Chapter 9

Accounting for Current Liabilities

QUESTIONS

1. A current liability is expected to be paid within one year or the company’s operating

cycle, whichever is longer. Any liability that is not current is considered to be long

term.

5. The combined Social Security tax rate (assuming the maximum wage amount is not

6. The Medicare tax rate is 1.45%. This rate is applied to all wages earned by an

employee—no maximum limit exists.

7. The employee is responsible for federal income taxes, state income taxes, local

8. An employee’s gross earnings along with the number of withholding allowances that

9. An unemployment merit rating is based on an evaluation of an employer’s

experience in creating or avoiding unemployment with its employees. The merit

10. The obligation to correct or replace defective products (or services) is created when

the products are sold with the warranties. Even though the seller does not know

11. There are no conditions in which a probable loss tied to a future event can create a

12.A A wage bracket withholding table shows for a pay period of a given length (weekly,

13.A Single employee earning $725 with two allowances has $76 taxes withheld.

Single employee earning $625 with no allowances has $81 taxes withheld.

15. At December 31, 2013, Google reports the following accrued expenses:

16. At December 31, 2013, Samsung reports nine current liabilities: Trade and other

17. Samsung’s current liabilities include one income-tax-related liability titled: Income

tax payable. This account reflects taxes that must be paid to the government in the

QUICK STUDIES

Quick Study 9-1 (5 minutes)

Items 1, 4, 5 and 6 are current liabilities for this company.

Quick Study 9-2 (10 minutes)

Sept. 30

Cash ………………………………………………………..………

6,300

Sales ………………………………………………….……

6,000

Sales Taxes Payable …………………………..

300

To record cash sales and 5% sales tax.

Sept. 30

Cost of Goods Sold ………………………………….………

3,900

Merchandise Inventory ……………………….….

3,900

To record cost of Sept. 30 sales.

Oct. 15

Sales Taxes Payable ………………………………..………

300

Cash …………………………………………………..…..

300

To record remittance of sales taxes to govt.

Quick Study 9-3 (10 minutes)

Oct. 31

Cash ………………………………………………………..………

5,000,000

Unearned Ticket Revenue …………………………..

5,000,000

To record sales in advance of concerts.

Nov. 5

Unearned Ticket Revenue …………………………..

1,250,000

Earned Ticket Revenue ……………………….….

1,250,000

To record concert revenues earned.

Quick Study 9-4 (15 minutes)

1. Computation of interest payable at December 31, 2015:

Days from November 7 to December 31 ………………..

54 days

Accrued interest (8% x $160,000 x 54/360) …………….

$1,920

2. 2015

Dec.31

Interest Expense ……………………………………………...

1,920

Interest Payable ………………………………………...

1,920

To record accrued interest (8% x $160,000 x 54/360).

3. 2016

Feb. 5

Interest Expense …………………………………………..….

1,280

Interest Payable ……………………………………………….

1,920

Notes Payable ………………………………………………….

160,000

Cash ……………………………………………………….

163,200

To record payment of note plus interest

(8% x $160,000 x 90/360 = 3,200).

Quick Study 9-5 (15 minutes)

Jan. 15

Sales Salaries Expense …………………………………….

35,000.00

FICA—Social Sec. Taxes Payable* …………..….

2,170.00

FICA—Medicare Taxes Payable** …………….….

507.50

Employee Fed. Inc. Taxes Payable …………..….

6,500.00

Employee Medical Insurance Payable ………….

772.50

Employee Union Dues Payable ………………..….

120.00

Salaries Payable ……………………………………..….

24,930.00

To record payroll for period.

* $35,000 x 6.2%

** $35,000 x 1.45%

Quick Study 9-6 (15 minutes)

[Note: Two months (January and February) of earnings have

already been recorded for each of the 10 employees.]

Mar. 31

Payroll Taxes Expense ……………………………………..

2,730.00

FICA—Social Security Taxes Payable1 ………...

1,240.00

FICA—Medicare Taxes Payable2 …………………..

290.00

State Unemployment Taxes Payable3 …………..

1,080.00

Federal Unemployment Taxes Payable4 ……….

120.00

To record employer payroll taxes.

1(10 x $2,000) x 6.2% = $1,240.00

2(10 x $2,000) x 1.45% = $290.00

3(10 x $2,000 [check $2,000 under max: $7,000 – {$2,000 x 2}]) x 5.4% = $1,080.00

4(10 x $2,000 [check $2,000 under max: $7,000 – {$2,000 x 2}]) x 0.6% = $120.00

Quick Study 9-7 (5 minutes)

Dec. 31

Employee Bonus Expense ………………………………..

15,000

Bonus Payable ………………………………………....

15,000

To record expected bonus costs.

Quick Study 9-8 (5 minutes)

Vacation Benefits Expense* ……………………………..

500

Vacation Benefits Payable ………………………...

500

To record vacation benefits accrued.

* ($6,500-6,000)

Quick Study 9-9 (10 minutes)

2014

Sep 11

Cash ………………………………………………………………..

500

Sales …………………………………………………………..

500

To record mower sales.

Sep 11

Warranty Expense …………………………………………...

40

Estimated Warranty Liability ………………………..

40

To record estimated warranty expense.

2015

July 24

Estimated Warranty Liability …………………………..

35

Repair Parts Inventory ………………………………...

35

To record cost of warranty repairs.

Quick Study 9-10 (10 minutes)

1. (b); reason—is reasonably estimated but not a probable loss.

2. (b); reason—probable loss but cannot be reasonably estimated.

3. (a); reason—can be reasonably estimated and loss is probable.

Quick Study 9-11 (10 minutes)

Quick Study 9-12A (15 minutes)

Gross Pay ………………………………………………………………….

$740.00

Social Security tax deduction (6.2%) ………………………...

$45.88

Medicare tax deduction (1.45%) ………………………………..

10.73

Federal income tax deduction (from Exhibit 9A.6) ……..

96.00

State income tax deduction (1.0%) …………………………..

7.40

Total deductions ……………………………………………………...

160.01

Net Pay ……………………………………………………………………...

$579.99

Quick Study 9-13B (10 minutes)

Dec. 31

Income Taxes Expense …………………………………....

40,000

Income Taxes Payable ………………………………..

34,000

Deferred Income Tax Liability ……………………..

6,000

To record tax expense and deferred tax liability.

Quick Study 9-14 (10 minutes)

a. The definitions and characteristics of current liabilities are broadly

$1,885,000

EXERCISES

Exercise 9-1 (10 minutes)

1.

L

3.

L

5.

C

7.

N

9.

C

2.

C

4.

C

6.

C

8.

C

10.

C

Exercise 9-2 (10 minutes)

[Note: All entries dated December 31, 2015]

1.

Cash ………………………………………………………………..

10,400

Sales …………………………………………………………..

10,000

Sales Taxes Payable ……………………………………

400

To record sales and sales taxes.

Cost of Goods Sold …………………………………………..

5,000

Merchandise Inventory ………………………………..

5,000

To record cost of sales.

2.

Unearned Services Revenue ……………………………..

50,000

Earned Services Revenue …………………………...

50,000

To record revenue earned.

Exercise 9-3 (30 minutes)

1. Maturity date = May 15 + 60 days = July 14, 2015

2a.

May 15

Cash ………………………………………………………………..

110,000

Notes Payable …………………………………………....

110,000

Borrowed cash by issuing an interest-bearing note.

2b.

July 14

Interest Expense* …………………………………………....

2,200

Notes Payable ………………………………………………....

110,000

Cash …………………………………………………………..

112,200

Repaid note plus interest.

* Principal …………………….…….

$110,000

x Interest rate ……………..……..

12%

x Fraction of year ……….……..

60/360

Total interest ……………………..

$ 2,200

Exercise 9-4 (30 minutes)

1. Maturity date = November 1 + 90 days = January 30, 2016.

2.

Principal ……………………………………………..

$200,000

x Interest rate ……………………………………...

9%

x Fraction of year (Nov. 1 – Dec. 31)……..

60/360

Total interest in 2015 …………………………..

$ 3,000

3.

Principal ……………………………………………..

$200,000

x Interest rate ……………………………………...

9%

x Fraction of year (Jan. 1 – Jan. 30)……...

30/360

Total interest in 2016 …………………………..

$ 1,500

4a.

2015

Nov. 1

Cash ………………………………………………………………..

200,000

Notes Payable …………………………………………....

200,000

Borrowed cash by issuing an interest-bearing note.

4b.

2015

Dec. 31

Interest Expense ……………………………………………...

3,000

Interest Payable ………………………………………....

3,000

Accrued interest on note payable.

4c.

2016

Jan. 30

Interest Expense ……………………………………………...

1,500

Interest Payable ……………………………………………....

3,000

Notes Payable ………………………………………………....

200,000

Cash …………………………………………………………..

204,500

Repaid note plus interest.

Exercise 9-5 (20 minutes)

Subject

to Tax

Rate

Tax

Explanation

a.

FICA—Social Security ……

$ 800

6.20%

$ 49.60

Full amount is subject to tax.

FICA—Medicare ……………

800

1.45

11.60

Full amount is subject to tax.

FUTA ……………………………..

600

0.60

3.60

$200 is over the maximum.

SUTA …………………………….

600

2.90

17.40

$200 is over the maximum.

b.

FICA—Social Security ……

$2,100

6.20%

$130.20

Full amount is subject to tax.

FICA—Medicare ……………

2,100

1.45

30.45

Full amount is subject to tax.

FUTA ……………………………..

0

0.60

0.00

Full amount is over maximum.

SUTA …………………………….

0

2.90

0.00

Full amount is over maximum.

c.

FICA—Social Security ……

$6,300

6.20%

$390.60

$1,700 is over the maximum.

FICA—Medicare ……………

8,000

1.45

116.00

Full amount is subject to tax.

FUTA ……………………………..

0

0.60

0.00

Full amount is over maximum.

SUTA …………………………….

0

2.90

0.00

Full amount is over maximum.

Exercise 9-6 (10 minutes)

Sept. 30

Salaries Expense ……………………………………………..

800.00

FICA—Social Security Taxes Payable ………….

49.60

FICA—Medicare Taxes Payable …………………..

11.60

Employee Federal Income Taxes Payable ……...

80.00

Salaries Payable ………………………………………...

658.80

To record payroll for pay period ended September 30.

Exercise 9-7 (10 minutes)

Sept. 30

Payroll Taxes Expense ……………………………………..

82.20

FICA—Social Security Taxes Payable ………....

49.60

FICA—Medicare Taxes Payable …………………..

11.60

Federal Unemployment Taxes Payable ………..

3.60

State Unemployment Taxes Payable …………...

17.40

To record employer payroll taxes.

Exercise 9-8 (30 minutes)

1. July 31

Sales Salaries Expense ………………………………..…..

200,000

Office Salaries Expense ……………………………….…..

160,000

FICA—Social Sec. Taxes Payable ………………..

22,320

FICA—Medicare Taxes Payable ……………….…..

5,220

Employee Fed. Inc. Taxes Payable …………..…..

90,000

Employee State Inc. Taxes Payable ……………..

20,000

Employee Medical Insurance Payable* …….…..

2,800

Employee Life Insurance Payable** ……………..

1,600

Employee Union Dues Payable ………………..…..

1,000

Salaries Payable ……………………………………..…..

217,060

To record payroll for period.

* $7,000 x 40% ** $4,000 x 40%

2. July 31

Salaries Payable …………………………………………..…..

217,060

Cash ……………………………………………………….

217,060

To record payment of payroll.*

*Check numbers may be entered in the Payroll Register.

3. July 31

Payroll Taxes Expense ……………………………………..

30,540

FICA⎯Social Sec. Taxes Payable ………………..

22,320

FICA⎯Medicare Taxes Payable ……………….…..

5,220

State Unemployment Taxes Payable………..…..

2,700

Federal Unemployment Taxes Payable ………..

300

To record employer payroll taxes.

SUTA = $50,000 x 5.4% = $2,700

FUTA = $50,000 x 0.6% = $300

FICA—Social Sec. & Medicare = Same as employees

July 31

Employee Benefits Expense …………………………..

6,600

Employee Medical Insurance Payable* …….…..

4,200

Employee Life Insurance Payable** ……………..

2,400

To record costs of employee benefits.

* $7,000 x 60% ** $4,000 x 60%

4. July 31

FICA⎯Social Security Taxes Payable………………..

44,640

FICA⎯Medicare Taxes Payable …………………….…..

10,440

Employee Fed. Income Taxes Payable. ……………..

90,000

Employee State Income Taxes Payable. ………..…..

20,000

Employee Medical Insurance Payable …………..…..

7,000

Employee Life Insurance Payable ……………………..

4,000

Employee Union Dues Payable ……………………..…..

1,000

State Unemployment Taxes Payable ……………..…..

2,700

Federal Unemployment Taxes Payable………….…..

300

Cash ……………………………………………………….

180,080

To record payment of FICA, income taxes, SUTA,

FUTA, union dues, and insurance premiums.

Exercise 9-9 (30 minutes)

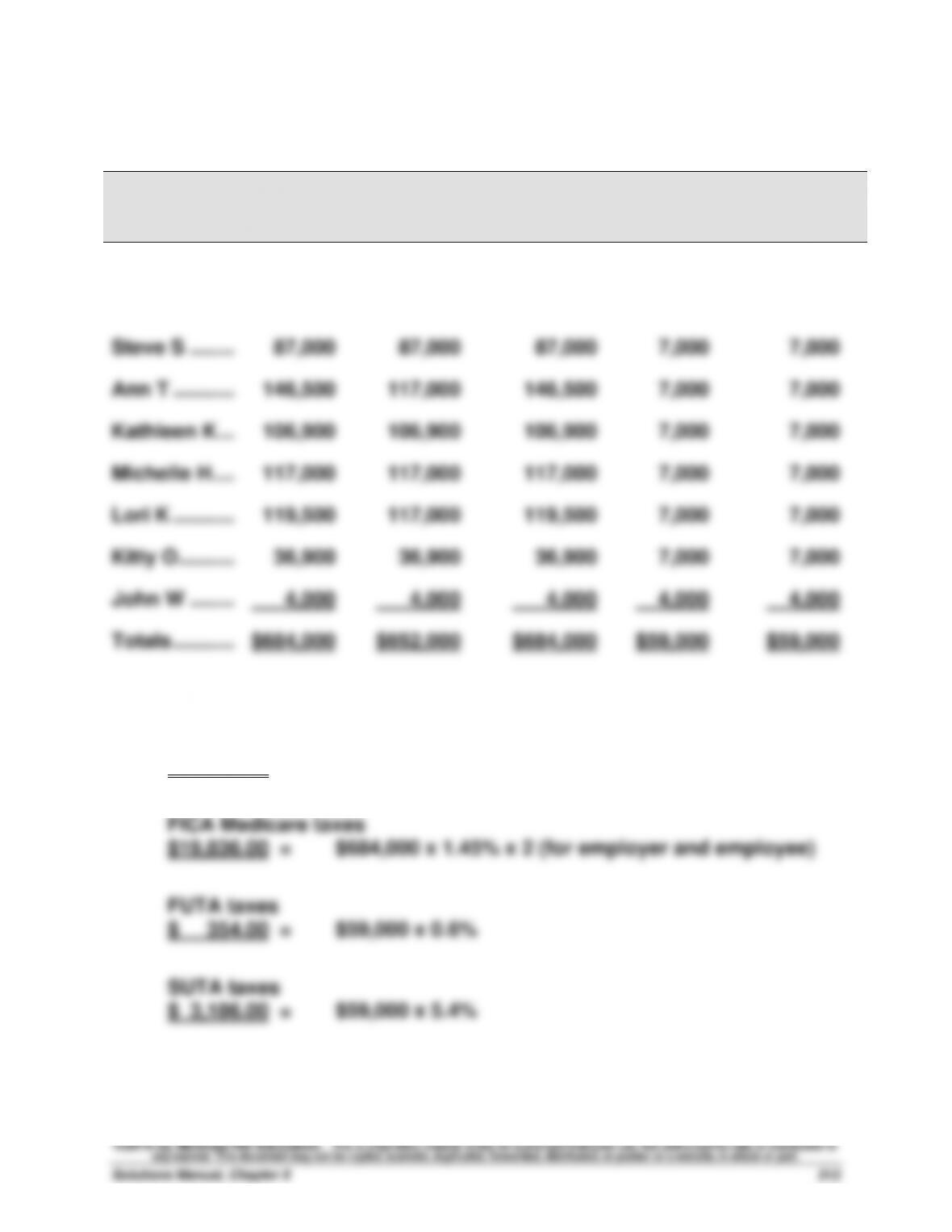

a.

Employee

Cumulative

Pay

Pay Subject to

FICA Social

Security

Pay Subject

to FICA

Medicare

Pay Subject

to FUTA

Taxes

Pay Subject

to SUTA

Taxes

Ken S ………..……..

$ 6,000

$ 6,000

$ 6,000

$ 6,000

$ 6,000

Tim V ………………..

60,200

60,200

60,200

7,000

7,000

Steve S ……..……..

87,000

87,000

87,000

7,000

7,000

Ann T ………..……..

146,500

117,000

146,500

7,000

7,000

Kathleen K ………..

106,900

106,900

106,900

7,000

7,000

Michelle H ….……..

117,000

117,000

117,000

7,000

7,000

Lori K ………..……..

119,500

117,000

119,500

7,000

7,000

Kitty O ……….……..

36,900

36,900

36,900

7,000

7,000

John W ……..……..

4,000

4,000

4,000

4,000

4,000

Totals ………..……..

$684,000

$652,000

$684,000

$59,000

$59,000

b. FICA Social Security taxes

$80,848.00 = $652,000 x 6.2% x 2 (for employer and employee)

©2016 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in

any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in whole or part.

Financial Accounting Fundamentals, 5th Edition

514

Exercise 9-10 (25 minutes)

1. Warranty Expense = 4% of dollar sales = 4% x $6,000 = $240

2. The December 31, 2015, balance of the liability equals the expense

3. The company should report no additional warranty expense in 2016 for

this copier.

4. The December 31, 2016, balance of the Estimated Warranty Liability

account equals the 2016 beginning balance minus the costs incurred in

Less parts cost …………………………..

5. Journal entries

2015

(a)

Aug. 16

Cash ………………………………………………………………..

6,000

Sales ………………………………………………………….

6,000

To record cash sale of copier.

Aug. 16

Cost of Goods Sold ………………………………………….

4,800

Merchandise Inventory ……………………………….

4,800

To record cost of August 16 sale.

(b)

Dec. 31

Warranty Expense …………………………………………...

240

Estimated Warranty Liability ……………………….

240

To record warranty expense for copier sold in 2015.

2016

(c)

Nov. 22

Estimated Warranty Liability …………………………….

209

Repair Parts Inventory ………………………………..

209

To record cost of warranty repairs.

Exercise 9-11 (15 minutes)

1. B = 0.03 ($500,000 – B)

B = $15,000 – 0.03B

1.03B = $15,000

B = $14,563 (rounded to nearest dollar)

2.

3.

2016

Exercise 9-12 (10 minutes)

[Note: All entries dated December 31, 2015.]

1.

Vacation Benefits Expense …………………………………....

3,200

Vacation Benefits Payable ………………………………..

3,200

To record vacation benefits expense

[20 employees x 1 day x $160].

2.

Warranty Expense………………………………………………....

18,000

Estimated Warranty Liability …………………………..

18,000

To record warranty expense [12,000 units x 10% x $15].

Exercise 9-13 (10 minutes)

[Note: All entries dated December 31, 2015.]

1. No adjusting entry is required since it is not probable that the supplier will

2. No adjusting entry can be made since the loss cannot be reasonably

Exercise 9-14 (15 minutes)

(a)

(b)

(c)

(d)

(e)

(f)

Numerator

Income before

interest & taxes ….

$194,000

$176,000

$182,000

$379,000

$103,000

$ 5,000

Denominator

Interest expense …...

$ 44,000

$ 16,000

$ 12,000

$ 14,000

$ 14,000

$10,000

Ratio ………………….

4.41

11.00

15.17

27.07

7.36

0.50

Analysis: Company (d) has the strongest ability to pay interest expense as it

comes due as evidenced by the company’s times interest earned (coverage)

ratio of 27.07 times.

Exercise 9-15B (25 minutes)

1.

Income Taxes Payable (target balance) ……………………………….……….

$28,300

Total accrued [($28,600 + $19,100 + $34,600) x .30] ……………………….

24,690

Adjustment (additional expense) ………………………………………………….

$ 3,610

2.

2015

(a)

Dec. 31

Income Tax Expense …………………………………………

3,610

Income Taxes Payable …………………………………

3,610

To adjust tax expense and liability.

2016

(b)

Jan. 20

Income Taxes Payable ………………………………………

28,300

Cash ……………………………………………………………

28,300

To make the final quarterly payment

of income taxes for 2015.

Exercise 9-16A (15 minutes)

Regular pay (40 hours @ $14) …………………………………....

$560.00

Overtime premium pay (8 hours @ [$14 x 150%]) ………..

168.00

Gross pay ……………………………………………………….……....

728.00

FICA—Social Security tax deduction (6.2%) ………………..

$ 45.14

FICA—Medicare tax deduction (1.45%) ……………………....

10.56

Income tax deduction (from Exhibit 9A.6) …………………...

76.00

Total deductions ……………………………………………………...

131.70

Net pay ……………………………………………………………………...

$596.30

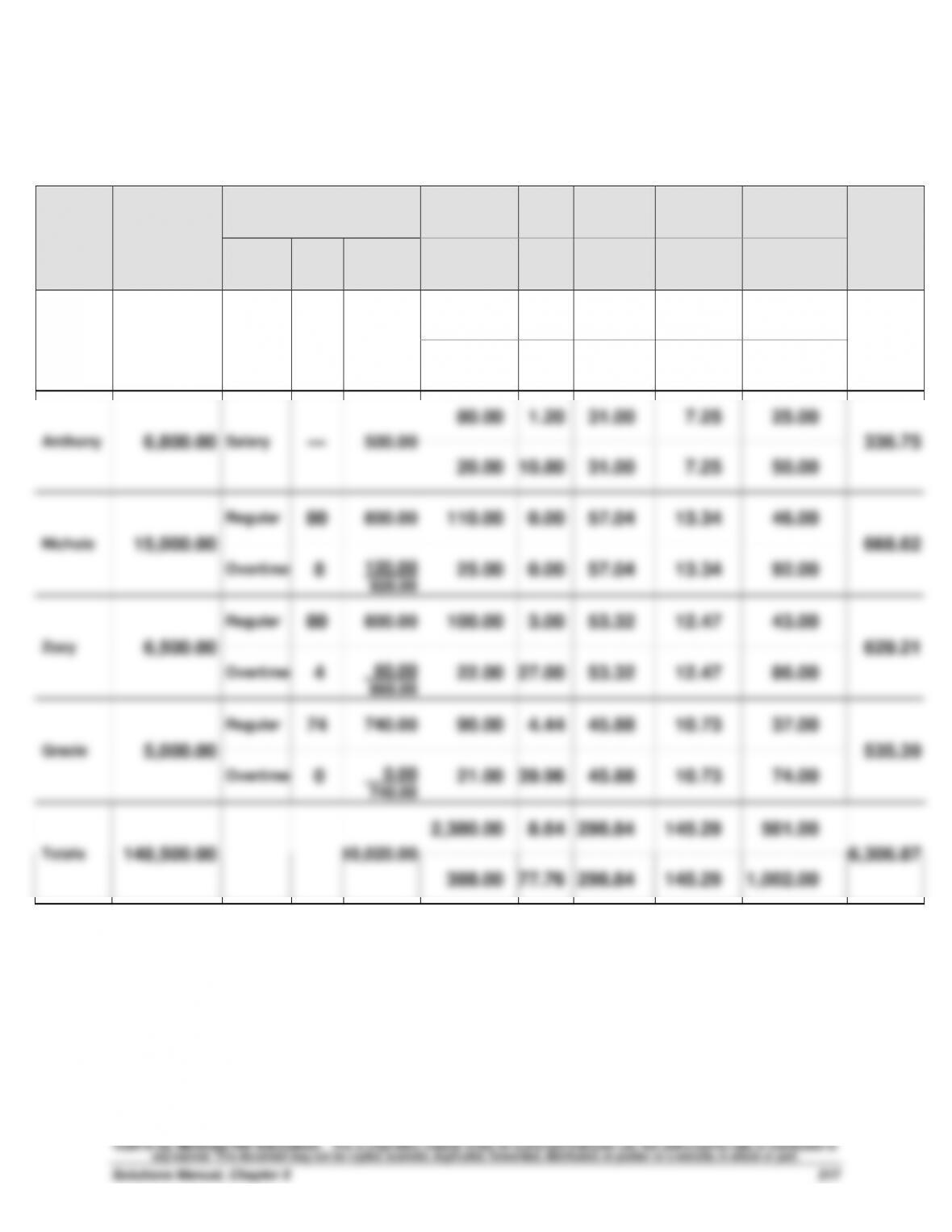

Exercise 9-17 (30 minutes)

(a)

Employee

Cumulative

Pay (Excludes

Current Period)

Current Period Gross Pay

FIT

Withholding

FUTA

FICA S.S.

Employee

FICA

Medicare

Employee

Employee—

Benefits Plan

Withholding

Employee

Net Pay

Pay

Type

Pay

Hours

Gross Pay

SIT

Withholding

SUTA

FICA S.S.

Employer

FICA

Medicare

Employer

Employer—

Benefits Plan

Expense

Kathleen

115,200.00

Salary

—

7,000.00

2,000.00

0.00

111.60

101.50

350.00

4,136.90

300.00

0.00

111.60

101.50

700.00

Anthony

6,800.00

Salary

—

500.00

80.00

1.20

31.00

7.25

25.00

336.75

20.00

10.80

31.00

7.25

50.00

Nichole

15,000.00

Regular

80

800.00

110.00

0.00

57.04

13.34

46.00

668.62

Overtime

8

120.00

920.00

25.00

0.00

57.04

13.34

92.00

Zoey

6,500.00

Regular

80

800.00

100.00

3.00

53.32

12.47

43.00

629.21

Overtime

4

60.00

860.00

22.00

27.00

53.32

12.47

86.00

Gracie

5,000.00

Regular

74

740.00

90.00

4.44

45.88

10.73

37.00

535.39

Overtime

0

0.00

740.00

21.00

39.96

45.88

10.73

74.00

Totals

148,500.00

10,020.00

2,380.00

8.64

298.84

145.29

501.00

6,306.87

388.00

77.76

298.84

145.29

1,002.00