Problem C-3A (Concluded)

Part 2

12/31/2015

12/31/2016

12/31/2017

Long-Term AFS Securities (cost)……………....

$117,100

$85,143

$212,160

Fair Value Adjustment ………………………....

(3,650)

(13,818)

8,040

Long-Term AFS Securities (fair value) ……....

$113,450

$71,325

$220,200

Part 3

2015

2016

2017

Realized gains (losses)

Sale of Johnson & Johnson shares …….

$ 2,235

Sale of Mattel shares …………………………..

(5,080)

Sale of Sara Lee shares ……………………...

$(4,665)

Sale of Sony shares …………………………..

1,055

Sale of Eastman Kodak shares …………...

______

_______

4,352

Total realized gain (loss) ……………………...

$ 0

$ (2,845)

$ 742

Unrealized gains (losses) at year–end*…..

$(3,650)

$(13,818)

$ 8,040

* Equals the balance of the Fair Value Adjustment account.

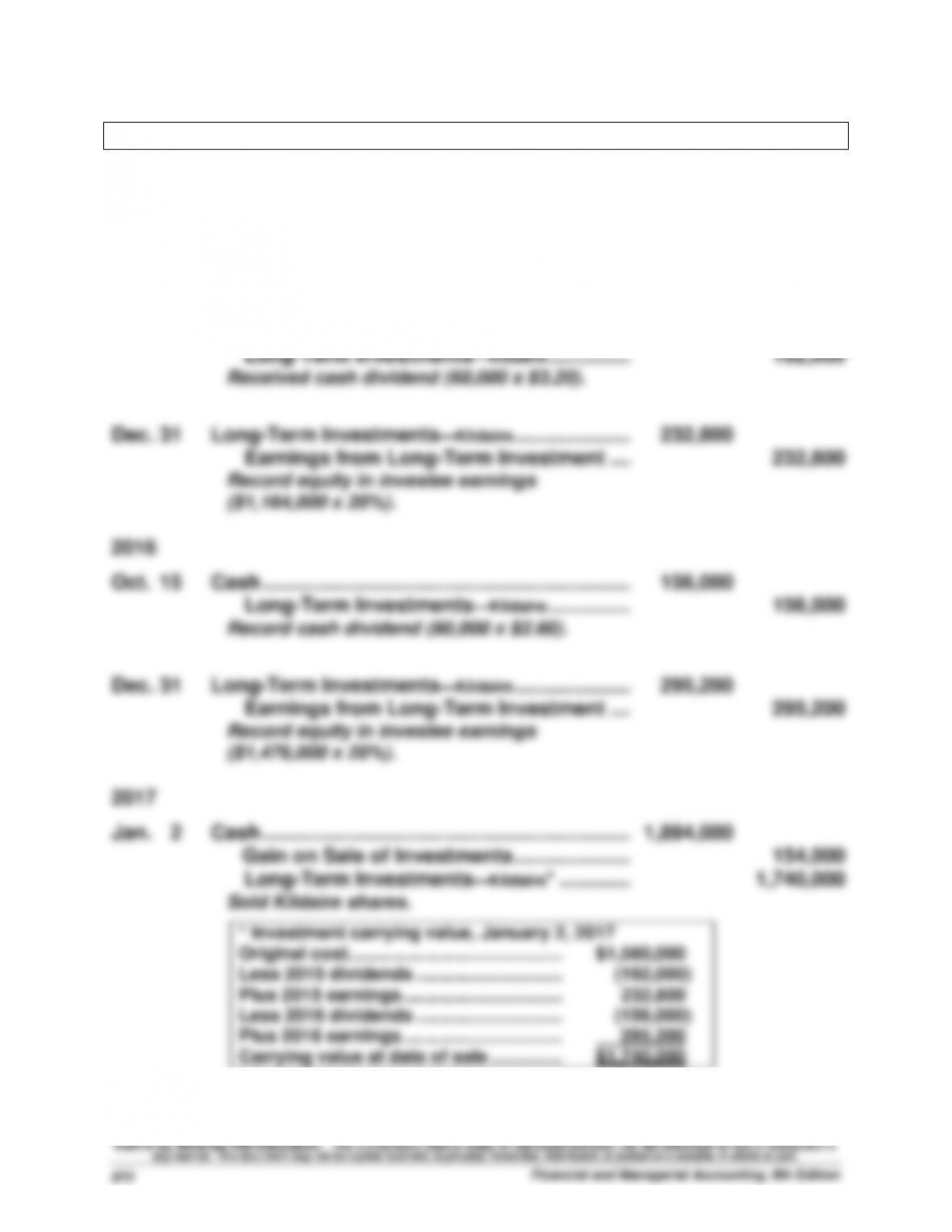

Problem C-4A (30 minutes)

Part 1

1. Journal entries (assuming significant influence)

2015

Jan. 5

Long-Term Investments—Kildaire …………………………..

1,560,000

Cash ……………………………………………………….

1,560,000

Purchased Kildaire shares.

Oct. 23

Cash ………………………………………………………………………………

192,000

Long–Term Investments—Kildaire …………………………..

192,000

Received cash dividend (60,000 x $3.20).

Dec. 31

Long-Term Investments—Kildaire …………………………..

232,800

Earnings from Long–Term Investment ….……………………

232,800

Record equity in investee earnings

($1,164,000 x 20%).

2016

Oct. 15

Cash ………………………………………………………………………………

156,000

Long–Term Investments—Kildaire …………………………..

156,000

Record cash dividend (60,000 x $2.60).

Dec. 31

Long-Term Investments—Kildaire …………………………..

295,200

Earnings from Long–Term Investment ….……………………

295,200

Record equity in investee earnings

($1,476,000 x 20%).

2017

Jan. 2

Cash ………………………………………………………………………………

1,894,000

Gain on Sale of Investments …………………………..

154,000

Long–Term Investments—Kildaire* ………….……………….

1,740,000

Sold Kildaire shares.

* Investment carrying value, January 2, 2017

Original cost ……………………………………….

$1,560,000

Less 2015 dividends …………………………..

(192,000)

Plus 2015 earnings ……………………………..

232,800

Less 2016 dividends …………………………..

(156,000)

Plus 2016 earnings ……………………………..

295,200

Carrying value at date of sale ……………..

$1,740,000

Problem C-4A (Continued)

2. Carrying value per share, January 1, 2017 (see computations in part 1)

3. Change in Selk’s equity due to stock investment

Earnings from Kildaire (2015) …………………….…….

$232,800

Earnings from Kildaire (2016) …………………….…….

295,200

Gain on sale of investments …………………………..

154,000

Net increase ……………………………………………..………..

$682,000

Part 2

1. Journal entries (assuming NO significant influence)

2015

Jan. 5

Long-Term Investments—AFS (Kildaire) ……….………………….

1,560,000

Cash ……………………………………………………….

1,560,000

Purchased Kildaire shares.

Oct. 23

Cash ………………………………………………………………………………

192,000

Dividend Revenue ……………………………….……………………

192,000

Received cash dividend (60,000 x $3.20).

Dec. 31

Fair Value Adjustment—AFS (LT)* ……………..……………

240,000

Unrealized Gain—Equity …………………………..

240,000

Record fair value adjustment.

*60,000 x $30.00 = $1,800,000

$1,800,000 – $1,560,000 = $240,000

Cash ………………………………………………………………………………

Dividend Revenue ……………………………….……………………

Dec. 31

Unrealized Gain—Equity …………………………..

Record fair value adjustment.

$1,920,000 – $1,560,000 = $360,000

$360,000 – $240,000 = $120,000

Problem C-4A (Concluded)

2017

Jan. 2

Cash ………………………………………………………………………………

1,894,000

Long–Term Investments—AFS (Kildaire) ….……………………

1,560,000

Gain on Sale of Investments ………………..…………

334,000

Sold Kildaire shares.

Jan. 2

Unrealized Gain—Equity …………………………………………………

360,000

Fair Value Adjustment—AFS (LT) …………………………..

360,000

To remove fair value adjustment and related

accounts ($240,000 + $120,000 = $360,000).

2. Investment cost per share, January 1, 2017

3. Change in Selk’s equity due to stock investment

Dividend Revenue (2015) ………………………….

$192,000

Dividend Revenue (2016) ………………………….

156,000

Gain on sale of investments ……………………..

334,000

Net increase …………………………………………….

$682,000

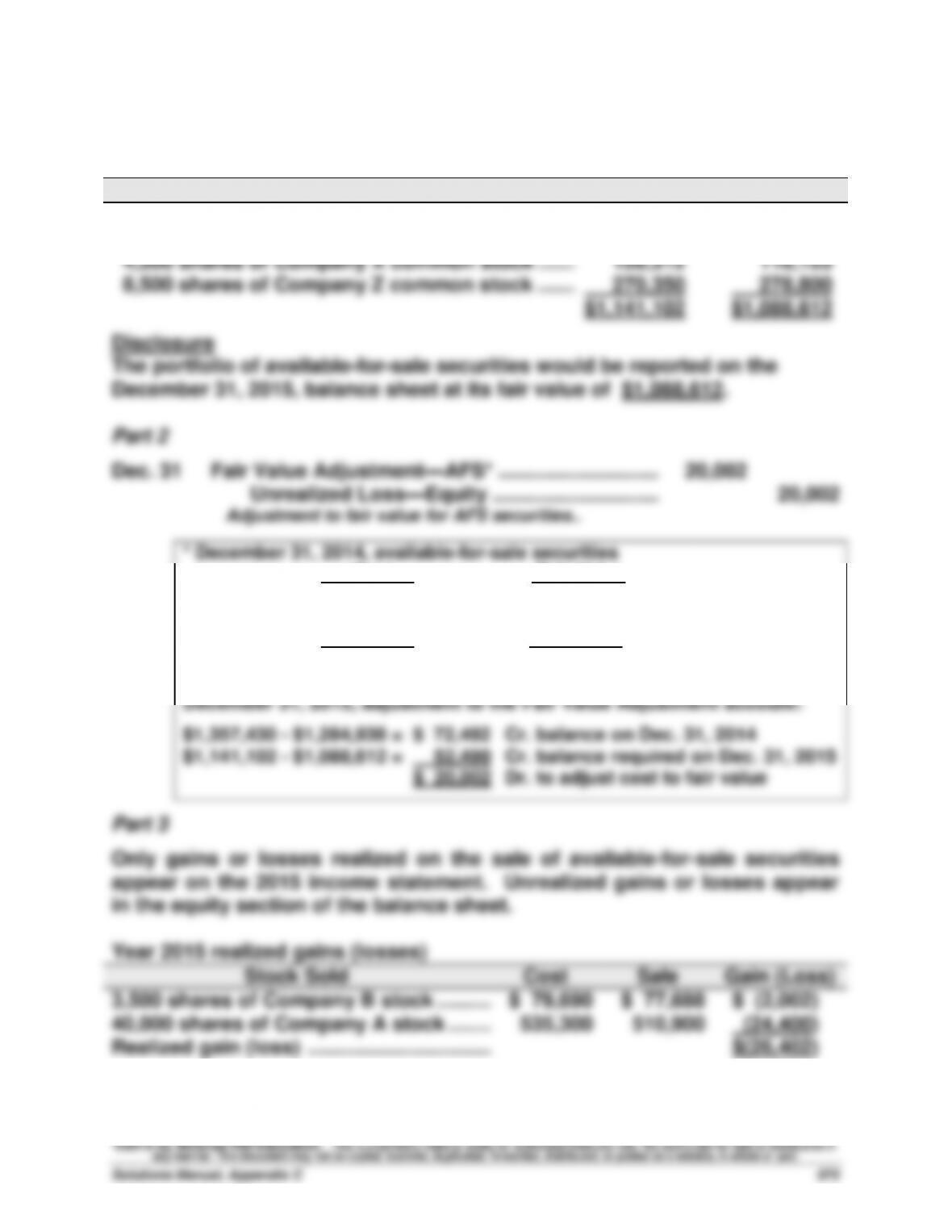

Problem C-5A (40 minutes)

Part 1

Available-for-sale securities on December 31, 2015

Security

Cost

Fair Value

3,500 shares of Company B common stock …….…….

$ 79,690

$ 81,375

17,500 shares of Company C common stock …….…….

662,750

610,312

4,500 shares of Company X common stock …….…….

128,312

118,125

8,500 shares of Company Z common stock …….…….

270,350

278,800

$1,141,102

$1,088,612

Disclosure

The portfolio of available–for-sale securities would be reported on the

December 31, 2015, balance sheet at its fair value of $1,088,612.

Part 2

Dec. 31

Fair Value Adjustment—AFS* ………………………..…

20,002

Unrealized Loss—Equity …………………………..

20,002

Adjustment to fair value for AFS securities..

* December 31, 2014, available-for-sale securities

Cost _

Fair Value

$ 535,300

$ 490,000

159,380

154,000

662,750

640,938

$1,357,430

$1,284,938

December 31, 2015, adjustment to the Fair Value Adjustment account:

$1,357,430 – $1,284,938 = $ 72,492 Cr. balance on Dec. 31, 2014

$1,141,102 – $1,088,612 = 52,490 Cr. balance required on Dec. 31, 2015

$ 20,002 Dr. to adjust cost to fair value

Part 3

Only gains or losses realized on the sale of available–for-sale securities

appear on the 2015 income statement. Unrealized gains or losses appear

in the equity section of the balance sheet.

Year 2015 realized gains (losses)

Stock Sold

Cost

Sale

Gain (Loss)

3,500 shares of Company B stock ………...

$ 79,690

$ 77,688

$ (2,002)

40,000 shares of Company A stock ……....

535,300

510,900

(24,400)

Realized gain (loss) ……………………………..

$(26,402)

Problem C-6AA (60 minutes)

Part 1

2015

Apr. 8

Cash …………………………………………………………..………………….

5,938

Sales …………………………………………………….…

5,938

July 21

Accounts ReceivableSumito …………………….…….

14,100

Sales …………………………………………………….…

14,100

(1,500,000 yen x $0.0094/yen)

Oct. 14

Accounts ReceivableSmithers …………………………..

27,675

Sales …………………………………………………….…

27,675

(19,000£ x $1.4566/£)

Nov. 18

Cash …………………………………………………………..………………….

13,800

Foreign Exchange Loss ………………………………………………….

300

Accounts ReceivableSumito ……………….………….

14,100

(1,500,000 yen x $0.0092/yen)

Dec. 20

Accounts ReceivableHamid Albar …………….…………….

7,652

Sales …………………………………………………….…

7,652

(17,000 ringgits x $0.4501/ringgits)

Dec. 31

Accounts ReceivableSmithers. ………………..…………

103

Foreign Exchange Gain * ……………………….….

103

Foreign Exchange Loss* ……………………………..………………….

Accounts ReceivableHamid Albar ……….………………….

Cash*…………………………..……………………………..………………….

Accounts ReceivableSmithers** ………….……………….

Foreign Exchange Gain …………………………..

Foreign Exchange Loss ………………………………………………….

Accounts ReceivableHamid Albar** …….………………….

Problem C-6AA (Continued)

Part 2

Foreign exchange loss reported on the 2015 income statement

November 18 …………………………..…….

$(300)

December 31 ………………………………….

103

December 31 ………………………………….

(77)

Total ……………………………………………...

$(274)

Part 3

To reduce the risk of foreign exchange gain or loss, Doering could attempt

to negotiate foreign customer sales that are denominated in U.S. dollars.

PROBLEM SET B

Problem C-1B (60 minutes)

Part 1

2015

Mar. 10

Short-Term Investments—Trading (AOL) ……………....

143,505

Cash ……………………………………………………….

143,505

Purchased AOL shares

[(2,400 x $59.15) + $1,545].

May 7

Short–Term Investments—Trading (MTV) …………..

184,105

Cash ……………………………………………………….

184,105

Purchased MTV shares

[(5,000 x $36.25) + $2,855].

Sept. 1

Short–Term Investments—Trading (UPS) …………..

69,950

Cash ……………………………………………………….

69,950

Purchased UPS shares

[(1,200 x $57.25) + $1,250].

Dec. 31

Unrealized Loss—Income …………………………..…..

17,560

Fair Value Adjustment—Trading (ST) ………...

17,560

Record fair value of securities.

$380,000 fair value – $397,560 cost*; thus,

FVA—Trading s/b $17,560 Cr.

Note: Unadjusted FVA is $0; Ending bal. FVA s/b

$17,560 Cr; thus, entry must $17,560 Cr FVA.

*$397,560 = $143,505 + $184,105 + $69,950

We could also use a T-account to determine the needed adjustment to fair value:

12/31/2015—F.V. Adj—Trading

Unadj.

0

Adj.

17,560

End.

17,560

Problem C-1B (Continued)

2016

Apr. 26

Cash ……………………………………………………………..

170,450

Loss on Sale of Short-Term Investments ………..

13,655

Short–Term Investments—Trading (MTV) …….

184,105

Sold MTV shares [(5,000 x $34.50) – $2,050].

Apr. 27

Cash ……………………………………………………………..

70,812

Gain on Sale of Short–Term Investments …..

862

Short–Term Investments—Trading (UPS) …….

69,950

Sold UPS shares [(1,200 x $60.50) – $1,788].

June 2

Short-Term Investments—Trading (SPW) …………….

622,450

Cash ……………………………………………………….

622,450

Purchased SPW shares

[(3,600 x $172.00) + $3,250].

June 14

Short–Term Investments—Trading (W-M) ………….

46,307

Cash ……………………………………………………….

46,307

Purchased Wal–Mart shares

[(900 x $50.25) + $1,082].

Dec. 31

Fair Value Adjustment—Trading (ST) ……………..

33,298

Unrealized Gain—Income ………………………….

33,298

Record fair value of securities.

$828,000 fair value – $812,262 cost*; thus,

FVA—Trading s/b $15,738 Dr.

Note: Unadjusted FVA is $17,560 Cr; Ending bal. FVA s/b

$15,738 Dr; thus, entry must $33,298 Dr FVA.

*$812,262 = $397,560 -$184,105 -$69,950 +622,450 +$46,307

We could also use a T-account to determine the needed adjustment to fair value:

12/31/2016—F.V. Adj—Trading

Unadj.

17,560

Adj.

33,298

End.

15,738

Problem C-1B (Concluded)

2017

Jan. 28

Short–Term Investments—Trading (Pepsi) …………

88,890

Cash …………………………………………………………

88,890

Purchased PepsiCo shares

[(2,000 x $43.00) + $2,890].

Jan. 31

Cash ………………………………………………………………

602,760

Loss on Sale of Short-Term Investments …………

19,690

Short–Term Investments—Trading (SPW) ……….

622,450

Sold SPW shares [(3,600 x $168) – $2,040].

Aug. 22

Cash ………………………………………………………………

133,720

Loss on Sale of S-T Investments ……………………..

9,785

Short–Term Investments—Trading (AOL) ……….

143,505

Sold AOL shares [(2,400 x $56.75) – $2,480].

Sept. 3

Short–Term Investments—Trading (Voda) ………….

62,430

Cash …………………………………………………………

62,430

Purchased Vodaphone shares

[(1,500 x $40.50) + $1,680].

Oct. 9

Cash ………………………………………………………………

47,155

Gain on Sale of Short-Term Investments ………...

848

Short-Term Investments—Trading (W-M) ………...

46,307

Sold Wal-Mart shares

[(900 x $53.75) – $1,220].

Dec. 31

Unrealized Loss—Income …………………………..…..

27,058

Fair Value Adjustment—Trading (ST) …………

27,058

Record fair value of securities.

$140,000 fair value – $151,320 cost*; thus,

FVA—Trading s/b $11,320 Cr.

Note: Unadjusted FVA is $15,738 Dr; Ending bal. FVA s/b

$11,320 Cr; thus, entry must $27,058 Cr FVA.

*$812,262 +$88,890 -$622,450 -$143,505 +$62,430 -$46,307

We could also use a T-account to determine the needed adjustment to fair value:

12/31/2017—F.V. Adj—Trading

Unadj.

15,738

Adj.

27,058

End.

11,320