APPENDIX C

INVESTMENTS AND

INTERNATIONAL OPERATIONS

Related Assignment Materials

Student Learning Objectives

Questions

Quick

Studies*

Exercises*

Problems*

Beyond the

Numbers

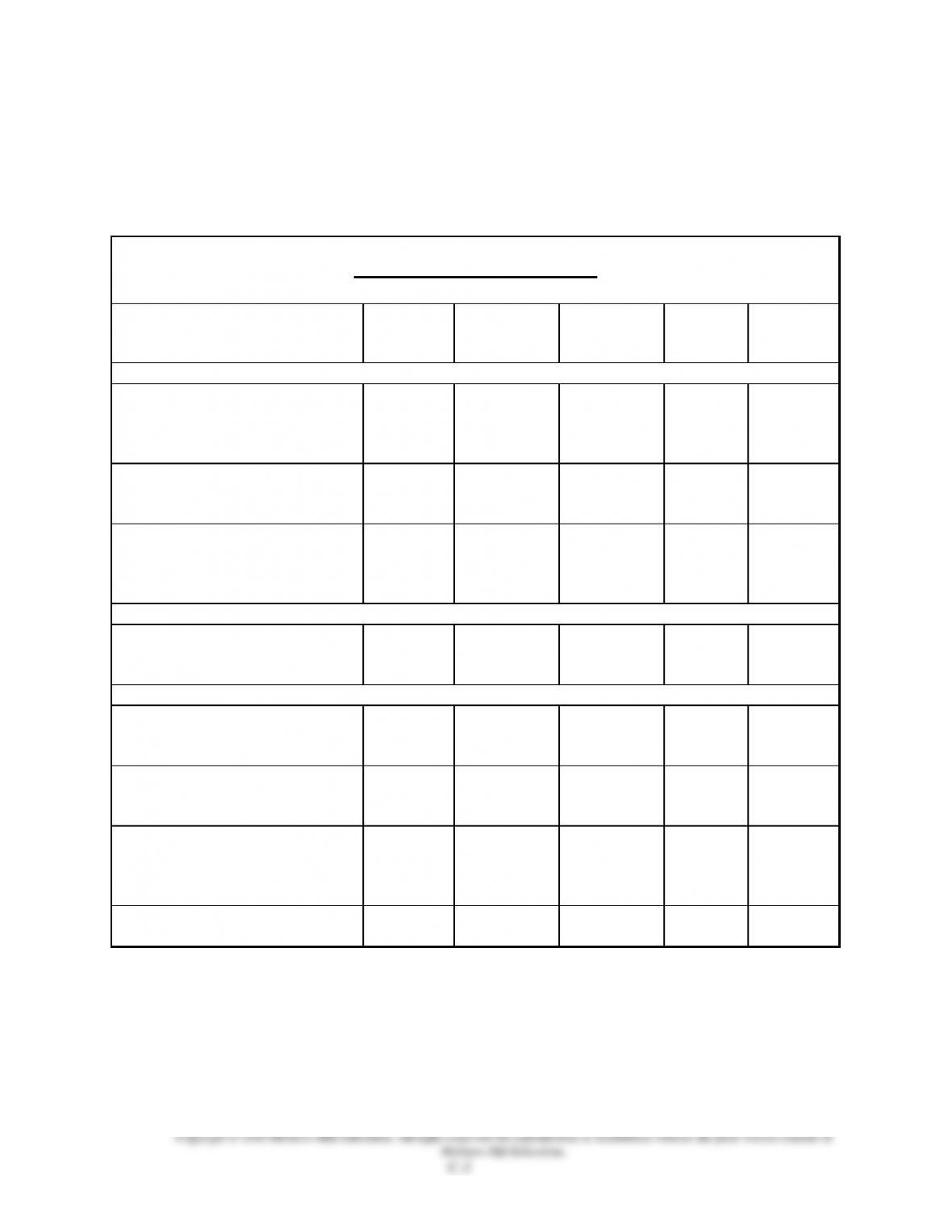

Conceptual objectives:

C1. Distinguish between debt and

equity securities and between

long-term investments and

short-term investments.

1, 2, 5

C-1, C-2

C-1, C-11

C-5, C-6

C2. Describe how to report equity

securities with controlling

influence.

17, 18

C-12, C-13

C-13

C-5

C-6

C3. Explain foreign exchange rates

between currencies and record

transactions listed in a foreign

currency.

12, 13, 14,

15

C-16, C-17

C-15, C-16

C-6

C-1, C-7,

C-8

Analytical objectives:

A1. Compute and analyze the

components of return on total

assets.

C-14, C-15

C-14

C-1, C-2,

C-9

Procedural objectives:

P1. Account for trading securities.

C-3, C-4,

C-5, C-16,

C-18

C-2, C-3,

C-6, C-8

C-1

C-6

P2. Account for held-to–maturity

securities.

5, 9

C-6

C-4, C-6,

C-11

C-3, C-6

P3. Account for available-for-sale

securities.

3, 4, 6, 7, 8,

15

C-7, C-8,

C-9, C-10

C-5, C-6,

C-7, C-8,

C-9, C-10,

C-11, C-17

C-2, C-3,

C-4, C-5

C-3, C-6

P4. Account for securities with

significant influence.

4, 10, 11

C-11

C-11, C-12

C-4, C-5

C-4, C-6

*See additional information on next page that pertains to these quick studies, exercises and problems.

Additional Information on Related Assignment Material

Corresponding problems in set B (in text), also relate to learning objectives identified in grid on

previous page. The Serial Problem for Success Systems continues in this chapter. Problem C-1A, C-3A

can be completed with Sage 50 or QuickBooks

Connect reproduces assignments online, in static or algorithmic mode, which allows instructors to

monitor, promote, and assess student learning. It can be used for practice, homework, or exams.

Synopsis of Chapter Revisions

BANGS: NEW opener with new entrepreneurial assignment

New 3-step process for fair value adjustment

New learning note for investee vs investor securities

New Google example for learning comprehensive income

Updated return analysis using Gap

Chapter Outline

Notes

I. Basics of Investments

A. Motivation for Investments—three reasons:

1. Companies transfer excess cash to investments to produce

higher income.

2. Some entities, such as mutual funds and pension funds, are set

up to produce income from investments.

3. Strategic reasons. Examples: investments in competitors,

suppliers or customers.

B. Short-Term Investments

1. Cash equivalents are investments that are both readily

converted to known amounts of cash and mature within three

months.

2. Short-term investments (temporary investments or marketable

securities) -current assets that must meet these 2 requirements:

a. Intended to be converted into cash within one year or the

current operating cycle, whichever is longer.

b. Readily convertible to cash.

C. Long-Term Investments

1. Are not readily convertible to cash and not intended to be

converted to cash in short-term.

2. Can also include funds earmarked for special purpose funds or

investments in land or other assets not used in business

operations.

D. Investments in securities can include both debt and equity

securities.

1. Debt securities reflect a creditor relationship.

2. Equity securities reflect an owner relationship.

E. Classification and Reporting of Investments—accounting for

investments in securities depends on three factors:

1. Security type—either debt or equity.

2. Holding intention—either short term or long term.

3. Percentage of ownership.

E. Classifications of investments and reporting approach:

1. Trading securities (always short-term)—reported at fair value.

2. Held–to-maturity (debt securities)—reported at amortized cost

3. Available-for-sale (debt and non-influential equity

securities)—reported at fair value.

4. Significant influence (equity securities)—reported under

equity method.

5. Controlling influence (equity securities)—reported in

consolidated statements.

Chapter Outline

Notes

F. Accounting Basics for Investments

1. Debt Securities

a. Acquisition is recorded at cost (including any fees).

b. Interest revenue recorded when earned.

c. When the cost is greater than maturity value, the

difference is amortized over remaining life of security.

2. Equity Securities.

a. Acquisition is recorded at cost (including any fees).

b. Dividends received are recorded as dividend revenue and

reported on income statement.

c. At sale, proceeds are compared to cost and any gain or

loss is recorded.

II. Reporting of Noninfluential Investments—most must be reported at

fair value. Exact reporting depends on classification. The accounting

for each classification is as follows:

A. Trading (debt and equity –less than 20% of voting stock)—

intended to be actively managed and traded for profit.

1. Entire portfolio is reported at fair value.

2. Fair value adjustment from cost results in unrealized gain (or

loss) which is reported on the income statement.

3. Upon sales of individual securities, the difference between

their cost and net proceeds is recognized as gain or loss.

Subsequent fair value adjustments will exclude the sold

securities.

B. Held-to–Maturity Securities (HTM)—Debt securities a company

intends and is able to hold until maturity.

1. Classify as long-term investment when maturity date extends

beyond one year or the operating cycle, whichever is longer.

2. Record interest revenue when earned.

3. Amortize the difference between cost and maturity value over

the remaining life of the security. (Discussed in advance

course.)

4. Adjustments to fair value are not required.

Chapter Outline

Notes

C. Available-for-Sale Securities (AFS)—debt and equity (less than

20% of voting stock) securities that are not intended to be held to

maturity. Intent is to sell them in future.

1. Long vs. short-term classification depends on when they are

intended to be sold.

2. Entire portfolio is reported at fair value.

3. Unrealized gains or losses are not reported on income

statement. It is reported in equity section of the balance sheet

and is part of comprehensive income. (discussed later)

III. Reporting of Influential Investments

A. Equity Securities with Significant Influence.—Implies investor

can exert significant influence over the investee.

1. An investor who owns more than 20% (but not more than

50%) is presumed to have a significant influence over the

investee.

2. Equity method is used. Under this method the investor

a. records its share of the investee’s earnings as increase to

its investment and on its income statement.

b. reduces investment by share of losses and also reports

them on the income statement.

c. does not record cash dividends received as income (share

of investee’s income already reported) but instead that

dividend is viewed as a conversion of one asset to another

asset. (Cash increased and investment account decreased).

d. records and reports gain or loss when investment is sold.

Gain or loss is computed by comparing proceeds from sale

to book value of the investment on the date of sale.

B. Equity Securities with Controlling Influence—Investor is able to

exert a controlling influence over the investee (generally owns

more than 50% of a company’s voting stock).

1. The equity method with consolidation (subject for advanced

course) is used.

2. The controlling investor is called the parent company and the

investee company is called the subsidiary.

3. Investor also reports consolidated financial statements

(subject for advanced course) to the public when owning such

securities.

C. Summary of Accounting for Investments in Securities

See Exhibit C.8 (text p. 634).

Chapter Outline

Notes

D. Comprehensive Income—is defined as all changes in equity for a

period except those due to owner investments and dividends.

1. Includes: Unrealized gains and losses on AFS securities,

foreign currency adjustments and certain pension adjustments.

2. Can be reported in financial statements in one of two ways

(new FASB guidelines):

a. on a separate statement of comprehensive income that

immediately follows the income statement

b. On the lower section of the income statement (as a single

statement of income and comprehensive income).

IV. Global View—Compares U.S. GAAP to IFRS

A. Accounting for Noninfluential Securities—both systems are

broadly similar. Differences in terminology exist.

B. Accounting for Influential Securities—both systems are broadly

similar. Differences in terminology exist.

V. Decision Analysis—Components of Return on Total Assets

A. Assesses financial performance and can be separated into two

components:

1. Profit margin (net income divided by net sales) reflects the

percentage of net income in each dollar of net sales.

2. Total asset turnover (net sales divided by average total assets)

reflects a company’s ability to produce net sales from total

assets

B. Calculated as:

Net Income

Average total assets

Net Income

Net Sales xNet Sales

Average total assets

VI. Investments in International Operations—Appendix C-A

A. Exchange Rates Between Currencies

1. Price of one currency stated in terms of another currency is

called a foreign exchange rate.

2. These rates fluctuate due to changing economic and political

conditions (include the supply and demand for currencies and

expectations about future events).

B. Sales and Purchases Listed in a Foreign Currency

1. Companies making sales (or purchases) for which they receive

(or pay) foreign currency must translate the transaction

amounts into domestic currency. The transaction is recorded

using exchange rates on the date of the event.

2. Prior to statements, and/or at point of collection/payment,

adjustments to receivables/payables resulting from change in

exchange rates must be recorded. These adjustments result in

Foreign Exchange Gains/Losses.

Alternate Demonstration Problem

Appendix C

2015

Jan

1

Investor Corporation purchased 8,000 shares (20%) of Investee

Company’s outstanding stock at a cost of $150,000.

May

31

Investee Company declared and paid a cash dividend of $1.50 per

share.

Dec

31

Investee Company announced that its net income for the year was

$100,000.

2016

Oct

1

Investee Company declared and paid a cash dividend of $1.00 per

share.

Dec

31

Investee Company announced that its net income for the year was

$80,000.

2017

Jan

1

Investor Corporation sold all of its shares of Investee Company

for $178,000 cash.

Required:

1. Prepare journal entries on Investor Corporation’s books using the

equity method, which assumes that Investor has significant influence

over Investee Company.

2. Prepare journal entries on Investor Corporation’s books using the cost

method, which assumes that even though Investor owns 20% of

Investee’s stock, Investor does not have significant influence over

Investee (for example, another corporation owns 70% of Investee

Company’s stock).

Solution: Alternate Demonstration Problem

Appendix C

Part 1

2015

Jan

1

Long-Term Investment—Investee Stock ..

150,000

Cash ………………………………………………

150,000

May

31

Cash ……………………………………………………

12,000

Long-Term Investment—Investee Stock

12,000

Dec

31

Long-Term Investment—Investee Stock ..

20,000

Earnings from Long-Term Investment —Investee Stock

20,000

2016

Oct

1

Cash ……………………………………………………

8,000

Long-Term Investment—Investee Stock

8,000

Dec

31

Long-Term Investment—Investee Stock ..

16,000

Earnings from Long-Term Investment —Investee Company

16,000

2017

Jan

1

Cash ……………………………………………………

178,000

Long-Term Investment—Investee Stock

166,000

Gain on Sale of Investments …………..

12,000

Solution: Alternate Demonstration Problem

Appendix C

Part 2

2015

Jan

1

Long-Term Investment—Investee Stock ..

150,000

Cash ………………………………………………

150,000

May

31

Cash ……………………………………………………

12,000

Dividends Earned …………………………..

12,000

Dec

31

No entry

2016

Oct

1

Cash ……………………………………………………

8,000

Dividends Earned …………………………..

8,000

Dec

31

No entry

2017

Jan

1

Cash …………………………………………………….

178,000

Long-term Investment—Investee Stock

150,000

Gain on Sale of Investments ……………

28,000

Note that the total income statement effect is the same under both

methods:

Part 1:

$20,000

earnings in 2013

16,000

earnings in 2014

12,000

gain on sale in 2015

$48,000

Part 2:

$12,000

dividends in 2013

8,000

dividends in 2014

28,000

gain on sale in 2015

$48,000