Problem 8-4B (50 minutes)

2014

Jan. 1

Equipment …………………………………………………………..

27,670

Cash ……………………………………………………………...

27,670

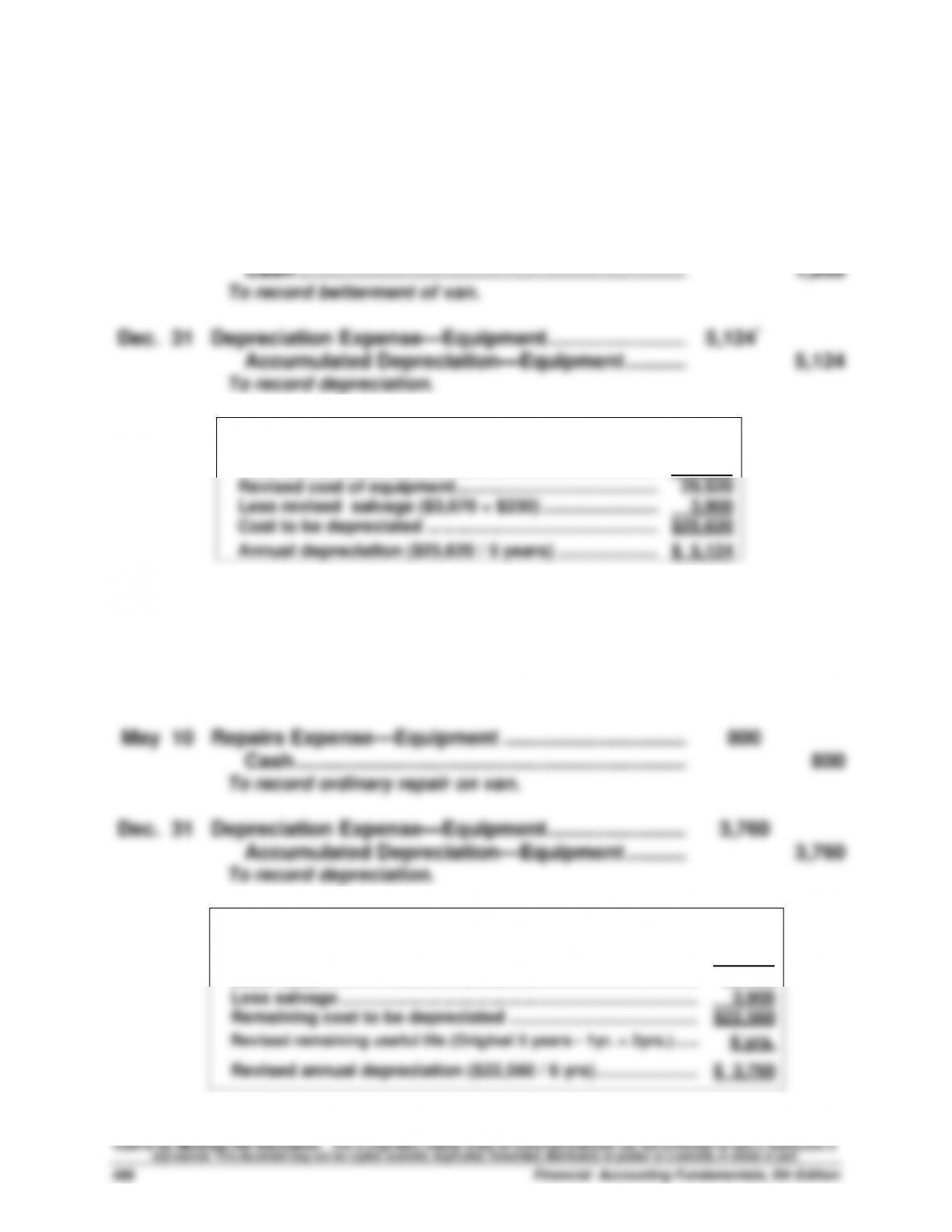

To record costs of van ($25,860 + $1,810).

Jan. 3

Equipment …………………………………………………………..

1,850

Cash ……………………………………………………………...

1,850

To record betterment of van.

5,124

To record depreciation.

Jan. 1

Equipment …………………………………………………………..

2,064

Cash ……………………………………………………………...

2,064

To record extraordinary repair on van.

Cash ……………………………………………………………...

To record ordinary repair on van.

3,760

Problem 8-5B (40 minutes)

2014

Jan. 1

Machinery ……………………………………………………….

114,270

Cash ………………………………………………………….…..

114,270

To record costs of machinery ($107,800 +$6,470).

Problem 8-6B (20 minutes)

1.

Jan. 1

Machinery ………………………………………………………...

150,000

Cash …………………………………………………………...

150,000

To record machinery costs.

Jan. 2

Machinery ………………………………………………………...

3,510

Cash …………………………………………………………...

3,510

To record machinery costs.

Jan. 4

Machinery ………………………………………………………...

4,600

Cash …………………………………………………………...

4,600

To record machinery costs.

2. a. First year

Dec. 31

Depreciation Expense—Machinery ……………………….

20,000

Accumulated Depreciation—Machinery ……….….

20,000

To record depreciation [($158,110-$18,110)/7 = $20,000].

b. Sixth year

Dec. 31

Depreciation Expense—Machinery ……………………….

20,000

Accumulated Depreciation—Machinery ……….….

20,000

To record the sixth year’s depreciation.

3. Accumulated depreciation at the date of disposal

First six years’ depreciation (6 x $20,000) ………………...

$120,000

Book value at the date of disposal

Original total cost …………………………………………………...

$158,110

Accumulated depreciation ……………………………………....

(120,000)

Total ……………………………………………………………………....

$ 38,110

a. Sold for $28,000 cash

Dec. 31

Cash ……………………………………………………………….…..

28,000

Loss on Sale of Machinery …………………………………..

10,110

Accumulated Depreciation—Machinery ………………..

120,000

Machinery ………………………………………………….…..

158,110

Dec. 31

Cash ……………………………………………………………….…..

52,000

Accumulated Depreciation—Machinery ………………..

120,000

Machinery ………………………………………………….…..

158,110

Gain on Sale of Machinery …………………………..

13,890

Dec. 31

Cash ……………………………………………………………….…..

25,000

Loss from Fire ……………………………………………………..

13,110

Accumulated Depreciation—Machinery ………………..

120,000

Problem 8-7B (20 minutes)

a.

Feb. 19

Mineral Deposit ………………………………………….………..

5,400,000

Cash …………………………………………………….…

5,400,000

To record purchase of mineral deposit.

b.

Mar. 21

Machinery ………………………………………………….……

400,000

Cash …………………………………………………….…

400,000

To record costs of machinery.

c.

Dec. 31

Depletion Expense—Mineral Deposit ………….………..

342,900

Accum. Depletion—Mineral Deposit ………………..

342,900

To record depletion [$5,400,000/

4,000,000 tons = $1.35 per ton.

254,000 tons x $1.35 = $342,900].

d.

Dec. 31

Depreciation Expense—Machinery ……………..………..

25,400

Accum. Depreciation—Machinery …………………..

25,400

To record depreciation [$400,000/

4,000,000 tons = $0.10 per ton.

254,000 tons x $0.10 = $25,400].

Analysis Component

Similarities—Amortization, depletion, and depreciation are similar in that

Problem 8-8B (20 minutes)

1.

2015

(a)

Jan. 1

Leasehold ……………………………………………………….

40,000

Cash ………………………………………………………….…..

40,000

To record payment for sublease.

(b)

Jan. 1

Prepaid Rent……………………………………………………….

36,000

Cash ………………………………………………………….…..

36,000

To record prepaid annual lease rental.

(c)

Jan. 3

Leasehold Improvements ………………………………..…..

20,000

Cash ………………………………………………………….…..

20,000

To record costs of leasehold improvements.

2.

2015

(a)

Dec. 31

Rent Expense ………………………………………………….…..

8,000

Accumulated Amortization—Leasehold …………..

8,000

To record leasehold amortization ($40,000/5).

(b)

Dec. 31

Amortization Expense—Leasehold Improvements ….…..

4,000

Accumulated Amortization—Leasehold

Improvements …………………………………………………..

4,000

To record leasehold improvement amortization

($20,000/5 years remaining on lease).

(c)

Dec. 31

Rent Expense ………………………………………………….…..

36,000

Prepaid Rent ……………………………………………..…..

36,000

To record annual lease rental.

Serial Problem — SP 8

Serial Problem — SP 8, Business Solutions (45 minutes)

1. For the three months ended March 31, 2016, depreciation expense was

$400 for office equipment and $1,250 for the computer equipment.

2.

December 31,

2015

December 31,

2016

Office Equipment …………………………….……

$ 8,000

$ 8,000

Accumulated Depreciation–Office

Equipment ………………………………….……

400

2,000

Office Equipment (book value) ………..……

$ 7,600

$ 6,000

$20,000

$20,000

Accumulated Depreciation–

$13,750

Reporting in Action — BTN 8-1

1. The percent of original cost remaining to be depreciated is computed

by taking the ratio of the book value of property and equipment to the

original cost ($ millions):

2. In Apple’s “Summary of Significant Accounting Policies” (Note 1:

Property, Plant and Equipment) it discloses estimated useful lives by

major asset category as follows:

Asset Life (in years)

3. The change in total property and equipment before accumulated

depreciation for the year ended September 28, 2013, is an increase of

4. Total asset turnover for year ended ($ millions):

5. Solution depends on the financial statement data obtained.

Comparative Analysis — BTN 8-2

Note: Total asset turnover = Net sales / Average total assets

1. Total asset turnover for Apple ($ millions)

2. Each dollar of Apple’s assets produces $0.89 and $1.07 in net sales for

the current and prior year, respectively. Each dollar of Google’s assets

Ethics Challenge — BTN 8-3

1. When managers acquire new assets a number of decisions relative to

2. When assets are placed in use on a day other than the first day of the

month an assumption is often made that the assets are placed in use on

the first day of the month nearest to the date of the purchase. For

example, for assets purchased on the 1st through 15th days of the month,

3. By always assuming the first day of the following month as the date of

purchase, less depreciation is (initially) accrued for the assets

Communicating in Practice — BTN 8-4

The solution to this activity will vary based on the industry and the

companies chosen for analysis. Many instructors find it useful to report

the results from the teams to the class for purposes of classroom

discussion and analysis.

Taking It to the Net — BTN 8-5

1. Yahoo! has Goodwill in the amount of ($ thousands) $4,679,648 at

2.

Goodwill (in $ thousands)

Total

Amount

$ Change

from Prior

Year

%

Change

Balance, December 31, 2012 ……………..…

$3,826,749

Balance, December 31, 2013 ……………..…

$4,679,648

$852,899

22.3%

Goodwill has increased over this period. The increase is due mainly to

new goodwill recorded due to acquisitions in 2013 and, secondly, to

Foreign Currency Translation Adjustments that Yahoo! has experienced

over this period. There was also a goodwill impairment.

3. Yahoo!’s intangible assets are categorized into the three categories

below at December 31, 2013. These intangibles represent 2.5%

4. Note 6 indicates that Trade names, trademarks, and domain names

have original estimated useful lives of “one year to an indefinite life.” If

Teamwork in Action — BTN 8-6

1. Annual depreciation for each year of the asset’s useful life:

Year

Straight-line

Double-Declining-Balance

Units-of-Production

2013

($44,000-$2,000)/4

= $10,500

(100%/4) x 2 = 50% is

declining-balance rate.

BV x rate = $44,000 x 50%

= $22,000

($44,000-$2,000)/60,000 miles

= $.70 per mile.

12,000 miles x $.70 = $ 8,400

2014

$10,500

$22,000 x 50%= $11,000

18,000 miles x $.70 = $12,600

2015

$10,500

$11,000 x 50% = $5,500

21,000 miles x $.70 = $14,700

2016

$10,500

$5,500 (depreciate to

salvage) = $3,500

9,000* miles x $.70 = $ 6,300

* Depreciation is based on the estimated capacity of 60,000 miles. Even though the van is

driven 10,000 miles in the last year, depreciation can only be taken for the remaining 9,000

miles of estimated capacity. This will record depreciation to the estimated salvage value.

2. Depreciation is recorded in an adjusting entry at the end of each

period. The entry is:

3. Each expert’s presentation of the comparison of methods will be

slightly different. The experts should make the following points: The

Teamwork in Action — BTN 8-6 – continued

4. Book value at the end of each year

= Cost – Accumulated depreciation

= $44,000 – (amount varies by method—see part 1 for annual amounts)

Year

Straight–line

Double-Declining-

Balance

Units of Production

2013 ……..

$33,500

$22,000

$35,600

2014 ……..

23,000

11,000

23,000

2015 ……..

12,500

5,500

8,300

2016 ……..

2,000

2,000

2,000

For reporting purposes, each expert will have different results. But

each should show:

Plant Assets:

Entrepreneurial Decision — BTN 8-7

Part 1

(a) Under current conditions, the total asset turnover is 3.2. This is

(b) Under this proposal, its asset turnover would increase to 4. This is

computed by taking its net sales of $12,000,000 ($8,000,000 +

Part 2

The proposal would yield an improved total asset turnover of 4 vis-à-vis the

current total asset turnover of 3.2. However, we need to recognize that this

proposal depends on our confidence in both maintaining current sales,

*We must remember that total asset turnover is only one dimension of a complete analysis of this

proposal. For example, we would want to explore the impact of this proposal on net income and

other activities.

Average total assets

Hitting the Road — BTN 8-8

No formal solution exists for this activity. It is usually interesting for the

class to exchange their discoveries via class discussion. This is

particularly the case with respect to patents, copyrights, and trademarks.

Global Decision — BTN 8-9

Note: Total asset turnover = Net sales / Average total assets

1. Total asset turnover for Samsung (KRW in millions):

2. Samsung was more efficient in using its assets to generate net sales

than Google and Apple. Specifically, in the current year, each KRW