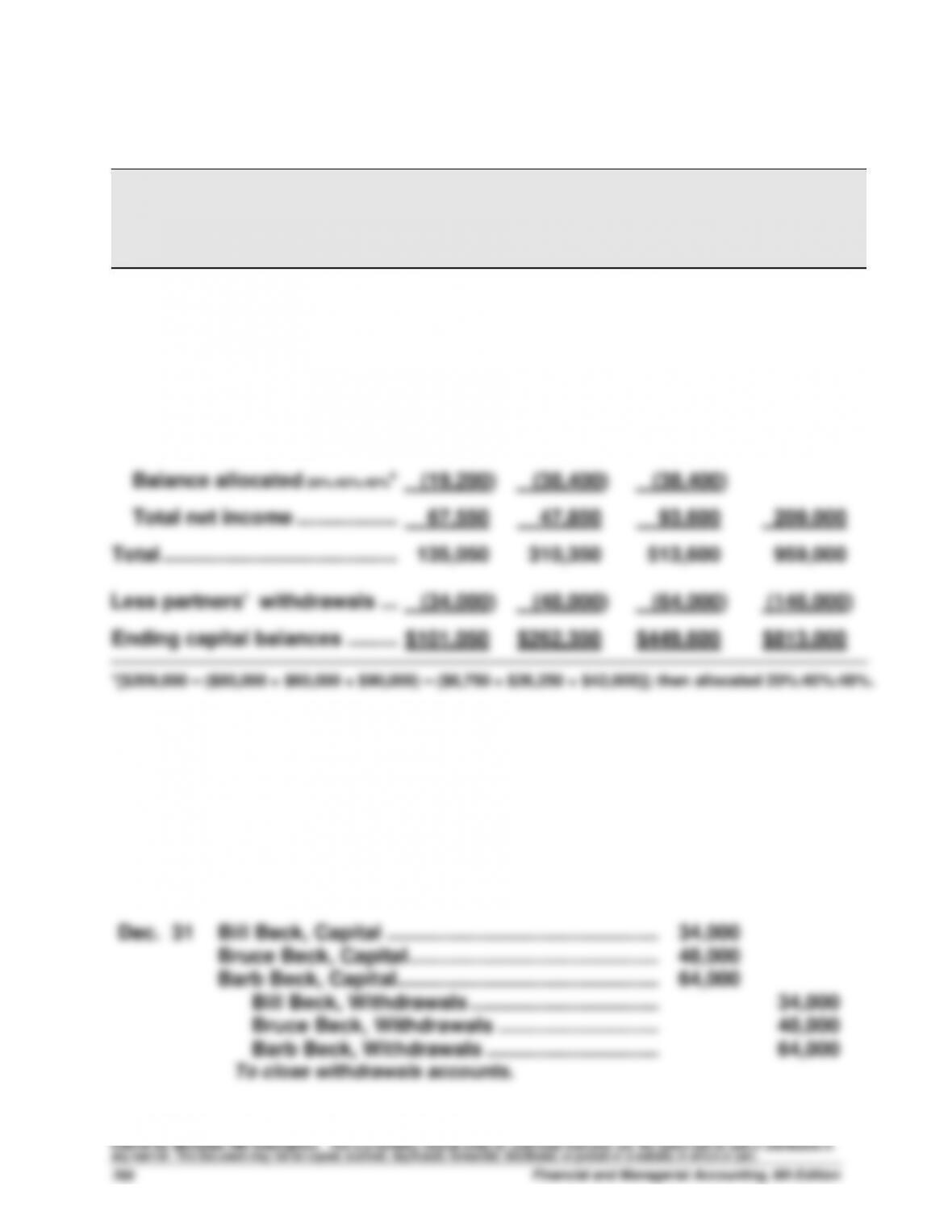

Part 2

BBB PARTNERSHIP

Statement of Partners’ Equity

For Year Ended December 31

Bill

Bruce

Barb

Total

Beginning capital balances …..………

$ 0

$ 0

$ 0

$ 0

Plus

Investments by owners ………………

67,500

262,500

420,000

750,000

Net income

Salary allowances ……………..………

80,000

60,000

90,000

Interest allowances …………..………

6,750

26,250

42,000

Balance allocated 20%:40%:40%*

(19,200)

(38,400)

(38,400)

Total net income ……………….………

67,550

47,850

93,600

209,000

Total …………………………………….………

135,050

310,350

513,600

959,000

Less partners’ withdrawals ….………

(34,000)

(48,000)

(64,000)

(146,000)

Ending capital balances ……….………

$101,050

$262,350

$449,600

$813,000

*[$209,000 – ($80,000 + $60,000 + $90,000) – ($6,750 + $26,250 + $42,000)]; then allocated 20%:40%:40%.

Part 3

Dec. 31

Income Summary ……………………………………………..

209,000

Bill Beck, Capital …………………………………….…..

67,550

Bruce Beck, Capital ……………………………………..

47,850

Barb Beck, Capital …………………………………..…..

93,600

To close Income Summary.

Dec. 31

Bill Beck, Capital ………………………………………….…..

34,000

Bruce Beck, Capital …………………………………………..

48,000

Barb Beck, Capital ………………………………………..…..

64,000

Bill Beck, Withdrawals …………………………….…..

34,000

Bruce Beck, Withdrawals ………………………..…

48,000

Barb Beck, Withdrawals …………………………..

64,000

To close withdrawals accounts.