Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Exercise 9-17 (concluded)

(b)

Aug 31

Salaries (or Wages) Expense ................................

10,020.00

FICA—Social Sec. Taxes Payable ....................

298.84

FICA—Medicare Taxes Payable ........................

145.29

Employee Fed. Inc. Taxes Payable ...................

2,380.00

Employee State Inc. Taxes Payable .................

388.00

Employee Benefits Plan Payable ......................

501.00

Salaries Payable .................................................

6,306.87

To record payroll for period.

Aug 31

Salaries (or Wages) Payable ................................

6,306.87

Cash ................................................................

6,306.87

To record payment of payroll.

(d)

Aug 31

Payroll Taxes Expense ............................................

530.53

FICA⎯Social Sec. Taxes Payable ....................

298.84

FICA⎯Medicare Taxes Payable ........................

145.29

Federal Unemployment Taxes Payable ...........

8.64

State Unemployment Taxes Payable................

77.76

To record employer payroll taxes.

Aug 31

Employee Benefits Expense ................................

1,002.00

Employee Benefits Plan Payable ......................

1,002.00

To record costs of employee benefits.

(e)

Aug 31

FICA⎯Social Security Taxes Payable....................

597.68

FICA⎯Medicare Taxes Payable ..............................

290.58

Employee Fed. Income Taxes Payable. .................

2,380.00

Employee State Income Taxes Payable. ................

388.00

Employee Benefits Plan Payable ............................

1,503.00

Federal Unemployment Taxes Payable..................

8.64

State Unemployment Taxes Payable ......................

77.76

Cash ................................................................

5,245.66

To record payment of FICA, income taxes,

SUTA, FUTA, and benefit plan contributions.

Exercise 9-18 (25 minutes)

(in SEK millions)

1.

Warranty Expense ...................................................

7,706

Estimated Warranty Liability ............................

7,706

To record warranty expense and liability.

2.

Estimated Warranty Liability ..................................

6,677

Inventory.............................................................

6,677

To record cost of warranty replacements.

PROBLEM SET A

Problem 9-1A (45 minutes)

Locust

Natl. Bank

Fargo

1.

Maturity dates

Date of the note ..............................

May 19

July 8

Nov. 28

Term of the note (in days) .............

90

120

60

Maturity date ................................

Aug. 17

Nov. 5

Jan. 27

2.

Interest due at maturity

Principal of the note ......................

$35,000

$80,000

$42,000

Annual interest rate .......................

10%

9%

8%

Fraction of year ..............................

90/360

120/360

60/360

Interest expense.............................

$ 875

$ 2,400

$ 560

3.

Accrued interest on Fargo note at the end of 2014

Total interest for note ....................................................

$ 560

Fraction of term in 2014 ................................................

33/60

Accrued interest expense .............................................

$ 308

4.

Interest on Fargo note in 2015

Total interest for note ....................................................

$ 560

Fraction of term in 2015 ................................................

27/60

Interest expense in 2015 ...............................................

$ 252

Problem 9-1A (Concluded)

5.

2014

Apr. 20

Merchandise Inventory ...........................................

40,250

Accounts Payable—Locust ..............................

40,250

Purchased merchandise on credit.

May 19

Accounts Payable—Locust ....................................

40,250

Cash ....................................................................

5,250

Notes Payable—Locust .....................................

35,000

Paid $5,250 cash and gave a 90-day,

10% note to extend due date on account.

July 8

Cash ..........................................................................

80,000

Notes Payable—National ..................................

80,000

Borrowed cash with a 120-day, 9% note.

Aug. 17

Interest Expense ......................................................

875

Notes Payable—Locust ...........................................

35,000

Cash ....................................................................

35,875

Paid note with interest.

Nov. 5

Interest Expense ......................................................

2,400

Notes Payable—National Bank ..............................

80,000

Cash ....................................................................

82,400

Paid note with interest.

Problem 9-2A (25 minutes)

Part 1

Jan. 8

Office Salaries Expense ..........................................

22,760.00

Sales Salaries Expense ...........................................

65,840.00

FICA—Social Sec. Taxes Payable* ..................

5,493.20

FICA—Medicare Taxes Payable** ....................

1,284.70

Employee Fed. Inc. Taxes Payable ..................

12,860.00

Employee Medical Insurance Payable .............

1,340.00

Employee Union Dues Payable ........................

840.00

Salaries Payable ................................................

66,782.10

To record payroll for period.

* $88,600 x 6.2%

** $88,600 x 1.45%

Part 2

Jan. 8

Payroll Taxes Expense ............................................

10,853.50

FICA—Social Sec. Taxes Payable ....................

5,493.20

FICA—Medicare Taxes Payable .......................

1,284.70

State Unemployment Taxes Payable* ..............

3,544.00

Federal Unemployment Taxes Payable** ...........

531.60

To record employer payroll taxes.

* $88,600 x .04 = $3,544.00

**$88,600 x .006 = $531.60

Problem 9-3A (60 minutes)

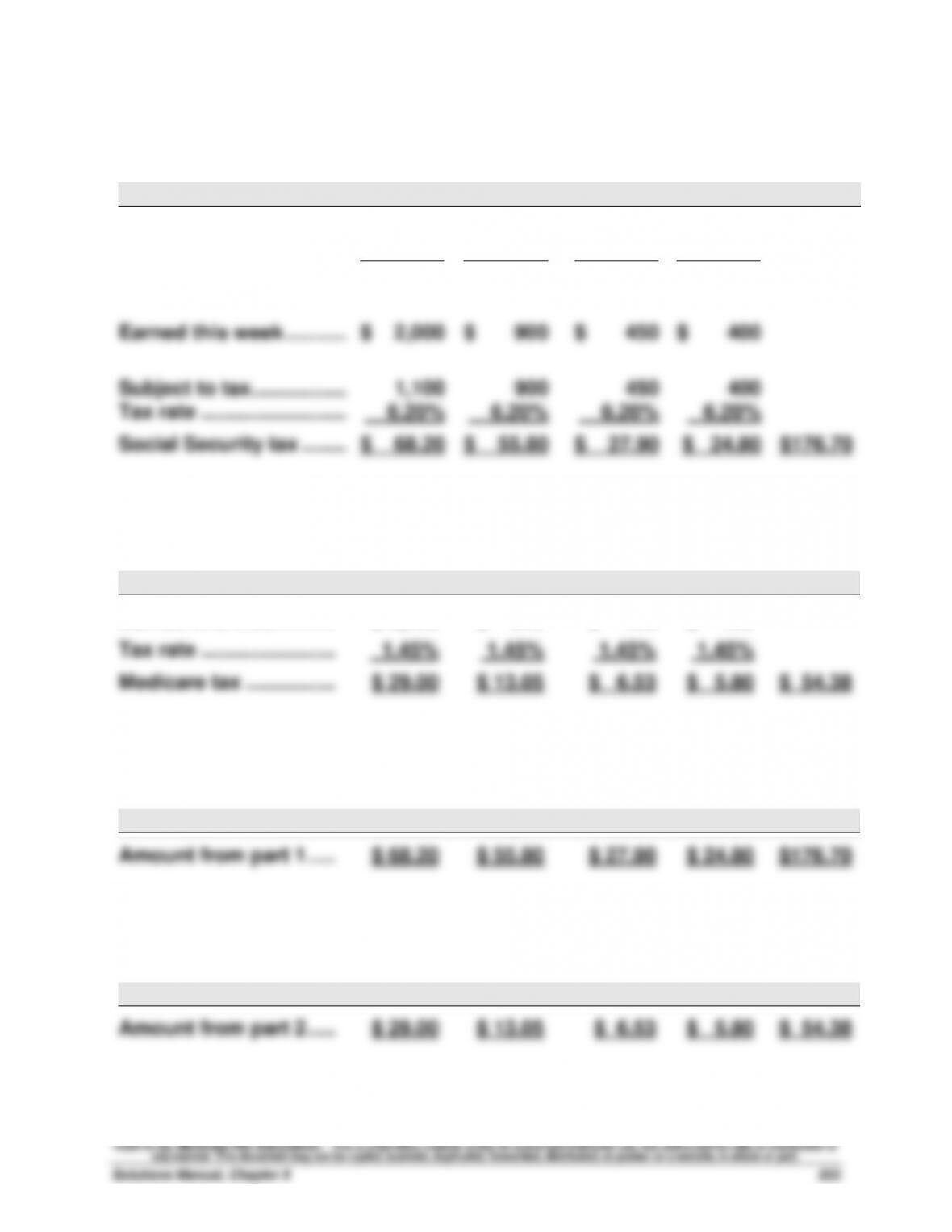

1. Each employee’s FICA withholdings for Social Security

Dahlia

Trey

Kiesha

Chee

Total

Maximum base ..............

$117,000

$117,000

$117,000

$117,000

Earned through 8/18 .....

115,900

116,100

7,100

1,050

Yet under maximum ......

$ 1,100

$ 900

$109,900

$115,950

Earned this week ...........

$ 2,000

$ 900

$ 450

$ 400

Subject to tax .................

1,100

900

450

400

Tax rate ..........................

6.20%

6.20%

6.20%

6.20%

Social Security tax ........

$ 68.20

$ 55.80

$ 27.90

$ 24.80

$176.70

2. Each employee’s FICA withholdings for Medicare (no limits)

Dahlia

Trey

Kiesha

Chee

Total

Earned this week .........

$ 2,000

$ 900

$ 450

$ 400

Tax rate ........................

1.45%

1.45%

1.45%

1.45%

Medicare tax ................

$ 29.00

$ 13.05

$ 6.53

$ 5.80

$ 54.38

3. Employer’s FICA taxes for Social Security

Dahlia

Trey

Kiesha

Chee

Total

Amount from part 1 .....

$ 68.20

$ 55.80

$ 27.90

$ 24.80

$176.70

4. Employer’s FICA taxes for Medicare

Dahlia

Trey

Kiesha

Chee

Total

Amount from part 2 .....

$ 29.00

$ 13.05

$ 6.53

$ 5.80

$ 54.38

Problem 9-3A (Concluded)

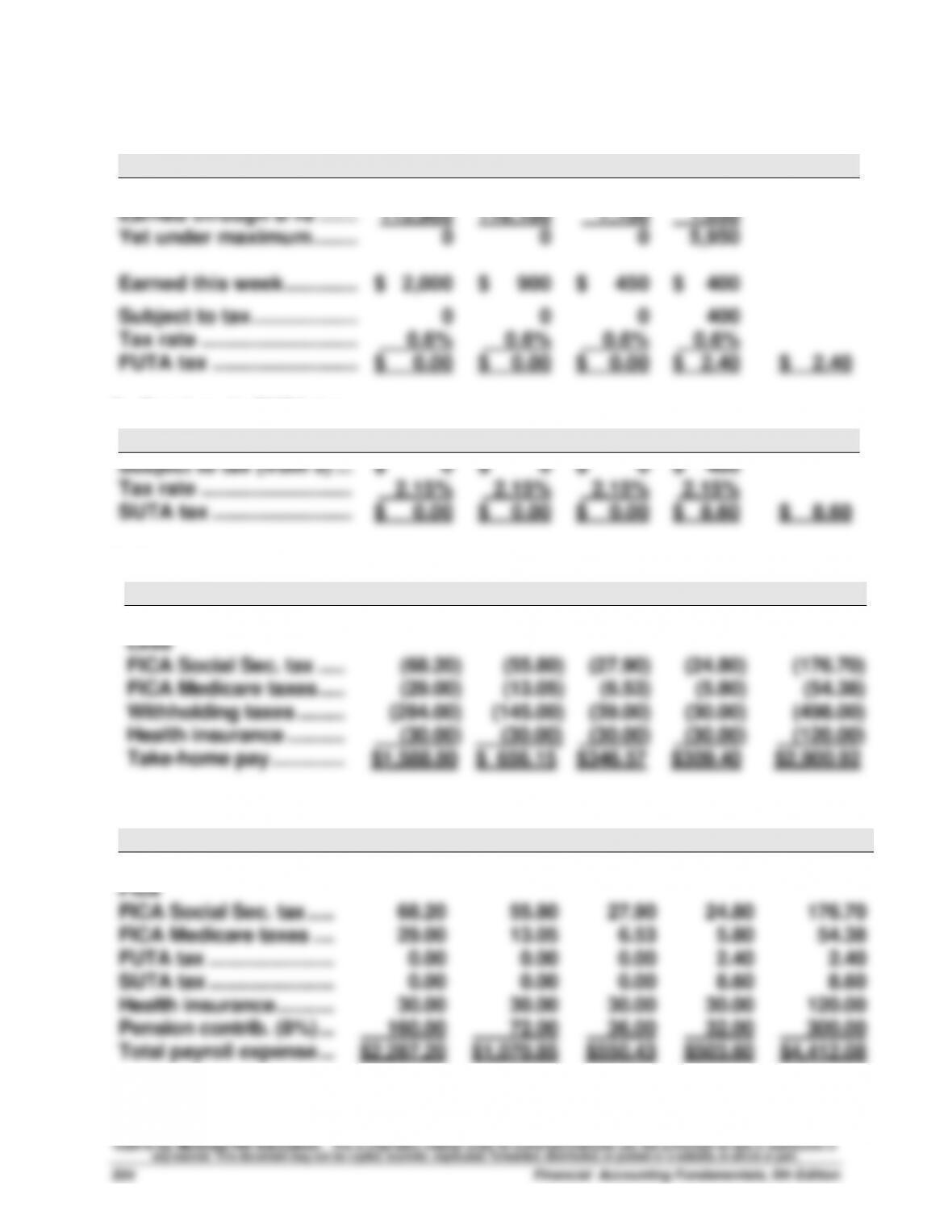

5. Employer’s FUTA taxes

Dahlia

Trey

Kiesha

Chee

Total

Maximum base .................

$ 7,000

$ 7,000

$ 7,000

$ 7,000

Earned through 8/18 ........

115,900

116,100

7,100

1,050

Yet under maximum .........

0

0

0

5,950

Earned this week ..............

$ 2,000

$ 900

$ 450

$ 400

Subject to tax ....................

0

0

0

400

Tax rate .............................

0.6%

0.6%

0.6%

0.6%

FUTA tax ...........................

$ 0.00

$ 0.00

$ 0.00

$ 2.40

$ 2.40

6. Employer’s SUTA taxes

Dahlia

Trey

Kiesha

Chee

Total

Subject to tax (from 5) ...

$ 0

$ 0

$ 0

$ 400

Tax rate ...........................

2.15%

2.15%

2.15%

2.15%

SUTA tax .........................

$ 0.00

$ 0.00

$ 0.00

$ 8.60

$ 8.60

7. Each employee’s net (take-home) pay

Dahlia

Trey

Kiesha

Chee

Total

Gross earnings ..............

$2,000.00

$ 900.00

$450.00

$400.00

$3,750.00

Less

FICA Social Sec. tax .....

(68.20)

(55.80)

(27.90)

(24.80)

(176.70)

FICA Medicare taxes .....

(29.00)

(13.05)

(6.53)

(5.80)

(54.38)

Withholding taxes .........

(284.00)

(145.00)

(39.00)

(30.00)

(498.00)

Health insurance ...........

(30.00)

(30.00)

(30.00)

(30.00)

(120.00)

Take-home pay ..............

$1,588.80

$ 656.15

$346.57

$309.40

$2,900.92

8. Employer’s total payroll-related expense for each employee

Dahlia

Trey

Kiesha

Chee

Total

Gross earnings ...............

$2,000.00

$ 900.00

$450.00

$400.00

$3,750.00

Plus

FICA Social Sec. tax .......

68.20

55.80

27.90

24.80

176.70

FICA Medicare taxes ......

29.00

13.05

6.53

5.80

54.38

FUTA tax ..........................

0.00

0.00

0.00

2.40

2.40

SUTA tax ..........................

0.00

0.00

0.00

8.60

8.60

Health insurance .............

30.00

30.00

30.00

30.00

120.00

Pension contrib. (8%) .....

160.00

72.00

36.00

32.00

300.00

Total payroll expense .....

$2,287.20

$1,070.85

$550.43

$503.60

$4,412.08

Problem 9-4A (40 minutes)

1.

2014

Nov. 11

Cash ..........................................................................

7,875

Sales ...................................................................

7,875

Sold razors to customers.

11

Cost of Goods Sold .................................................

2,100

Merchandise Inventory .....................................

2,100

To record cost of November 11 sale (105 x $20).

30

Warranty Expense ...................................................

630

Estimated Warranty Liability ............................

630

To record razor warranty expense

and liability at 8% of selling price.

Problem 9-4A (Concluded)

2015

Jan. 5

Cash ..........................................................................

11,250

Sales ...................................................................

11,250

Sold razors to customers.

5

Cost of Goods Sold .................................................

3,000

Merchandise Inventory .....................................

3,000

To record cost of January 5 sale (150 x $20).

17

Estimated Warranty Liability ..................................

1,000

Merchandise Inventory .....................................

1,000

To record cost of razor warranty

replacements (50 x $20).

31

Warranty Expense ...................................................

900

Estimated Warranty Liability ............................

900

To record razor warranty expense

and liability at 8% of selling price.

2. Warranty expense for November 2014 and December 2014

Sales

Percent

Warranty Expense

November .................

$ 7,875

8%

$ 630

December ..................

16,500

8

1,320

Total ..........................

$24,375

$1,950

3. Warranty expense for January 2015

Sales in January ..............................

$11,250

Warranty percent .............................

8%

Warranty expense ...........................

$ 900

4. Balance of the estimated liability as of December 31, 2014

Warranty expense for November ....................................

$ 630

credit

Warranty expense for December ....................................

1,320

credit

Cost of replacing items in December (45 x $20) ...........

(900)

debit

Estimated Warranty Liability balance ............................

$1,050

credit

5. Balance of the estimated liability as of January 31, 2015

Beginning balance ..........................................................

$1,050

credit

Warranty expense for January ......................................

900

credit

Cost of replacing items in January (50 x $20) ..............

(1,000)

debit

Estimated Warranty Liability balance ...........................

$ 950

credit

Problem 9-5A (60 minutes)

1. Miller Company

2. Weaver Company

3. Sales increase by 30% (multiply prior sales by 1.3)

Miller Co.

Weaver Co.

Sales .............................................

$1,300,000

$1,300,000

Variable expenses ......................

1,040,000

780,000

Income before interest ...............

260,000

520,000

Interest expense (fixed) ..............

60,000

260,000

Net income ...................................

$ 200,000

$ 260,000

Net income increases by* ..........

43%

86%

* Computed as the increase in net income divided by prior net income.

4. Sales increase by 50% (multiply prior sales by 1.5)

Miller Co.

Weaver Co.

Sales .............................................

$1,500,000

$1,500,000

Variable expenses ......................

1,200,000

900,000

Income before interest ...............

300,000

600,000

Interest expense (fixed) ..............

60,000

260,000

Net income ...................................

$ 240,000

$ 340,000

Net income increases by ............

71%

143%

5. Sales increase by 80% (multiply prior sales by 1.8)

Miller Co.

Weaver Co.

Sales .............................................

$1,800,000

$1,800,000

Variable expenses ......................

1,440,000

1,080,000

Income before interest ...............

360,000

720,000

Interest expense (fixed) ..............

60,000

260,000

Net income ...................................

$ 300,000

$ 460,000

Net income increases by ............

114%

229%

Problem 9-5A (Continued)

6. Sales decrease by 10% (multiply prior sales by 0.9)

Miller Co.

Weaver Co.

Sales ........................................

$900,000

$900,000

Variable expenses .................

720,000

540,000

Income before interest ..........

180,000

360,000

Interest expense (fixed) .........

60,000

260,000

Net income ..............................

$120,000

$100,000

Net income decreases by ......

-14%

-29%

7. Sales decrease by 20% (multiply prior sales by 0.8)

Miller Co.

Weaver Co.

Sales ........................................

$800,000

$800,000

Variable expenses .................

640,000

480,000

Income before interest ..........

160,000

320,000

Interest expense (fixed) .........

60,000

260,000

Net income ..............................

$100,000

$ 60,000

Net income decreases by ......

-29%

-57%

8. Sales decrease by 40% (multiply prior sales by 0.6)

Miller Co.

Weaver Co.

Sales ........................................

$600,000

$600,000

Variable expenses .................

480,000

360,000

Income before interest ..........

120,000

240,000

Interest expense (fixed) .........

60,000

260,000

Net income ..............................

$ 60,000

$ (20,000)

Net income decreases by ......

-57%

-114%

9. The higher fixed cost strategy (having more fixed interest expense) of

Weaver Co. accentuates the effects of increases and decreases in sales.

That is, increases in sales produce greater increases in net income and

Problem 9-6AA (50 minutes)

Mar. 15

FICA⎯Social Security Taxes Payable ...................

3,472

FICA⎯Medicare Taxes Payable .............................

812

Employee Fed. Income Taxes Payable. .................

4,000

Cash ................................................................

8,284

To record payment of FICA & federal income taxes.

31

Office Salaries Expense ..........................................

11,200

Shop Salaries Expense ...........................................

16,800

FICA⎯Social Sec. Taxes Payable ....................

1,736

FICA⎯Medicare Taxes Payable .......................

406

Employee Fed. Income Taxes Payable ............

4,000

Salaries Payable ................................................

21,858

To record payroll for the period.

31

Salaries Payable ......................................................

21,858

Cash ................................................................

21,858

To record payment of payroll.*

*Check numbers are likely entered in the Payroll Register.

31

Payroll Taxes Expense* ...........................................

2,786

FICA⎯Social Sec. Taxes Payable ....................

1,736

FICA⎯Medicare Taxes Payable .......................

406

State Unemployment Taxes Payable ...............

560

Federal Unemployment Taxes Payable ...........

84

To record employer payroll taxes.

*Amount earned through 2/28 = 2 x $2,800 = $5,600

Subject to SUTA/FUTA in March = $7,000 - $5,600 = $1,400

SUTA = $1,400 x 10 employees x 4.0% = $560

FUTA = $1,400 x 10 employees x 0.6% = $84

FICA⎯Social Security Taxes = $1,736 (same as employees)

FICA⎯Medicare Taxes = $406 (same as employees)

Problem 9-6AA (Concluded)

Apr. 15

FICA⎯Social Security Taxes Payable ...................

3,472

FICA⎯Medicare Taxes Payable .............................

812

Employee Fed. Income Taxes Payable ..................

4,000

Cash ................................................................

8,284

To record payment of FICA & federal income taxes.

15

State Unemployment Taxes Payable .....................

2,800

Cash ................................................................

2,800

To record payment of SUTA taxes [$2,240 + $560].

30

Federal Unemployment Taxes Payable .................

420

Cash ................................................................

420

To record payment of FUTA taxes [$336 + $84].

30

No entry required upon mailing Form 941.

PROBLEM SET B

Problem 9-1B (45 minutes)

Fox

Products

Spring

Bank

City

Bank

1.

Maturity dates

Date of the note ................................

May 23

July 15

Dec. 6

Term of the note (in days) ...............

60

120

45

Maturity date ................................

July 22

Nov. 12

Jan. 20

2.

Interest due at maturity

Principal of the note .........................

$4,600

$12,000

$8,000

Annual interest rate .........................

15%

10%

9%

Fraction of year ................................

60/360

120/360

45/360

Interest expense ...............................

$ 115

$ 400

$ 90

3.

Accrued interest on City Bank note at the end of 2014

Total interest for note ................................................................

$ 90

Fraction of term in 2014 .............................................................

25/45

Accrued interest expense .........................................................

$ 50

4. Interest in 2015

Total interest for note ................................................................

$ 90

Fraction of term in 2015 .............................................................

20/45

Interest expense in 2015............................................................

$ 40

Problem 9-1B (Concluded)

5.

2014

Apr. 22

Merchandise Inventory ...........................................

5,000

Accounts Payable⎯Fox Products ...................

5,000

Purchased merchandise on credit.

May 23

Accounts Payable⎯Fox Products .........................

5,000

Cash ....................................................................

400

Notes Payable⎯Fox Products .........................

4,600

Paid $400 cash and gave a 60-day,

15% note to extend due date on account.

July 15

Cash ..........................................................................

12,000

Notes Payable⎯Spring Bank ...........................

12,000

Borrowed cash with a 120-day, 10% note.

22

Interest Expense ......................................................

115

Notes Payable⎯Fox Products ...............................

4,600

Cash ....................................................................

4,715

Paid note with interest.

Nov. 12

Interest Expense ......................................................

400

Notes Payable⎯Spring Bank .................................

12,000

Cash ....................................................................

12,400

Paid note with interest.

Dec. 6

Cash ..........................................................................

8,000

Notes Payable⎯City Bank ................................

8,000

Borrowed cash with a 45-day, 9% note.